Asymptotic analysis for a simple explicit estimator in Barndorff-Nielsen and Shephard stochastic volatility models††thanks: We thank Ole Barndorff-Nielsen, Michael Sørensen, Bent Nielsen and Søren Johansen for helpful comments. We thank Mathieu Kessler for making his PhD-thesis available to us. Financial support from the Austrian Science Fund (FWF) under grant P15889 is gratefully acknowledged.

Abstract

We provide a simple explicit estimator for discretely observed Barndorff-Nielsen and Shephard models, prove rigorously consistency and asymptotic normality based on the single assumption that all moments of the stationary distribution of the variance process are finite, and give explicit expressions for the asymptotic covariance matrix.

We develop in detail the martingale estimating function approach for a bivariate model, that is not a diffusion, but admits jumps. We do not use ergodicity arguments.

We assume that both, logarithmic returns and instantaneous variance are observed on a discrete grid of fixed width, and the observation horizon tends to infinity. As the instantaneous variance is not observable in practice, our results cannot be applied immediately. Our purpose is to provide a theoretical analysis as a starting point and benchmark for further developments concerning optimal martingale estimating functions, and for theoretical and empirical investigations, that replace the variance process with a substitute, such as number or volume of trades or implied variance from option data.

KEYWORDS:

Martingale estimating functions, stochastic volatility models with jumps, consistency and asymptotic normality

1 Introduction

In [BNS01] Barndorff-Nielsen and Shephard introduced a class of stochastic volatility models in continuous time, where the instantaneous variance follows an Ornstein-Uhlenbeck type process driven by an increasing Lévy process. Those models allow flexible modelling, capture many stylized facts of financial time series, and yet are of great analytical tractability. For further information see also [BNNS02]. BNS-models, as we will call them from now on, are affine models in the sense of [DPS00] and [DFS03], where the associated Riccati type equations can be solved up to quadrature in general. In several concrete cases the integration can be performed explicitly in closed form in terms of elementary functions, see [NV03] and [Ven01].

BNS-models have been studied from various points of view in mathematical finance and related fields. In [NV03] option pricing and structure preserving martingale measures are studied. In [BK05, BMB05, BG05, RS06] the minimal entropy martingale measure is investigated. The papers [BKR03, Lin06] address the portfolio optimization problem. Bayesian/MCMC/computer intensive estimation is already in the seminal paper [BNS01], and in the works [RPD04, GS01, FSS01, tH03]. The papers [Jam05, Jam06] exploit the analytical tractability to develop maximum likelihood estimation using the results of [CM00, CR90] for Dirichlet processes. BNS models are also treated in the textbooks [CT04, Sch03].

Unfortunately, it seems that statistical estimation of the model is the most difficult problem, and most of the work in that area is focused on computationally intensive methods.

The contributions of the present paper are as follows: first we develop a simple and explicit estimator for BNS models. Secondly, we give rigorous proofs of its consistency and asymptotic normality. In doing so we compute explicitly the asymptotic covariance matrix and develop to that purpose formulas for arbitrary bivariate integer moments of returns and variance. Thirdly we provide a detailed application of the theory of martingale estimating functions in a non-diffusion setting, including numerical illustrations.

The literature on estimation for discretely observed diffusions is vast, a few references are [Uch04b, Uch04a, DS04, MR03, KP02, Jac02, Jac01, Sør01, BS01, Kes00, KS99a, Sør97, BS95]. In particular, the martingale estimating function approach is used, developed and studied for example in [Sø99], [Sø00], [Sø97]. In the diffusion setting the major difficulty is that the transition probabilities are not known and are difficult to compute. In contrast to that, the characteristic function of the transition probability is known in closed form for many BNS models and the transition probability can be computed with Fourier methods with high precision. Yet the model exhibits other peculiarities, see the remarks in section 2.3.

In the present paper we explore the joint distribution of logarithmic returns and the instantaneous variance supposing that both processes can be observed in discrete time. Since the joint conditional moment-generating function of is known in closed form we obtain closed form expressions for the joint conditional moments up to any desired order which yields a sequence of martingale differences. We employ then the large sample properties, in particular the strong law of large numbers for martingales and martingale central limit theorem. In this way we do not need ergodicity, mixing conditions, etc.111Let us mention though, that the martingale strong law and the ergodic theorem have similar proofs and can be derived from a common source, [Rao73].

The remainder of the paper is organized as follows: in section 2.1 we describe the class of BNS models in continuous time and present two concrete examples, the OU and IG-OU model. In section 2.2 we introduce the quantities observed in discrete time that are used for estimation. Section 2.3 contains some remarks of particular features of the model and its estimation. In section 3 we present the estimating equations, their explicit solution which is our estimator and prove its consistency and asymptotic normality. In section 4 we present numerical illustrations. In section 5 we sketch further and alternative developments, in particular considering the issue that volatility is typically not observed in discrete time. Explicit moment calculations of any order can be found in Appendix A. In Appendix B we provide for the reader’s convenience a simple multivariate martingale central limit theorem.

2 The model

2.1 The continuous time model

2.1.1 The general setting

As in Barndorff-Nielsen and Shepard [BNS01], we assume that the price process of an asset is defined on some filtered probability space and is given by with a constant. The process of logarithmic returns and the instantaneous variance process satisfy

| (1) |

and

| (2) |

where the parameters and are real constants with The process is a standard Brownian motion, the process is an increasing Lévy process, and we define for notational simplicity. Adopting the terminology introduced by Barndorff-Nielsen and Shepard, we will refer to as the background driving Lévy process (BDLP). The Brownian motion and the BDLP are independent and is assumed to be the usual augmentation of the filtration generated by the pair . The random variable has a self-decomposable distribution corresponding to the BDLP such that the process is strictly stationary and

| (3) |

To shorten the notation we introduce the parameter vector

| (4) |

and the bivariate process

| (5) |

If the distribution of is from a particular class then is called a BNS-DOU() model.

The process is clearly Markovian.

2.1.2 The -OU model

The -OU model is obtained by constructing the BNS-model with stationary gamma distribution, , where the parameters are and . The corresponding background driving Lévy process is a compound Poisson processes with intensity and jumps from the exponential distribution with parameter . Consequently both processes and have a finite number of jumps in any finite time interval.

For the -OU model it is more convenient to work with the parameters and . The connection to the generic parameters used in our general development is given by

| (6) |

As the gamma distribution admits exponential moments we have integer moments of all orders and our Assumption 1 below is satisfied.

2.1.3 The IG-OU model

The IG-OU model is obtained by constructing the BNS-model with stationary inverse Gaussian distribution, , with parameters and .

The corresponding background driving Lévy process is the sum of an IG( process and an independent compound Poisson process with intensity and jumps from an distribution. Consequently both processes and have infinitely many jumps in any finite time interval.

For the IG-OU model it is more convenient to work with the parameters and . The connection to the generic parameters used in our general development is given by

| (7) |

As the inverse Gaussian distribution admits exponential moments we have integer moments of all orders and our Assumption 1 below is satisfied.

2.2 Discrete observations

We observe returns and the variance process on a discrete grid of points in time,

| (8) |

This implies

| (9) |

Using

| (10) |

we have that is a sequence of independent random variables, and it is independent of . If the grid is equidistant, then are iid. Observing the returns on the grid we have

| (11) |

where

is the integrated variance process. This suggests introducing the discrete time quantities

| (12) |

and

| (13) |

Furthermore, it is also convenient to introduce the discrete quantity

| (14) |

It is not difficult to see (conditioning!) that is an iid sequence independent from all other discrete quantities. We note also that is a bivariate iid sequence, but and are obviously dependent.

From now on, for notational simplicity, we consider the equidistant grid with

| (15) |

where is fixed. This implies

| (16) |

and

| (17) |

where

| (18) |

Furthermore,

| (19) |

The sequence is clearly Markovian. From now on we assume all moments of the stationary distribution of exist.

Assumption 1

| (20) |

In the estimating context we assume all moments are finite with respect to all probability measures under consideration, where is the parameter space.

No other assumptions are made, and all conditions required for consistency and asymptotic normality of our estimator will be proven rigorously from that assumption.

Proposition 1

We have for all that

| (21) |

and

| (22) |

Consequently the expectation of any (multivariate) polynomial in exists under .

Proof: We will use repeatedly the well-known relation between the existence of moments and the differentiability of the characteristic function of a random variable, see [CT97, Theorem 8.4.1, p.295f], for example.

Let denote the characteristic function of . By assumption for all . Thus is arbitrarily many times differentiable. The law of is self-decomposable, thus infinitely divisible and for all . Thus the Fourier cumulant function is arbitrarily many times differentiable. It follows from [BNS01, equation (12)], that the characteristic function of is . Thus is arbitrarily many times differentiable and consequently , for all . As is a Lévy process this implies , and as we have shown , for all .

From (10) and (14) we have and so and for all . As has a standard normal distribution it follows trivially for all . Repeated application of the binomial resp. multinomial theorem, the Hölder and the Cauchy-Schwarz inequalities yields and for all , and the final conclusion for polynomials.

Let us remark that, by the stationarity, the above result holds also for instead of , where is arbitrary.

2.3 Some remarks

Most work on estimating functions is developed for diffusions, see for example [Sø97, Uch04b, Uch04a, DS04, MR03, KP02, Jac02, Jac01, Sør01, BS01, Kes00, KS99a, Sør97, BS95], although it is often remarked that the results extend to Markov chains. Yet the models under consideration here display several peculiarities.

One assumption that is usually made is that the transition probabilities under have the same support for each Typically the support of the conditional distribution of in a BNS model given is under , thus depends on . This does not affect our analysis. The experiment is not homogeneous, cf.[Str85].

If the BDLP is a compound Poisson process, as in the OU case, we have the atom of the conditional distribution of given under at the parameter dependent position . Consequently no dominating measure exists and maximum likelihood cannot be defined in the usual way. There is an alternative definition covering that case, cf. [KW56, Joh78], but we have not exploited that direction further. See also [NS03]. This problem does not appear with an infinite activity BDLP such as in the IG-OU model and standard maximum likelihood estimation could be studied.

The description given in sections 2.1 and 2.2 provides a BNS model for each , but not a statistical experiment as it is taken as a starting point in section 3. The reason is that the processes and will depend on . This can be avoided by introducing a statistical experiment generated by a BNS model. In analogy to the statistical experiment generated by a diffusion, see [SS00]. This means we take the distribution of and on the Skorohod space under each as a starting point.

3 The simple explicit estimator

3.1 The simple estimating equations and their explicit solution

For estimation purposes we consider a probability space on which a parameterized family of probability measures is given:

| (23) |

where . The data is generated under the true probability measure with some . The expectation with respect to is denoted by and with respect to simply by .

We assume there is a process that is BNS-DOU() under . We want to find an estimator for using observations . We are interested in asymptotics as . To that purpose let us consider the following martingale estimating functions:

| (24) |

Lemma 1

We have the explicit expressions

| (25) |

Proof: The formulas are special cases of the general moment calculations given in Appendix A. In order to demonstrate the basic idea we will prove the statements for two special and simple cases here, namely for and . From (16) it follows that

| (26) |

and from the stationarity of we have

| (27) |

Furthermore, from (19) and the fact that it follows that

| (28) |

But, from (17) we have that

| (29) |

and

| (30) |

So, from (28) it follows that

| (31) |

The estimator is obtained by solving the estimating equation and it turns out that this equation has a simple explicit solution.

Proposition 2

The estimating equation admits for every on the event

| (32) |

a unique solution that is given by

| (33) |

where

| (34) |

and

| (35) |

Proof: The first three equations , for contain only the unknowns and are easily solved. In fact we get a familiar estimator for the first two moments and the autocorrelation coefficient of an AR(1) process. The last three equations , for can be seen as a linear system for the unknowns , once the other parameters have been determined.

Remark 1

The exceptional set could be simplified to

| (36) |

Since the jump times and the jump sizes of the BDLP are independent, and the former have an exponential distribution it follows that is with probability one not constant, so . But although it can be shown that the probability of tends to zero, for finite we have . This is the common phenomenon that sample moments do not share all properties of their theoretical counterparts. For definiteness we put outside .

3.2 Consistency

Let us investigate the consistency of the estimator from the previous section. First, we will need the following lemma.

Lemma 2

For every and

| (37) |

Proof: The random variables are identically distributed and for all Thus we are in the situation of [Sto74, Exercise 2.1.2(i), p.14].

Let and be arbitrarily chosen. Taking any integer and using the Chebyshev inequality we obtain

| (38) |

Therefore from the Borel-Cantelli lemma it follows that .

Lemma 3

We have for all that

| (39) |

as .

Proof: We will prove this statement by

induction.

Let us define

Obviously, is a sequence of martingale differences and is therefore uncorrelated. Using expressions (10) and (16) we obtain

so have a common bound for every Since the assumptions of the Theorem 5.1.2 from [Chu01] are satisfied, it follows that

But using again definition (16), the last expression is equivalent to

Finally, using the result of the previous lemma and the fact that it follows

This completes the proof for

(2) Suppose now that the statement of the theorem holds

for i.e. and

| (40) |

when For and for let

| (41) |

Obviously, is a sequence of martingale differences and in particular is uncorrelated. Moreover, due to the strong stationarity of the volatility sequence and relations (41) and (16) we obtain

| (42) | |||||

denoting some constant that does not depend on Hence, by [Chu01, Theorem 5.1.2, p.108], it follows that when which in our case, due to the definition of is equivalent to

| (43) |

Using again the definition (16) and the independency of from for we obtain

Finally, applying the assumption of the induction, Lemma 2 and the statement (43), we obtain

where the last equality follows calculating using (16).

In the next lemma we extend the strong law of large numbers for to more general sequences.

Lemma 4

For all integers we have

| (44) |

as .

Proof: : Let

Obviously, is a sequence of martingale differences, and in particular it is uncorrelated. It is stationary and . So we can use again [Chu01, Theorem 5.12] to show

The conditional expectation is a polynomial in , namely

This is shown in section A.5 in Appendix A where the coefficients are explicitly calculated. Applying Lemma 3 yields

As we have

| (45) |

the proof is completed.

Theorem 1

We have when and the estimator is consistent on , namely

on as

3.3 Asymptotic normality

For a concise vector notation we introduce

| (48) |

and write the estimating equations in the form

| (49) |

and given by (25). We write

| (50) |

with

| (51) |

and

| (52) |

We will use, that is a polynomial in , and that its coefficients are smooth functions in .

We shall first prove the central limit theorem for the estimating functions.

Proposition 3

We have

| (53) |

as , where

| (54) |

Proof: To show the above result, we use the multivariate martingale central limit theorem, that is recapitulated in Appendix B. To that purpose we introduce the vector martingale difference array

| (55) |

We have to show the two assumptions from the previous theorem. First, we prove a multivariate Lyapuonov condition which implies the Lindeberg condition. From (55) it follows that is of the form where is a polynomial in which does not depend on Thus, has the same property and from the explicit moment expression from Appendix A it follows that

| (56) |

where is a polynomial in From Lemma 3 it thus follows

| (57) |

where the expression on the righthand side exists and is finite. Thus the first condition of the martingale central limit theorem is satisfied. In order to verify the second condition of the same theorem we consider the th element of the matrix which is given by

| (58) |

This is again a polynomial in and so by Lemma 4 it follows that

| (59) |

as .

Remark 2

Lemma 5

We have

| (60) |

where

| (61) |

and

| (62) |

with denoting the Kronecker delta.

Proof: We can write

| (63) |

with

| (64) |

In view of Lemma 2 above we see, that the remainder term goes to zero in probability as . As has determinant it is invertible, and we have

| (65) |

with going to zero in probability as . The expression is asymptotically normal with mean and covariance matrix . An application of Slutsky’s Theorem proves the lemma.

Finally, we have all the ingredients for proving the following result.

Theorem 2

The estimator

| (66) |

is asymptotically normal, namely

| (67) |

as , where

| (68) |

and is explicitly given according to (69).

Proof: We observe from (33) that , where is well defined and continuously differentiable in a neighborhood of . Using the Taylor expansion in the last two variables we have , where is well defined and continuously differentiable in a neighborhood of , and goes to zero in probability in view of Lemma 2. Thus it can be neglected according to Slutsky’s Theorem. We apply the delta method, see [Leh99] for example, and compute the Jacobian matrix with

| (69) |

A lengthy elementary calculation shows that the matrix has determinant , thus it is invertible.

Remark 3

For comparison it is instructive to study our simple estimator in the general framework of [Sø99] where the properties of the estimator are studied without exploiting the fact that the estimating equation allows an explicit solution. This is done in [Pos07]. There the theory is extended in the case of a bivariate Markov process and Condition 2.6 of [Sø99] is proven in order to use his Corollary 2.7 and Theorem 2.8.

4 Numerical illustrations

4.1 Description of the model and its parameter values

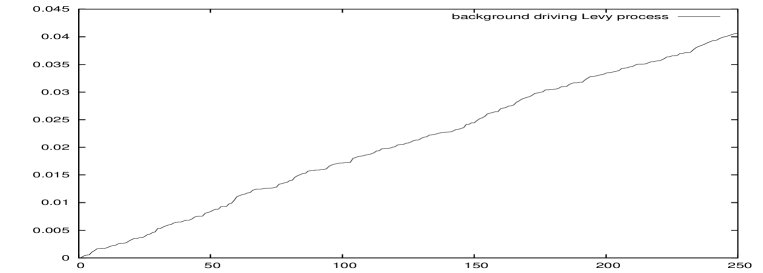

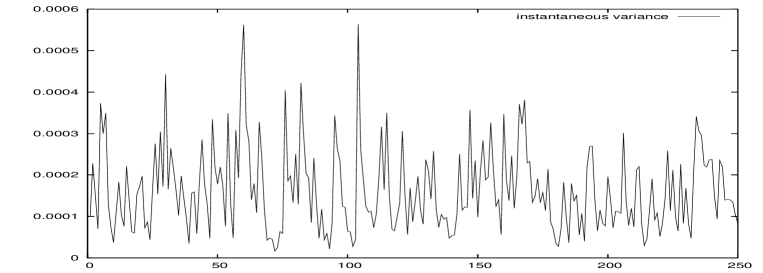

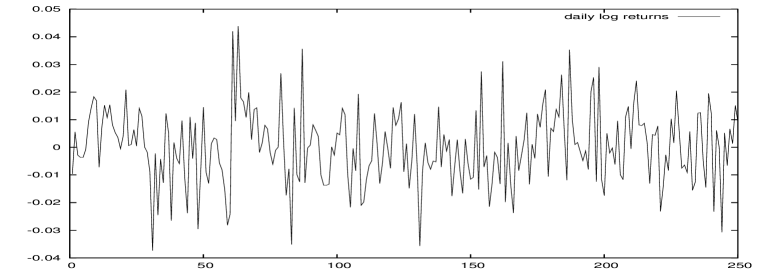

To illustrate the results from the previous sections numerically, we consider the -OU model from Section 2.1.2, where the variance has a stationary gamma distribution. We use as time unit one year consisting of 250 trading days. The true parameters are

| (70) |

The parameters imply that there are on average jumps per day and the jumps in the BDLP and in the volatility are exponentially distributed with mean . The interpretation is, that typically every day two or three new pieces of information arrive and make the variance process jump. The stationary mean of the variance is 0.04. Hence, if we define instantaneous volatility to be the square root of the variance, it will fluctuate around 20% in our example. The half-life of the autocorrelation of returns is about half a day.

In our example annual log returns have (unconditional) mean and a annual volatility 20%. Figure 1 displays a simulation of one year of daily observations from the background driving Lévy process, from the instantaneous variance process, and log returns, or more precisely, simulated realizations of , , and for .

In [Pos07] other scenarios are considered, for example, small jumps arriving every minute, with fast decaying autocorrelation, or few jumps per year, corresponding to exceptional news with heavy impact on the variance process.

4.2 The asymptotic covariance matrix of the estimator

As our goal is an analysis of the estimator, and not an empirical study, we do not estimate the asymptotic covariance, but evaluate the explicit expression using the true parameters. Denoting the vector of asymptotic standard deviations of the estimates and the correlation matrix by resp. we have

| (71) |

4.3 Distribution of the estimates

Figure 2 illustrates the empirical and asymptotic distribution of the simple estimators for the -OU model. The histograms are produced from replications consisting of observations each, corresponding to 32 years with 250 daily obervations per year.

We see from the graphs that in our illustration the parameters , , , and can be estimated quite accurately, in the sense that the usual confidence intervals yield one or two significant digits at least. The estimate for is not as accurate and the accuracy for the estimate for is unsatisfactory.

The bad quality of the estimator for is neither surprising nor very troublesome. It has little impact on the model. The main reason for including the parameter in the specification of BNS models is, for derivatives pricing: A risk-neutral BNS-model must have . In most applications working under a physical probability measure can be assumed without much loss of generality or flexibility.

In ongoing work [HP06] we compare this asymptotic covariance with the covariance of the optimal quadratic estimating function.

5 Further and alternative developments

5.1 Optimal quadratic estimating functions

Our choice of estimating functions is natural, but, mathematically speaking, somewhat arbitrary. In ongoing work [HP06] we show, that the optimal quadratic estimating function based on the moments of can be computed explicitly, though the corresponding estimator has to be determined numerically. Our simple estimator can be used as a starting point for an iterative root-finding procedure. Consistency and asymptotic normality can be shown using the general theory as presented in [Sø99] along the lines of the present paper, although the expressions involved are slightly more complicated.

5.2 Using more integer or trigonometric moments for better efficiency

More efficient estimators than provided by the optimal quadratic estimating function can be obtained by incorporating further moments. As we have provided explicit computations for arbitrary integer moments and conditional moments, our methods can be extended to that situation. We might even have the number of moments tend to infinity with the number of observations, and obtain an estimator that is asymptotically equivalent to the maximum likelihood estimator, when the latter exists resp. can be defined, see 2.3. The reader might object, that very high moments are not reliable for empirical investigations. BNS-models allow also explicit computation of the characteristic function and thus of conditional and unconditional trigonometric moments and for arbitrary constants and , that could be used instead for constructing estimating functions. See [AS02] for diffusions, [Sch05] for Lévy type processes, and [Sin01] for affine models.

5.3 Intra-day observations

Our approach is based on the explicit calculation of conditional and unconditional moments. Those calculations can be done for BNS-models on arbitrary time intervals. Hence our analysis is not restricted to a fixed time grid with the number of observation intervals tending to infinity, but could be performed also on a fixed horizon, with the number of intra-day observations increasing to infinity. The resulting estimators should then be compared to power-variation methods, cf. [Tod06].

5.4 Comparison to the generalized method of moments

We would be interested in a comparison of our results to the related generalized methods of moments. For a rigorous treatment of the latter, a precise specification of the weighting matrix is required, see [HHY96] and the references therein.

5.5 Unobserved volatility and substitutes for volatility

Finally, perhaps the biggest issue is, that the instantaneous variance is not observed in discrete time. In [Lin05] it is reported, that the number of trades is an excellent substitute for statistical purposes. This is certainly a promising starting point for an empirical analysis. For a theoretical analysis a joint model for the number prices and number of trades has to be specified.

Another direction would be to adapt the implied state method (IS-GMM) as introduced in [Pan02] to our martingale estimating function approach: We replace the unobserved in the estimating equations by the model-implied variance that is obtained from option prices, assuming that the dynamics are governed by BNS-models both under the physical probability measure and a risk-neutral measure . The resulting estimating function will not be a martingale estimating function any more, and the bias has to be accounted for in a rigorous analysis. Nevertheless, in view of the results of [Pan02], we are optimistic, that consistency and asymptotic normality will hold also here.

Appendix A Explicit moment calculations

This section is about computing explicitly and . All moments below will be given in terms of the cumulants of the stationary distribution, denoted by . We set

| (72) |

If the stationary distribution is determined by the two parameters and the higher cumulants are obviously functions of and , but the formulae hold in more general cases.

The calculations exploit the analytical tractability of the BNS-model, namely conditional Gaussianity of the logarithmic returns and the linear structure of the OU-type process . From that it follows, and it is well-known, that univariate and multivariate cumulants can be computed easily. It remains to transform multivariate cumulants to multivariate moments, again a topic that is well-understood, and explicit expressions involve the multivariate Faa di Bruno formula, multivariate Bell polynomials and integer partitions, see for example [McC87].

We have chosen to use simple recursions, that are easy to implement on a computer algebra system, in particular, since the expressions, though completely explicit and elementary, are rather lengthy when it comes to evaluating moments of order four for the asymptotic covariance matrix. For the reader’s convenience, we give the details in this appendix.

A.1 Preliminaries

Let us recapitulate the variables and notation from section 2.2, that are required in the following calculations. We use

| (73) |

We have

| (74) |

where

| (75) |

Note, that we have the simpler formula , but the integral above is sometimes notationally more convenient. We have

| (76) |

A.2 Stationary moments

We use the well-known recursion to compute moments from cumulants

| (77) |

Alternatively we have , where denotes the complete Bell polynomials. Explicit non-recursive expressions can be given, but we do not use them.

A.3 Trivariate cumulants

From the key formula for Wiener-type integrals with Lévy process integrator, it follows that the joint cumulants of are given by

| (78) |

with

| (79) |

A.4 Trivariate Moments

Trivariate moments can be computed recursively from trivariate cumulants

| (80) |

| (81) |

| (82) |

Alternatively, we can express as trivariate complete Bell polynomials evaluated at the trivariate cumulants of , and explicit non-recursive expressions are available, but not very useful for us.

A.5 Some conditional expectations

Using (74) gives

| (83) |

Collecting powers of gives

| (84) |

with

| (85) |

Then using (76) and conditioning gives

| (86) |

Collecting powers of gives

| (87) |

with

| (88) |

Finally using (76) and the Gaussian moments gives

| (89) |

Collecting powers of gives

| (90) |

with

| (91) |

It follows from the calculations above that are polynomials in .

A.6 Some unconditional expectations

The same structure pertains for the unconditional expectations,

| (92) |

then

| (93) |

and finally

| (94) |

Appendix B The simple multivariate martingale central limit theorem

The following simple version of a multivariate martingale central limit theorem is certainly well-known or obvious for experts, some references are [CP05, KS99b, vZ00].

However, when looking for references, we found statements that do not exactly apply, or that are much more general (continuous time, random normalizations,…). It turned out that the elementary proof below is shorter, than an attempt to verify the assumptions and deduce the result from a more ’advanced’ theorem. Yet, any concrete and precise hint for an appropriate reference would be most welcome to the authors.

Theorem 3

Suppose is a martingale difference array such that for every

| (95) |

and

| (96) |

as Then

| (97) |

Proof: We will use the Cramer-Wold device. For let us define a random variable

| (98) |

Then we have

| (99) | |||||

From Assumption (96) it follows that the expression (99) converges to and thus

| (100) |

as Furthermore, it holds

| (101) |

Thus, for an arbitrary we have

| (102) | |||||

Since for the condition implies

| (103) |

it follows that

| (104) |

and thus using the Assumption (95), from (102) it follows that

| (105) |

as Now, the statement follows from the univariate martingale central limit theorem from [HH80].

Lemma 6

The conditional Lyapounov condition implies the conditional Lindeberg condition, namely, if

| (106) |

then

| (107) |

as

Proof: For every we have

| (108) | |||||

since

From Assumption (106) the statement follows.

References

- [AS02] Yacine Aït-Sahalia. Maximum likelihood estimation of discretely sampled diffusions: a closed-form approximation approach. Econometrica, 70(1):223–262, 2002.

- [BG05] F.E. Benth and M. Groth. The minimal entropy martingale measure and numerical option pricing for the Barndorff-Nielsen–Shephard stochastic volatility model. E-print, Department of Mathematics, University of Oslo, 2005.

- [BK05] Fred Espen Benth and Kenneth Hvistendahl Karlsen. A PDE representation of the density of the minimal entropy martingale measure in stochastic volatility markets. Stochastics, 77(2):109–137, 2005.

- [BKR03] Fred Espen Benth, Kenneth Hvistendahl Karlsen, and Kristin Reikvam. Merton’s portfolio optimization problem in a Black and Scholes market with non-Gaussian stochastic volatility of Ornstein-Uhlenbeck type. Math. Finance, 13(2):215–244, 2003.

- [BMB05] Fred Espen Benth and Thilo Meyer-Brandis. The density process of the minimal entropy martingale measure in a stochastic volatility model with jumps. Finance Stoch., 9(4):563–575, 2005.

- [BNNS02] Ole E. Barndorff-Nielsen, Elisa Nicolato, and Neil Shephard. Some recent developments in stochastic volatility modelling. Quant. Finance, 2(1):11–23, 2002. Special issue on volatility modelling.

- [BNS01] Ole E. Barndorff-Nielsen and Neil Shephard. Non-Gaussian Ornstein-Uhlenbeck-based models and some of their uses in financial economics. J. R. Stat. Soc. Ser. B Stat. Methodol., 63(2):167–241, 2001.

- [BS95] Bo Martin Bibby and Michael Sørensen. Martingale estimation functions for discretely observed diffusion processes. Bernoulli, 1(1-2):17–39, 1995.

- [BS01] Bo Martin Bibby and Michael Sørensen. Simplified estimating functions for diffusion models with a high-dimensional parameter. Scand. J. Statist., 28(1):99–112, 2001.

- [Chu01] Kai Lai Chung. A course in probability theory. Academic Press Inc., San Diego, CA, third edition, 2001.

- [CM00] Donato Michele Cifarelli and Eugenio Melilli. Some new results for Dirichlet priors. Ann. Statist., 28(5):1390–1413, 2000.

- [CP05] Irene Crimaldi and Luca Pratelli. Convergence results for multivariate martingales. Stochastic Processes and their Applications, 115(4):571–577, 2005.

- [CR90] Donato Michele Cifarelli and Eugenio Regazzini. Distribution functions of means of a Dirichlet process. Ann. Statist., 18(1):429–442, 1990.

- [CT97] Yuan Shih Chow and Henry Teicher. Probability theory. Springer-Verlag, New York, third edition, 1997.

- [CT04] Rama Cont and Peter Tankov. Financial modelling with jump processes. Chapman & Hall/CRC, Boca Raton, FL, 2004.

- [DFS03] D. Duffie, D. Filipović, and W. Schachermayer. Affine processes and applications in finance. Ann. Appl. Probab., 13(3):984–1053, 2003.

- [DPS00] Darrell Duffie, Jun Pan, and Kenneth Singleton. Transform analysis and asset pricing for affine jump-diffusions. Econometrica, 68(6):1343–1376, 2000.

- [DS04] Susanne Ditlevsen and Michael Sørensen. Inference for observations of integrated diffusion processes. Scand. J. Statist., 31(3):417–429, 2004.

- [FSS01] Sylvia Frühwirt-Schnatter and Leopold Sögner. MCMC estimation of the Barndorff-Nielsen-Shephard stochastic volatility model. Unpublished talks, 2001.

- [GS01] James E. Griffin and Mark F.J. Steel. Inference with non-Gaussian Ornstein-Uhlenbeck processes for stochastic volatility. Journal of Econometrics, forthcoming, 2001.

- [HH80] P. Hall and C. C. Heyde. Martingale limit theory and its application. Academic Press Inc., New York, 1980.

- [HHY96] L.P. Hansen, J. Heaton, and A. Yaron. Finite-sample properties of some alternative GMM estimators. Journal of Business Economic Statistics, 14:262–280, 1996.

- [HP06] Friedrich Hubalek and Petra Posedel. Asymptotic analysis for an optimal estimating function for Barndorff-Nielsen-Shephard stochastic volatility models. Work in progress, 2006.

- [Jac01] Martin Jacobsen. Discretely observed diffusions: classes of estimating functions and small -optimality. Scand. J. Statist., 28(1):123–149, 2001.

- [Jac02] Martin Jacobsen. Optimality and small -optimality of martingale estimating functions. Bernoulli, 8(5):643–668, 2002.

- [Jam05] Lancelot F. James. Analysis of a class of likelihood based continuous time stochastic volatility models including Ornstein-Uhlenbeck models in financial economics. arXiv:math/0503055, 2005.

- [Jam06] Lancelot F. James. Laws and likelihoods for Ornstein Uhlenbeck-gamma and other BNS OU stochastic volatility models with extensions. arXiv:math/0604086, 2006.

- [Joh78] Søren Johansen. The product limit estimator as maximum likelihood estimator. Scand. J. Statist., 5(4):195–199, 1978.

- [Kes00] Mathieu Kessler. Simple and explicit estimating functions for a discretely observed diffusion process. Scand. J. Statist., 27(1):65–82, 2000.

- [KP02] Mathieu Kessler and Silvestre Paredes. Computational aspects related to martingale estimating functions for a discretely observed diffusion. Scand. J. Statist., 29(3):425–440, 2002.

- [KS99a] Mathieu Kessler and Michael Sørensen. Estimating equations based on eigenfunctions for a discretely observed diffusion process. Bernoulli, 5(2):299–314, 1999.

- [KS99b] Uwe Küchler and Michael Sørensen. A note on limit theorems for multivariate martingales. Bernoulli, 5(3):483–493, 1999.

- [KW56] J. Kiefer and J. Wolfowitz. Consistency of the maximum likelihood estimator in the presence of infinitely many incidental parameters. Ann. Math. Statist., 27:887–906, 1956.

- [Leh99] E. L. Lehmann. Elements of large-sample theory. Springer-Verlag, New York, 1999.

- [Lin05] Carl Lindberg. Portfolio Optimization and Statistics in Stochastic Volatility Markets. PhD dissertation, Chalmers University of Technology, 2005.

- [Lin06] Carl Lindberg. News-generated dependence and optimal portfolios for stocks in a market of Barndorff-Nielsen and Shephard type. Math. Finance, 16(3):549–568, 2006.

- [McC87] Peter McCullagh. Tensor methods in statistics. Chapman & Hall, London, 1987.

- [MR03] Rosa Maria Mininni and Silvia Romanelli. Martingale estimating functions for Feller diffusion processes generated by degenerate elliptic operators. J. Concr. Appl. Math., 1(3):191–216, 2003.

- [NS03] B. Nielsen and N. Shephard. Likelihood analysis of a first-order autoregressive model with exponential innovations. J. Time Ser. Anal., 24(3):337–344, 2003.

- [NV03] Elisa Nicolato and Emmanouil Venardos. Option pricing in stochastic volatility models of the Ornstein-Uhlenbeck type. Math. Finance, 13(4):445–466, 2003.

- [Pan02] Jun Pan. The jump-risk premia implicit in options: evidence from an integrated time-series study. J. Financial Economics, 63:3–50, 2002.

- [Pos07] Petra Posedel. Inference for a class of stochastic volatility models in presence of jumps: a martingale estimating function approach. PhD dissertation, Bocconi University, 2007.

- [Rao73] M. M. Rao. Abstract martingales and ergodic theory. In Multivariate analysis, III ( Proc. Third Internat. Sympos., Wright State Univ., Dayton, Ohio, 1972), pages 45–60. Academic Press, New York, 1973.

- [RPD04] Gareth O. Roberts, Omiros Papaspiliopoulos, and Petros Dellaportas. Bayesian inference for non-Gaussian Ornstein-Uhlenbeck stochastic volatility processes. J. R. Stat. Soc. Ser. B Stat. Methodol., 66(2):369–393, 2004.

- [RS06] Thorsten Rheinländer and Gallus Steiger. The minimal entropy martingale measure for general Barndorff-Nielsen/Shephard models. The Annals of Applied Probability, 16(3), 2006.

- [Sch03] Wim Schoutens. Lévy processes in finance. Wiley, 2003.

- [Sch05] Ernst Schaumburg. Estimation of Markov processes with Lévy type generators. Working paper, 2005.

- [Sin01] Kenneth J. Singleton. Estimation of affine asset pricing models using the empirical characteristic function. J. Econometrics, 102(1):111–141, 2001.

- [Sø97] Michael Sørensen. Statistical inference for discretely observed diffusion. Lectures at Berliner Graduiertenkolleg ’Stochastische Prozesse und Probabilistische Analysis’, 1997.

- [Sø99] Michael Sørensen. On asymptotics of estimating functions. Brazilian Journal of Probability and Statistics, (13):111–136, 1999.

- [Sø00] Helle Sørensen. Inference for Diffusion Processes and Stochastic Volatility Models. PhD thesis, 2000.

- [Sør97] Michael Sørensen. Estimating functions for discretely observed diffusions: a review. In Selected Proceedings of the Symposium on Estimating Functions (Athens, GA, 1996), volume 32 of IMS Lecture Notes Monogr. Ser., pages 305–325, Hayward, CA, 1997. Inst. Math. Statist.

- [Sør01] Helle Sørensen. Discretely observed diffusions: approximation of the continuous-time score function. Scand. J. Statist., 28(1):113–121, 2001.

- [SS00] A. N. Shiryaev and V. G. Spokoiny. Statistical experiments and decisions. World Scientific Publishing Co. Inc., River Edge, NJ, 2000.

- [Sto74] William F. Stout. Almost sure convergence. Academic Press, New York-London, 1974.

- [Str85] Helmut Strasser. Mathematical theory of statistics. Walter de Gruyter & Co., Berlin, 1985.

- [tH03] Enrique ter Horst. A Lévy generalization of compound Poisson processes in finance: Theory and application (Chapter 3). PhD thesis, Duke University, 2003.

- [Tod06] Viktor Todorov. Econometric analysis of jump-driven stochastic volatility models. preprint, 2006.

- [Uch04a] Masayuki Uchida. Estimation for discretely observed small diffusions based on approximate martingale estimating functions. Scand. J. Statist., 31(4):553–566, 2004.

- [Uch04b] Masayuki Uchida. Minimum contrast estimation for discretely observed diffusion processes with small dispersion parameter. Bull. Inform. Cybernet., 36:35–49, 2004.

- [Ven01] Emmanouil Venardos. Derivatives Pricing and Ornstein-Uhlenbeck type Stochastic Volatility. Dissertation, University of Oxford, 2001.

- [vZ00] Harry van Zanten. A multivariate central limit theorem for continuous local martingales. Statistics & Probability Letters, 50(3):229–235, 2000.