Joint analysis and estimation of stock prices and trading volume in Barndorff-Nielsen and Shephard stochastic volatility models

Abstract

We introduce a variant of the Barndorff-Nielsen and Shephard stochastic volatility model where the non Gaussian Ornstein-Uhlenbeck process describes some measure of trading intensity like trading volume or number of trades instead of unobservable instantaneous variance. We develop an explicit estimator based on martingale estimating functions in a bivariate model that is not a diffusion, but admits jumps. It is assumed that both the quantities are observed on a discrete grid of fixed width, and the observation horizon tends to infinity. We show that the estimator is consistent and asymptotically normal and give explicit expressions of the asymptotic covariance matrix. Our method is illustrated by a finite sample experiment and a statistical analysis on the International Business Machines Corporation (IBM) stock from the New York Stock Exchange (NYSE) and the Microsoft Corporation (MSFT) stock from Nasdaq during a history of five years.

KEYWORDS:

Martingale estimating functions, stochastic volatility models with jumps, consistency and asymptotic normality, trading intensity

1 Introduction

In [BNS01] Barndorff-Nielsen and Shephard introduced a class of stochastic volatility models in continuous time, where the instantaneous variance follows an Ornstein-Uhlenbeck type process driven by an increasing Lévy process. BNS-models, as we will call them from now on, allow flexible modelling, capture many stylized facts of financial time series, and yet are of great analytical tractability. Those models have been studied from various points of view in mathematical finance and related fields. Unfortunately, it seems that statistical estimation of the model is the most difficult problem, and most of the work in that area is focused on computationally intensive methods. In [HP07] an explicit estimator based on martingale estimating functions was developed under the assumptions that returns and volatility are observed. That paper contains also further references on BNS models, martingale estimating functions, estimating discretely observed diffusions models, etc. The literature on estimation for discretely observed diffusions is vast, a few references are [Uch04, KP02, Jac01, Kes00, KS99, BS95]. In particular, the martingale estimating function approach is used, developed and studied for example in [Sø99]. In the diffusion setting the major difficulty is that the transition probabilities are not known and are difficult to compute. In contrast to that, the characteristic function of the transition probability is known in closed form for many BNS models and the transition probability can be computed with Fourier methods with high precision.

In practice volatility is not observed, but many researchers, including, for example, [Kar87, GT92, JL94] have established a connection between volatility and different measures of trading intensity, such as traded volume or number of trades. In particular, [Lin07] gives a first application of this approach to BNS models. We take up this idea and combine it with the martingale estimating function approach. Measures of trading intensity contain much information about the volatility. We identify the volatility with a multiple of some measure of trading intensity, in this paper the daily traded volume. In doing so, our bivariate time series is given by the logarithmic returns and trading volume which are both observable quantities. We explore the joint distribution of logarithmic returns and the instantaneous trading volume/number of trades . The joint conditional moment-generating function of is known in closed form and thus we obtain closed form expressions for the joint conditional moments up to any desired order. This yields a sequence of martingale differences and the martingale estimating function approach is used. We employ then the large sample properties, in particular the strong law of large numbers for martingales and the martingale central limit theorem. In this way we do not need ergodicity, mixing conditions, etc.

The contributions of the present paper are as follows: first we develop a simple and explicit estimator for BNS models using a martingale estimating function approach and identifying the volatility with a multiple of trading volume. Secondly, we give proofs of its consistency and asymptotic normality. In doing so we compute explicitly the asymptotic covariance matrix. Thirdly, we include numerical illustrations and apply our method on real data.

Since in this analysis we assume that the discrete time variance process is proportional to the trading volume/number of trades , we are able to directly model the stochastic volatility in asset price dynamics. Due to the analytical tractability of BNS models, we can work with the exact dynamics for discrete observations of the continuous time model. We want to stress that our approach leads to simple and explicit formulas for the estimator and its asymptotic covariance matrix, and no simulation or other computer intensive methods are required. Simulations are only used to illustrate the finite sample performance in numerical experiments. Finally, we apply the method to real data and do a statistical analysis on the International Business Machines Corporation (IBM) stock from the New York Stock Exchange (NYSE) and the Microsoft Corporation (MSFT) stock from Nasdaq during a volatile history of five years.

The remainder of the paper is organized as follows: in section 2.1 we describe the class of BNS models in continuous time and present two concrete examples, the OU and IG-OU model. In section 2.2 we introduce the quantities observed in discrete time that are used for estimation. In section 3 we present the estimating equations, their explicit solution which is our estimator and its consistency and asymptotic normality are proven. In section 4 numerical illustrations are presented. In section 5 we apply our results on daily data on the IBM stock from NYSE and the MSFT stock from Nasdaq.

2 The model

2.1 The continuous time model

2.1.1 The general setting

As in Barndorff-Nielsen and Shepard [BNS01], we assume that the price process of an asset is defined on some filtered probability space and is given by with a constant. The process of logarithmic returns and the instantaneous trading volume/number of trades process satisfy

| (1) |

and

| (2) |

where the parameters and are real constants with The process is a standard Brownian motion, the process is an increasing Lévy process, and we define for notational simplicity. Adopting the terminology introduced by Barndorff-Nielsen and Shepard, we will refer to as the background driving Lévy process (BDLP). The Brownian motion and the BDLP are independent and is assumed to be the usual augmentation of the filtration generated by the pair . The random variable has a self-decomposable distribution corresponding to the BDLP such that the process is strictly stationary and

| (3) |

For our analysis we will assume that the instantaneous variance process is a constant time the trading volume/number of trades That is,

| (4) |

with

Remark 1

Equation (4) implies that the instantaneous variance of log returns is a constant multiple of the trading volume/number of trades, and trading volume/number of trades is modelled as an OU-type process.

To shorten the notation we introduce the parameter vector

| (5) |

and the bivariate process

| (6) |

If the distribution of is from a particular class then is called a BNS-DOU() model.

The process is clearly Markovian.

2.1.2 The -OU model

The -OU model is obtained by constructing the BNS-model with stationary gamma distribution, , where the parameters are and . The corresponding background driving Lévy process is a compound Poisson processes with intensity and jumps from the exponential distribution with parameter . Consequently both processes and have a finite number of jumps in any finite time interval.

For the -OU model it is more convenient to work with the parameters and . The connection to the generic parameters used in our general development is given by

| (7) |

As the gamma distribution admits exponential moments we have integer moments of all orders and our Assumption 1 below is satisfied.

2.1.3 The IG-OU model

The IG-OU model is obtained by constructing the BNS-model with stationary inverse Gaussian distribution, , with parameters and .

The corresponding background driving Lévy process is the sum of an IG( process and an independent compound Poisson process with intensity and jumps from an distribution. Consequently both processes and have infinitely many jumps in any finite time interval.

For the IG-OU model it is more convenient to work with the parameters and . The connection to the generic parameters used in our general development is given by

| (8) |

As the inverse Gaussian distribution admits exponential moments we have integer moments of all orders and our Assumption 1 below is satisfied.

2.2 Discrete observations

The following description is rather analogous to [HP07, Section ]. The only (but important) exception is the introduction of the parameter in (12) and (21). We observe returns and the trading volume/number of trades process on a discrete grid of points in time

| (9) |

which relates trading volume/number of trades and the instantaneous variance of log returns. This implies

| (10) |

Using

| (11) |

we have that is a sequence of independent random variables, and it is independent of . If the grid is equidistant, then are iid. Observing the returns on the grid we have

| (12) |

where

| (13) |

is the integrated trading volume/number of trades process. This suggests introducing the discrete time quantities

| (14) |

and

| (15) |

Furthermore, it is also convenient to introduce the discrete quantity

| (16) |

It is not difficult to see (conditioning!) that is an iid sequence independent from all other discrete quantities. We note also that is a bivariate iid sequence, but and are obviously dependent.

From now on, for notational simplicity, we consider the equidistant grid with

| (17) |

where is fixed. This implies

| (18) |

and

| (19) |

where

| (20) |

Furthermore,

| (21) |

The sequence is clearly Markovian. From now on we assume all moments of the stationary distribution of exist.

Assumption 1

| (22) |

In the estimating context we assume all moments are finite with respect to all probability measures under consideration, where is the parameter space.

No other assumptions are made, and all conditions required for consistency and asymptotic normality of our estimator will be proven rigorously from that assumption.

Proposition 1

We have for all that

| (23) |

and

| (24) |

Consequently the expectation of any (multivariate) polynomial in exists under .

Proof: The proof is given in [HP07, Proposition ].

Let us remark that, by the stationarity, the above result holds also for instead of , where is arbitrary.

3 A theoretical framework of the estimation procedure

3.1 The estimating equations and their explicit solution

The reader familiar with [HP07] will notice that the following developments are quite similar to the paper mentioned, the main (but important) difference is an additional estimating equation for the new parameter

For estimation purposes we consider a probability space on which a parameterized family of probability measures is given:

| (25) |

where . The data is generated under the true probability measure with some . The expectation with respect to is denoted by and with respect to simply by .

We assume there is a process that is BNS-DOU() under . We want to find an estimator for using observations . We are interested in asymptotics as . To that purpose let us consider the following martingale estimating functions:

| (26) |

Lemma 1

We have the explicit expressions

| (27) |

Proof: The formulas are special cases of the general moment

calculations given in [HP07, Appendix A].

The estimator is obtained by solving the estimating equation and it turns out that this equation has a simple explicit solution.

Proposition 2

The estimating equation admits for every on the event

| (28) |

a unique solution that is given by

| (29) |

where

| (30) |

and

| (31) |

Proof: The first three equations , for

contain only the unknowns and are easily

solved. In fact we get a familiar estimator for the first two

moments and the autocorrelation coefficient of an AR(1) process.

The last four equations , for can be

seen as a linear system for the unknowns ,

once the other parameters have been determined.

Remark 2

The exceptional set could be simplified to

| (32) |

Since the jump times and the jump sizes of the BDLP are independent, and the former have an exponential distribution it follows that is with probability one not constant, so . Furthermore, for finite we have . For definiteness we put outside .

3.2 Consistency and asymptotic normality

Let us investigate the consistency and asymptotic normality of the estimator from the previous section.

Theorem 1

We have when and the estimator is consistent on , namely

on as

Proof: From [HP07, Lemma 4] it follows that for all integers we have

| (33) |

as . Using this results it easily follows that

| (34) |

so as . Furthermore, from (33) it follows that the empirical moments in (30) and (31) converge to their theoretical counterparts, and , where

| (35) |

Plugging the limits into (29) shows, after a short

mechanical calculation, that the estimator is consistent.

In order to prove asymptotic normality, we use the general framework and results of [Sø99]. We extend the theory in the case of a bivariate Markov process. To

apply [Sø99, Theorem 2.8], requires to show that

[Sø99, Condition 2.6] is satisfied.

Proposition 3

The Condition of [Sø99] is satisfied.

Proof: For a concise vector notation we introduce

| (36) |

and we write the estimating equations in the form

| (37) |

Looking at (27) we note that is a polynomial in namely

| (38) |

where the degree and the coefficients

which are smooth functions in can be read off

from (27).

Now

the proof is completely analogous to that of

[HP07, Proposition 4].

Finally, we have all the ingredients for proving the following result.

Theorem 2

The estimator

| (39) |

is asymptotically normal, namely

| (40) |

as , where

| (41) |

and

| (42) |

Remark 3

4 A numerical illustration of the finite sample performance of the estimator

4.1 Description of the model and its parameter values

To illustrate the results from the previous sections numerically, we consider the -OU model from Section 2.1.2, where the trading volume has a stationary gamma distribution. The corresponding BDLP is a compound Poisson process with intensity and jumps from the exponential distribution with parameter We use as time unit one year consisting of 250 trading days. The true parameters are

| (45) |

The parameters imply that there are on average jumps per day and the jumps in the BDLP and in the trading volume are exponentially distributed with mean and standard deviation . The interpretation is, that typically every day or new pieces of information arrive and make the trading volume process jump. The stationary mean of the trading volume is and of the variance is . Hence, if we define instantaneous volatility to be the square root of the variance, it will fluctuate around in our example. The half-life of the autocorrelation of the variance process is about a day.

In our example annual log returns have (unconditional) mean and annual volatility . We will perform the estimation procedure for two different sample sizes, namely and corresponding to years and years respectively, with daily observation per year.

4.2 Simulation study

We first simulate 1000 samples of equidistant observations of and Table summarizes the estimation results of our simulation study concerning the parameters

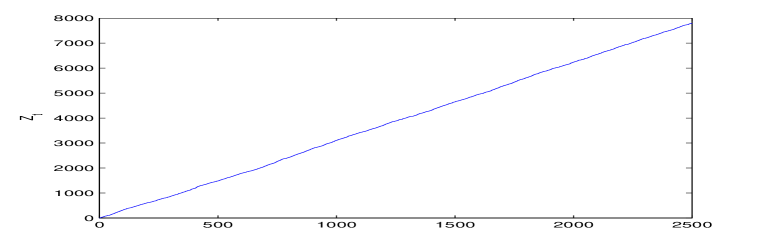

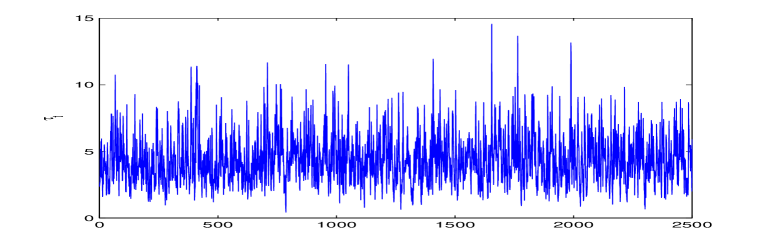

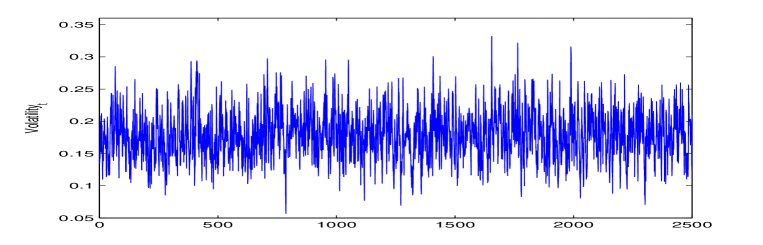

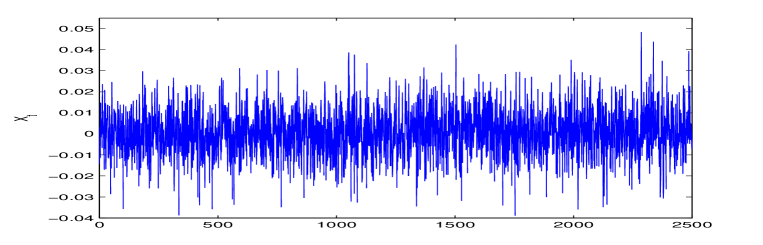

Figure 1 displays a simulation of ten years of daily observations from the background driving Lévy process, the instantaneous trading volume process, the volatility process and log returns for .

The empirical mean of all the estimated parameter values is shown in the first line, with the empirical standard deviations in brackets. We also estimated mean square error (MSE) and mean absolute error (MAE), again with the standard deviation in brackets. The corresponding results for a sample size of observations are reported in the last three lines of Table 1 and Table 2.

| Mean | 6.2145 (0.2552) | 1.435 (0.0588) | 177.865 (8.9257) |

| MSE | 0.0672 (0.1046) | 0.0036 (0.0055) | 79.5956 (115.6766) |

| MAE | 0.2016 (0.1629) | 0.047 (0.0369) | 7.0692 (5.4454) |

| Mean | 6.1642 (0.1424) | 1.4186 (0.0329) | 177.1342 (5.208) |

| MSE | 0.0203 (0.0283) | 0.0011 (0.0016) | 27.7663 (39.1414) |

| MAE | 0.1135 (0.0862) | 0.0259 (0.0203) | 4.2191 (3.1584) |

| Mean | 0.4402 (0.1849) | 0.0148 (0.053) | 0.0871 (0.0013) | |

| MSE | 0.0342 (0.0492) | 0.0028 (0.0039) | ||

| MAE | 0.1483 (0.1105) | 0.0428 (0.0313) | 0.0011 (0.0008) | |

| Mean | 0.4388 (0.1002) | 0.0129 (0.0278) | ||

| MSE | 0.01 (0.0138) | 0.0008 (0.0011) | ||

| MAE | 0.08 (0.0604) | 0.0222 (0.0169) |

When one compares the estimates for the different sample sizes, it can be seen that the MSE reduces for all seven estimators, when the sample size is increased and the reduction is roughly of a factor of which would correspond to the asymptotic properties of the estimators.

4.3 The asymptotic covariance matrix and the finite sample distribution of the estimator

As our goal is an analysis of the estimator, we do not estimate the asymptotic covariance, but evaluate the explicit expression using the true parameters. Denoting the vector of asymptotic standard deviations of the estimates and the correlation matrix by resp. we have

| (46) |

| (47) |

We will discuss what this values of implies for the sample size of below. The correlations among parameters related to the returns distribution, namely and are rather small except for and In contrast to that, correlations among the trading volume parameters, namely and are very high. Theoretically, this can be addressed using the optimal martingale estimating function approach, even though the corresponding equations can not be solved explicitly and the optimal estimator has to be obtained by numerical optimization, see [HP06] for developments in this direction.

Figure 2 illustrates the empirical distribution of the simple estimators for the -OU model. The histograms are produced from replications consisting of observations each, corresponding to 10 years with 250 daily observations per year. Both from the graphs and the asymptotic standard deviations we see that the parameter can be estimated quite accurately to at least one digit of precision. The parameter is estimated even better with almost two digits of precision. The autocorrelation parameter is estimated slightly less accurate. The parameter which connects the trading volume/number of trades and volatility is estimated quite accurate with one to two digits of precision. This means that if the relation between volatility and trading volume is exploited, not too much uncertainty is introduced by the estimating procedure. This can be also very promising for option pricing purposes. The bad quality of the estimator for is neither surprising nor very troublesome. It has little impact on the model. The main reason for including the parameter in the specification of BNS models is, for derivatives pricing: A risk-neutral BNS-model must have . In most applications working under a physical probability measure can be assumed without much loss of generality or flexibility. For the same reason the parameter is not very relevant although it can be estimated more accurate than Even though the value of the leverage parameter is rather small, it can be estimated very accurately.

4.4 Estimation of the volatility

Recall from (4), that we assumed that the instantaneous variance is a multiple of trading volume and thus we have the following equation for the volatility

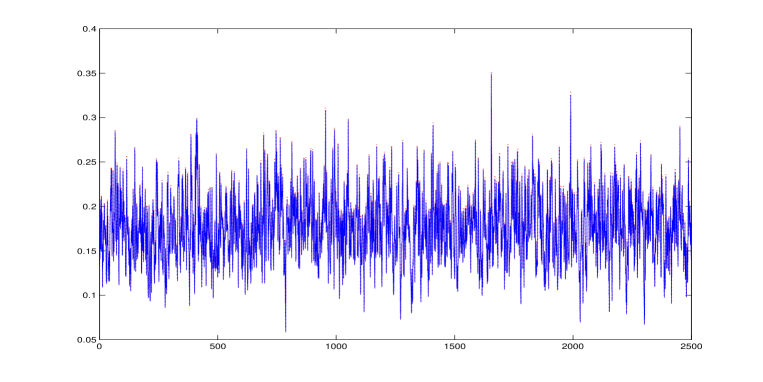

| (48) |

Since we observe at integer times, an estimate of the volatility process can therefore be calculated from (48) and it is plotted in Figure 3 together with the exact volatility for one simulated path. The estimator for is calculated from the simulated path and since is very accurate, the two graphs are almost indistinguishable.

Next we investigate the goodness of fit of our estimation method by a residual analysis. Recall from (21), the estimated residuals are given by

| (49) |

where the integrated instantaneous trading volume is given by (19). The quantity is not observable, but we can find an approximation as follows. For the integral we use simple Euler approximations

| (50) |

with are approximately and i.i.d. The estimated residuals are given by

where

| (51) |

Since we assume that is an iid sequence, our goal is to check if the residuals are iid and The residuals should be symmetric around zero and thus their mean and skewness should be close to zero. Furthermore, we expect the kurtosis to be close to three. Consequently, we estimated mean, MSE, MAE and the corresponding standard deviations for the mean, the standard deviation, the skewness and the kurtosis of the residuals based on simulations. The results for both sample sizes are reported in Table 3 and indicate a reasonable fit.

| mean | Std | skew | kurt | |

|---|---|---|---|---|

| Mean | 0.11753 (0.03455) | 1.02865 (0.0067) | -0.04114 (0.06107) | 3.3018 (0.17843) |

| MSE | 0.015(0.0086) | 0.00087 (0.00039) | 0.00542 (0.00753) | 0.12289 (0.14759) |

| MAE | 0.11753 (0.03455) | 0.02865 (0.0067) | 0.05885 (0.04423) | 0.30291 (0.17654) |

| mean | Std | skew | kurt | |

| Mean | 0.1166 (0.01951) | 1.02838 (0.00373) | -0.03876 (0.03476) | 3.29937 (0.10449) |

| MSE | 0.01398 (0.00456) | 0.00082 (0.00021) | 0.00271 (0.00333) | 0.10053 (0.07529) |

| MAE | 0.1166 (0.01951) | 0.02838 (0.00373) | 0.04335 (0.02883) | 0.299938 (0.10446) |

The correlation of the squared residuals was checked by performing a Ljung-Box test for each sample. For we computed the test statistic based on lags and had to reject the null hypothesis of no correlation times out of 1000 simulations at the level. Whereas for the test statistic was computed using lags and the null hypothesis was rejected times out of simulations again at the level.

5 Real data analysis

The BNS model will be fitted to daily log returns of the International Business Machines Corporation (IBM) stock and the Microsoft Corporation (MSFT) stock. The IBM stock is from the New York Stock Exchange (NYSE), whereas MSFT belongs to Nasdaq. The data spans over roughly 5 years starting in March , to March , for IBM and starting in April , to February , for MSFT. There were and observations for IBM and MSFT respectively of daily closing prices and trading volumes. The resulting time series are shown in Figure 4 and Figure 5. Data on trading volumes are expressed in millions. Sample measures of skewness and kurtosis111Skewness is measured as and kurtosis as where is the ith central moment. of the returns are and respectively for IBM and and for MSFT. Throughout, we consider the -OU model from section 2.1.2.

5.1 Parameter estimates and interpretation

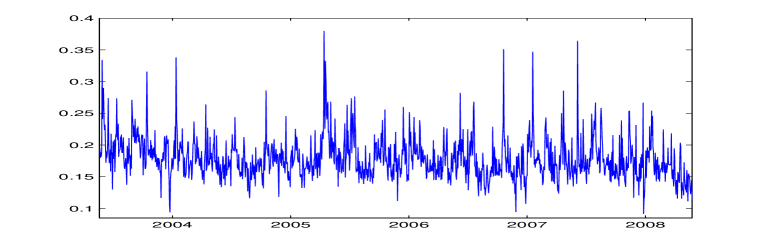

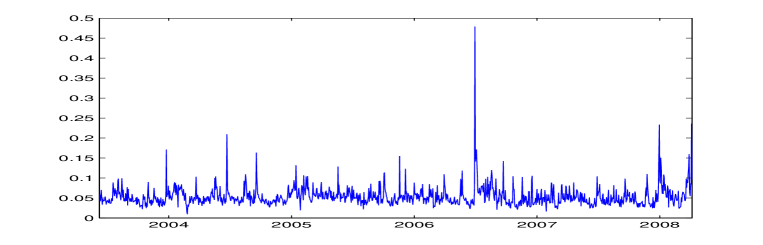

Table 4 presents the estimated parameter values for the IBM and MSFT stocks. In the IBM case, for example, the parameters imply that there are on average jumps per day each with mean and standard deviation . Typical volatility is with standard deviation The proportionality of trading volume and the instantaneous variance is given by The leverage is very small.

5.2 Returns distribution

The estimated parameters in the IBM case, for example, imply that the mean of daily log-returns including or not a leverage effect in the model equal and respectively. If the trading volume process jumps by a typical size, the returns jump by Using the estimated parameters, the volatility processes for the IBM and MSFT stocks are shown in Figure 6. In Table 5 some results on the marginal moments of daily log returns and the instantaneous variance process using the estimated model parameters are presented. Furthermore, the theoretical density and log density of log returns and the estimated ones are shown in Figure 15 and Figure 16. A systematic method how to calculate the theoretical density of log returns is given in Appendix A.

5.3 The autocorrelation function

The theoretical autocorrelation function for the variance process and the estimated autocorrelation for both the stocks are shown in Figure 7 which is not very satisfactory. We will address this issue in the concluding remarks below.

| Parameter | Value IBM | St.dev. |

|---|---|---|

| 6.17 | 0.339 | |

| 1.42 | 0.079 | |

| 177.95 | 12.509 | |

| 0.435 | 0.254 | |

| -0.015 | 0.072 | |

| 0.087 | 0.002 | |

| -0.00056 | 0.0002 |

| Parameter | Value MSFT | St.dev. |

|---|---|---|

| 4.496 | 0.247 | |

| 67.895 | 3.773 | |

| 201.99 | 14.420 | |

| 0.4162 | 0.265 | |

| -0.464 | 5.059 | |

| 0.81 | 0.018 | |

| -0.025 | 0.013 |

| Unconditional moments IBM | Value |

|---|---|

| Unconditional moments MSFT | Value |

|---|---|

5.4 The model fit

To investigate the model fit, we performed a Ljung-Box test for squared residuals of the data set. The test statistic used lags of the corresponding empirical autocorrelation function. The null hypothesis was not rejected for MSFT at the level. For the MSFT squared residuals the p-value was The test statistic for the IBM squared residuals was equal to which led to a rejection of the null hypothesis, since the test had a critical value of at the level. This result is also obvious from Figure 8 where the empirical autocorrelation function of the squared residuals is plotted, showing significant correlations of the IBM residuals. The empirical autocorrelation functions of the squared residuals for MSFT is shown in Figure 9. Furthermore, the autocorrelation functions of for both the stocks are shown in Figure 14.

The estimated mean, standard deviation, skewness and kurtosis of the residuals for both the stocks are summarized in Table 6.

| mean() | std() | skew() | kurt() | |

|---|---|---|---|---|

| IBM | ||||

| MSFT |

The numbers show that the mean and variation of the residuals are according to our model, but the residuals seem to have heavier tails than the normal distribution, see Figure 10 and Figure 11. The IBM residuals pass the Kolmogorov-Smirnov test of normality222In [Lin07] a similar approach is used, with number of trades as a measure of trading intensity. In that work, superposition of two OU-processes are analyzed for the modelling procedure, but without a leverage in the specification of returns. It is also pointed out that typically their approach gives normalized returns with heavier tails than the normal distribution for illiquid stocks and for special dates such as the trading day before a holiday., for example, with p-value whereas the test statistic for the MSFT residuals was equal to , which lead to a rejection of the null hypothesis, since the test had a critical value of at the level. Log returns for the IBM and MSFT stocks and their residuals are shown in Figure 12 and Figure 13.

6 Conclusion and further developments

We introduce a new variant of the Barndorff-Nielsen and Shephard stochastic volatility model where the non Gaussian Ornstein-Uhlenbeck process describes some measure of trading intensity like trading volume or number of trades instead of unobservable instantaneous variance.

This allows us to implement a martingale estimating function approach and obtain an explicit consistent and asymptotically normal estimator. We first perform the numerical finite sample experiment to assess the quality of our procedure and then apply the obtained results to real stock data.

According to the residual analysis and to the return distribution, the model fit is in many aspects quite satisfactory except for the autocorrelation function of the trading volume. The graph indicates that superposition of OU-processes could be used for a more accurate description of the autocorrelation function, see also [Lin07, GS06], but it is not clear how to extend the martingale estimating function approach in this direction. This is left open for future research.

In this paper the empirical analysis uses trading volume. It would be interesting to compare the results to a similar analysis using number of trades as suggested by [Lin07].

The present analysis was performed for daily data, but the approach applies for any sampling frequency since it is based on the continuous time specification of the Barndorff-Nielsen and Shephard model. In particular, the approach could be applied directly to high frequency data.

Further and alternative developments like optimal quadratic estimating functions, use of trigonometric moments and comparison to the generalized method of moments suggested in [HP07] apply also to the present framework.

Appendix A Some numerical and analytical aspects of the density function of log returns

In this section we compute and analyze in detail the distribution and the density function of log returns . By stationarity, it is sufficient to show the results for . The main tool for the computation is the well-known key formula, see for example [NV03, ER99].

A.1 Cumulant of

A.2 Cumulant of

A.3 Cumulant of

Finally, we are able to calculate the cumulant function of log returns according to the obtained expressions of bivariate cumulants in sections A.1 and A.2. Furthermore, using relation (21) and the key formula it follows that

Since in the -OU case we have that

integrating out the cumulant function of it follows that

Furthermore, the density function of log returns will be calculated by Laplace inversion. Denoting the density function of log returns by we have

| (55) |

where denotes the real part of a complex number. The numerical integration is performed in MATLAB using the function quadgk.

References

- [BNS01] Ole E. Barndorff-Nielsen and Neil Shephard. Non-Gaussian Ornstein-Uhlenbeck-based models and some of their uses in financial economics. J. R. Stat. Soc. Ser. B Stat. Methodol., 63(2):167–241, 2001.

- [BS95] Bo Martin Bibby and Michael Sørensen. Martingale estimation functions for discretely observed diffusion processes. Bernoulli, 1(1-2):17–39, 1995.

- [ER99] Ernst Eberlein and Sebastian Raible. Term structure models driven by general Lévy processes. Math. Finance, 9(1):31–53, 1999.

- [GS06] James E. Griffin and Mark F.J. Steel. Inference with non-Gaussian Ornstein-Uhlenbeck processes for stochastic volatility. Journal of Econometrics, 134:605–644, 2006.

- [GT92] Rossi P.E. Gallant, A. R. and G. Tauchen. Stock prices and volume. Review of Financial Studies, 5:199–242, 1992.

- [HP06] Friedrich Hubalek and Petra Posedel. Asymptotic analysis for an optimal estimating function for Barndorff-Nielsen and Shephard stochastic volatility models. Work in progress, 2006.

- [HP07] Friedrich Hubalek and Petra Posedel. Asymptotic analysis for a simple explicit estimator in Barndorff-Nielsen and Shephard stochastic volatility models. Thiele Research Report 2007-05. Submitted, 2007.

- [Jac01] Martin Jacobsen. Discretely observed diffusions: classes of estimating functions and small -optimality. Scand. J. Statist., 28(1):123–149, 2001.

- [JL94] Kaul G. Jones, C. and M.L. Lipson. Transactions, volume and volatility. Review of Financial Studies, 7:631–651, 1994.

- [Kar87] J. M. Karpoff. The relation between price changes and trading volume: a survey. Journal of Financial and Quantitative Analysis, 22:109–126, 1987.

- [Kes00] Mathieu Kessler. Simple and explicit estimating functions for a discretely observed diffusion process. Scand. J. Statist., 27(1):65–82, 2000.

- [KP02] Mathieu Kessler and Silvestre Paredes. Computational aspects related to martingale estimating functions for a discretely observed diffusion. Scand. J. Statist., 29(3):425–440, 2002.

- [KS99] Mathieu Kessler and Michael Sørensen. Estimating equations based on eigenfunctions for a discretely observed diffusion process. Bernoulli, 5(2):299–314, 1999.

- [Lin07] Carl Lindberg. The estimation of the Barndorff-Nielsen and Shephard model from daily data based on measures of trading intensity. www.intersience.wiley.com, 2007.

- [NV03] Elisa Nicolato and Emmanouil Venardos. Option pricing in stochastic volatility models of the Ornstein-Uhlenbeck type. Math. Finance, 13(4):445–466, 2003.

- [Sø99] Michael Sørensen. On asymptotics of estimating functions. Brazilian Journal of Probability and Statistics, (13):111–136, 1999.

- [Uch04] Masayuki Uchida. Estimation for discretely observed small diffusions based on approximate martingale estimating functions. Scand. J. Statist., 31(4):553–566, 2004.