Stochastic Control up to a Hitting Time: Optimality and Rolling-horizon Implementation

Abstract.

We present a dynamic programming-based solution to a stochastic optimal control problem up to a hitting time for a discrete-time Markov control process. First we determine an optimal control policy to steer the process toward a compact target set while simultaneously minimizing an expected discounted cost. We then provide a rolling-horizon strategy for approximating the optimal policy, together with quantitative characterization of its sub-optimality with respect to the optimal policy. Finally we address related issues of asymptotic discount-optimality of the value-iteration policy.

2000 Mathematics Subject Classification:

Primary: 90C39, 90C40; Secondary: 93E201. Introduction

Optimal control of Markov control processes (MCP) up to an exit time is a problem with a long and rich history. It has mostly been studied as the minimization of an expected undiscounted cost until the first time that the state enters a given target set, see e.g., [12, Chapter II], [20, Chapter 8], and the references therein. In particular, if a unit cost is incurred as long as the state is outside the target set, then the problem of minimizing the cost accumulated until the state enters the target is known variously as the pursuit problem [16], transient programming [34], the first passage problem [15, 25], the stochastic shortest path problem [6], and control up to an exit time [11, 12, 24]. These articles deal with at most countable state and action spaces. The problem of optimally controlling a system until an exit time from a given set has gained significance in financial and insurance mathematics, see, e.g., [10, 32].

Our interest in this problem stems from our attempts to develop a general theory of stochastic model-predictive control (MPC). In its bare essentials, deterministic MPC [26] consists of two steps: (i) solving a finite-horizon optimal control problem with constraints on the state and the controlled inputs to get an optimal policy, and (ii) applying a controller derived from the policy obtained in step (i) in a rolling-horizon fashion. Theoretical foundation of stochastic MPC is still in its infancy, see [29, 7, 33, 14, 2] and the references therein for some related work. In view of its close relationship with applications, any satisfactory theory of stochastic MPC must necessarily take into account its practical aspects. In this context an examination of a standard linear system with constrained controlled inputs affected by independent and identically distributed (i.i.d.) unbounded (e.g., Gaussian) disturbance inputs shows that no control policy can ensure that with probability one the state stays confined to a bounded safe set for all instants of time. This is because the noise is unbounded and the samples are independent of each other. Although disturbances are not likely to be unbounded in practice, assigning an a priori bound seems to demand considerable insight. In case a bounded-noise model is adopted, existing robust MPC techniques [4, 8] may be applied, in which the central idea is to synthesize a controller based on the bounds of the noise such that the target set becomes invariant with respect to the closed-loop dynamics. However, since the optimal policy is based on a worst-case analysis, it usually leads to rather conservative controllers and sometimes even to infeasibility. Moreover, complexity of the optimization problem grows rapidly (typically exponentially) with the optimization horizon. An alternative is to replace the hard constraints by probabilistic (soft) ones. The idea is to find a policy that guarantees that the state constraints are satisfied with high probability over a sufficiently long time horizon. While this approach may improve feasibility aspects of the problem, it does not address the issue of what actions should be taken once the state violates the constraints. See [23, 22, 1] for recent results in this direction.

In view of the above considerations, developing recovery strategies appears to be a necessary step. Such a strategy is to be activated once the state violates the constraints and to be deactivated whenever the system returns to the safe set. In general, a recovery strategy must drive the system quickly to the safe set while simultaneously meeting other performance objectives. In the context of MPC, two merits are immediate: (a) once the constraints are transgressed, appropriate actions can be taken to bring the state back to the safe set quickly and optimally, and (b) if the original problem is posed with hard constraints on the state, in view of (a) they may be relaxed to probabilistic ones to improve feasibility.

In this article we address the problem of synthesizing optimal recovery strategies. We formulate the problem as the minimization of an expected discounted cost until the state enters the safe set. An almost customary assumption in the literature (see, e.g., [21] and the references therein,) concerned with stochastic optimal control up to an exit time is that the target set is absorbing. That is, there exists a control policy that makes the target set invariant with respect to the closed-loop stochastic dynamics. This is rather restrictive for MPC problems—it is invalid, for instance, in the very simple case of a linear controlled system with i.i.d. Gaussian noise inputs. We do not make this assumption, for, as mentioned above, our primary motivation for solving this problem is precisely to deal with the case that the target set is not absorbing. As a result of this, it turns out that the dynamic programming equations involve integration over subsets of the state-space and therefore are difficult to solve. At present there is no established method to solve such equations in uncountable state-spaces. However, in finite state-space cases tractable approximate dynamic programming methods [5, 28] may be employed to arrive at suboptimal but efficient policies.

This article unfolds as follows. In §2 we define the general setting of the problem, namely, Markov control processes on Polish spaces, their transition kernels and the main types of control strategies. In §3 we establish our main Theorem 3.7 under standard mild hypotheses. This result guarantees the existence of a deterministic stationary policy that leads to the minimal cost and also provides a Bellman equation that the value function must satisfy. A contraction mapping approach to the problem is pursued in §4 under the (standard) assumption that the cost-per-stage function satisfies certain growth-rate conditions. The main result (Proposition 4.6) of this section asserts both the existence and uniqueness of the optimal value function. Asymptotic discount-optimality of the value-iteration policy is investigated in §5 under two different sets of hypotheses; in particular, the results of this section show that rolling-horizon strategy approaches optimality as the length of the horizon window increases to infinity. A rolling-horizon strategy corresponding to our optimal control problem is developed in §7; in Theorem 7.2 we establish quantitative bounds on the degree of sub-optimality of the rolling-horizon strategy with respect to the optimal policy. We conclude in §9 with a discussion of future work. The state and control/action sets are assumed to be Borel subsets of Polish spaces.

2. Preliminaries

We employ the following standard notations. Let denote the natural numbers , and denote the nonnegative integers . Let be the standard indicator function of a set , i.e., if and otherwise. For two real numbers and , let .

Given a nonempty Borel set (i.e., a Borel subset of a Polish space), its Borel -algebra is denoted by . By convention “measurable” means “Borel-measurable” in the sequel. If and are nonempty Borel spaces, a stochastic kernel on given is a mapping such that is a probability measure on for each fixed , and is a measurable function on for each fixed . We let be the family of all stochastic kernels on given .

We briefly recall some standard definitions.

2.1 Definition.

A Markov control model is a five-tuple

| (2.2) |

consisting of a nonempty Borel space called the state space, a nonempty Borel space called the control or action set, a family of nonempty measurable subsets of , where denotes the set of feasible controls or actions when the system is in state , and with the property that the set of feasible state-action pairs is a measurable subset of , a stochastic kernel on given called the transition law, and a measurable function called the cost-per-stage function.

2.3 Assumption.

The set of feasible state-action pairs contains the graph of a measurable function from to .

We let , , and denote the set of all randomized and history-dependent admissible policies, randomized Markov, deterministic Markov and deterministic stationary policies, respectively. For further details and notations on policies see, e.g., [19]. Consider the Markov control model (2.2), and for each define the space of admissible histories up to time as , and for . A generic element of , called an admissible -history is a vector of the form , with for and . Hereafter we let the -algebra generated by the history be denoted by , . Let be the measurable space consisting of the (canonical) sample space , and is the corresponding product -algebra. Let be an arbitrary control policy and an arbitrary probability measure on , referred to as the initial distribution. By a theorem of Ionescu-Tulcea [30, Chapter 3, §4, Theorem 5], there exists a unique probability measure on supported on , and such that for all , , and , , and

| (2.4a) | ||||

| (2.4b) | ||||

The stochastic process is called a discrete-time Markov control process. Let denote the set of stochastic kernels in such that for all , and let denote the set of all measurable functions satisfying for all . The functions in are called selectors of the set-valued mapping .

The transition kernel in (2.4b) under a policy is given by , defined as . Occasionally we suppress the dependence of on and write in place of . The cost-per-stage function at the -th stage under a policy is written as . We simply write and , respectively, for policies and .

Since we shall be exclusively concerned with Markov policies and its subclasses, in the sequel we use the notation for the class of all randomized Markov strategies.

3. Expected Discounted Cost up to the first Exit Time

Let be a measurable set, and let .111As usual the infimum over an empty set is taken to be . We note that is an -stopping time. Let us define

as the -discounted expected cost under policy corresponding to the Markov control process .222We employ the standard convention that a summation from a higher to a lower index is defined to be . Our objective is to minimize over a class of control policies , i.e., find the -discount value function

| (3.1) |

A policy that attains the infimum above is said to be -discount optimal.

3.2 Remark.

As mentioned in the introduction, the optimization problem (3.1) with and the cost-per-stage function is known as the stochastic shortest path problem. The objective of this problem is to drive the state to a desired set ( in our case) as soon as possible, and the expected cost for a policy corresponding to the above cost-per-stage function is readily seen to be . In this light we observe that the minimization problem in (3.1) with the cost-per-stage function can be viewed as a discounted stochastic shortest path problem. It follows immediately that the corresponding expected cost is . Note that the minimization of over a class of policies is always well-defined for . Moreover, because of the monotonic behavior of the map , one may hope to get a good approximation of the original stochastic shortest path problem. However, pathological examples can be constructed to show that a solution to the stochastic shortest path problem may not exist, whereas minimization of is always well defined, although in either case the state may never reach the desired set almost surely-.

3.3 Remark.

Given a cost-per-stage function on , one can redefine it to be to turn the problem (3.1) into the minimization of for . This cost functional can be equivalently written as an infinite horizon cost functional, as in , or as in . However, the absence of a policy that guarantees that stays inside for all time after necessarily means that the problem (3.1) corresponding to the Markov control model in Definition 2.1 is not equivalent to the minimization of the infinite horizon cost functional .

3.4.

A word about admissible policies. It is clear at once that the class of admissible policies for the problem (3.1) is different from the classes considered in §2. Indeed, since the process is killed at the stopping time , it follows that the class of admissible policies should also be truncated at the stage . For a given stage we define the -th policy element only on the set . Note that with this definition becomes a -measurable randomized control (in general). It is also immediate from the definition of that if the initial condition is inside , then the set of admissible policies is empty; indeed, in this case , and there is no control needed. In other words, the domain of is contained in the “spatial” region ; since is not defined on , this is equivalent to being well-defined on .

3.5.

Some re-definitions. To simplify the formulas from now on we let the cost-per-stage function to be defined on . With this convention in place our problem (3.1) can be posed as the minimization of over admissible policies. Also, henceforth we redefine the set of state-action pairs to be , and we note that this new set is a measurable subset of the original set of state-action pairs. Also, we let be the set of selectors of the set-valued mapping .

Recall that a function is said to be inf-compact on if for every and the set is compact. A transition kernel on a measurable space given another measurable space is said to be strongly Feller (or strongly continuous) if the mapping is continuous and bounded for every measurable and bounded function . A function is lower semicontinuous (l.s.c.) if for every sequence converging to , we have ; or, equivalently, if for every , the set is closed in .

3.6 Assumption.

In addition to Assumption 2.3, we stipulate that

-

(i)

the set is compact for every ,

-

(ii)

the cost-per-stage is lower semicontinuous, nonnegative, and inf-compact on , and

-

(iii)

the transition kernel is strongly Feller.

The following is our main result on expected discounted cost up to the first time to hit ; a proof is presented later in this section.

3.7 Theorem.

Suppose that Assumption 3.6 holds. Then

-

(i)

The -discount value function is the (positive) minimal measurable solution to the -discounted cost optimality equation (-DCOE)

(3.8) - (ii)

We observe that Theorem 3.7 does not assert that the optimal value function is unique in any sense. In §4 we prove a result (Proposition 4.6) under additional hypotheses that guarantees uniqueness of .

Since we do not assume that the cost-per-stage function is bounded, a useful approach is to consider the -value iteration (-VI) functions defined by

| (3.10) |

Of course we have to demonstrate that for all .

The functions , , may be identified with the optimal cost function for the minimization of the process stopped at the -th step, i.e.,

To get an intuitive idea, fix a deterministic Markov policy , and take the first iterate . From (3.10) it is immediately clear that if , and not defined otherwise. For the second iterate, we have

Note that only those sample paths that do not enter at the first step contribute to the cost at the second stage. This property is ensured by the indicator function that appears on the right-hand side of the last equality above.

3.11 Example.

Let be a Markov chain with state-space and transition probability matrix , where the argument of depicts the dependence on the action with being a compact subset of . Let for , fix and let . Suppose further that for all ; this means, in particular, that the target set cannot be absorbing for any deterministic stationary policy. Our objective is to find an optimal policy corresponding to the the minimal cost (3.9). The optimal value function is on and for every we have . The most elementary case is that of ; then , and given a sufficiently regular function this can be solved at once to get , which characterizes the function (vector) completely. The optimal policy in this case is ; if the function is convex, then the minimum is attained on and thus leads to a unique optimal policy.

Proof of Theorem 3.7

Recall from paragraph 3.5 that is defined on , and is the set of selectors of the set-valued map . We begin with a sequence of Lemmas.

3.12 Lemma ([19, Lemma 4.2.4]).

Let the functions and , , be l.s.c., inf-compact and bounded below. If , then

3.13 Lemma (Adapted from [31]).

Suppose that

-

•

is compact for each and is a measurable subset of , and

-

•

is a measurable inf-compact function, is l.s.c. on for each .

Then there exists a selector such that

and is a measurable function.

3.14 Definition.

Let denote the convex cone of nonnegative extended real-valued measurable functions on , and for every let us define the map by

| (3.15) |

The map is the dynamic programming operator corresponding to our problem (3.1).

Having defined the dynamic programming operator above, it is important to distinguish conditions under which the function is measurable for . We have the following lemma.

3.16 Lemma.

Proof.

Fix . The strong-Feller property of on and lower-semicontinuity of the cost-per-stage function defined on show that the map

is lower-semicontinuous. From nonnegativity of it follows that for every and ,

| (3.18) |

and the set is compact by inf-compactness of . Since by definition , by Lemma 3.13 it would follow that a selector exists such that once we verify the hypotheses of this Lemma. For this we only have to verify that is l.s.c. (which implies it is measurable) and inf-compact on . We have seen above that is a l.s.c. function on . Therefore, for each the map is also l.s.c. on . Thus, by definition of lower semicontinuity, the set in (3.18) is closed for every and . Since a closed subset of a compact set is compact, it follows that is compact, which in turn shows inf-compactness of on and proves the assertion. ∎

The following lemma shows how functions satisfying relate to the optimal value function.

3.19 Lemma.

Suppose that Assumption 3.6 holds. If is such that , then .

Proof.

Suppose satisfies , and let be a selector (whose existence is guaranteed by Lemma 3.16) that attains the infimum in (3.15). Fix . We have

The operator in (3.15) is monotone, for if are two functions with , then clearly due to nonnegativity of . Therefore, iterating the above inequality for a second time we obtain

After such iterations we arrive at

Since , letting we get

Since is arbitrary, the assertion follows. ∎

The next lemma deals with convergence of the value iterations to the optimal value function.

3.20 Lemma.

Proof.

Note that since for , it follows that

and therefore, taking the infimum over all policies on the right hand side, we get

| (3.21) |

Since the cost-per-stage function is nonnegative, is a monotone operator. Therefore, since and for , it follows that the -VI functions form a nondecreasing sequence in , which implies that for some function . For we define

The monotone convergence theorem guarantees that pointwise on . As in the proof of Lemma 3.16 one can establish inf-compactness and lower semicontinuity of , and on . From Lemma 3.12 it now follows that for every we have

This shows that satisfies the -DCOE, .

3.22 Lemma.

For every deterministic stationary policy we have

| (3.23) |

Proof.

Proof of Theorem 3.7.

(i) That is a solution of the -DCOE follows from Lemma 3.20, and that is the minimal solution follows from Lemma 3.19, since implies .

(ii) Lemma 3.16 guarantees the existence of a selector such that (3.9) holds. Fix and . As in the proof of Lemma 3.19, iterating equation (3.9) -times we arrive at

By the monotone convergence theorem we have

which shows that , and since is arbitrary, it follows that . The reverse inequality follows from the definition of in (3.1). We conclude that , and that is an optimal policy.

4. A Contraction Mapping Approach

For the purposes of this section we let denote the real vector space of real-valued measurable functions on , and be the convex cone of nonnegative elements of . (Note that according to paragraph 3.5 we let the elements of take the value .) Given a measurable weight function in , we define the weighted norm . It is well-known that is a Banach space.

4.1 Assumption.

In addition to Assumption 3.6, we require that there exist , , and a measurable weight function such that for every

-

(i)

;

-

(ii)

.

4.2 Remark.

If is bounded, the weight function may be taken to be . Also, if and are the current and the next states of the Markov control process, respectively, then Assumption 4.1(ii) implies that

We observe that this bears a resemblance with classical Lyapunov-like stability criteria, more specifically, the Foster-Lyapunov conditions [27, Chapter 8], [17]. However, the condition in Assumption 4.1(ii) is uniform over the set of actions pointwise in . It connects the growth of the cost-per-stage function with a contraction induced by the discount factor .

Recall that a mapping on a nonempty complete metric space is a contraction if there exists a constant such that for all . The constant is said to the the modulus of the map . A contraction has a unique fixed point satisfying .

4.3 Proposition ([20, Proposition 7.2.9]).

Let be a monotone map from the Banach space into itself. If there exists a such that

| (4.4) |

then is a contraction with modulus .

We have the following lemma.

Proof.

Fix with . As in the proof of Lemma 3.16, the mapping

is well-defined and l.s.c. in for all . By the same Lemma we also know that maps into . For every , by Assumption 4.1,

which shows that . Therefore, maps into itself. Since , it is clear that is a monotone map on . By Assumption 4.1(ii), for and we have

This shows that (4.4) holds with , and Proposition 4.3 implies that is a contraction on . ∎

The following proposition establishes bounds for the distance between the optimal value function and the -VI functions by employing the contraction mapping of Lemma 4.5.

4.6 Proposition.

Proof.

(i) Let be an arbitrary Markov policy. Trivially we have . Fix , and a history . In view of Assumption 4.1(ii), on the event we have

which shows that . Iterating this inequality we arrive at . Also, by Assumption 4.1(i) we have for all such that , which in conjunction with the above inequality gives

| (4.7) |

By the monotone convergence theorem and (4.7) we have

| (4.8) | ||||

It follows immediately that .

(ii) By definition, the -VI functions satisfy , with . Since is a contraction on by Lemma 4.5, it follows that has a unique fixed point, which, by definition is , since by (i). A standard property of contraction maps implies that

With the bound on obtained in (i), we get . Since is also a contraction on , , and , the last inequality yields for every .

Note that the conditions in Assumption 4.1 are automatic if is bounded. This gives the following straightforward result.

5. Asymptotic Discount Optimality of the -VI Policy

We have seen that the -value iteration functions defined in (3.10) converge to by Lemma 3.20. In this section we address the question whether the -VI policies converge in some sense to a policy as .

5.1 Definition.

Let be the sequence of -VI functions in (3.10), and let be a deterministic Markov policy such that is arbitrary, and for ,

Then is called an -VI policy.

Under Assumption 3.6 we get the following basic existential result.

5.2 Proposition.

The proof is based on the following immediate adaptation of [19, Lemma 4.6.6].

5.3 Lemma.

Let and , , be l.s.c. functions, bounded below, and inf-compact on . For every let and , let be a selector such that for all . If is locally compact and , then there exists a selector such that is an accumulation point of the sequence for every , and .

Proof of Proposition 5.2.

Under the stronger Assumption 4.1 we get quantitative estimates of the rate at which the -VI policy defined in Definition 5.1 converges to an optimal one.

5.5 Definition.

The function defined by

is called the -discount discrepancy function. The -VI policy defined in Definition 5.1 is called pointwise asymptotically discount optimal if for every we have .

It is clear that for and a selector (see paragraph 3.5), the -discount discrepancy function is if and only if is an optimal policy. The function measures closeness to an optimal selector in a weak sense.

5.6 Proposition.

Suppose that Assumption 4.1 holds, and let . Then the -VI policy is pointwise asymptotically discount optimal, and for every and ,

Proof.

The first inequality follows directly from the definition of . To prove the second inequality fix . We see that by the definition of the discrepancy function,

| (5.7) | ||||

By Proposition 4.6(ii) we have

| (5.8) |

and in the light of Assumption 4.1(ii) we arrive at

| (5.9) | ||||

The assertion follows immediately after substituting (5.8) and (5.9) in (5.7). ∎

For bounded costs we have the following straightforward conclusion.

5.10 Corollary.

Suppose that Assumption 3.6 holds, and . Then the -VI policy is pointwise asymptotically discount optimal, and for every and ,

6. Average cost of recovery

As mentioned in §1, a motivation for this work was to come up with a suitable recovery strategy for MPC. Tracing our development of the MPC methodology in §1, one sees that in the presence of state and/or action constraints, one seeks a deterministic stationary policy that is active whenever the state is inside the safe set , and a recovery strategy outside . Let us assume that for a given problem we have determined such a policy, and we have also determined a deterministic stationary policy corresponding to the recovery strategy corresponding to a cost-per-stage function defined on for the same problem as described in the preceding sections. One of the natural questions at this stage is whether one can find estimates of the average cost of recovery.

To this end let us define two constants:

| (6.1) |

where is as defined in (3.1). Let be the deterministic stationary policy defined by

| (6.2) |

to wit, consists of concatenation of and between exit and entry times to . We have the following result:

6.3 Proposition.

Let be a deterministic stationary policy that is active whenever the state is inside the set , and let be a recovery strategy corresponding to the problem (3.1). Let the initial condition be in . We define the average cost of recovery

where is as defined in (6.2), , is the first entry time to , is the first exit time from after , and so on. Suppose that from any initial condition in the first hitting time of is finite almost surely under , and from any initial condition in the first hitting time of is finite almost surely under . Then we have , where are as defined in (6.1).

Note that an identical bound holds if the initial condition , with an obvious relabelling of the stopping times .

Proof.

First of all, note that the policy is deterministic stationary, and under this policy the controlled process is stationary Markov. Now we have for a fixed :

| (6.4) | ||||

where the first equality follows from monotone convergence and the last equality from the strong Markov property. Appealing to the strong Markov property once again we see that . Finally, from the definition of it follows that

It is not difficult to arrive at the lower bound by following the same steps as above. Substituting in (6.4) and taking limits we arrive at the assertion. ∎

7. A Rolling Horizon Implementation

The rolling-horizon procedure can be briefly described as follows. Fix a horizon and set . Then

-

(a)

we determine an optimal control policy, say , for the -period cost function starting from time , given the (perfectly observed) initial condition ; standard arguments lead to a realization of this policy as a sequence of selectors ;

-

(b)

we increase to , and go back to step (a).

Accordingly, the -th step of this procedure consists of minimizing the stopped -period cost function starting at time , namely, the objective is to find a control policy that attains

| (7.1) |

for . By stationarity and Markovian nature of the control model, it is enough to consider the control problem of minimizing the cost for , i.e., the problem of minimizing over . The corresponding policy is given by the policy that minimizes the -stage -VI function in (3.10). This particular policy is realized as a sequence of selectors . Thus, in the light of the above discussion, the rolling-horizon procedure yields the stationary suboptimal control policy for the original problem (3.1).

Let be the value function corresponding to the deterministic stationary policy , . Observe that , which follows from the more general estimate in (4.8). Our objective in this section is to give quantitative estimates of the extent of sub-optimality of the rolling-horizon policy , compared to the optimal policy that attains the infimum in (3.1). We shall follow the notations of §4 above.

7.2 Theorem.

A proof of Theorem 7.2 is given in the Appendix, if follows the arguments in [3, Theorem 1] for finite state-space Markov decision processes and bounded costs. It is of interest to note that the bound in (7.3) is identical to the bound between and that appears in Proposition 4.6.

If the cost-per-stage function is bounded on , we have the following immediate corollary:

7.5 Corollary.

Suppose the Markov control process satisfies Assumption 3.6. Let the cost-per-stage function be bounded, with . Then for every , and

8. Application

In this section we give a numerical example concerning fishery management. The example is motivated by [18, Chapter 7]. The example considers a fishery modeled in discrete-time with the time period representing a fishing season. The state of the controlled Markov chain is the population of the fish species of interest. Fishermen might on the one hand want to harvest all that they can manage in order to increase their short-run profit, but on the other hand this might lead to very low levels of the population. Our goal is to design a recovery strategy for the case that the population gets over-fished and goes below a critical level.

For doing so, we consider a simple model, with four possible fish population levels, 1 (almost extinct), 2, 3, and 4 (the target set). We assume that we can accurately measure the population size at the beginning of each season , . During a season the following set of actions are available: Harvest (1), Harvest less (2), Do nothing (3), Import fish (4), Import less (5). We also take as given the following transition probabilities between the Markov States, where denotes the probability that the population level at the beginning of the next season will be , given that the current population is and action is applied during this season.

The costs incurred at each state are , where

represents a cost incurred for being at the current state and

the action cost associated with each action and state. We assume a discount factor .

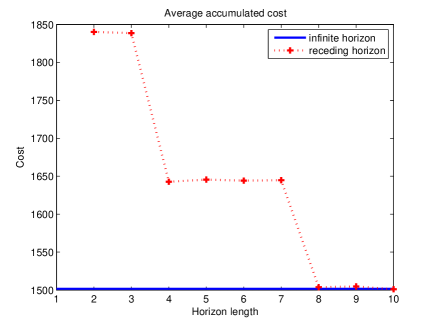

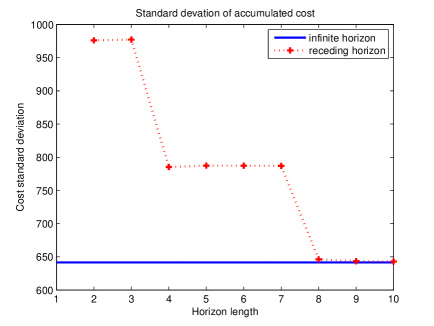

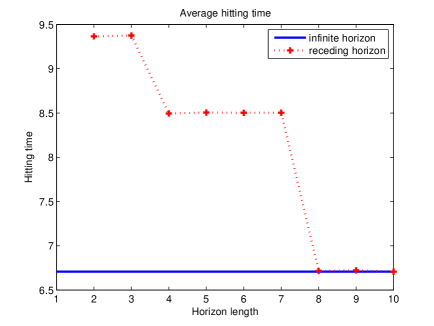

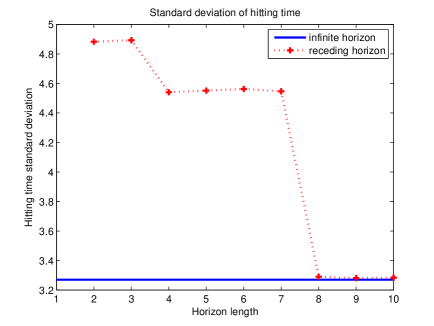

Using this setting, one can compute the policy that attains the -discount value function (3.1). This turns out to be to import fish when in state , to import fewer fish in state , and do nothing at state . Next, we search for the optimum policy, while using a rolling horizon control scheme, i.e., finding the policy that attains (7.1). We solve the problem for horizon lengths between and , in order to compare the results with the infinite horizon optimal policy.

Figure 1 shows the average and the standard-deviation of the accumulated costs over Monte Carlo runs, with the initial population level at state . Similarly, Figure 2 shows the average and the standard-deviation of the time steps needed for the recovery into the target state . The results suggest that for the rolling horizon policy to match the optimal infinite horizon one, a horizon length of at least should be used. Smaller horizons provide sub-optimal policies (with respect to the infinite horizon one), with the sub-optimality gap reducing as the horizon length increases. Note that the case of is not included in the data; this is because for horizon length of the optimal policy is to harvest while the system is at state , leading to an cost and recovery time, which does not allow the system to ever recover to state .

9. Future Work

We established in §3 that the optimal value function is the minimal solution of the -discounted cost optimality equation (3.8). However, obtaining analytical expression of the optimal value function is difficult, particularly due to the integration over a subset of the state space. Obtaining good approximations of is of vital importance, and will be reported in subsequent articles.

It is interesting to note that our basic framework of stochastic model-predictive control (described in §1) naturally leads to a partitioning of the state-space with different dynamics in each partition; thus, the controlled system may be viewed as a stochastic hybrid system. One of the basic questions in this context is that of stability of the controlled system, and in view of the fact that in general there will be infinitely many excursions of the state outside the safe set, establishing any stability property is a challenging task. Classical Lyapunov-based methods are difficult to apply directly precisely because of the infinitely many state-dependent switches between multiple regimes, each with different dynamics. However, excursion-theory of Markov processes [9] enables us to establish certain stability properties of quite general stochastic hybrid systems with state-dependent switching; some of these results are reported in [13].

Acknowledgments

The authors are grateful to Vivek S. Borkar, Onésimo Hernández-Lerma, and Sean P. Meyn for illuminating discussions and pointers to relevant literature. They also thank the anonymous reviewers for their helpful comments.

Appendix A Proof of Theorem 7.2

Proof of Theorem 7.2.

For brevity of notation in this proof, we let , and let denote the (ordered) elements of the policy from stage through for . The first inequality in (7.3) is trivial because for all . Before the proof of the second inequality in (7.3), let us fix some notation. Pick . For , a policy for stages through , and , let denote -th element of the policy . Also, let denote the sub-stochastic kernel333Recall that is a sub-stochastic kernel on given if is a measurable function on for each , and is a measure on with for each . defined for by

for .

Let be an optimal policy for stages through , i.e., let attain the infimum in (7.1). Fix . Let be an -period policy starting from stage , such that its first elements are identical to the last elements of , i.e., for . By optimality of we have

Since by construction, conditional on ,

| (A.1) |

By definition of we have

and the right-hand side equals

In conjunction with (A.1) and conditional on , we have

To wit, conditional on ,

Let be a selector that attains the minimal value of

whenever , and let the corresponding minimal value be denoted by ; clearly is well-defined on , and is a measurable function of . With this notation, the last inequality becomes

whenever . Therefore,

Rearranging and summing over we arrive at

| (A.2) |

In (A.2) we have employed the notation for any policy . We observe that the left-hand side of (A.2) is just . By Assumption 4.1(i),

and by Assumption 4.1(ii),

We notice that since , the first series on the right-hand side of (A.2) is at most

| (A.3) |

For a fixed , the quantity is at most in view of Assumption 4.1(ii) and the definition of the stochastic kernel at the beginning of this proof. Therefore,

This shows that series in (A.3) is summable. Hence, cancellations of the telescopic terms in the first series on the right-hand side of (A.2) are justified. The inequality in (A.2) now simplifies to

| (A.4) |

By Assumption 4.1(ii) and the definition of , conditional on ,

Substituting the last inequality in (A.4) we arrive at

which is the second bound in (7.3). The inequality (7.4) follows immediately from the fact that for every . ∎

References

- [1] M. Agarwal, E. Cinquemani, D. Chatterjee, and J. Lygeros, On convexity of stochastic optimization problems with constraints. To be presented at the ECC 2009, 2008.

- [2] I. Batina, Model predictive control for stochastic systems by randomized algorithms, PhD thesis, Technische Universiteit Eindhoven, 2004.

- [3] J. M. Alden and R. L. Smith, Rolling horizon procedures in nonhomogeneous Markov decision processes, Operations Research, 40 (1992), pp. S183–S194.

- [4] A. Bemporad and M. Morari, Robust model predictive control: a survey, Robustness in Identification and Control, 245 (1999), pp. 207–226.

- [5] D. Bertsekas and J. Tsitsiklis, Neuro-Dynamic Programming, Athena Scientific, 1996.

- [6] D. P. Bertsekas, Dynamic Programming and Optimal Control, vol. 2, Athena Scientific, 3 ed., 2007.

- [7] D. Bertsimas and D. B. Brown, Constrained stochastic LQC: a tractable approach, IEEE Transactions on Automatic Control, 52 (2007), pp. 1826–1841.

- [8] F. Blanchini, Set invariance in control, Automatica, 35 (1999), pp. 1747–1767.

- [9] R. M. Blumenthal, Excursions of Markov processes, Probability and its Applications, Birkhäuser Boston Inc., Boston, MA, 1992.

- [10] K. Boda, J. A. Filar, Y. Lin, and L. Spanjers, Stochastic target hitting time and the problem of early retirement, IEEE Transactions on Automatic Control, 49 (2004), pp. 409–419.

- [11] V. S. Borkar, A convex analytic approach to Markov decision processes, Probabability Theory and Related Fields, 78 (1988), pp. 583–602.

- [12] , Topics in Controlled Markov Chains, vol. 240 of Pitman Research Notes in Mathematics Series, Longman Scientific & Technical, Harlow, 1991.

- [13] D. Chatterjee and S. Pal, An excursion-theoretic approach to stability of stochastic hybrid systems. http://arxiv.org/abs/0901.2269, 2008.

- [14] P. D. Couchman, M. Cannon, and B. Kouvaritakis, Stochastic MPC with inequality stability constraints, Automatica J. IFAC, 42 (2006), pp. 2169–2174.

- [15] C. Derman, Finite State Markovian Decision Processes, vol. 67 of Mathematics in Science and Engineering, Academic Press, New York, 1970.

- [16] J. H. Eaton and L. A. Zadeh, Optimal pursuit strategies in discrete-state probabilistic systems, Transactions of the ASME Ser. D. J. Basic Engineering, 84 (1962), pp. 23–29.

- [17] S. Foss and T. Konstantopoulos, An overview of some stochastic stability methods, Journal of Operations Research Society of Japan, 47 (2004), pp. 275–303.

- [18] K. Hastings, Introduction to the Mathematics of Operations Research, Pure and Applied Mathematics, 128, 1989.

- [19] O. Hernández-Lerma and J. B. Lasserre, Discrete-Time Markov Control Processes: Basic Optimality Criteria, vol. 30 of Applications of Mathematics, Springer-Verlag, New York, 1996.

- [20] , Further Topics on Discrete-Time Markov Control Processes, vol. 42 of Applications of Mathematics, Springer-Verlag, New York, 1999.

- [21] K. Hinderer and K.-H. Waldmann, Algorithms for countable state Markov decision models with an absorbing set, SIAM Journal on Control and Optimization, 43 (2005), pp. 2109–2131 (electronic).

- [22] D. Chatterjee, P. Hokayem and J. Lygeros, Stochastic model predictive control with bounded control inputs: a vector space approach. http://arxiv.org/abs/0903.5444, 2009.

- [23] P. Hokayem, D. Chatterjee, and J. Lygeros, On stochastic model predictive control with bounded control inputs. http://arxiv.org/abs/0902.3944, 2009.

- [24] H. Kesten and F. Spitzer, Controlled Markov chains, Annals of Probability, 3 (1975), pp. 32–40.

- [25] H. Kushner, Introduction to Stochastic Control, Holt, Rinehart and Winston, Inc., New York, 1971.

- [26] J. M. Maciejowski, Predictive Control with Constraints, Prentice Hall, 2001.

- [27] S. P. Meyn, Control Techniques for Complex Networks, Cambridge University Press, Cambridge, 2008.

- [28] W. B. Powell, Approximate Dynamic Programming, Wiley Series in Probability and Statistics, Wiley-Interscience [John Wiley & Sons], Hoboken, NJ, 2007.

- [29] J. A. Primbs and C. H. Sung, Stochastic receding horizon control of constrained linear systems with state and control multiplicative noise, IEEE Transactions on Automatic Control, 54 (2009), pp. 221–230.

- [30] M. M. Rao and R. J. Swift, Probability Theory with Applications, vol. 582 of Mathematics and Its Applications, Springer-Verlag, 2 ed., 2006.

- [31] U. Rieder, Measurable selection theorems for optimization problems, Manuscripta Mathematica, 24 (1978), pp. 115–131.

- [32] H. Schmidli, Stochastic Control in Insurance, Probability and its Applications, Springer-Verlag London Ltd., London, 2008.

- [33] D. H. van Hessem and O. H. Bosgra, Stochastic closed-loop model predictive control of continuous nonlinear chemical processes, Journal of Process Control, 16 (2006), pp. 225–241.

- [34] P. Whittle, Optimization Over Time. Vol. II, vol. 2 of Wiley Series in Probability and Mathematical Statistics: Applied Probability and Statistics, John Wiley & Sons Ltd., Chichester, 1983.