On the first passage time for Brownian motion subordinated by a Levy process

Abstract

This paper considers the class of Lévy processes that can be written as a Brownian motion time changed by an independent Lévy subordinator. Examples in this class include the variance gamma model, the normal inverse Gaussian model, and other processes popular in financial modeling. The question addressed is the precise relation between the standard first passage time and an alternative notion, which we call first passage of the second kind, as suggested by [7] and others. We are able to prove that standard first passage time is the almost sure limit of iterations of first passage of the second kind. Many different problems arising in financial mathematics are posed as first passage problems, and motivated by this fact, we are lead to consider the implications of the approximation scheme for fast numerical methods for computing first passage. We find that the generic form of the iteration can be competitive with other numerical techniques. In the particular case of the VG model, the scheme can be further refined to give very fast algorithms.

Key words: Brownian motion, first passage, time change, Lévy subordinators, stopping times, financial models.

1 Introduction

First passage problems are a classic aspect of stochastic processes that arise in many areas of application. In mathematical finance, for example, first passage problems lie at the heart of such issues as credit risk modelling, pricing barrier options, and the optimal exercise of american options. If is any process with initial value , the first passage time to a lower level is defined to be the stopping time

| (1) |

The distributional properties of are well studied when the underlying process is a diffusion, but when has jumps, for example, for Lévy processes, much less is known.

Explicit formulas for first passage are known only for certain special Lévy processes, specifically the Kou-Wang jump diffusion model [9] and its generalization to phase type processes [3]. In the setting of general Lévy processes, one analytical approach to first passage is the Wiener-Hopf method, described in [1]. This method can for example compute first passage problems for processes with one-sided jumps. A second general approach to first passage is to solve the Fokker-Planck equation for the probability density of conditioned on the set . For Lévy processes this amounts to solving a certain linear partial integral differential equation (PIDE) with Dirichlet boundary conditions. The PIDE approach to first passage in the general setting has apparently not been widely implemented: it seems that when faced with difficult first passage problems, practitioners often fall back on Monte Carlo methods.

Our purpose here is to present a new approach to first passage problems applicable whenever the underlying Lévy process can be realized as a Lévy subordinated Brownian motion (LSBM), that is, whenever can be constructed as where is a standard drifting Brownian motion and is a non-decreasing Lévy process independent of . The class of Lévy processes that are realizable as LSBMs is broad enough to include most of the Lévy processes that have so far been used in finance, such as the Kou-Wang model, the variance gamma (VG) model, and the normal inverse Gaussian (NIG) model.

The basis for our approach is that for processes that are realizable as time changes of Brownian motions, there is an alternative notion that is also relevant, namely, the first time the time change exceeds the first passage time of the Brownian motion. This notion, called first passage of the second kind in [7], shares some characteristics with the usual first passage time and can be applied in a similar way. The usefulness of this new concept is that it can be computed efficiently in many cases where the usual first passage time cannot.

In the present paper, we study first passage for LSBMs and show how the first passage of the second kind is the first of a sequence of stopping times that converges almost surely to the first passage time. Expressed differently, first passage can be viewed as a stochastic sum of first passage times of the second kind. This sequence leads to a convergent and computable expansion for the first passage probability distribution function in terms of a similar function that describes the first passage distribution of the second kind. The outline of the paper is as follows. In Section 2, we define the objects needed to understand first passage time, and prove the expansion formula for first passage. In Section 3, we demonstrate the usefulness of this expansion by proving several explicit two dimensional integral formulas for , the first passage distribution of the second kind. Section 4 provides two proofs of the convergence of the expansion. The first proof is a proof of convergence in distribution, the second is in the pathwise (almost sure) sense. Section 5 focusses on the special case of the variance gamma (VG) model. In this important example, the formula for is reduced to a one-dimensional integral (involving the exponential integral function),. In Section 6, the expansion of the function is studied numerically, and found to be numerically stable and efficient.

2 First Passage for LSBMs

Let be a general Lévy process with initial value and characteristics with respect to a truncation function (see [2] or [8]). This means is an infinitely divisible process with identical independent increments and cádlág paths almost surely. are real numbers and is a sigma finite measure on that integrates the function . By the Lévy-Khintchine formula, the log-characteristic function of is

| (2) |

In what follows we will find it convenient to focus on the Laplace exponent of :

For simplicity of exposition, we specialize slightly by assuming that is continuous with respect to Lebesgue measure , and integrates , allowing us to take . In this setting, the Markov generator of the process applied to any sufficiently smooth function is

| (3) |

Definition 1.

For any , the random variable is called the first passage time for level . When , we drop the subscript and is called simply the first passage time of .

Remarks 2.

-

1.

Since distributions of the increments of are invariant under time and state space shifts, we can reduce computations of to computations of .

-

2.

A general Lévy process is a mixture of a continuous Brownian motion with drift and a pure jump process, and is the minimum of a predictable stopping time (coming from the diffusive part) and a totally inaccessible stopping time (coming from the down jumps). Only if is predictable. If or if has an infinite activity of down jumps (i.e. if ), then is totally inaccessible.

-

3.

When , we say that jumps across , and define the overshoot to be .

The central object of study in this paper is the joint distribution of and the overshoot , in particular the joint probability density function

| (4) |

The marginal density of is .

In the introduction, we noted that general results on first passage for Lévy processes, in particular results on the functions , are difficult to come by. For this reason, we now focus on the special class of Lévy processes that can be expressed as a drifting Brownian motion subjected to a time change by an independent Lévy subordinator. Such Lévy subordinated Brownian motions (LSBM) have been studied in a general review by [5] and more specifically in [7]. The general LSBM is constructed as follows:

-

1.

For an initial value and drift , let be a drifting BM;

-

2.

For a Lévy characteristic triple with and , let the time change process be the associated nondecreasing Lévy process (a subordinator), taken to be independent of ;

-

3.

The time changed process is defined to be a LSBM.

So constructed, it is known that is itself a Lévy process: [5] provide a characterization of which Lévy processes are LSBMs. It was observed in [7] that for any LSBM , one can define an alternative notion of first passage time, which we denote here by .

Definition 3.

For any LSBM we define the first passage time of to be . Note when . The first passage time of the second kind of is defined to

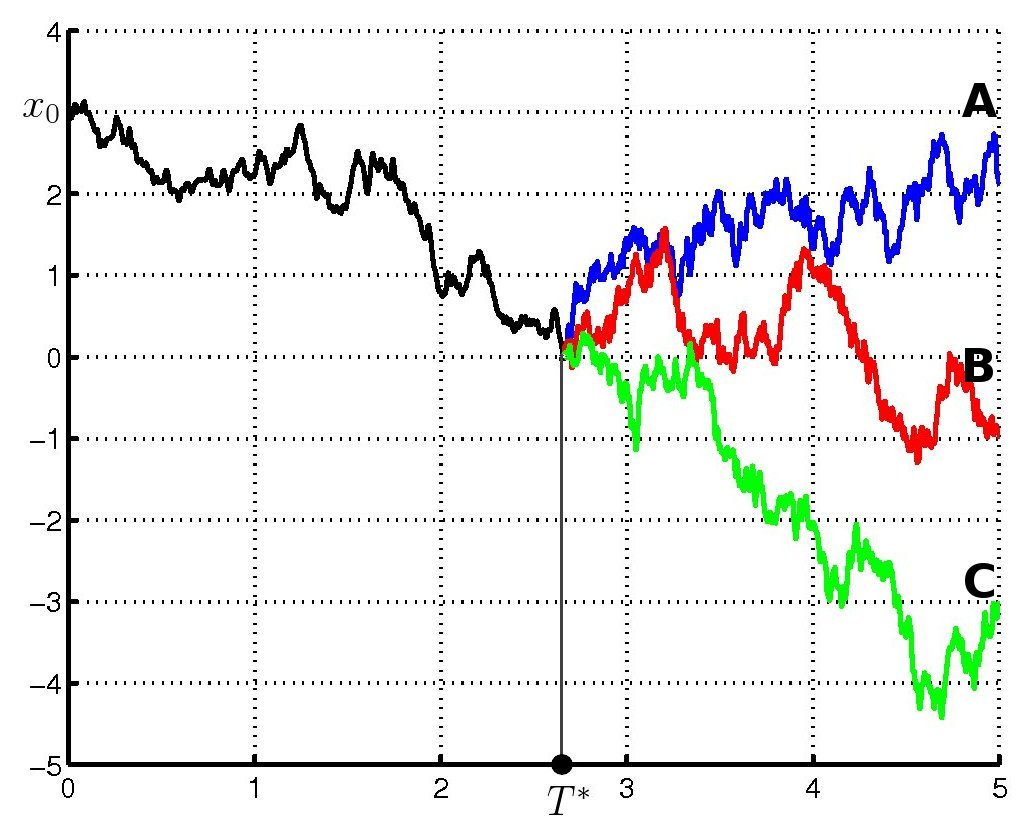

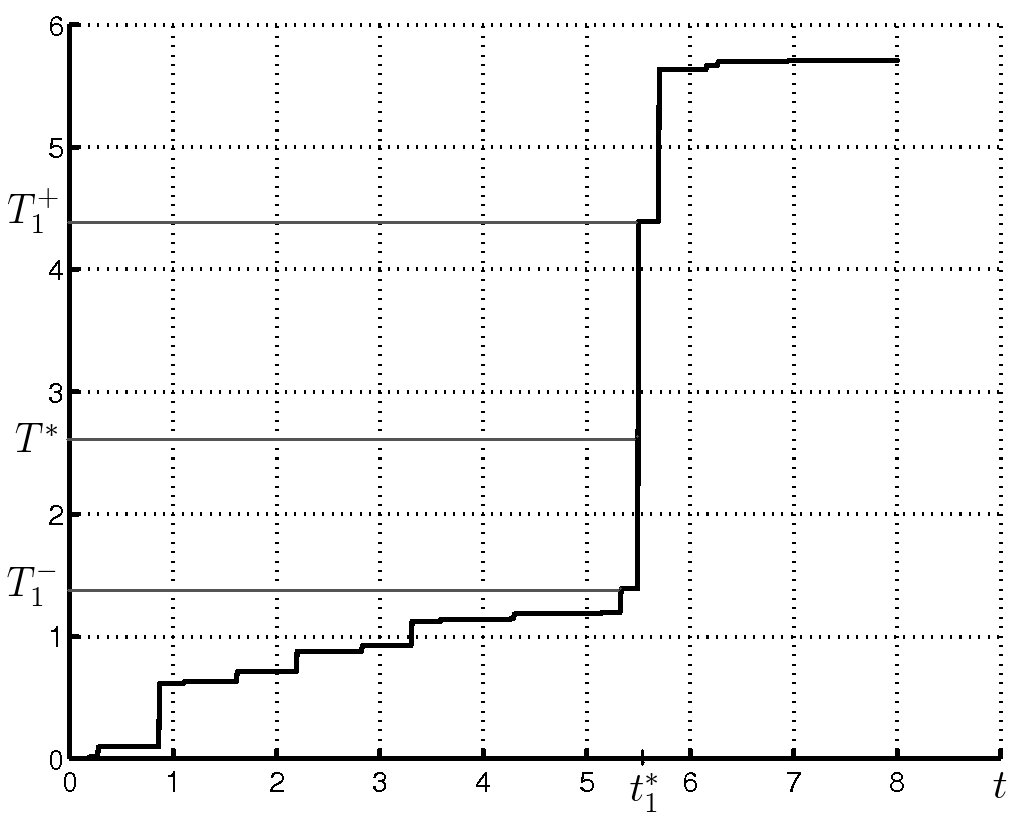

This definition of , and its relation to , is illustrated in Figure 1.

We now show that is the first of a sequence of approximations to the stopping time . The construction of is pathwise: We introduce the second argument which denotes a sample path, that is, a pair where is a continuous drifting Brownian path and is a cádlág sample time change path . Thus . The natural “big filtration” for time-changed Brownian motion has . For any there is a natural “time translation” operation on paths where .

The construction of for a given sample path is as follows. Inductively, for , we define the time of the -th excursion overjump

| (5) |

where denotes a time shifted sample path. Note that if and only if or . At any excursion overjump event , the time interval which covers the event has left and right endpoints and . The joint distribution of can be written

| (6) |

The definition of this sequence of stopping times is summarized by the pathwise equation

| (7) |

where . The identical increments property of the LSBM implies the joint probability densities satisfy the recursive relation

| (8) |

Similarly, the PDF of the first passage time satisfies the relation

| (9) |

Examples of LSBMs: We note here three classes of Lévy processes that can be written as LSBMs and have been used extensively in financial modeling.

-

1.

The exponential model with parameters arises by taking to be the increasing process with drift and jump measure on . The Laplace exponent of is

The resulting time-changed process has triple with

where . This forms a four dimensional subclass of the six-dimensional family of exponential jump diffusions studied by [9].

-

2.

The variance gamma (VG) model [10] arises by taking to be a gamma process with drift defined by the characteristic triple with (usually is taken to be ) and jump measure on . The Laplace exponent of is

The resulting time-changed process has triple with

-

3.

The normal inverse Gaussian model (NIG) with parameters [4] arises when is the first passage time for a second independent Brownian motion with drift to exceed the level . Then

and the resulting time-changed process has Laplace exponent

3 Computing First Passage of the Second Kind

We have just seen that first passage for LSBMs admits an expansion as a sum of first passage times of the second kind. In this section, we show that this expansion can be useful, by proving several equivalent integral formulas for computing the structure function for general LSBMs. While the equivalence of these formulas can be demonstrated analytically, their numerical implementations will perform differently: which formula will be superior in practice is not a priori clear, but will likely depend on the range of parameters involved. For a complete picture, we provide independent proofs of the two given formulas.

Theorem 1.

Let be the Laplace exponent of , and let have drift . Then

| (11) | |||||

Here denotes that the principal value contour is taken.

Remark 4.

The equivalence of these two formulas can be demonstrated directly by performing a change of variables , followed by a deformation of the contours. Justification of the contour deformation (from the branch of a left-right symmetric hyperbola in the upper half -plane to the real axis) depends on the decay of the integrand, and the computation of certain residues.

3.1 First proof of Theorem 1

For a fixed level , the first passage time and the overshoot of the process above the level are defined to be and . The Pecherskii-Rogozin identity [11] applied to the nondecreasing process says that

Inversion of the Laplace transform in the above equation then leads to

| (12) |

The first passage time of the BM with drift is defined as . Next, we need to find the joint Laplace transform of and the overshoot . Since is independent of we find that

where in the last equality we have used the following well-known result for the characteristic function of the first passage time of BM with drift:

Next we use the Fourier transform of the PDF of the BM with drift in time variable to obtain

| (14) |

Thus, using the fact that is independent of and we obtain

Now, the statement of the Theorem follows after one additional Fourier inversion:

where we have also used the following Fourier integral:

3.2 Second proof of Theorem 1

The strategy of the proof is to compute

| (15) |

and then take the limit of as . The key idea is to note that where are copies of , independent of the filtration . We can then perform the above expectation via an intermediate conditioning on :

| (17) | |||||

To evaluate the expectations that arise, we will need the second and third of the following results that were stated and proved in [7]:

Lemma 2.

-

1.

For any

(18) -

2.

For any and

(19) -

3.

For any in the upper half plane,

(20)

First, using (19), we find

| (22) | |||||

When we paste this expression into the final expectation over we can use Fubini to interchange the expection and integral providing we choose . Then we find

| (23) |

We can now use (20) from Lemma 2 obtain

| (24) |

Noting that and taking now gives

Here the arbitrary parameter can be seen to ensure the correct prescription for dealing with the pole at .

Finally, the complex integration in (3.2) can be expressed in the following manifestly real form:

| (26) | |||||

involving a principle value integral plus explicit half residue terms for the poles .

4 The iteration scheme and its convergence

The next theorem shows that (8) can be used to compute . We define a suitable norm for functions :

| (27) |

Theorem 3.

The sequence converges exponentially in the norm.

Proof.

The proof is based on the probabilistic interpretation of the constant : by definition is the joint density of and , thus we obtain:

Next, using the fact that ( is the first passage time of and is a continuous process) and the strong Markov property of the Brownian motion we find that

where the Brownian motion is independent of and is the overshoot of the time change above .

Thus we need to prove that

| (28) |

where , and the Brownian motion is independent of and .

First we will consider the case when . In this case we obtain

where we have used the fact that is independent of the overshoot and that for any and any . Thus in the case when the drift is negative we obtain an estimate .

The case when the drift is positive is more complicated. We can not use the same techniques as before, since the bound is no longer true: in fact monotonically increases to as .

First we will consider the case when is bounded away from : . Then has a positive probability of escaping to and never crossing the barrier at 0, thus

Now we need to consider the case when . The proof in this case is based on the following sequence of inequalities:

where is any positive number and the last inequality is true since is a decreasing function of .

Since , we also have with probability 1. Since is the overshoot of , and as , we see that the distribution of the overshoot converges either to the distribution of the jumps of if the time change process is a compound Poisson process or to the Dirac delta distribution at if has infinite activity of jumps. Therefore in the case when is a compound Poisson process with the jump measure we choose such that , and if has infinite activity of jumps we can take any . Then we obtain , where in the case of compound Poisson process, and in the case of the process with infinite activity of jumps. Using (4) we find that as

To summarize, we have proved that the function

satisfies the following properties:

-

•

for any there exists such that for all

-

•

there exists such that .

Therefore we conclude that there exists

, such that for

all , thus . This ends the proof in the second case .

For a complementary point of view, the next result shows that the sequence converges pathwise.

Theorem 4.

For any TCBM with Lévy subordinator and Brownian motion with drift the sequence of stopping times converges a.s to .

Proof: 111The authors would like to thank Professor Martin Barlow for providing ths proof. If , then certainly , so we suppose . In this case, if for some the sequence converges, and thus the only interesting case to analyze is if for all . Then we have . Correspondingly, we have an infinite sequence of excursion overjump intervals which do not overlap: let their endpoints be . The following observations lead to the conclusion:

-

1.

by monotonicity and boundness of the sequences and , exists;

-

2.

by the continuity of Brownian motion;

-

3.

exists, and ;

-

4.

Jump times are totally inaccessible, so there is no time jump at time almost surely, hence ;

-

5.

Therefore and so : hence .

5 The Variance Gamma model

The Variance Gamma (VG) process described in Section 2 is the LSBM where the time change process is the Lévy process with jump measure on and the Laplace exponent . In this section we take the parameter . This model has been widely used for option pricing where it has been found to provide a better fit to market data than the Black-Scholes model, while preserving a degree of analytical tractability. The main result in this section reduces the 2D integral representation (11) for to a 1D integral and leads to greatly simplified numerical computations.

Theorem 5.

Proof.

Consider the function which represents the outer integral in (11)

First we perform the change of variables and obtain

| (31) |

where the contour obtained from under map is transformed into contour (this is justified since the integrand is an analytic function in this region for any ). To finish the proof we separate the logarithms

use the partial fractions decomposition

and we obtain the six integrals, which can be computed by shifting the contours of integration and using the following Fourier transform formulas (see Gradshteyn-Ryjik…)

Remark: Using the change of variables and simplifying the expression we can obtain a simpler formula for :

Applying the Plancherel formula to the above expression gives us the following representation for :

where

The above expression is useful for computations when is small. In particular, when we find

| (33) |

6 Numerical implementation for VG model

The algorithm for computing the functions and can be summarized as follows:

-

1.

Choose the discretization step sizes , and discretization intervals , . The grid points are , and , .

- 2.

- 3.

Theorem 3 implies that Step 3 in the above algorithm has to be repeated only a few times: In practice we found that 3-4 iterations is usually enough. An important empirical fact is that the above algorithm works quite well with just a few discretization points in the -variable. We found that if one uses a non-linear grid (which places more points near ) then the above algorithm produces reasonable results with values of as small as 10 or 20.

We compared our algorithm for the PDF to a finite-difference method that was implemented as follows. First we approximated the first passage time by its discrete counterpart:

where , is the discretization of the interval . The probabilities satisfy the iteration:

| (34) |

with and can be computed numerically with the following steps:

-

1.

discretize the space variables , , ;

-

2.

compute the array of transitional probabilities , and normalize so that ;

-

3.

use the convolution (based on FFT) to iterate equation (34) times;

-

4.

compute the approximation of the first passage time density .

The big advantage of this method is that it is explicit and unconditionally stable: we can choose the number of discretization points in -space and -space independently. This is not true in general explicit finite difference methods, where one would solve the Fokker-Plank equation by discretizing the Markov generator and derivative in time, since and have to lie in a certain subset in order for the methods to be stable.

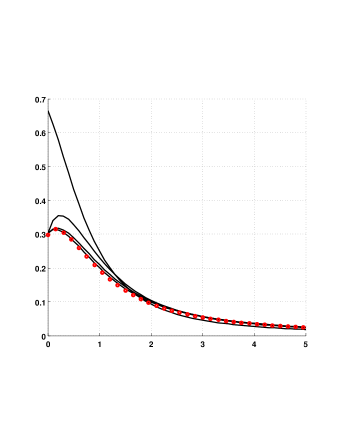

Figure 2 summarizes the numerical results for the PDF over the time interval for the VG model with the following two sets of parameters:

The number of grid points used was and . The red circles correspond to the solution obtained by a high resolution finite difference PIDE method as described above (with and ), and the black lines show successive iterations converging to . As we see, 3 iterations of equation (9) provide a visually acceptable accuracy in a running time of less than 0.1 second (on a 2.5Ghz laptop).

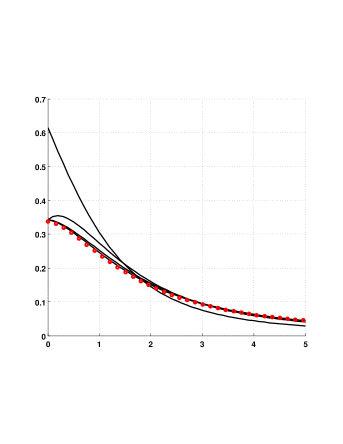

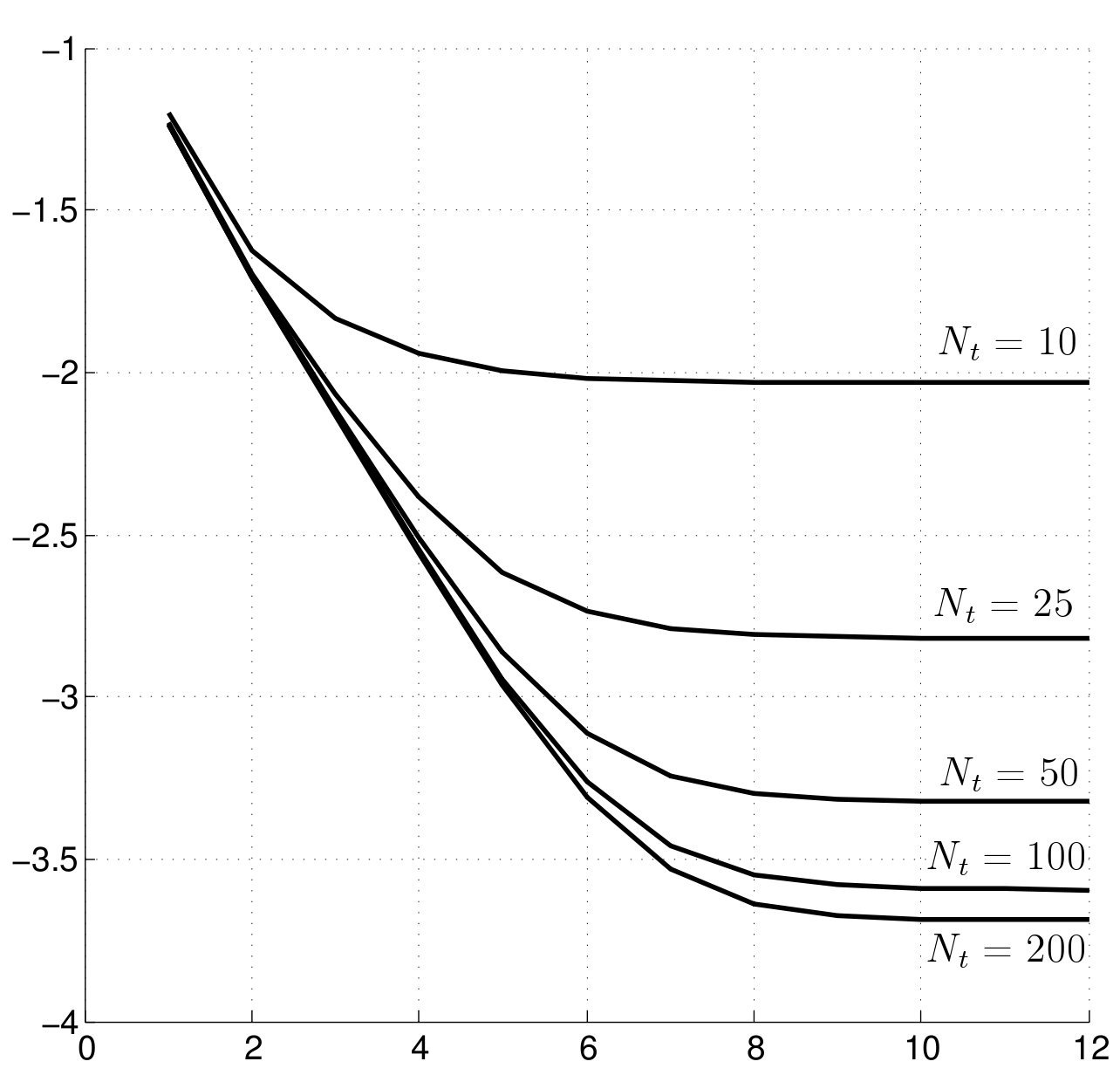

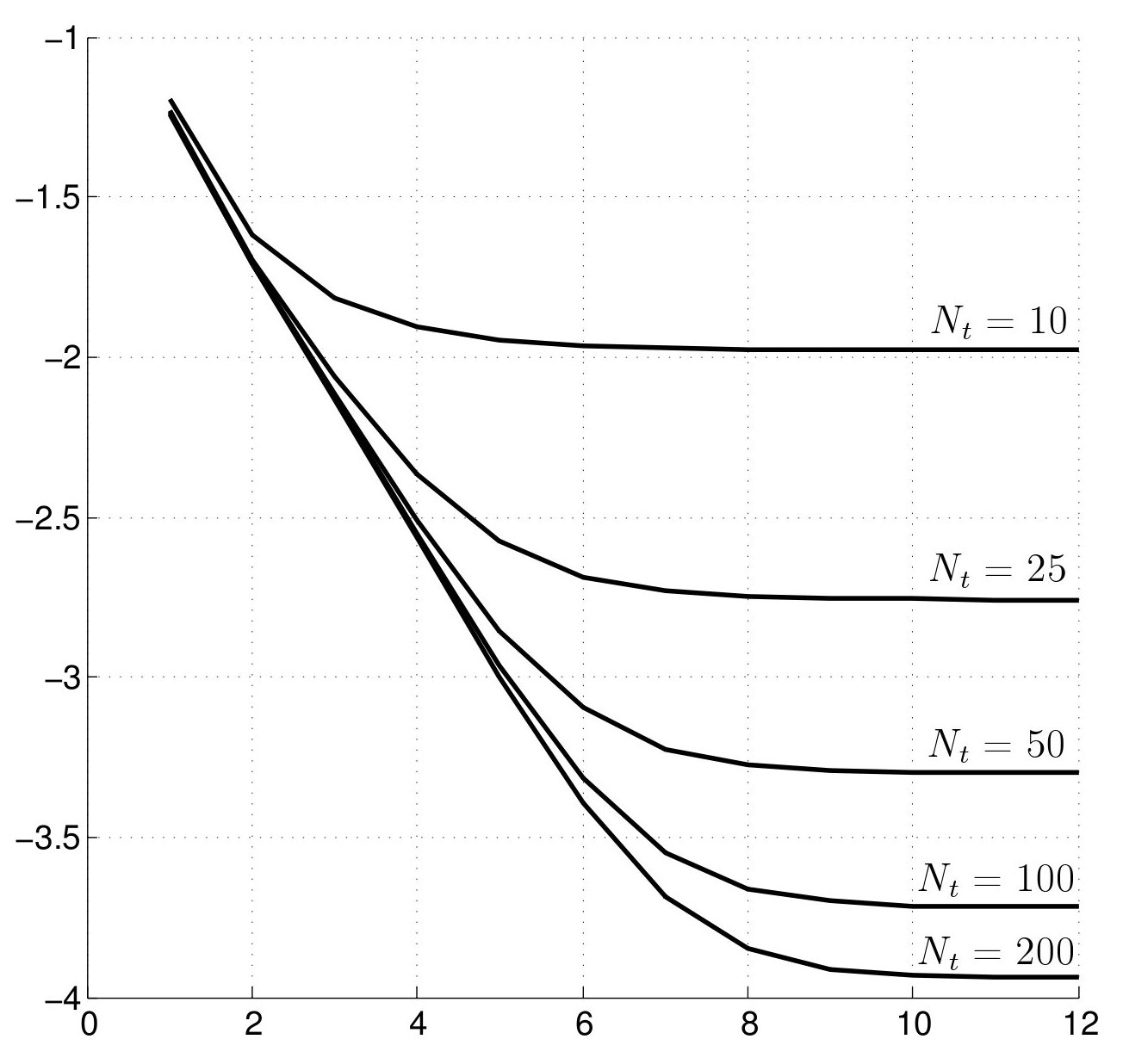

Figure 3 illustrates the convergence of our method and Table 1 shows the computation times (on the same 2.5Ghz laptop). We used Set II of parameters for the VG process, and the PIDE method with and to compute the “exact” solution . Figure 3 shows the of the error

on the vertical axis and the number of iterations on the horizontal axis; different curves correspond to different number of discretization points in -space. The number of discretization points in -space is fixed at for the left picture and for the right picture. We see that initially the error decreases exponentially and then flattens out. The flattening indicates that our method converges to the wrong target (which is to be expected since there is always a discretization error coming from and being finite). However, increasing and brings us closer to the “target”. In the table 1 we show precomputing time needed to compute the 3D array and the time needed to perform each iteration (9).

| precomputing time | 0.0313 | 0.0259 | 0.0324 | 0.0461 | 0.0687 | |

|---|---|---|---|---|---|---|

| each iteration | 0.0006 | 0.0008 | 0.0011 | 0.0021 | 0.0046 | |

| precomputing time | 0.0645 | 0.0612 | 0.0745 | 0.0868 | 0.1298 | |

| each iteration | 0.0037 | 0.0045 | 0.0066 | 0.0120 | 0.0269 |

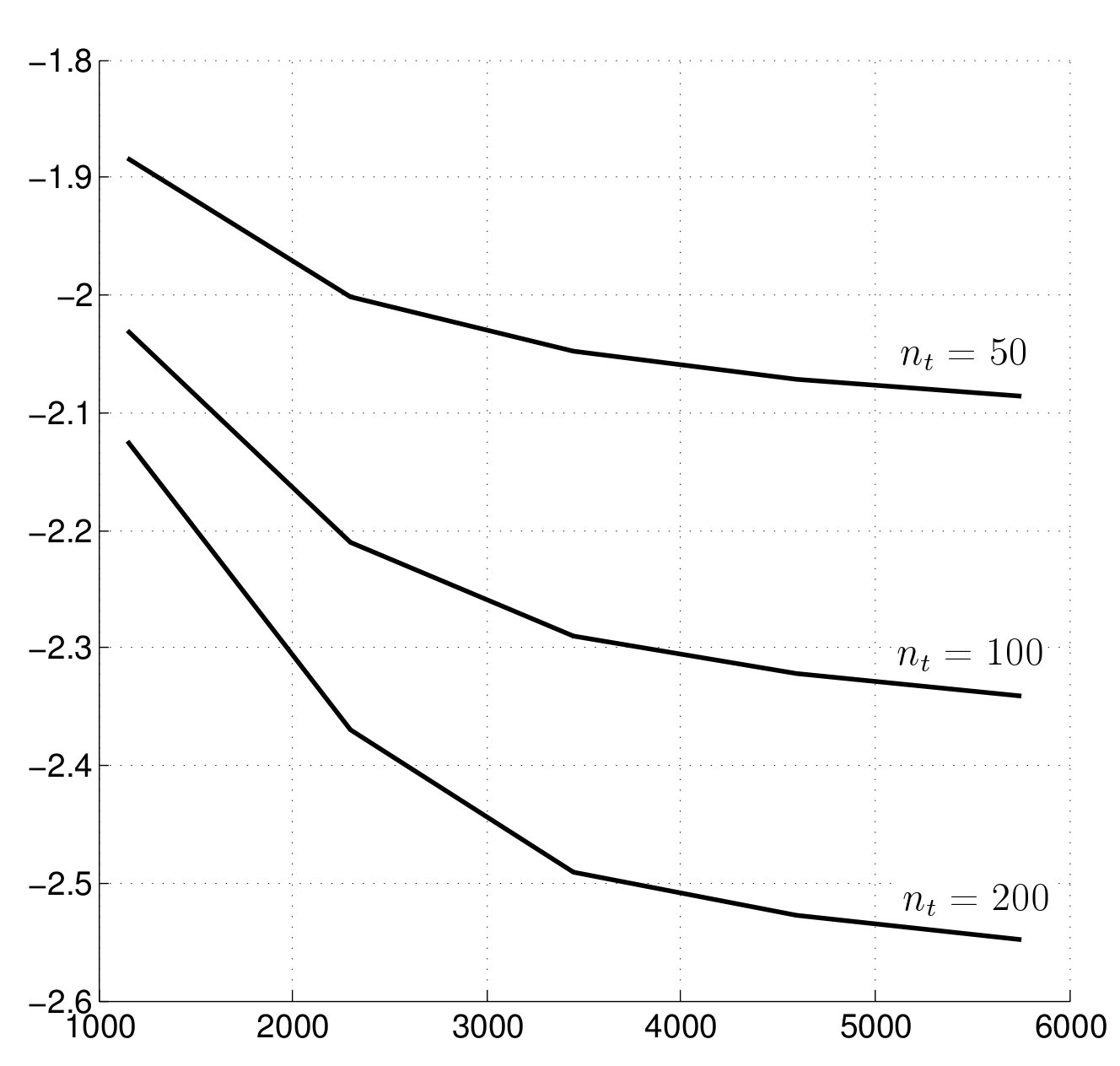

To put these results into perspective, on Figure 4 and Table 2 we present similar results for finite difference method. On Figure 4 we show the same logarithm of the error on the vertical axis, and the number of discretization points on the horizontal axis. Different curves correspond to . The running time presented in Table 2 includes only the time needed to perform convolutions (34) using the FFT. As we see, the finite difference method is substantially slower than our method.

| 0.0756 | 0.2935 | 0.9582 | 1.8757 | 2.9967 | |

| 0.1456 | 0.5821 | 1.9397 | 3.7409 | 6.0026 | |

| 0.2870 | 1.1478 | 3.8833 | 7.4768 | 11.9935 |

7 Conclusions

First passage times are an important modeling tool in finance and other areas of applied mathematics. The main result of this paper is the theoretical connection between two distinct notions of first passage time that arise for Lévy subordinated Brownian motions. This relation leads to a new way to compute true first passage for these processes that is apparently less expensive than finite difference methods for a given level of accuracy. Our paper opens up many avenues for further theoretical and numerical work. For example, the methods we describe are certainly applicable for a much broader class of time changed Brownian motions and time changed diffusions. Finally, it will be worthwhile to explore the use of the first passage of the second kind is a modeling alternative to the usual first passage time.

References

- [1] L. Alili and A. E. Kyprianou. Some remarks on first passage of Lévy processes. Ann. Appl. Probab., 15:2062 2080, 2005.

- [2] David Applebaum. Lévy processes and stochastic calculus, volume 93 of Cambridge Studies in Advanced Mathematics. Cambridge University Press, Cambridge, 2004.

- [3] S. Asmussen, F. Avram, and M.R. Pistorius. Russian and american put options under exponential phase-type l vy models. Stochastic Processes and their Applications, 109:79–111, 2004.

- [4] O. E. Barndorff-Nielsen. Normal inverse Gaussian distribution and stochastic volatility modelling. Scandinavian Journal of Statistics, 24:1–13, 1997.

- [5] A. S. Cherny and A. N. Shiryaev. Change of time and measures for Lévy processes. Lectures for the Summer School “From Lévy Processes to Semimartingales: Recent Theoretical Developments and Applications to Finance”, Aarhus 2002, 2002.

- [6] I. S. Gradshteyn and I. M Ryzhik. Tables of integrals series and products, 6th edition. Academic Press, 2000.

-

[7]

T. R. Hurd.

Credit risk modelling using time-changed Brownian motion.

Working paper

http://www.math.mcmaster.ca/tom/HurdTCBMRevised.pdf, 2007. - [8] J. Jacod and A. N. Shiryaev. Limit theorems for stochastic processes. Springer-Verlag, Berlin, 1987.

- [9] S. G. Kou and H. Wang. First passage times of a jump diffusion process. Adv. in Appl. Probab., 35(2):504–531, 2003.

- [10] D. Madan and E. Seneta. The VG model for share market returns. Journal of Business, 63:511–524, 1990.

- [11] E. A. Percheskii and B. A. Rogozin. On the joint distribution of random variables associated with fluctuations of a process with independent increments. Theory Probab. Appl., 14:410 423, 1969.