The Question of Relaxation in the Wealth Exchange Models

Abhijit Kar Gupta

Physics Department, Panskura Banamali College

Panskura R.S., East Midnapore, WB, India, Pin-721 152

e-mail: kg.abhi@gmail.com

Abstract

We look at the meaning of ’relaxation’ in the wealth exchange models that are recently proposed in Econophysics to interpret the wealth distributions. To quantify and characterise the process of relaxation, we define an appropriate quantity and evaluate that numerically for the systems of many agents. Also, it has been supported heuristically by constructing a simple differential equation.

Introducing the Models

The wealth exchange models are many agent models for wealth distributions where a randomly chosen pair of agents interact and exchange wealth between them in a certain fashion. We here deal with the models that are primarily based on the kinetic theory of gas in statistical physics. The interactions among agents can be thought of as an elastic collision as the total wealth of the interacting agents is kept constant and this in turn ensures the total wealth of all the agents to remain conserved. There has been a great amount of study [1] in this kind of wealth exchange models in econophysics in recent times [1].

The time evolution of wealth () in the wealth exchange models can be summarised as follows:

| (1) |

| (2) |

The above is a zero sum process where the wealth of an agent evolves through such a simple rule and a distribution of wealth emerges after a certain ’time’ . It is possible to obtain a wide variety of distributions within this framework namely, the exponential Boltzmann-Gibbs type distributions, the gamma type distributions and more interestingly the power laws. Power laws that are obtained from fitting the tail ends of the wealth distributions of real data are known as Pareto’s law in the economic literature for over a hundred years and this is known to possess some universality.

The emergence of a distribution depends on the expression of exchange amount which stems from the description of the model. The models developed out of the above principle have been quite useful in understanding the wealth distributions of individuals (or that of companies or societies) in an economy (see the recent reviews [2, 3]).

In the following, we write down the expressions for the exchange amount for different models:

| (3) | |||||

| (4) | |||||

| (5) |

The first step in the above [eqn.(3)] is for the pure gambling model [4] where we write the evolution of the wealth of -th agent is given by , being a random number between 0 and 1 drawn from a random number generator. Note that here, . The exponential Boltzmann-Gibbs type distribution results from this model. In the next model [in eqn.(4)], the agents have a fixed saving propensity [5] introduced through a parameter where the evolution of the -th agent is given by . In this, each agent saves -fraction of his/ her wealth and puts the rest for gambling. It has been shown that the distributions found from this model are of the gamma-type. The last step [eqn.(5)] corresponds to the model where the saving propensity is characteristic of an agent i.e., the parameter has been assigned a distribution (in our case a uniform distribution in ). Power laws in wealth distributions are obtained from this random or distributed saving model [6] and hence this model does attract enhanced attention.

As the system of many agents evolves in time (as suitably defined), it relaxes towards a steady state equilibrium so that the distribution of wealth assumes a definite shape. In the pure gambling model and in the model with fixed saving propensity, the idea of relaxation can hardly be of interest as the agents do not possess any characteristic feature; they are having equal opportunities (either no saving or equal saving) through random interactions. We shall, therefore, concentrate on the random saving model out of the three as the meaning of relaxation can be rightfully associated with this. The relaxation study has been made earlier [8] on this model but the concept and purpose of that had been different from the present study.

To Observe Relaxation

The question is how we may characterise the ’relaxation’ of an evolving system. If a system is allowed to go towards a steady or fixed state, it will relax (usually exponentially) after the external disturbance is withdrawn (as is well known in the context of a model spin system in statistical physics). As the system approaches a steady state, the successive values (in time) of a measurable quantity for the whole system are supposed to be nearing each other. From this idea we check the concept of relaxation in the wealth exchange models in the following way.

The following quantity may be defined as a measure of relaxation:

| (6) |

The quantity is averaged over interactions. Further, it is averaged over a number of initial configurations. When the configuration averaged value of is plotted against time we expect a graph decaying with time for a system which is supposed to relax to equilibrium. Here we define one ’time step’ to be equal to interactions on average, where is the number of agents in the system: , being the number of interactions.

Numerical Results

From the numerical study of the above models it is seen that the system of many agents relaxes towards a steady state equilibrium and the wealth of each individual attains a specific time independent distribution. It will be of interest to see how a system of many agents, as a whole, relaxes as it evolves from arbitrary initial distributions. The system obviously does not head towards a fixed stationary state. Rather it fluctuates around some average value (in equilibrium) in all cases as the exchange of wealth is allowed to happen all the time. It may be emphasised here that the steady state equilibrium states are not affected by the choice of initial configurations. Also, the initial configurations do not have any bearing on the overall process of relaxation (i.e. the shape of the decay curves). We check all these numerically (the data are not presented here).

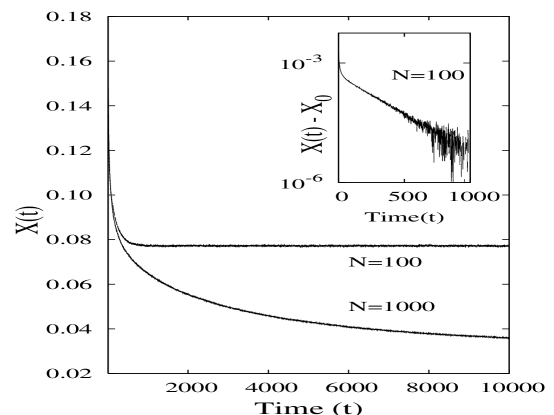

In the numerical simulation, we take =100 in most of the cases as this is sufficient for our purpose; only in some cases we take to demonstrate the size dependence. The averaging, in all cases, have been done over initial configurations. The appearance of exponential decay in relaxation in the random saving model [6] may be anticipated due to a probable reason that the agents possess a characteristic feature (random distribution in the saving parameter in our case). The system is expected to be driven towards a steady state equilibrium through a possible exponential decay in such a case. In fig.1, we plot averaged value of against time where the relaxation seems to be of the form: . Thus to demonstrate the exponential character we determine and then subtract that from to plot in the semi-log scale as shown in the inset of fig.1. The relaxation time can be identified as the inverse of the slope of the straight line (inset in fig.1). The relaxation is seen to be dependent upon the system size (number of agents ) which can be intuitively understood. How it exactly depends on the system size, can be studied later.

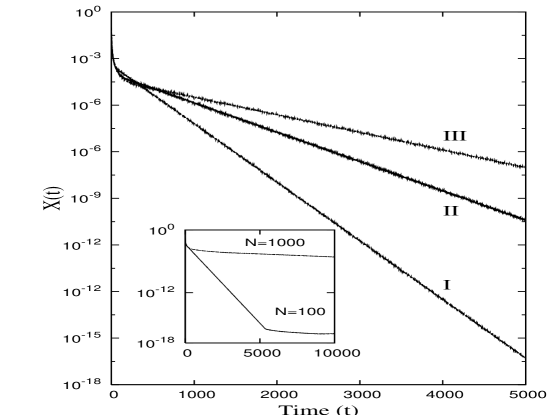

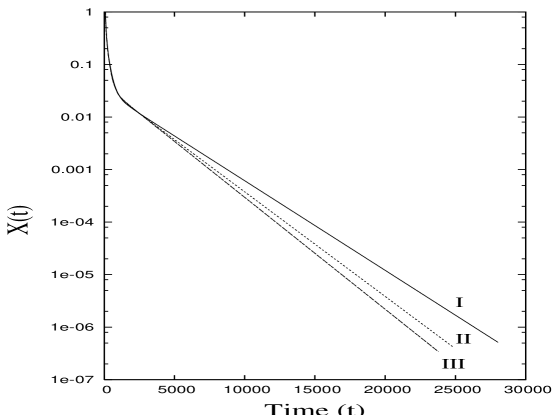

The random saving model has two parameters namely, and where both are taken from a uniform distribution between 0 and 1. It is checked through numerical simulation that as the parameter is taken to be random (as per the requirement of the model), the other parameter may be held constant and for that the ultimate wealth distribution does not change. Therefore, we check the relaxation in this model with different fixed values of and out of those we find that the relaxation is found to be purely exponential (up to a certain time) for . In fig.2, we demonstrate this and plot the graphs for different widths in the random distribution in . Note that the plots are made here without the subtraction of the saturation value (unlike that in fig.1). The subtraction is not required as the straight line portion in the semi-log plot shows a pure exponential decay of the type: . The system stabilises only after a spell of pure exponential decay. The relaxation time (inverse of the slope of the straight line) seems to depend on the width of distribution in in a definite way. As the mean in the distribution in increases, the relaxation time increases (slope decreases) which is evident from the graphs. We have not investigated here how may depend on the width or the mean of the distribution in . This can be interesting and it will be studied later.

In passing, a similarity of this kind of computer model with the well known random resistor network (rrn) model [9] may be noted. The potential of a node in a resistor network can correspond to the wealth of an agent. In rrn, the voltage is updated by Kirchhoff’s law: , where , , being the conductances of the connecting resistors. The above updating rule is very similar to that in the wealth exchange models. Note that can be positive or negative. The quantity that remains conserved here is the total current through the connecting resistors in and out of a node. Interestingly, here too the relaxation is observed to be exponential. To check this, we do a simulation on a random resistor network over a square lattice. We calculate a similar quantity as that is done before. Here we define

| (7) |

where is the potential at a node (,). The resistors are assigned conductance values (inverse of resistance) taken from a uniformly random distribution.

It is also seen that the relaxation time is dependent upon the width of randomness in the distribution of resistances/ conductances in rrn, quite a similar thing that happens in the wealth distribution model with random saving (the results of which is presented in fig.2). Therefore, a similarity (between the models in two areas) may be drawn in many ways but we should emphasise here that this is only tentative. However, the random resistor network model is obviously done on a regular lattice whereas the wealth exchange models are usually not done on any lattice. But it is also can be checked numerically that in the wealth exchange models, the wealth distribution does not change if the agents are taken on a regular lattice. Numerical investigations nevertheless suggests that the relaxation time in the present wealth exchange model changes due to the presence of a lattice.

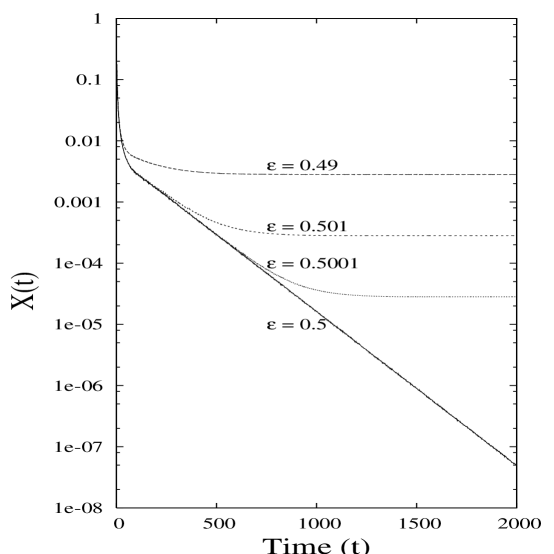

We observe that the exponential decay can be prominently demonstrated for the case of . In this case the system is seen to settle to the lowest possible equilibrium value for . So this is a special case. We also examined the cases with very close to (but not exactly equal to) which are demonstrated in fig.3. As the value of is taken slightly away from 0.5, the relaxation curve stabilises far off from that for (fig.3).

The natural question now is to ask how the wealth of an individual approaches a value (for some it grows and for some it decays) on an average with time. This question is addressed in the work in [8]. In the random gambling model and in the model with constant an agent ends up with the same value of wealth on the average. However, the model with random or characteristic saving [6] that we have dealt with here is quite different. The agents with higher (higher saving propensity) ends up with more wealth than another with smaller value. This can be understood from common knowledge. The agents with higher saving tendencies ends up with accumulating more wealth than those with smaller saving tendencies. As we start from any arbitrary initial configuration, the wealths of some agents thus grow towards some higher values and that for others decay towards some lower values. This decay or growth is exponential (as this is also checked numerically). The growth or decay of all the agents are reflected in the relaxation of the entire system. A heuristic argument that follows, may may be helpful in understanding the general nature of relaxation and that for the special case of .

Heuristic Arguments on the Nature of Relaxation

Let us consider a general model which can correspond to any of the models stated earlier as we tune the parameters in it appropriately. A discussion over this based on the transfer matrix approach is given in [7]. The algorithm of wealth exchange in the general model is the following:

| (8) | |||||

| (9) |

where the parameters and can be positive or negative and they can be related to the actual parameters in the models under consideration. Note that the values of the above parameters are supposed to be uniformly distributed in some range. For example, if and both are uniform random numbers between 0 and 1, a little analysis suggests that in eqn.(8) will be distributed uniformly in the range between and . Thus ’s can be thought of continuous variables in a certain range. The ’s, however, can take only positive values in the models by design. Therefore, we attempt to construct differential equations out of the above mentioned coupled equations [eqn.(8) & (9)] assuming that the change in the wealth, occurs in time =1. The time steps can be adjusted according to our convenience.

We arrive at the following differential equation:

| (10) |

The solution of the above homogeneous differential equation is of the following form:

| (11) |

where ; can be positive or negative depending on the choice of the parameters, and . Therefore, the above solution can be seen to be either growing or decaying exponentially from or to a certain value.

Now we think of the wealth exchange model with random saving as a special case. The wealth of the -th agent evolves through the following way:

| (12) |

where -th and -th agents save and fractions of their wealths respectively, at time . In view of the general equation as mentioned above [eqn.(8)], we have and . Thus for the random saving model, we obtain the following expression for for the choice of :

| (13) |

As we consider the distributions in such that , the value of must always be positive (). Hence the solution [eqn.(11)] always decays exponentially for this special case for any values of ’s as long as they are bounded between 0 and 1. Infact, now we may intuitively understand how a pure exponential relaxation may appear in the case for which is shown in fig.2. This fact is even more evident from the demonstration in fig.3.

In conclusion, we have tried to establish the nature of relaxation in the wealth exchange models of a certain class by studying the relaxation in random saving model. The nature of relaxation is found to be exponential (followed by a saturation) and this is possibly true for other models (that are not discussed here) based on the similar principles. The relaxation process (and the relaxation time) can be greatly manipulated by tuning the parameters, and that are involved in random saving model. The relaxation is shown to be purely exponential for the special choice of in this model. The claims are made from numerical simulation results and are supported by heuristic arguments.

Acknowledgement

The author wants to thank D. Stauffer and B.K. Chakrabarti for their valuable comments and critical remarks on the work and on the manuscript.

References

- [1] Articles in Econophysics of Wealth Distributions, A. Chatterjee, S. Yarlagadda and B.K. Chakrabarti (eds.), Springer (2005). [See the Chapters by T. Lux (p.51); by A. Chatterjee and B. chakrabarti (p.79); by K. Bhattacharya, G. Mukherjee and S.S. Manna (p.111); by P. Richmond, P. Repetowicz and S. Hutzler (p.120); by S. Sinha (p.177)].

- [2] A. Kar Gupta in ’Econophysics and Sociophysics: trends and perspectives’ (p.161), B.K. Chakrabarti, A.K. Chakraborty, A.K. Chatterjee (eds.), Wiley-VCH, Verlag GmbH & Co. KGaA (2006); Also see arXiV.org, Physics/0604161. Also see the chapters by P. Richmond et al. (p.131) and by Y. Wang et al. (p.191) in the same book.

- [3] Victor M. Yakovenko, Econophysics, Statistical Mechanics Approach to, review article for ”Encyclopedia of Complexity and System Science” to be published by Springer; arXiv:0709.3662v1 [physics.soc-ph].

- [4] A.A. Drăgulescu, V.A. Yakovenko, Eur. Phys. J. B 17 723 (2000).

- [5] A. Chakraborti and B.K. Chakrabarti, Eur. Phys. J. B 17 167 (2000).

- [6] A. Chatterjee, B.K. Chakrabarti and S.S. Manna, Physica A 335 155 (2004).

- [7] A. Kar Gupta, Physica A 359 634 (2004).

- [8] M. Patriarca, A. Chakraborti, E. Heinsalu and G. Germano, Eur. Phys. J. B 57, 219 (2007).

- [9] S. Kirkpatrick, Rev. Mod. Phys. 45, 574 (1973); A. Kar Gupta and A.K. Sen, Physica A 215, 1 (1995).