Informed Traders

Abstract

statistical arbitrage; asymmetric information; information-based asset pricing; hedge funds; insider trading; mutual information An asymmetric information model is introduced for the situation in which there is a small agent who is more susceptible to the flow of information in the market than the general market participant, and who tries to implement strategies based on the additional information. In this model market participants have access to a stream of noisy information concerning the future return of an asset, whereas the informed trader has access to a further information source which is obscured by an additional noise that may be correlated with the market noise. The informed trader uses the extraneous information source to seek statistical arbitrage opportunities, while at the same time accommodating the additional risk. The amount of information available to the general market participant concerning the asset return is measured by the mutual information of the asset price and the associated cash flow. The worth of the additional information source is then measured in terms of the difference of mutual information between the general market participant and the informed trader. This difference is shown to be nonnegative when the signal-to-noise ratio of the information flow is known in advance. Explicit trading strategies leading to statistical arbitrage opportunities, taking advantage of the additional information, are constructed, illustrating how excess information can be translated into profit.

1 Introduction

There are many different approaches to the modelling of so-called insider trading strategies. Starting with the work of Kyle (1985) and Back (1992), a number of investigations have been carried out (to name a few, Amendinger et al. 1998, Seyhun 1988, Föllmer et al. 1999, Back et al. 2000, León et al. 2003, Corcuera et al. 2004, Biagini & Øksendal 2005, 2006, Ankirchner et al. 2006, Campi & Çetin 2007). It is sometimes assumed in the literature that the ‘insider’ has direct access to the values of future asset prices. While such a scenario may indeed occasionally prevail, the more common situation is that informed agents do not have advance access to the exact values of future asset prices. How, then, do agents having high information susceptibility—when compared to the average market participant—utilise their strengths in reality? An increasingly popular strategy adopted by some large hedge funds is to make use of publicly available information in addition to high-frequency price data. What gives these funds an edge is their significant computational power for data and text mining, thus allowing them to extract useful information from publicly available sources faster than their competitors. Against this background it is natural to ask how much added information an extra source provides, how does it affect trading strategies, and more generally in what way can such information-based strategies be modelled mathematically.

The purpose of the present paper is: (i) to introduce a phenomenological approach to model the agent susceptive to information, (ii) to quantify the amount of added information, and (iii) to derive trading strategies that lead to statistical arbitrage opportunities for such an agent. Our analysis is carried out within the information-based asset pricing framework of Brody, Hughston and Macrina (Macrina 2006; Brody et al. 2007, 2008a,b; Rutkowski & Yu 2007; Hughston & Macrina 2008). In this framework—hereafter referred to as the BHM framework—the price process of an asset is derived from the specification of (a) future cash flows associated with the asset, and (b) the flow of information accessible to market participants. The price is then given by the discounted risk-adjusted expectation of the cash flows conditional on the available information.

The simplest model that arises in the BHM framework is briefly reviewed in §2. In this setup the asset is characterised by a contract that delivers a single random cash flow at a predesignated time. Such an asset can be interpreted as having the structure of a credit-risky discount bond. In §3 we consider the problem of quantifying the amount of information contained in the bond price concerning the value of the future bond payout. To this end we determine the mutual information (Yaglom & Yaglom 1983, Cover & Thomas 1999) of these two random variables. Initially the market has no information, beyond that already implicit in the asset price, concerning the value of the cash flow. However, as time goes by, the market gathers information. When the amount of information reaches the level of the initial entropy of the cash flow, the market finally ‘learns’ what the value of the cash flow is. The information-theoretic analysis is extended in §4 where we show that the mutual information at time is given by the initial uncertainty, less the expected uncertainty that remains at that time.

In §5 a simple model for an informed trader is introduced. In our approach the informed trader is more susceptive to the flow of market information than other market participants, and thus on average is able to estimate the value of the impending cash flow more quickly and accurately than the other market participants. Simulation studies show a comparison of the sample paths for the market price process and the corresponding valuations made by the informed trader, revealing various intuitive as well as counterintuitive properties of these processes. The dynamics of the valuations estimated by the informed trader are worked out in §6, where we obtain the associated innovations representation. With a basic model for an informed trader at hand we are able to quantify the amount of added information held by the trader. This is worked out in §7, where we construct an elementary trading strategy making use of the additional information, demonstrating the existence of statistical arbitrage opportunities in such circumstances.

2 Information and asset pricing

The simplest model arising in the BHM framework can be summarised thus. We fix a probability space , where denotes the risk-neutral measure. We write for expectation with respect to . The market is not assumed complete, but we assume the absence of arbitrage and the existence of an established pricing kernel—these assumptions ensure the existence of a preferred pricing measure (cf. Cochrane 2005). We let denote the random cash flow associated with the asset and paid at time (for example, the payout of a credit-risky discount bond). Before time market participants do not have direct access to the value of the cash flow. We assume nevertheless that partial information concerning the value of , obscured by the market noise, can be obtained before time . This noisy ‘observation’ of generates the market filtration , and the price at time is given by the risk-neutral expectation of the discounted cash flow, conditional on .

We assume that the ‘signal’ of the noisy observation concerning is revealed to the market at a constant rate , that the ‘noise’ is generated by an independent Brownian bridge process , and that the market filtration is generated by an information process defined for by

| (1) |

In other words, . The use of a bridge process for the noise is motivated by the idea that at time all the available information about is incorporated into the a priori distribution, and that at time the value of is revealed and there is no remaining noise: the choice of a Brownian bridge is made for simplicity and tractability. If we further assume that the default-free system of interest rates is deterministic and let denote the price at time of a discount bond that matures at , then the price of the credit-risky discount bond at time is given by . In the case where takes the discrete values with the a priori probabilities , a calculation shows that

| (2) |

This follows from the fact that the conditional risk-neutral probability defined by takes the form

| (3) |

By taking the stochastic differential of (2) one finds that the dynamical equation satisfied by the bond price is

| (4) |

where , and where the process defined by the expression

| (5) |

turns out to be a standard -Brownian motion. Here denotes the conditional expectation of the cash flow , and

| (6) |

is the conditional variance of (see Macrina 2006 and Brody et al. 2007 for derivations of the foregoing results).

We observe that in the information-based framework it is possible to deduce the diffusive dynamics (4) for the price process, starting from the specification of the cash flow and the information process . The theme that underlies this framework is that the market acts as a ‘signal processor’ for future cash flows so as to generate the dynamics of asset prices. This point of view is natural as a basis for understanding the elements of price formation, since investment decisions are often made in accordance with the perceptions of market participants concerning the future cash flows associated with the given asset.

As far as the market filtration is concerned, the information contained in is equivalent to that in : we have . This follows from the fact that one can write , where

| (7) |

from which by differentiation we deduce that

| (8) |

which is positive. Therefore, is monotonically increasing in , and hence invertible. It follows that from knowledge of the trajectory one can construct ; conversely from knowledge of the trajectory one can construct .

3 Amount of information about the future cash flow contained in the price process

We would like to quantify how much information regarding the value of the cash flow is contained in the value at time of the information process (1). A reasonable measure for such quantification is given by the mutual information between the two random variables (Shannon & Weaver 1949; Gel’fand et al. 1956; Gel’fand & Yaglom 1957), which in the present context is given by the expression

| (9) |

where

| (10) |

is the joint density function of the random variables , and and are the respective marginal probabilities. By use of the relation

| (11) |

we deduce that

| (12) |

since conditional on the random variable is normally distributed with mean and variance . From (12) the marginal densities

| (13) |

can be deduced at once. In particular, we have , as it should be.

An alternative way of deriving the mutual information in this context is to make use of the identity

| (14) |

Here is the entropy of the random variable (Wiener 1948, Khintchine 1953), and is the entropy of conditional on . The conditional density function , , is defined by . Since conditional on the random variables and are both normally distributed, with the same variance , and since the entropy of a normally distributed random variable is independent of its mean, we find that . In other words, the mutual information in the present context is given by the difference of the two entropies:

| (15) |

As a consequence, the information about the cash flow contained in can be determined (a different approach to extracting information concerning the asymptotic dividend stream from option price data is considered in Geman et al. 2007).

From an information-theoretic point of view a pair of processes related through an invertible smooth function, and thus sharing the same filtration, in general possess different information content (entropy). On the other hand, since what is directly observed in the market is the price , which is an invertible function of , one might argue that it is more relevant to determine the mutual information , that is, the amount of information about the future cash flow contained in the market price. However, since mutual information is given by a difference of entropies, and since changes in the two entropies resulting from the transform cancel, we have . Therefore, the amount of information about contained in is given by (15).

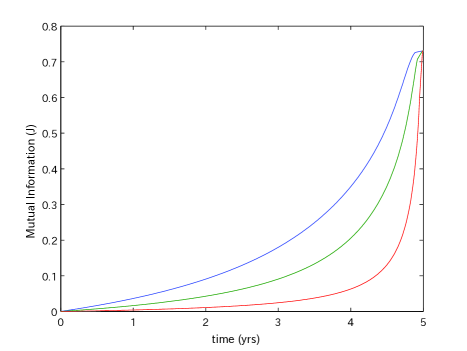

In Figure 1 we plot the mutual information as a function of for three values of the information flow-rate parameter . The information gained by market participants increases more rapidly as is raised. On the other hand, the dynamical relation (4) shows that the value of determines the overall magnitude of the price volatility. Thus it is possible to quantify the market information gain and compare this with the price volatility.

To see how entropy transforms under a nonlinear invertible map, suppose that is a random variable with density , and that is another random variable given by , where is smooth and invertible. Then the density function for is given by . Substituting this in and changing variables by setting , we find that . As a consequence, we have

| (16) |

where . The advantage of this expression is that we need not determine the inverse of the function defined in (7) in order to calculate . From (8) it follows that

| (17) |

In other words, the difference between and is the average log-volatility of the price process at time .

4 Analysis of information measures

We proceed in this section to consider the Shannon-Wiener entropy associated with the conditional risk-neutral probabilities. Analysis of the entropy leads to insights into the qualitative behaviour of the asset price volatility. The Shannon-Wiener entropy is defined by the expression

| (18) |

We shall demonstrate that the mutual information (9) and the Shannon-Wiener entropy (18) are related as follows:

| (19) |

Thus, the mutual information at time is given by the initial uncertainty, less the expected uncertainty that still remains at that time.

The derivation of (19) proceeds in two steps. First we shall show that

| (20) |

and then we shall show that

| (21) |

Proof of (20). Let us begin by deriving the dynamical equation satisfied by the Shannon-Wiener entropy. From (3) and (5) we find that the conditional probability satisfies

| (22) |

It follows, by an application of Ito’s lemma to (18), that

| (23) |

Taking the expectation of both sides of (23), we obtain (20), as desired.

Proof of (21). In Gel’fand & Yaglom (1957) it is shown that the mutual information can be expressed as the expectation of the log density of the joint measure with respect to the product measure :

| (24) |

We are thus required to determine the relevant Radon-Nikodym derivative. We shall follow the line of argument presented in Davis (1978) (see, also, Duncan 1970). To proceed, we require the introduction of an auxiliary measure introduced in Macrina (2006) and Brody et al. (2007, 2008a). This is the so-called bridge measure under which the information process becomes a Brownian bridge. The argument goes as follows. We fix the probability space with a filtration , and introduce a -Brownian motion such that the Brownian bridge appearing in (1) is given by

| (25) |

This is the standard integral representation for a Brownian bridge (see, e.g., Hida 1980, Protter 2005). Setting we define

| (26) |

where is -independent of and is -measurable. For fixed we introduce the measure on by writing

| (27) |

Then the process defined by

| (28) |

is a -Brownian motion, since is bounded for any .

Under we find that the distribution of is same as it is under , that and are independent, and that is a -Brownian bridge (cf. Brody et al. 2008a). To see these, recall that since and , and hence and , are independent, the probability law of conditional on remains that of a Brownian motion. Now take a bounded function and consider

| (29) |

Conditional on , takes the form of a Girsanov exponential, since is a -Brownian motion. Therefore, the inner expectation equals unity, and we find

| (30) |

for every bounded function . In other words, has the same probability law under and . In a similar manner, for any sequence of times and any bounded function we wish to calculate

| (31) |

By the same argument as above, for each the process is Brownian under the measure whose density is . Since itself is Brownian under we have

| (32) |

and hence

| (33) |

However, and coincide on so that , from which it follows that and are -independent. By combining (25) and (28) we get

| (34) |

Eliminating by use of we obtain the relation

| (35) |

which is the dynamical equation satisfied by a Brownian bridge in the measure.

Let be the map: . Then the joint sample space measure of is for any measurable set , and the sample space measure of is for any measurable set . However, since and are independent under , and is a -Brownian bridge, we have . It follows from (26) that

| (36) |

Substituting (28) in here we thus deduce that

| (37) |

Turning to the innovations representation (5) we find, along with (35), that and are related according to

| (38) |

Thus, following a similar line of argument we obtain

| (39) |

which is a version of the likelihood ratio formula of Kailath (1971). The measure thus corresponds to the ‘signal present’ situation, while the ‘signal absent’ case corresponds to being pure bridge noise with measure . Combining (37) and (39), and making use of (28), we deduce

| (40) |

Taking the expectation of the logarithm of this, bearing in mind that is a -Brownian motion, we recover (21), as claimed.

The entropy process has the property that . This follows from the fact that the conditional probability process has the limiting behaviour

| (41) |

for . The proof of (41) is as follows. Let be fixed, and suppose that for some . For this realisation of the information process is given by . Substituting this expression for into (3) and dividing the denominator and the numerator by the exponential factor appearing in the numerator, we deduce that

| (42) |

Observe that all of the terms in the sum in the denominator vanish as approaches , and therefore . It follows that for , and thus (41). Finally, since by (18) and since , we deduce that .

If we let approach in (20) we find the following relation:

| (43) |

Since is bounded by , where is the number of values can take, and since the coefficient of the conditional variance in the integrand diverges quadratically as approaches , this relation shows that the variance process has to decay sufficiently rapidly to ensure the existence of the right side of (43). On the other hand, the conditional variance also generates the random movement of the asset price volatility in (4). As a consequence we are able to obtain a crude estimate of the magnitude of the cumulative volatility. It is worth noting that in models based on Brownian noise the entropy and mutual information are closely related to prices of variance or volatility derivatives. A related observation has been made by Soklakov (2008).

It should be remarked that the limiting behaviour is specific to the case in which takes discrete values. If is a continuous random variable, then the associated entropy has the property that , which can be seen from the Hirschman inequality in Fourier analysis (Beckner 1975):

| (44) |

It follows from (23) that the variance process in this case does not vanish sufficiently rapidly to ensure finiteness of the right side of (20) as approaches . In other words, there is a qualitative difference in the behaviour of the volatility process, depending on whether the cash flow is a continuous or discrete random variable. In particular, volatility products may be overpriced in models based on continuous cash flows, since real market cash flows are not continuous.

5 A model for an informed trader

In the previous sections we have examined the BHM framework from an information theoretic perspective. In particular, we have been able to quantify the amount of information about the future cash flow of an asset contained in its price. We turn now to consider a model for an informed trader who has access to an additional information source, apart from the price process itself, concerning the future return of an asset. We assume that the informed trader is ‘small’ in the sense that access to the additional information is limited, and that the actions of the informed trader will not impact the price process. In other words, the model is not for a large number of small agents; rather, it is for a single agent, or a highly restricted number of agents, who carefully execute their trading strategies, taking advantage of the additional information.

One might expect that the use of additional information gives a definite advantage for the trader. This, however, is not necessarily the case: additional information is in general obscured by additional noise. As a consequence, the valuation process estimated by the informed trader can entail higher volatility than the actual market price movements. It follows that any strategy making use of additional information will tend to embody additional risk. Nevertheless, on average such strategies are expected to outperform the market, and this is the idea behind some of the statistical arbitrage strategies adopted by hedge funds.

The BHM framework is sufficiently flexible to model this kind of scenario. Indeed, the use of this framework as a basis for the development of insider-trading models was recognised early on (Macrina 2006). Our intention here is to apply such ideas to describe the disparity in the ability of processing publicly available information, and to illustrate how statistical arbitrage opportunities can be seen to arise in a simple model. It should be emphasised that many of the simplifying assumptions—that the asset entails a single cash flow; that the information flow rates are constants; that the interest rate is deterministic; and that the noises are modelled by Brownian bridges—can be relaxed without affecting the main qualitative features of the model.

We assume the setup for the market outlined in §2. However, in addition there is an informed trader who has a further noisy information source represented by the information process

| (45) |

The noise term may or may not be correlated with the market noise . We let and be a pair of Brownian motions with correlation , and define the associated Brownian bridges by

| (46) |

In this way we can model the two noise terms with fair amount of generality (we may use alternatively the integral representation (25) to construct the bridge processes; however, the choice (46) is more suitable for simulation purposes), since determines the correlation of and . In particular, if then the informed trader has two linear equations (1) and (45) for the two unknowns and ; hence the value of the future cash flow will become instantly accessible to the trader (assuming ). This situation corresponds to the fully-informed conventional ‘insider’ often considered in the literature. The other extreme, for which , is of interest, since the informed trader must choose a strategy optimally so as not to be overwhelmed by the additional noise.

We let denote the filtration generated by . If , then knowledge of the value of is revealed at a faster rate in the ‘primed’ filtration. This, however, does not mean that is contained in even if ; the two filtrations are merely inequivalent. On the other hand, since the informed trader also has access to the price process, which is adapted to , it is reasonable to assume that the information source is given by . We assume that the additional information commences at time ; hence the a priori probabilities for to take the values remain the same. This assumption may seem limiting; however, it is not unreasonable since the ‘lifetime’ of the extra information, i.e. the period over which extra information has value, is often short in practice.

The informed trader will use the extra information to work out the price that the market would have made had been accessible to general market participants. We shall now calculate the valuation process made by the informed trader on this basis. From the Markov property of the joint information process we find that the informed valuation process is given by

| (47) |

where . By use of the Bayes formula

| (48) |

where the conditional density is given by the bivariate normal density function

| (49) |

we deduce that

| (50) |

Here we set , , , and .

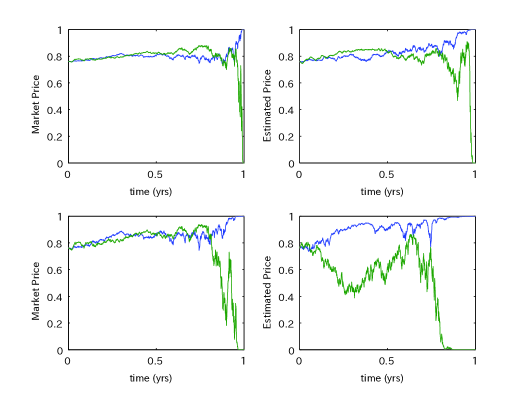

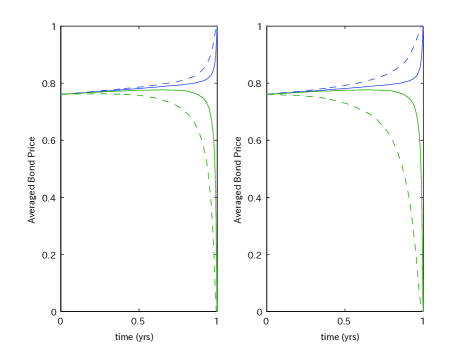

The process (50) is our model for the valuations made by the informed trader. It is straightforward to simulate the informed valuation process and compare this against the uninformed market price process . By suitably adjusting the values for , , and we are able to confirm various intuitive aspects of the behaviour of these processes; some examples are displayed in Figure 2. With respect to any given sample path the expected price of the informed trader at time may be less accurate (by ‘accurate’ we mean close to the true value) than the market price. However, on average the valuation determined by the informed trader converges more rapidly to the true value of the bond. This is illustrated in Figure 3 where we plot the averaged sample paths conditional on the given outcome.

The plot on the right side of Figure 3 indicates that the performance of the informed trader is high even if the signal-to-noise ratio of the additional information source is set to zero (and hence is pure noise). In fact the quality of the estimate decreases as the value of is raised from zero, until it reaches the critical level . Putting the matter differently, the quality of the estimate made by an informed trader is not monotonic in the signal-to-noise ratio of the additional information source. This feature may appear counterintuitive, but it can be understood by rearrangement of terms in (50) into a form analogous to (22):

| (51) |

Here we write . This expression shows that the exponential rate of convergence for the process to approach the ‘true’ value is governed by the ratio . In particular, for fixed and this ratio takes a minimum value at . When , the linear equations and become closest to being degenerate, and hence the value of the additional information is minimised.

6 Innovations and the dynamics of informed valuations

Our objective now is to obtain an innovations representation for the valuations made by the informed trader. For this purpose it suffices to derive the dynamical equation satisfied by the ‘insider’ valuation , or equivalently, by the conditional probability . The calculation simplifies if we express (50) in the form

| (52) |

Here the process

| (53) |

represents the ‘enhanced’ information being effectively received by the informed trader, with the modified bridge noise

| (54) |

Applying Ito’s lemma to (48) and making use of (53), we find that

| (55) |

where . The process appearing in (55) is defined by

| (56) |

By following a line of argument similar to that presented in Brody et al. (2007) it can be shown that is a standard -Brownian motion. It follows that the valuation process of the informed trader obeys the following dynamical equation:

| (57) |

where the volatility process is given by

| (58) |

and denotes the variance of conditional on .

The fact that the information accessible to the informed trader can be ‘compactified’ into a single enhanced information can be understood as follows. Since the noise processes and have correlation , one can write

| (59) |

where the Brownian bridge process is taken to be independent of . Similarly, we can decompose the extra information in the form

| (60) |

where and . It should be evident that the filtration generated jointly by is equivalent to that generated jointly by . However, the information processes and have independent noises. To proceed we note that the process defined by

| (61) |

is purely noise, and is independent of . We can construct a new Brownian bridge that is independent of this noise. A standard orthogonalisation shows that this is given by the bridge process defined by (54). It follows that the enhanced information process defined by (53) is independent of . Furthermore, the filtration generated jointly by is equivalent to that generated jointly by . Since provides no useful information about , i.e. , the informed trader in effect has as the primary basis for valuation.

This line of argument, making use of the orthogonalisation procedure, extends more generally to the case where there are multiple information processes relating to the cash flow : Starting with a family of processes with signal-to-noise ratios one orthogonalises the associated noises. The result is a new set of information processes with signal-to-noise ratios . Then the information process that the informed trader uses as a basis for valuation can be represented by a single effective information process with the enhanced signal-to-noise ratio .

7 Additional information held by the informed trader and statistical arbitrage strategies exploiting this

We are in a position to quantify the amount of excess information held by the informed trader above that of the market. This is measured by the difference of the mutual information:

| (62) |

By the argument in §3, the mutual information of the informed trader is given by an entropy difference of the form

| (63) |

The entropy of the ‘insider’ information is determined by the marginal density of , whereas the conditional entropy is the entropy of a Brownian bridge.

Following the line of argument presented in §4 we are able to represent the mutual information difference in terms of the expected entropy differences:

| (64) |

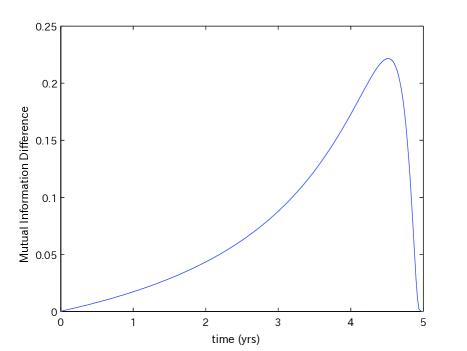

where . This expression makes it apparent that is nonnegative, since the entropy characterises the amount of uncertainty concerning the value of the cash flow , and for any this uncertainty is greater on average for the general market participant than for the informed trader. In Figure 4 we plot an example of , indicating the way in which the excess information held by the informed trader changes in time.

Given that the informed trader is on average ‘more knowledgable’ than the general market participant it is natural to ask how this advantage can be turned into profit. One of the issues that can be addressed in this connection is the derivation of optimal trading strategies. For such an analysis one may need to introduce additional structure into the problem in the form of a suitable criterion for optimality and a specification of the market price of risk. In the present investigation, we confine the discussion to a demonstration, supported by simulation studies, of how even very simple strategies can yield statistical arbitrage opportunities by outperforming the market.

For example, suppose we consider a strategy such that at some designated time a market trader purchases a digital bond iff at that time the bond price is greater than for some specified threshold . The value of can be regarded as the risk aversion level of the trader. An informed trader follows the same rule, but makes a better estimate for the value of the bond, and hence purchases the bond iff . In either case a bond that is purchased will be held until maturity. That such a strategy leads to a statistical arbitrage opportunity for the informed trader can be seen as follows. We assume that the initial position of the trader is zero, i.e. purchase of a digital bond at requires borrowing the amount at that time, and repaying the amount at . Thus the value of the market trader’s portfolio at is

| (65) |

whereas the terminal value of the informed trader’s portfolio is

| (66) |

Consider now the present value of a security that delivers a cash flow equal to the excess P&L generated by the strategy of the informed trader. By use of the tower property we have ; but

| (67) |

since the random variables and are both -measurable. If then is nonnegative, whereas if then is nonpositive. It follows that is a nonnegative random variable, and hence , since with probability greater than zero. Therefore, the informed trader can execute a transaction at zero cost that has positive value, and this is what we mean by ‘statistical arbitrage’.

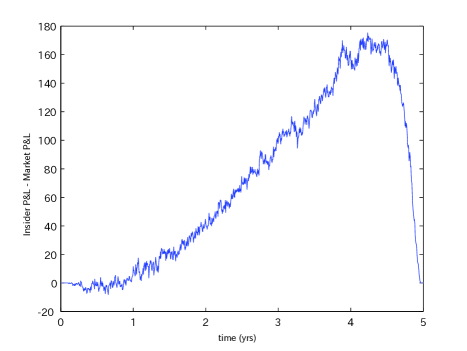

We have examined the profit and loss (P&L) profile, both for a general market trader and for an informed trader, resulting from the repeated application of such a strategy. The results are plotted in Figure 5. In particular, we consider 2000 realisations (sample paths) for the information processes governing the bond price valuations. For each fixed we calculate the total P&L for the informed trader and for the market trader obtained by following the specified strategy over and over for each of the 2000 independent sample paths. For each fixed , we chart in Figure 5 the difference between the total P&L of the informed trader and that of the market trader. Providing that the strategy is executed after enough time has passed for the informed trader to gain an informational advantage, we find that the difference between the P&L of the informed trader and that of the market trader is always positive. Furthermore, the qualitative behaviour of the resulting P&L difference is in agreement with the qualitative behaviour of the magnitude of the excess information possessed by the informed trader indicated in Figure 4 (we have chosen the same parameter values for these two figures to allow for direct comparison).

Our objective has been to demonstrate how statistical arbitrage strategies arise in a market characterised by heterogeneous information flow. It is interesting that a qualitatively similar behaviour for the excess information and the excess P&L is observed in the case of the rather primitive strategy we have considered here. There are many ways in which one can improve upon the trading strategy examined above. An important open issue is to determine the optimal trading strategy, subject to suitable optimality criteria, that exploits the excess information. We conclude by remarking that a related approach to the modelling of insider trading within the information-based framework is suggested in Macrina (2006), where the asset return is modelled as being dependent on more than one market factor, for which only some of the associated information processes are accessible to the market. It would be of interest to examine whether the kind of hedge fund strategy considered here is also applicable in a setup involving multiple market factors.

Acknowledgements.

We thank J. Z. Kelly, A. Macrina, B. K. Meister, and M. F. Parry for stimulating discussions.References

- [1]

- [2] Amendinger, J., Imkeller, P. & Schweizer, M. 1998 Additional logarithmic utility of an insider. Stochast. Process. Appl. 75 263-286. (doi:10.1016/S0304-4149(98)00014-3)

- [3]

- [4] Ankirchner, S., Dereich, S. & Imkeller, P. 2006 The Shannon information of filtrations and the additional logarithmic utility of insiders. Ann. Probab. 34, 743-778. (doi:10.1214/009117905000000648)

- [5]

- [6] Back, K. 1992 Insider trading in continuous time. Rev. Financial Stud. 5, 387-409. (doi:10.1093/rfs/5.3.387)

- [7]

- [8] Back, K., Cao, C. H. & Willard, G. A. 2000 Imperfect competition among informed traders. J. Finance 55, 2117-2155. (doi:10.1111/0022-1082.00282)

- [9]

- [10] Biagini, F. & Øksendal, B. 2005 A general stochastic calculus approach to insider trading. Appl. Math. Optim. 52, 167-181. (doi:10.1007/s00245-005-0825-2)

- [11]

- [12] Biagini, F. & Øksendal, B. 2006 Minimal variance hedging for insider trading. Int. J. Theo. Appl. Fin. 9, 1351-1375. (doi:10.1142/S0219024906003998)

- [13]

- [14] Brody, D. C., Hughston, L. P. & Macrina, A. 2007 Beyond hazard rates: a new framework to credit risk modelling. In Advances in Mathematical Finance (eds M. Fu, R. Jarrow, J.-Y. J. Yen, & R. Elliott), 231-257. Basel, Switzerland: Birkhäuser. (doi:10.1007/978-0-8176-4545-813)

- [15]

- [16] Brody, D. C., Hughston, L. P. & Macrina, A. 2008a Information-based asset pricing. Int. J. Theo. Appl. Fin. 11, 107-142. (doi:10.1142/S0219024908004749)

- [17]

- [18] Brody, D. C., Hughston, L. P. & Macrina, A. 2008b Dam rain and cumulative gain. Proc. R. Soc. London A464, 1801-1822. (doi:10.1098/rspa.2007.0273)

- [19]

- [20] Campi, L. & Çetin, U. 2007 Insider trading in an equilibrium model with default: a passage from reduced-form to structural modelling. Finance Stoch. 11, 591-602. (doi:10.1007/s00780-007-0038-4)

- [21]

- [22] Cochrane, J. H. 2005 Asset Pricing Princeton, NJ: Princeton University Press.

- [23]

- [24] Corcuera, J. M., Imkeller, P., Kohatsu-Higa, A. & Nualart, D. 2004 Additional utility of insiders with imperfect dynamical information. Finance Stoch. 8, 437-450. (10.1007/s00780-003-0119-y)

- [25]

- [26] Davis, M. H. A. 1978 Detection, mutual information and feedback encoding: applications of stochastic calculus. In Communication systems and random process theory (Proc. 2nd NATO Advanced Study Inst., Darlington, 1977), 705-720. NATO Advanced Study Inst. Ser., Ser. E: Appl. Sci., No. 25. Alphen aan den Rijn: Sijthoff & Noordhoff.

- [27]

- [28] Duncan, T. E. 1970 On the calculation of mutual information. SIAM J. Appl. Math. 19, 215-220. (doi:10.1137/0119020)

- [29]

- [30] Cover, T. M. & Thomas, J. A. 1991 Elements of Information Theory. New York, NY: John Wiley.

- [31]

- [32] Föllmer, H., Wu, C.-T. & Yor, M. 1999 Canonical decomposition of linear transformations of two independent Brownian motions motivated by models of insider trading. Stochastic Process. Appl. 84, 137-164. (doi:10.1016/S0304-4149(99)00057-5)

- [33]

- [34] Gel’fand, I. M., Kolmogorov, A. N. & Yaglom, A. M. 1956 On the general definition of the amount of information. Dokl. Akad. Nauk SSSR 111, 745-748.

- [35]

- [36] Gel’fand, I. M. & Yaglom, A. M. 1957 Calculation of the amount of information about a random function contained in another such function. Uspehi Mat. Nauk 12, 3-52.

- [37]

- [38] Geman, H., Madan, D. B. & Yor, M. 2007 Probing option prices for information. Methodol. Comput. Appl. Probab. 9, 115-131. (doi:10.1007/s11009-006-9005-3)

- [39]

- [40] León, J. A., Navarro, R. & Nualart, D. 2003 An anticipating calculus approach to the utility maximization of an insider. Math. Finance 13, 171-185. (doi:10.1111/1467-9965.00012)

- [41]

- [42] Hida, T. 1980 Brownian Motion. Berlin, Germany: Springer.

- [43]

- [44] Hughston, L. P. & Macrina, A. 2008 Information, inflation, and interest. To appear in Advances in Mathematics of Finance. (ed. L. Stettner), Warsaw, Poland: Banach Centre Publications.

- [45]

- [46] Kailath, T. 1971 The structure of Radon-Nikodým derivatives with respect to Wiener and related measures. Ann. Math. Statist. 42, 1054-1067. (doi:10.1214/aoms/1177693332)

- [47]

- [48] Khintchine, A. Ya. 1953 The concept of entropy in the theory of probability. Uspehi Mat. Nauk 8, 3-20.

- [49]

- [50] Kyle, A. S. 1985. Continuous auctions and insider trading. Econometrica 53, 1315-1335. (http://www.jstor.org/stable/1913210)

- [51]

- [52] Macrina, A. 2006 An information-based framework for asset pricing: -factor theory and its applications. PhD thesis, King’s College London. ArXiv: 0807.2124.

- [53]

- [54] Protter, P. 2005 Stochastic Integration and Differential Equations: A New Approach. 2nd edn., 3rd printing. Berlin, Germany: Springer.

- [55]

- [56] Rutkowski, M. & Yu, N. 2007 An extension of the Brody-Hughston-Macrina approach to modelling of defaultable bonds. Int. J. Theo. Appl. Fin. 10, 557-589. (doi:10.1142/ S0219024907004263)

- [57]

- [58] Seyhun, H. N. 1988 The information content of aggregate insider trading. J. Business 61, 1-24. (doi: 10.1086/296417)

- [59]

- [60] Shannon, C. E. & Weaver, W. 1949 The Mathematical Theory of Communication. Urbana, IL: University of Illinois Press.

- [61]

- [62] Soklakov, A. 2008 Information derivatives. Risk April, 90-94.

- [63]

- [64] Wiener, N. 1948 Cybernetics: or control and communication in the animal and the machine. Cambridge, MA: MIT Press.

- [65]

- [66] Yaglom, A. M. & Yaglom, I. M. 1983 Probability and Information. Delhi, India: Hindustan Publishing Corporation. (Translated from the Russian by V. K. Jain. Originally published as: Veroyatnost~ i informatsiya, 3rd revised and enlarged edition. Moscow: Izdatel’stvo “Nauka”, 1973.)

- [67]