Classification of barrier options

Abstract.

For a given level of accuracy in option prices, the paper considers the problem of deciding when exactly, as one or more of the pricing parameters change, a barrier option degenerates into a simpler type of option. This problem is meaningful in the real world where option prices are always determined within a certain level of accuracy. The problem is reduced to finding certain critical values of the initial stock price, and this is achieved through a probability-based approach.

Key words and phrases:

Key words and phrases:

Critical stock price, Barrier options classification, non-dimensional approximate parameter2000 Mathematics Subject Classification:

91b24, 65c301. Introduction

One of the topics that financial mathematics has been concerned with over the last decades is that of option pricing, and barrier option pricing features prominently among these topics, in particular because barriers can be added to any existing option. In this regard, Merton [18] obtained in the first pricing formula for a European down-and-out call option by solving explicitly the associated differential equation with the appropriate boundary conditions. Latter on in 1985, Cox and Rubistein [8] obtained a similar formula for the up-and-out barrier. Using a probabilistic approach based on certain theoretical results derived earlier on by Levy [16] and by Anderson [1], Kunitomo and Ikeda [15] obtained more general pricing formulas for European double barrier options with curved barriers and for a variety of path-dependent options and corporate securities, some of which had already been independently obtained for restricted cases in [7, 14, 17].

Attempts to extend these pricing formulas to the more complex case of American-style options have been undertaken in papers by Broadie and Detemple [5], Gao et al [11], and Haug [12]. All of these extensions to American-style options have however only lead to close-form approximations. In parallel with the determination of these pricing formulas, numerical methods have been used for pricing barrier options, especially in those cases where analytical pricing solutions remain unavailable, such as for discrete barrier options [3, 4, 9, 10], or for American-style options that, in some cases, comprise transaction costs or stochastic volatilities [2, 11, 6, 13].

An important problem about barrier options that doesn’t seem to have been considered is that of deciding when exactly, for a given level of accuracy in option prices, a double barrier option degenerates into a much elementary type of barrier option, as one or more of the pricing parameters change with time. Although this problem is meaningless in terms of the Brownian motion of the of the underlying asset price, it becomes fully meaningful in the real word where all prices are known only to within a finite number of precision digits. It is also a practical problem in the sense that it can lead to a more efficient pricing of various types of barrier options, and to a better insight into the dynamics of options, and more specifically barrier options.

In this paper, we consider the problem of determining when exactly, as the initial stock price or other pricing parameters evolve, and for a fixed level of accuracy in option prices, a barrier option with a single or a double barrier degenerates into a simpler type of option, which may be, for instance in the case of a double barrier option, a down-and-out or an up-and-out barrier option, or just a vanilla. We consider in this analysis more general types of barriers with time-dependent absorbing boundaries. The problem is reduced to finding certain critical values of the initial asset price, and we use a probabilistic approach to derive close-form approximate solutions for these values. Numerical experiments based on analytical option pricing results such as those from [15] are then implemented, to check the validity of the formulas obtained.

In the next section, we derive formulas for the classifying critical asset prices which in Section are applied to the problem of classification of barrier options. We present the numerical test of these formulas in Section and give some concluding remarks in Section 5. Due to the usual parity considerations, we focus our analysis solely on knock-out barrier options.

2. Classifying critical asset prices

We make the usual assumption that the stock price follows a geometric Brownian motion, or equivalently, that it is lognormally distributed. In this case, the stochastic differential equation satisfied by is given in terms of the standard Wienner process by

| (2.1) |

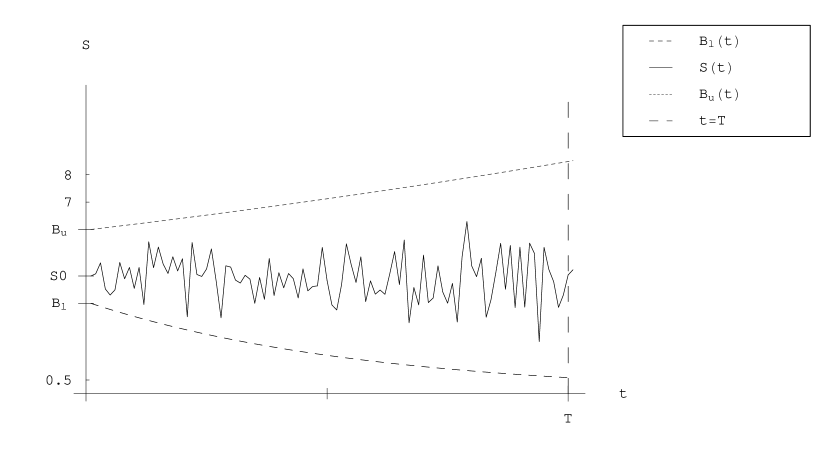

where and are the constant drift and volatility parameters, respectively. Consider two continuous curves and over the time interval such that where , and is a given time. Assume furthermore that the two curves are non-overlapping, so that we have for all A sample path of stock price together with the two adjacent curves are depicted in Figure 1.

Denote by the accuracy in a given option price For simplicity, we may write in the form where is the number of significant digits to the right of the decimal point in Suppose now that is the price of a double knock-out option contingent on with curved barriers and For any option under consideration, unless otherwise stated we denote by the initial price of the underlying asset, by its strike price and by its expiry date. Let be a variable symbol that may take on the value to mean ”upper” or to mean ”lower”. Let be the event that the barrier is breached before the other barrier by time and let be the corresponding rebate paid at the expiry date of the option. If we denote the risk-free interest rate by by the probability operator, and by the risk neutral expectation operator, then the price of the double knock-out option is given by

| (2.2) |

In terms of the geometric Brownian motion of the underlying, the probability that the stock price breaches a barrier before any given time is never zero. Note that the operator is additive with respect to each term in its argument in (2.2). By the same properties of the geometric Brownian motion, by choosing sufficiently far away from an initial barrier value we can make so small that if we let be the difference between the corresponding value of and the value of obtained by setting then This in terms of the accuracy of means that and thus the barrier has therefore no effect on the value of , and the double knock-out option degenerates into a simpler type of option, which may be a down-and-out barrier option if or an up-and-out barrier option if In the real world markets where all prices are determined only in terms of a finite number of precision digits, we may thus assume that the probability of a stock price breaching a barrier before a given time can take on the value zero for appropriately chosen values of the initial price .

It is therefore meaningful to consider the following two complementary problems, for a given accuracy of option prices.

- Problem 1:

-

Find the minimum value of which ensures that the stock price will not breach the lower curve before time

- Problem 2:

-

Find the maximum value of which ensures that the stock price will not breach the upper curve before time

Definition 1.

We say a curve is worthless with respect to the stock price movement over a given time interval and for a given accuracy in stock prices if, with probability the path followed by will not breach the curve (either from above or from below) over that time interval.

In other words, the problem we are interested in is that of finding the minimum (maximum) value of the initial stock price that will ensure that the lower (upper) curve is worthless over Let be the probability that Then by Eq. (2.1) we clearly have

| where | ||||

| (2.3) | ||||

and where is the standard normal distribution function. It is well known that is a positive definite increasing function satisfying However, this convergence of to is very fast and if we denote by the accuracy of then it is easy to see that we have for instance for For a given value of let be the smallest number for which the approximation holds, that is, such that We therefore have if and only if and solving this inequality for shows that

| (2.4a) | ||||

| where | ||||

| (2.4b) | ||||

| and where | ||||

| (2.4c) | ||||

Now, let be the maximum value of the continuous function achieved over the interval Then by compactness we have for some For Eq. (2.4a) shows that for all that is the lower curve is worthless. On the other hand, if then (2.4a) shows again that and thus the lower barrier isn’t worthless. Consequently, is the minimum value of the initial stock price above which the lower curve becomes worthless, that is, is the solution to Problem 1.

Similarly, let be the probability that Then we have

| where | ||||

| (2.5) | ||||

and using again the fact that if and only if it readily follows that

| (2.6a) | ||||

| where | ||||

| (2.6b) | ||||

Consequently, if we let be the minimum value of the continuous function over the interval then it can be shown in a similar manner as in the preceding case for the lower curve that is the maximum value of the initial stock price below which the upper curve is worthless. That is, is the solution to Problem We have thus obtained the following result.

Theorem 1.

Suppose that the stock price follows a geometric Brownian motion of the form (2.1). Suppose also that the two functions and given by (2.4b) and (2.6b), respectively, are continuous and considered over the time interval Let be the maximum value of and the minimum value of Then we have

-

(a)

is the minimum value of the initial stock price above which the curve becomes worthless.

-

(b)

is the maximum value of the initial stock price below which the curve becomes worthless.

3. Applications to barrier options

We now consider more explicitly the problem of determining when exactly a barrier option contingent on a stock price will degenerate into a simpler type of option, as a result of a change in the option’s pricing parameters. All barrier options will be assumed to have, in general curved barriers, and the underlying asset price is supposed to follow a geometric Brownian motion of the form (2.1). We shall also denote by and by the lower barrier and the upper barrier, respectively, and if any, for a given barrier option.

Definition 2.

We say that a barrier option of a given type is a typical barrier of that type if none of its barriers can be considered worthless for the corresponding parameter set. That is, if it cannot be priced as a barrier option of a different type with the same parameter set.

The equations (2.4b) and (2.6b) show that in addition to the parameters of the curved barriers, the critical values and of Theorem 1 depend only on the drift and volatility parameters and of the stock price and on the expiry time In a risk neutral world, we have where is the interest rate and is the continuous dividend yield, if any, paid by the underlying asset. However, the value of is of no importance for our analysis and we may assume without loss of generality that By the fixed parameter set for a given option, we shall therefore refer to the other parameters and as well as the initial asset price , the pay-off function parameters such the strike price and the curved barriers’ parameters.

Theorem 2.

Consider a down-and-out barrier option with (lower ) barrier and a given parameter set.

-

(a)

If the barrier is worthless and the option is equivalent to a vanilla option with the same parameter set.

-

(b)

The option is a typical down-and-out barrier option if and only if

Proof.

Part (a) of the theorem readily follows from the definition of and the fact that a down-and-out option with a worthless barrier is naturally equivalent to a vanilla option with the same parameter set. On the other hand, if there is no certainty that the barrier will not be breached before the expiry date and thus the option is necessarily a typical down-and-out barrier option. ∎

Theorem 3.

Consider an up-and-out barrier option with (upper) barrier and a given parameter set.

-

(a)

If the barrier is worthless and the option is equivalent to a vanilla option with the same parameter set.

-

(b)

The option is a typical up-and-out barrier option if and only if

Proof.

The proof also follows from the definition of and is similar to that of Theorem 2. ∎

The following result is also straightforward from the definitions of and given by Theorem 1.

Theorem 4.

Consider a double barrier option with lower barrier and upper barrier and a fixed parameter set.

-

(a)

If the option degenerates into a down-and-out barrier option.

-

(b)

If the option degenerates into an up-and-out barrier option.

-

(c)

The option is equivalent to the vanilla option with the same parameter set if and only if

-

(d)

The option is a typical double barrier option if and only if

It should be noted that the results of the theorems 2 - 4 do not depend on the pay-off function of the options considered, and consequently they may be applied to all options endowed with barriers, and in particular they apply to both barrier call and barrier put options, European as well as American options, and options including a rebate payment. The importance of these theorems also stem from the fact that barriers can be added to virtually all sorts of existing options, and this is one of the reasons why barrier options have become so popular. An important particular case is that of constant barriers. In such case, the lower and upper curves, if any, for a given option can be denoted by and respectively, where and are constants, and we can therefore give more explicit expressions for the critical values and It is easy to see that the functions and given by the equations (2.4b) and (2.6b) have in this particular case a common expression for the turning point when it exists, given by

| (3.1) |

Consequently we have the following explicit expressions for the critical asset prices and

| (3.2a) | ||||

| and | ||||

| (3.2b) | ||||

Although to the best of our knowledge the critical value and are considered for curved barriers only for the first time in this paper, it should be noted that equations of the form (3.2) have been used in [19] for an optimal determination of the solution domain in the numerical pricing of barrier options with flat barriers. It’s however, also the first time that these critical values are applied to the classification of barrier options.

4. Numerical test

The choice of the value of in the equations (2.4b) and (2.6b) is clearly crucial. Indeed, these equations show that the larger is, the farther both and will be with respect to their corresponding barriers, and vice versa. This means that, as expected, larger values of yield critical values and which ensure with a better certainty that the barriers are worthless, but which are however not optimal. Inversely, smaller values of will yield critical asset prices which are wrong by being too close to the barrier, and this is just a consequence of the fact that the equality is wrong for such values of . Ideally, should be as indicated the smallest number for which the equality holds. However, for any numerical determination, the constant and consequently both and are very sensitive to the level of accuracy required in option prices.

A numerical value for and can be found by trial and error on computing systems such as mathematica. For example in the case of a down-and-out barrier option, is the smallest value of the initial price for which the option price is the same as that of the vanilla option with the same parameters. We can then use such a numerical value to find the value of that yields the same value of given by Theorem 1. Next, using this choice of and the same accuracy in option prices, we can check whether numerically computed critical asset prices match those given by Theorem 1, for different sets of parameters.

| T | ) with | ||||

|---|---|---|---|---|---|

| 0.25 | 0.15 | 98.87 | 94.852 | 4.347 | |

| 0.25 | 0.30 | 144.00 | 156.744 | 5.465 | |

| 0.50 | 0.15 | 112.60 | 112.000 | 4.850 | |

| 0.50 | 0.30 | 192.00 | 229.999 | 6.129 |

For is the analytical value of given by Theorem 1, and is the corresponding numerical value computed by trial and error.

First, we show by an example the effect of accuracy in option prices on the critical asset prices and on by considering the case of a down-and-out barrier option. We assume that the parameter set is and Setting we see that when accuracy in option prices is to within digits, we have to within digits, and to within digits we have Intuitively, this clearly shows that higher accuracy yields better values for both and the critical values.

Table 1 reports the test of for a down-and-out barrier option with a flat barrier and with fixed parameter set and for variable values of the expiry date and volatility parameters In the table, is the analytical value of as given by Theorem 1, while is the corresponding numerical value computed by trial and error. The third column of the table contains analytical values of computed with a choice of according to the result of Theorem 1, and more specifically by using Eq. (3.2a). Column gives the actual numerical value of for each parameter set, while the last column gives the value of for which the analytical value of given by Eq. (3.2a) would agree with the numerical value given in the fourth column.

The table shows that the value of which is closely the smallest number for which mathematica gives is an appropriate value for Eq. (2.4b) for relatively small volatilities such as It also shows however that should be larger for larger volatilities. Unfortunately, we don’t know how exactly the choice of changes with the volatility, and with other pricing parameters. Nevertheless, Theorem 1 can be used efficiently when only approximate values of and are requested [19]. Thanks to the non dimensional nature of the parameter the equations (2.4b) and (2.6b) together with Theorem 1 provide all the properties of the critical assets prices and show how they depend in particular on the parameters and

5. Concluding Remarks

In this paper, we’ve found with very simple arguments in Theorem 1 critical stock prices that determine when exactly a given stock price becomes worthless with respect to some given curves, and we’ve given some applications of these critical values to barrier options. This simple determination gives fully explicit expressions for the critical stock prices and although it remains approximate due to the presence of the approximate parameter in these expressions. However, the explicit nature of this determination, as expressed for example in the particular case of flat barriers in (3.2) , provide us with simple means to understand the properties of this critical asset prices. Indeed, Table 1 intuitively confirms all the effects of the expiry date and volatility on these critical stock prices.

Although the comparison in Table 1 between actual numerical values and corresponding semi-analytical values of the critical prices displays some discrepancies, such values can be safely and efficiently used in certain cases such as the optimal truncation of the solution domain in a numerical scheme, and especially in the case of the difficult problem of discrete barrier options pricing. Indeed, in the case of constant barriers, an application of the critical asset prices given by (3.2) to the pricing of discrete barrier options has given in [19] results closest to the only semi-analytical one available [10], when compared with similar results obtained with five other numerical methods.

There are ways of finding exact numerical values for and For instance, the probability that the stock price will breach a given barrier before time given that it has value at time can be formulated as a first time exit problem, and it is well-known [20] that satisfies the Kolmogorov Backward equation

| (5.1) |

with and and with some boundary conditions that are easy to determine. For instance we have and on the boundary curves. The corresponding boundary value problem can be solved explicitly, at least by reducing Eq. (5.1) to a simpler equation. But after all such lengthy calculations the corresponding expressions for and are not likely to be found explicitly, although their exact numerical values can be found in this way. Equations of the form (3.2) therefore have the advantage of providing in a much quicker and simpler manner, in terms of the non-dimensional parameter all the information needed for the properties of the critical values and

By replacing the two curves in Theorem 1 by the straight line determined by the strike price of a given European option, Theorem 1 can also be used to determine the initial asset price range beyond which the option becomes worthless. There are certainly several other applications of this theorem in option pricing and finance.

References

- [1] T.W. Anderson, A modification of the sequential probability ratio test to reduce the sample size Ann. Math. Statist. 31 (1960) 165–197.

- [2] J. Barraquand and D. Martineau, Numerical valuation of high dimensional multivariate American securities. Journal of Financial and Quantitative analysis 30 (1995) 383–405.

- [3] M. Bertoli and M. Bianchetti, Monte carlo simulation of discrete barrier options. Internal report, Financial Engineering - Derivatives Modelling, Caboto SIM S.p.a., Banca Intesa Group, Milan, Italy (2003).

- [4] M. Braodie, P. Glasserman, and S. Kou, A continuity correction for barrier options. Math. Finance 7 (1997) 325–349.

- [5] M. Broadie and J. Detemple, American capped call options on dividend-paying assets. Review of Financial Studies 8 (1995) 161–192.

- [6] N. Clarke and K. Parrott, Multigrid for American option pricing with stochastic volatility. Applied Mathematical Finance 6 (1999) 177–195.

- [7] J.C. Cox and S.A. Ross, The valuation of options for alternative stochastic processes. J. Financial Econ. 3 (1976) 145–166.

- [8] J.C. Cox and M. Rubisntein, Options Markets. Prentice-Hall, Englewood Cliffs (1985).

- [9] J.C. Duan, E. Dudley, G. Gauthier, and J.G. Simonato, Pricing discretely monitored barrier options by a markov chain. J. Derivatives 10 (2003) 9–32.

- [10] G. Fusai, I.D. Abrahams, and C. Sgarra, An exact analytical solution for barrier options. Finance Stochast. 10 (2006) 1–26.

- [11] B. Gao, J. Huang, and M.G. Subrahmanyam, The valuation of American barrier options using the decomposition technique. Journal of Economic Dynamics and Control 24 (2000) 1783–1827.

- [12] E.G. Haug, Closed form valuation of American barrier options. International Journal of Theoretical and Applied Finance 4 (2001) 355–359.

- [13] S. Ikonen and J. Toivanen, Efficient numerical methods for pricing American options under stochastic volatility. Reports of the department of mathematical information technology, Series B. Scientific Computing, No B12 (2005).

- [14] J.E. Ingersoll. A contingent-claims valuation of convertible securities. J. Financial Econ. 4 (1979) 287–322.

- [15] N. Kunitomo and M. Ikeda, Pricing options with curved boundaries. Mathematical Finance 2 (1992) 275–298.

- [16] P. Levy, Processus Stochastic et Mouvement Brownien. Gauthier-Villars, Paris (1948).

- [17] J.J. McConnell and E.S. Schwartz, Lyon taming. J. Finance 41 (1986) 561–577.

- [18] R.C. Merton. Theory of rational option pricing. Journal of Economics and Management Science 4 (1973) 141–183.

- [19] J.C. Ndogmo, High-order accurate implicit methods for the pricing of barrier options. Available from http://arxiv.org/abs/math.pr/0710.0069 (2007).

- [20] J.N. Dewynne P. Wilmott and S. Howison, Option pricing: Mathematical models and computation. Oxford Financial Press, Oxford (1993).