Heterogeneous credit portfolios and the dynamics of the aggregate losses

Abstract

We study the impact of contagion in a network

of firms facing credit risk. We describe an intensity based model

where the homogeneity assumption is broken by introducing a

random environment that makes it possible to take into

account the idiosyncratic characteristics of the firms. We shall

see that our model goes behind the identification of groups of firms

that can be considered basically exchangeable. Despite this

heterogeneity assumption our model has the advantage of being

totally tractable. The aim is to quantify the losses that a bank may

suffer in a large credit portfolio. Relying on a large deviation

principle on the trajectory space of the process, we state a

suitable law of large number and a central limit theorem useful to

study large portfolio losses. Simulation results are provided as

well as applications to portfolio loss

distribution analysis.

Keywords: Central limit theorems in Banach spaces,

Credit contagion, intensity based models, Large Deviations, large

portfolio losses, random environment.

AMS 2000 subject classifications: 60K35, 91B70

Introduction

During the last years the challenging issue of describing the dynamics of the loss process connected with portfolios of many obligors has received more and more attention. Applications can be found both for management purposes (see [8]) and in the literature dealing with pricing and hedging of risky derivatives as CDOs (Collateralized Debt Obligations). For a discussion of this framework see [15] and [18].

When dealing with portfolio losses, it becomes crucial the modeling of the dependence structure among the obligors. One standard procedure is to directly specify the intensity of default of the single obligors belonging to the portfolio in order to infer the dynamics of the global system and thus the distribution of the aggregate losses. In the context of reduced form models a rather general framework is the conditionally Markov modeling approach by Frey and Backhaus (see [12] and [13]). One drawback of the intensity based models is the difficulty in managing large heterogeneous portfolios because of the presence of many obligors with different specifications. In this case it is common practice to assume homogeneity assumptions in order to reduce the complexity of the problem. A typical approach is to divide the portfolio into groups where the obligors may be considered exchangeable.

In this paper we describe an intensity based model where the homogeneity assumption is broken by introducing a random environment that makes it possible to take into account the idiosyncratic characteristics of the firms. We shall see that our model goes behind the identification of groups of firms that can be considered basically exchangeable. Despite this heterogeneity assumption our model has the advantage of being totally tractable.

The goal is to describe the evolution of the losses for a large

portfolio where heterogeneity and direct contagion

among the firms are taken into account. We denote by the

random variable describing the losses at time for a

portfolio of size . Our approach works as follows. First we study

the limiting distributions on the path space of some

aggregate variables useful to characterize the evolution of

for . To this effect we shall derive an

appropriate Law of Large Numbers based on a Large Deviations

Principle in order to describe a limiting behavior that can be

considered as a asymptotic regime with infinite firms. Finally, we

study the finite volume approximations (for finite but large

) of the limiting distribution via a suitable version of the

Central Limit Theorem that describes the fluctuations around

this limit. In most cases, these dynamical fluctuation theorems are

proved by method of weak convergence of processes; this approach has

been widely applied to models close in spirit to this work. We quote

[12] and [7] for applications

to finance. The effectiveness of those methods for heterogeneous

models is, however, unclear. We follow here a different approach,

which allows to prove a Central Limit Theorem directly in the

underlying trajectory space. This approach is based on a general

Central Limit Theorem in [3]. Although various applications of

this theorem to fluctuations of Markov processes can be found in the

literature (see e.g. [1] and [6]), to our knowledge the

first application to a non-reversible Markov process.

In the risk management context, our model may be useful for the management of large portfolios, in the spirit of other models proposed in [16] or in [7]. It has been remarked that in many real world applications default are rather rare events, so that, for instance, the fraction of defaulted firms is close to zero and a normal approximations is not meaningful. Our models and results are only concerned with time scales for which a proper fraction of the portfolio is likely to be affected by the defaults.

We believe that our paper may be considered as an original contribution in the modeling of portfolio losses dynamics that accounts for both heterogeneity and contagion. On the other hand, to our knowledge, this is the first attempt to apply large deviations and normal fluctuation theory on path spaces (that is, in a dynamic fashion) for finance or credit management purposes, except for what contained in[7]. For a survey on large deviations methods applied to finance and credit risk see [17].

The models we propose in this paper are the simplest heterogeneous models describing systems comprised by many defaultable components, whose defaults are positively correlated via an interaction of mean-field type, i.e. with no geometric structure. Although we have been inspired by financial applications, we believe the basic principles should apply to other contexts.

The outline of this paper is as follows. In Section 1 we illustrate the model and the main theorems. In Section 2 we apply these results to the large portfolio losses analysis. Some examples with explicit computations and simulations are also provided. In Section 3 we conclude. Appendix A is devoted to the proofs of the three main theorems stated in Section 1.

1 Model and main results

Consider a network of defaultable firms, whose states are denoted by , . The event means that the -th firm has defaulted. The values give rise to an aggregate variable which indicates the global state of the network:

where are given nonnegative numbers. can be interpreted as the impact the default of the -th firm has on the aggregate variable . In order to model contagion, we assume the instantaneous rate of default of the -th firm is an increasing function of . More specifically, we assume the rate of default of the -th firm is given by

where is the indicator function of the set , and , are given constant. represents the sensibility of the -th firm to variations of the aggregate variable , while can be interpreted as the “robustness” of the -th firm: a large value of means that the -th firm is very unlikely to default within a given time.

Thus, for any fixed value of , and , the variable evolves as a Markov chain in continuous time, with infinitesimal generator given by

| (1.1) |

where denotes the configuration obtained from by changing from to . We assume the system start at time from the configuration . The evolution randomly drives the network towards the trap state , which is reached in finite time.

From now on we denote by the triple of the parameters corresponding to the -th firm. The ’s model the heterogeneity of the system. We consider here the point of view of disordered models, i.e. we assume to be i.i.d. random variables, with a given law . In order to avoid inessential difficulties, the law is assumed to have compact support in . Note that, for a given , the random variables are not assumed to be independent. Sometimes, the vector will be referred to as random environment.

Consider a time , and denote by the trajectory described by the configuration under the stochastic evolution (1.1). Each component is either identically or it flips from to at the default time

| (1.2) |

By convention, we set . This set of -valued trajectories is denoted by . Each trajectory in can be identified with its default time (which is set to be equal to if there is no default); thus inherits the topology induced by the usual topology on for the default time. Equivalently, the topology on is the one induced by the Skorohod topology on the set of -valued functions which are right-continuous and admit limit from the left at any point of (see e.g. [11]).

In this paper we are interested in the asymptotic behavior, as , of empirical averages of the form

where is a Borel measurable function, and

is called empirical measure. More generally, we shall consider the empirical measure

which is a random measure on . Note that is the marginal of on .

In what follows, we denote by the set of probability measures on , while will denote the set of signed measure on . Both sets are provided with the weak topology.

For with , we set

For we define

| (1.2) |

where and . For a fixed , the infinitesimal generator (1.1), together with the initial condition induces a probability on . We think of as the conditional law of the process given the random environment. We denote by

the joint law of the process and the environment. The distribution of under will be denoted by .

A special case is when all components of are zero. In this case each firm defaults with rate , independently of the others. We denote by the law on of this process.

In what follows, for , we denote by

the relative entropy of with respect to .

Theorem 1

. The sequence of elements of satisfies a Large Deviation Principle (LDP) with good rate function

The proof of Theorem 1, as well as of the other results stated in this section, is postponed to the appendix.

We recall that the above statement means that, for each Borel

subset of ,

where and denote the interior and the closure of respectively; moreover the function is nonnegative, lower-semicontinuous, and the level sets are compact, for each .

Theorem 2

. The equation has a unique solution , that can be identified as follows. Consider the nonlinear integro-differential equation

| (1.3) |

for a real-valued , , . This equation has a unique solution . For every fixed, consider the Markov chain on with time-dependent infinitesimal generator

| (1.4) |

where

and starting from (note that this process jumps only once, from to , and it is then trapped in ). Let be the law of this process on . Then

Moreover

Theorems 1 and 2 have a simple consequence. Let be an open neighborhood of in . By Theorem 2, lower semicontinuity of and compactness of its level sets, a standard argument shows that . By the upper bound in Theorem 1 there exists such that

thus converges to zero with exponential rate. We summarize this fact in the following law of large numbers.

Corollary 1

. Let be any metric that induces the weak topology on . Then for every , the probability

converges to zero with exponential rate in .

Next result is about the fluctuations of about , which has the form of a Central Limit Theorem. In most cases, these dynamical fluctuation theorems are proved by method of weak convergence of processes. A typical tool in this context is Theorem 1.6.1 in [11]; it has been widely applied to models close in spirit to this work, see for instance [4] and [7]. The effectiveness of those methods for heterogeneous models is, however, unclear. The main point is that via Theorem 1.6.1 in [11] one obtains the dynamics of the fluctuation process, which is infinite dimensional; to get a computable expression for the asymptotic variance of a given function of the trajectory may be not feasible.

We follow here a different approach, which allows to prove a Central Limit Theorem directly in the space . This is inspired by the seminal work of E. Bolthausen [3], and it has been carried out in a context similar to ours in [1] and [6]. The main difference here is that the underlying stochastic dynamics are not reversible; the related difficulties have forced us to introduce a further assumption, that we call reciprocity condition:

-

(R)

There exists a deterministic such that for all the identity holds almost surely.

In economical terms, this means that the sensibility of a firm to variation of the aggregate variable is proportional to the impact the default of that firm has in the network. In different words, the interaction between firms is symmetric: if the -th firm strongly interact with the network (i.e. is large) then it has a large influence on the network but, symmetrically, it is also strongly influenced by the state of the network. This assumption may be reasonable in many situations.

From now on, whenever condition (R) is assumed, will denote the pair ; accordingly, and will be spaces of measures on , where .

In order to state our Central Limit Theorem, we need to introduce some notations. Let be the subset of comprised by the signed measures with zero total mass. Let be the law, induced by , of the -valued random variable . We then denote by the space of bounded, continuous, real valued functions on . For , define by

| (1.5) |

for measurable.

Theorem 3

. Let . Then the -law of the random vector

converges weakly as to an -dimensional Gaussian probability measure with zero mean and covariance matrix given by

where and is the second Fréchet directional derivative of at in the directions :

(all these limits will be shown to exist).

Moreover the diagonal terms of the covariance can be

written as

| (1.6) |

where

| (1.7) |

is the compensated -martingale associated with the jump process of .

2 Applications to the portfolio analysis

2.1 Computation of large portfolio losses

We are now going to state a definition of portfolio losses. When speaking of portfolio losses, we mean the losses that a financial institution may suffer in a credit portfolio due to the default events. Many specifications may be chosen to this aim. Some general rules are now stated. A rather general modeling framework is to consider the total loss that a bank may suffer due to a risky portfolio at time as a random variable defined by , where is the loss, called marginal loss, due to the obligor . Different specifications for the marginal losses can be chosen accounting for heterogeneity, time dependence, interaction, macroeconomic factors and so on. A punctual treatment of this general modeling framework can be found in the book by Embrechts, Frey and McNeil [10]. For a comparison with the most widely used industry examples of credit risk models see [14] or [5]. The same modeling insights are also developed in the most recent literature on risk management and large portfolio losses analysis, see [16], [13] and [8] for different specifications.

Here we assume that

| (2.1) |

where is bounded and

continuous in . In other

words the marginal loss depends explicitly on the realization of

and on the

history of .

As a particular case of our general framework we obtain the most

standard set up commonly used in the literature of credit risk:

consider where

is a continuous function of , and measures the exposure in case of

default. Thus

We shall often speak of asymptotic loss or asymptotic portfolio. In this case we are referring at the case of infinite obligors. The large portfolio is intended to be a large but finite approximation of this asymptotic regime.

As a consequence of the central limit theorem for the empirical measure, we obtain the following description for , the aggregate losses computed at time :

Corollary 2

Proof. We apply Theorem 3 with and . In this case and . Notice that we can consider, without loss of generality, as the final horizon of the time period, i.e. .

Remark 1

The asymptotic expected value corresponds to the fraction of loss at time in a benchmark portfolio of infinite firms. Concerning equation (2.2), notice that in the case of no interaction, (i.e., ) we have

In the case of there is a suppletive noise given by the

interaction.

It depends on the past history of the process, hence a sort of “memory”

of the variance .

The variance given in (2.2) involves the integral with respect to a martingale. A simpler form for the variance, more suitable for numerical computations, can be found in the following special but significant case.

Proposition 1

. Suppose that . Then as we have that

where , converges to a centered Gaussian random variable with variance

| (2.3) |

where .

Proof. We only need to show that the variance can be written in the form given in (2.3). From (2.2) it is easy to see that can be written as

| (2.4) |

We now look at the expectation in the integral

where we have used the fact that for and for all . Substituting in (2.4) we have

| (2.4) |

The first expectation is the variance of computed under . We show now that the second expectation is null. Indeed it is equal to

The second term is zero since is a martingale and the argument of the integral is measurable. Concerning the first one we see that

Where the last equality is due to the fact that is measurable. Concerning the last term in (2.4) we now show that

| (2.5) |

Indeed, being , it can be shown that the quadratic variation of , is , for all . Thus for each progressively measurable process , where ,

As a consequence, applying this last result with defined as

by the isometry between and , we have

which is exactly (2.5). Finally

and this proves (2.3).

In the next section we show an application of this law of large number (Theorem 2) and central limit theorem (Proposition 1). Indeed, we show the evolution of the default probability of certain groups of obligors and infer the corresponding probability of suffering large losses in a credit portfolio.

2.2 An example with simulation results

Consider the simplified case in which

and zero otherwise: the exposure at default is equal to one for each

obligor. Moreover assume that

. This means that the law

of the random environment puts mass on

two possible outcomes, that is . In this case

the index identifies a group of obligors with the same

marginal characteristics. In other words, we split the portfolio in

two types of obligors with different specifications. More complex

specifications could also be chosen since, as already said in the

introduction, we are not forced to split the sample in groups with

homogeneous characteristics. For sake of simplicity we start we an

illustrative example where interesting

features on the dynamic of the state variables can be captured.

Recall that specifies the relative weight of firm in

building the aggregate variable (see

equation (1.1)). is the parameter that

measures how sensitive obligor is with respect to the aggregate

variable , put differently it is a measure of the contagion

effect. is the idiosyncratic term in the marginal default

probability.

As an example, we take a portfolio of obligors. This is a

typical size for CDO’s portfolios. We suppose that the portfolio

consists of obligors of two types, in particular ,

. Notice that hence the reciprocity

condition (R) applies and we

are allowed to rely on Theorem 3 and Corollary 2.

Obligors of type 1 are more sensitive to the aggregate variable,

that is, their marginal default probability depends strongly on the

default indicator of the other firms. Obligors of type 2 are less

influenced by the aggregate variable . The idiosyncratic term

is the same for each obligor.

With this choice of the parameters, we want to stress the fact that

even though the marginal default probabilities of the two types are

rather similar for the very short horizon (where the impact of

is higher), the contagion effect becomes preeminent as time

goes by, at least

under certain specifications in the construction of the portfolio.

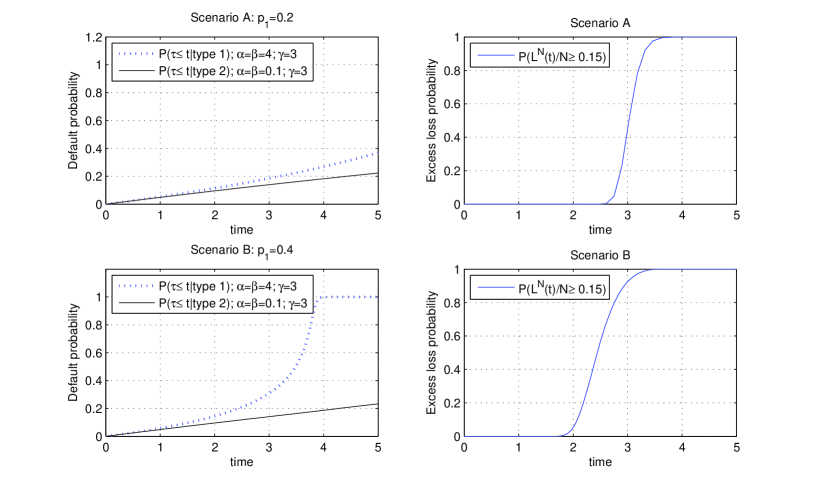

To illustrate this situation, in Figure 1 (on the left),

we show the dynamics of the marginal default probability of the two

groups in two different scenarios. Scenario A mimics a portfolio

where only of the obligors are in group 1, this means that

the proportion of firms exposed to contagion risk is lower.

In scenario B the proportion is increased to . Notice that in

the second scenario the probability of default of the firms in the

first group increases dramatically after the second year. Firms of

type 2 are less influenced.

Relying on Proposition 1, we compute the corresponding

excess probabilities, that is, the probability of suffering a loss

bigger than as a function of time in the two scenarios. In

Figure 1 (on the right) we see this probabilities for

. Notice that in this simple example, counts the

number of defaults up to time , so that

represents the probability of having at least of defaults in

the whole portfolio. Looking at the graphs, it is easy to see that

in the first scenario the probability of having such a loss is

smaller. At time the

whereas in the

second scenario .

This simple example suggests that the contagion effect can be very

significant when looking at the probability of suffering a certain

loss in a large portfolio. This is crucial for risk measurements

purposes and for pricing trances of CDO’s.

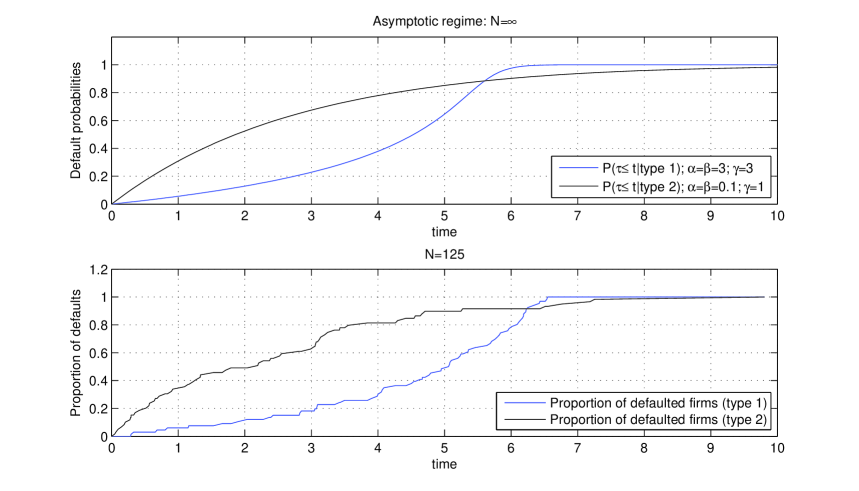

It may be argued that an approximation via an infinite portfolio may

not reproduce the real situation. In Figure 2 we show a

comparison between the evolution in time of the default

probabilities in the two groups of obligors computed under (in

the upper part) and simulated via the real Markov process

with (in the lower part). Here the parameters are

, . These graphs show that the

asymptotic equation is a good approximation for the Markov process even with .

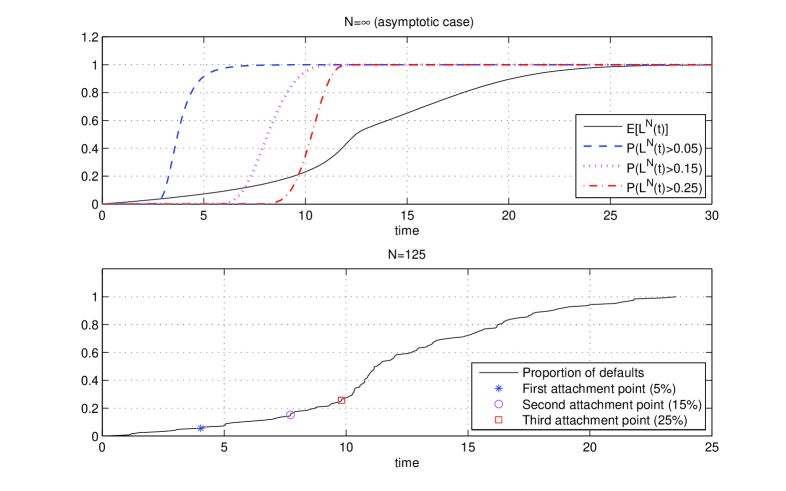

Finally we show in Figure 3 the comparison between the evolution of the aggregate loss (in black) evaluated as before in two different ways. In the upper part we see the aggregate loss computed relying on Proposition 1. Below we see the plot of a trajectory of the Markov Process (with ). In the same graphs we have also plotted the dynamics of the probability of suffering a loss over certain thresholds . In other words we plot for (in this case ). Those probabilities are building blocks for computing the price of trances of CDO’s contracts. For a description of such a credit derivative see for instance [10].

3 Conclusions

We have proposed a model for credit contagion where heterogeneity and direct contagion among the firms are taken into account. We have then quantified the impact of contagion on the losses suffered by a financial institution holding a large portfolio with positions issued by the firms.

Compared to the existing literature on credit contagion, we have proposed a dynamic model where it is possible to describe the evolution of the indicators of financial distress. In this way we are able to compute the distribution of the losses in a large portfolio for any time horizon , via a suitable version of the central limit theorem.

The peculiarity of our model is the fact that the homogeneity assumption is broken by introducing a random environment that makes it possible to take into account the idiosyncratic characteristics of the firms. One drawback of the intensity based models commonly proposed in the literature is the difficulty in managing large heterogeneous portfolios because of the presence of many obligors with different specifications. In this case it is common practice to assume homogeneity assumptions in order to reduce the complexity of the problem. A typical approach is to divide the portfolio into groups where the obligors may be considered exchangeable. We have shown that our model goes behind the identification of groups of firms that can be considered basically exchangeable. Despite this heterogeneity assumption our model has the advantage of being totally tractable: it is possible to compute in closed form the mean and the variance of a central limit type approximation for the losses due to a large portfolios in a dynamic fashion.

As an example of the general theory we have computed the default probabilities and different risk measures in a simple situation with only two groups of obligors. Moreover we have compared the numerical results obtained relying on the asymptotic model and on the central limit theorem (Corollary 2) with the results obtained in a simulation of the underlying Markov process with finite . These results show the goodness of the approximation and are encouraging a more involved analysis. This issue is left to future research: it is in fact out of the scope of this work to pursue a punctual calibration of the model to real data.

Appendix A Proofs of main results

A.1 Proof of Theorem 1

We need to prove some technical lemmas.

Lemma 1

. Let be a Polish space. Let satisfy the LDP with rate and good rate function . Let be measurable, bounded from above and continuous on the set . Then the sequence of probability measures defined by

| (A.1) |

satisfies the LDP with the good rate function

| (A.2) |

In particular

| (A.2) |

For a proof see [19]. This is a relaxed version of the usual

Varadhan’s Lemma for tilted large deviations principles (see

[20]). The statement is relaxed in the sense that we assume

that a suitable function ,

instead of being continuous on all its domain,

is continuous only on a subset in the following sense:

For any sequence such that , where we have .

We point out that this is a stronger assumption than assuming

continuity of the restriction of on the subset .

Lemma 2

Proof. It basically follows from the Girsanov formula for point processes (See [Br]).

where has been defined in (1.2).

The term in

the -brackets is exactly multiplied by

.

We now define for each and

| (A.4) |

We shall often use this notation in the rest of this appendix.

Lemma 3

. F(Q) is bounded on and continuous on the subset

| (A.4) |

The argument in the -brackets is bounded, thus we are allowed to interchange the expectation with respect to and the time integral.

We show now boundedness and continuity of . The

boundedness is easily proved since , and the

distribution of under has bounded support.

In order to prove the continuity on , we consider a

sequence of probabilities

converging weakly to . We split the proof in

different steps.

We show first that

| (A.5) |

for all and for any continuous function bounded on the support of . This statement is not trivial, since the projection is not continuous in . However, define for any the functions

where we suppose that the trajectory can be extended to the larger interval by continuity.

These functions are continuous in , bounded by for any and such that a.s. for any . Thus, by the

Lebesgue convergence theorem,

Letting and noticing that we get

The same argument holds for ; here . Thus

Notice that and may differ only on the event . But this event has measure zero for any , since . This implies that the corresponding expected values must coincide; as a consequence . We have thus proved that

| (A.6) |

Notice that in saying that

we have used the fact

that the distribution function of under is exponential.

In particular, it is absolutely continuous. A similar argument

shows that if then

converges pointwise in to , for

all those such that .

Taking

we simply have that for all , is a continuous

mapping in on . Choosing instead ,

and , we prove continuity for , and respectively.

The next step is to show that implies that

| (A.7) |

converges to zero.

We add and subtract :

where

goes to zero by weak convergence.

Concerning we see that

We now show that

We can rewrite it as

for a suitable , where we have used the fact that is uniformly bounded. We now look at the term into the expectation

again by uniformly boundedness, for a suitable . Thus

and this

converges to zero thanks to what we have shown in (A.5).

As a consequence,

goes to zero as well, since we are allowed to interchange the limit and the time integral, by dominated convergence.

It remains to show the continuity of the term

| (A.8) |

Indeed, take a sequence , , then

The second term goes to zero by weak convergence since the function is continuous. Concerning the first term, it is enough to show that converges to zero uniformly on . To show this, we fix then the following facts hold true:

-

(a)

For there exists such that

-

(b)

There exists such that

Point is due to the

continuity of for whereas follows by the

fact that pointwise in as shown in

(A.5). Notice that when or

the inequalities in are modified appropriately without loss of generality.

We now claim that fixing we have

| (A.9) |

Fix and and suppose (the other case is treated in the same way):

where we have used the fact that is increasing in for all . Thus we can extract a finite covering of where (A.9) holds true hence uniform convergence is proved.

Proof of Theorem 1.

We denote by the

distribution of under , i.e. . We now state a LDP for the sequence .

Thanks to Lemma 2, we have identified the Radon Nikodym

derivative that relates

and

(where plays the role of the reference measure).

A natural way to develop a large deviation principle is now to rely on

Lemma 1.

Since are i.i.d. random variables under

, we can apply Sanov’s Theorem (see

[20]) to the sequence of measures , where

represents the law of the empirical measure in the

case of independence (i.e. under ). Hence

obeys a large

deviation principle with rate function .

Being bounded in the weak topology and continuous on

where and , we

can rely on Lemma 1 to conclude that the sequence

obeys a large deviation principle with good rate

function

We finish the proof by showing that

| (A.10) |

The first equality is

simply a consequence of Equation

(A.2).

We are thus left to prove that . Indeed,

Being , the thesis follows.

A.2 Proof of Theorem 2

We need to define a new process and a technical lemma related to it.

We associate with any the law of a time inhomogeneous

Markov process on which evolves according to the following

rules:

and with for all .

We denote by the law of this process and by

. In other words, is the law

of the Markov process on with initial distribution

and time-dependent generator defined as

| (A.11) |

We show now an important property of .

Lemma 4

. For every , we have

Proof. We distinguish two cases:

Case 1. . We have

By Girsanov’s formula for continuous time Markov chains, we obtain

| (A.11) |

hence, by definition of given in (1.2) we have

so that

| (A.12) |

where the last equality follows from

Being , the thesis follows.

Case 2. . In this case .

Thus we have to

check that as well. Being

the thesis follows since being and since which is bounded .

Proof of Theorem 2.

By properness of the relative entropy (), from Lemma A.11 we have that the equation is equivalent to . Suppose is a solution of

this last equation. In this case , where is the law of the Markov

process on with initial distribution and

time-dependent generator as defined in (A.11).

The marginals of a Markov process are solutions of the corresponding

forward equation. This leads to the fact that , the projection of , is a

solution of where is the adjoint of :

More specifically, when we have

and when

| (A.13) |

We now prove that admits at

most one solution for each initial condition. To see this, define

. Then , where . Notice that and is a locally Lipschitz operator on a

Banach space. Thus has

at most one solution in ,

for a given initial condition (see [2], Theorem VII.3).

Since is totally determined by the flow ,

it follows that equation has at most one solution. The

existence of a solution follows from the fact that is the

rate function of a LDP, and therefore must have at least one

zero. By what shown in (A.13), solves

(1.3). Hence turns out to be the unique solution of

the fixed point argument . Moreover, it satisfies all the

conditions of Theorem 2.

A.3 Proof of Theorem 3

Theorem 4

. Let be a real separable Banach space. Let be a sequence of -valued, i.i.d. random variables, defined on the probability space and denote by their common law. Define and consider a continuous map . Suppose that the following conditions are satisfied:

-

(B.1)

for all .

-

(B.2)

For any , , for some . Moreover, is three times continuously Fréchet differentiable.

-

(B.3)

Define, for (the topological dual of ), , and for , . Assume that there exists a unique such that .

-

(B.4)

Define the probability on by for a suitable normalizing factor . This probability is well defined and . Let denote the centered version of , i.e., , where is defined by . For define by . Then we assume that for every such that

-

(B.5)

is a Banach space of type 2. 222A Banach space is said to be of type if . Here and where is a Bernoulli sequence, i.e., a sequence of independent random variables such that . For more details see [3].

Now, letting be the probability on given by

| (A.14) |

where is linear, continuous and bounded on the support of the law of , uniformly in . Then, for every , the -law of the dimensional vector

converges weakly, as , to the law of a centered Gaussian vector with covariance matrix , such that for

| (A.15) |

Remark 2

.

-

i.

The Theorem in [3] is stated for . The same proof applies with our assumptions on without changes. It is likely that these assumptions can be weakened considerably.

-

ii.

The Theorem in [3] contains a stronger statement that the one given here. Indeed, it is shown that the field converges weakly to a Gaussian field, while we only stated convergence for finite dimensional distributions. This is all we need to prove Theorem 3. Our proof has not allowed to take advantage of the full strength of the Theorem in [3].

The “natural” space for the Central Limit Theorem in Theorem 3 is the set of signed measures, which is not a Banach space. To apply Theorem 4, we need to map to a Banach space of type 2.

Lemma 5

. The following properties hold true under the reciprocity condition (R):

-

i)

There exists a Banach space of type , a linear map , continuous on the set . Moreover there exist two continuous maps , where is bounded and three times Fréchet differentiable and is linear, such that

(A.16) -

ii)

For any vector there exist such that , where stands for the topological dual of .

Proof. The first step consists in giving an alternative expression for given in (1.2). Look at the term

using the reciprocity condition (R), we obtain

Note that unless . Thus

Therefore

Thus, defining

| (A.17) |

and

| (A.18) |

we have that . Lemma 2 thus holds also after replacing by . Let be a constant such that, under , the random parameters and have absolute value less that . Now we define the following maps:

where is some positive constant such that almost surely. Note that, for and , we have that . Now, let be a function such that for , for and . For

we set

| (A.19) |

and

| (A.20) |

We now claim that, for and setting ,

| (A.21) |

Moreover

| (A.22) |

so that (A.16) holds. Equation (A.21)is straightforward; (A.22) follows since

where the one to last equality follows since simultaneous jumps may happen only with zero probability. We thus have that and the claim follows by definition of .

Now set

Clearly is a Hilbert space (hence a Banach space of type 2), and the maps are trivially extended to . Moreover, the map can be completed to a -valued map by letting, for ,

where is given.

To complete the proof of part i) of Lemma 5 one has to show the desired regularity of and . The only nontrivial fact is to show regularity of the term

However, the fact that allows to control the tails of the sum above; continuity and Fréchet differentiability of any order is obtained by standard estimates, The details are omitted.

Finally, to prove part ii), for , it is enough to define for

Proof of Theorem 3.

Having identified a suitable

Banach space, Theorem 3 immediately follows from Theorem

4 applied to the sequence taking values on . Notice that in our setting

and . Theorem

3 is guaranteed by the following three facts:

-

1.

, where is the probability appearing in Theorem 4;

-

2.

;

-

3.

.

Point follows from the definition of and from

equations (A.21) and (A.22). Point is a

consequence of the fact that and . Point will be proved in details in

Lemma 8 (see in particular equation (A.35)). An

immediate application of equations (A.35) and (A.30)

finally guarantees the validity of (1.6).

Assuming point , it remains to show the validity of the

central limit theorem in . In other words we need to check the

five assumptions of Theorem 4. , and

are easy to see. and are not

straightforward. The rest of this section is devoted to the proof

that these two assumptions are satisfied.

We begin to prove . We define two sequences

of measures on as follows:

From (A.16) it can be shown that

| (A.23) |

for

and as defined in (A.19) and (A.20).

By the contraction principle (see Theorem 4.2.1 in [9]),

the sequence satisfies a LDP with the good rate function

Being the unique zero for

, has a unique zero .

A LDP for the sequence can be obtained in an alternative way. Indeed, we notice that is the law of the random variables

where are i.i.d. valued random variables with law . Thus we have that satisfies a (weak) LDP with rate function , with and . Thus, applying Varadhan’s Lemma, satisfies a (weak) LDP with rate function . Since the rate function is unique, it follows that

Having proved already that has a unique zero, the proof of (B3) is completed.

We are thus left to show : for each such that we have

| (A.24) |

where and are defined in Theorem 4.

This proof is rather technical and long. We divide it into three

steps. We first show that the measure such that

is exactly the law of the

random variable induced by .

This argument is then used in the second step to ensure the

positivity of a suitable functional .

In the last part we see how to relate to assumption .

Step 1: The key result of this first step is given in Lemma 6 below. We look at the measure on , defined by

where, as already seen, represents the law of

induced by .

We shall prove in Lemma 6 that is the law of

induced by .

Lemma 6

. The measure is the law of induced by .

Proof. We first prove the following two claims

-

i)

(A.24) for almost all .

-

ii)

(A.25) for all such that , where is defined in (A.18).

To prove the claim we need to compute , i.e. the Fréchet derivative of the function at in the direction . An explicit computation reveals that for and , is well defined and in particular

where we have put as usual for , .

We now compute

. Notice that

for all

so that

| (A.26) |

By virtue of Girsanov’s Formula for Markov chains it can be seen that

where is the law of the Markov process with generator given in (A.11). (A.24) thus follows since as shown in the proof of Theorem 2. Concerning , notice that

When , the first two terms of the last expression vanish. Moreover under the same hypothesis . Hence

| (A.27) |

Notice that

in writing the latter equality we have implicitly used the fact

that

. This is true since for any

where

stands for the supremum of in the support of

and denotes the total variation of .

As a corollary of claim above we see that

Here we have used (A.27), the fact that since and equation (A.21).

Back to the statement of the lemma, we see that for measurable and bounded

where in the last equality we have used (A.24).

Step 2: The key result of the second step is given in Lemma 7 below. It involves the measures and defined in (1.5). First of all, it is not difficult to show that is absolutely continuous w.r.t. and in particular

| (A.28) |

Indeed, observe that, given as in (1.5), we have

for any . The second equality

follows since is the law of the random variable

induced by .

Notice that

,

being the expectation under of . Hence

and (A.28) follows.

Lemma 7

. Given and in , let

| (A.29) |

where . Then

Proof. A tedious but straightforward computations provides the second order derivative of :

Notice that we have written instead of : the reciprocity condition is not necessary in this calculation. We now show that is the expected value of a square. Indeed

The latter expectation can be rewritten as

where we have used (A.28)

and where defined by ,

is the Poisson process with intensity .

Recall that defined in (1.7) is nothing but its

compensated martingale. Hence

By the isometry property of square integrable martingales (and relying on the same argument used to prove (2.5)), we have

Hence

| (A.30) |

is thus the expected value of a square, hence it cannot be negative. For this reason, we simply need to prove that it is non-zero. Without loss of generality we take . Suppose by way of contradiction that . Then necessarily

Using the fact that

where the last equality follows since . We rewrite the expression above as

| (A.31) |

On the other hand, define , where

Notice that

Taking the conditional expectation in (A.31), we obtain

We now take the -norm in both sides. For all we have

Notice that , where . The first inequality follows since ; the second one is trivial and the latter one is due to the fact that is a submartingale and thus its expected value is an increasing function of time. Then

where is a constant such that .

As a consequence, , for .

This argument can be iterated defining .

The same argument shows that , for

; hence , for .

Eventually we extend the statement to . Being , we would have and this gives a contradiction.

Hence the thesis follows.

Step 3: Consider . Since , for , are in the topological dual of , there exist such that . We define

where we recall that , defined in of Theorem 4, is the centered version of the law of induced by . Then the following result holds true

Lemma 8

.

-

i)

-

ii)

For we have

Proof. Point . By the definition of and we see that

where we have used the fact that .

Concerning the second statement, we first prove the following claim.

| (A.32) |

To show the validity of (A.32), we use the following two facts:

The former follows by definition of , and , whereas the latter

is a consequence of the definition of given in (1.5).

(A.32) is a consequence of the fact that is both linear and continuous,

hence we are allowed to interchange the operator with the expectation.

Having proved (A.32), we compute the second order Fréchet

derivatives on the function as follows.

| (A.33) |

Notice that, by the linearity of and by (A.32), we have that

Thus

We now claim that

| (A.34) |

By (A.25) we see that since . Moreover both and since is absolutely continuous with respect to . This proves (A.34). Finally we use the fact that is Fréchet differentiable

We have thus proved that .

References

- [1] Ben Arous, G., Brudaud, M., Méthode de Laplace: étude variationnelle des fluctuations de diffusions de type “champ moyens“, Stochastics and Stochastic Reports 31, pp. 79-144, 1990.

- [2] Brezis, H., Analyse fonctionnelle - Théorie et applications, Masson Editeur, Paris, 1983.

- [3] Bolthausen, E. Laplace approximations for sums of independent random vectors, Probability Theory and Related Fields 72, pp.305-318, 1986.

- [4] Comets, F., Eisele, Th. Asymptotic Dynamics, Non-Critical and Critical Fluctuations for a Geometric Long-Range Interacting Model, Communications in Mathematical Physics 118, 531-567, 1988.

- [5] Crouhy, M., Galai, D., Mark, R. A comparative analysis of current credit risk models, Journal of Banking and Finance, 24, 59-117, 2000.

- [6] Dai Pra, P., Den Hollander, F. McKean-Vlasov Limit for Interacting Random Processes in Random Media, Journal of Statistical Physics, vol. 84, no3-4:735-772, 1996.

- [7] Dai Pra, P., Runggaldier, W.J., Sartori, E., Tolotti, M., Large portfolio losses; A dynamic contagion model., (forthcoming on Annals Applied Probability), arXiv:0704.1348v2, 2008.

- [8] Dembo,D., Deuschel, J.D., Duffie, D. Large portfolio losses, Finance and Stochastics, 8:3-16, 2004.

- [9] Dembo, A., Zeitouni O. Large Deviations Techniques, Jones and Bartlett Publishers, Boston, London, 1993.

- [10] Embrechts, P., Frey, R., McNeil, A. Quantitative Risk Management: Concepts, Techniques and Tools, Princeton Series in Finance, 2005.

- [11] Ethier, S.N., Kurtz, T.G. Markov Processes, Characterization and Convergence, John Wiley and Sons, 1986.

- [12] Frey, R., Backhaus, J. Credit Derivatives in Models with interacting default intensities: A Markovian approach, Preprint, 2006.

- [13] Frey, R., Backhaus, J. Dynamic hedging of syntentic CDO tranches with spread risk and default contagion, Working paper, 2007.

- [14] Frey, R., McNeil, A. VaR and Expected shortfall in portfolios of dependent credit risks: Conceptual and practical insights, Working paper, 2002.

- [15] Giesecke, K., Goldberg, L., A top.down approach to multi-name credit, Working paper, 2007.

- [16] Giesecke, K., Weber, S. Cyclical correlations, credit contagion and portfolio losses, Journal of Banking and Finance 28(12): 3009-3036, 2005.

- [17] Pham, H. Some applications and methods of large deviation in finance and insurance, arXiv PR/0702473v2, 2007.

- [18] Schönbucher, P., Portfolio losses and the term structure of loss transition rates: a new methodology for the pricing of portfolio credit derivatives, Working paper, 2006.

- [19] Tolotti, M. The impact of contagion on large portfolios. Modeling aspects, Ph.D. thesis, Scuola Normale Superiore, 2008.

- [20] Varadhan, S.R.S. Large deviations and applications, Society for Industrial and Applied Mathematics, Philadelphia, 1984.