Online Ad Slotting With Cancellations

Abstract

Many advertisers use Internet systems to buy advertisements on publishers’ webpages or on traditional media such as radio, TV and newsprint. They seek a simple, online mechanism to reserve ad slots in advance. On the other hand, media publishers represent a vast and varying inventory, and they too seek automatic, online mechanisms for pricing and allocating such reservations.

In this paper, we present and study a simple model for auctioning such ad slots in advance. Bidders arrive sequentially and report which slots they are interested in. The seller must decide immediately whether or not to grant a reservation. Our model allows a seller to accept reservations, but possibly cancel the allocations later and pay the bidder a cancellation compensation (bump payment).

Our main result is an online mechanism to derive prices and bump payments that is efficient to implement. This mechanism has many desirable properties. It is individually rational; winners have an incentive to be honest and bidding one’s true value dominates any lower bid. Our mechanism’s efficiency is within a constant fraction of the a posteriori optimally efficient solution. Its revenue is within a constant fraction of the a posteriori VCG revenue. Our results make no assumptions about the order of arrival of bids or the value distribution of bidders. All our results still hold if the items for sale are elements of a matroid, a more general setting than slot allocation.

1 Introduction

Many advertisers now use Internet advertising systems. These take the form of advertisement (ad, henceforth) placements either in response to users’ web search queries, or at predetermined slots on publishers’ web pages. In addition, increasingly, advertisers use Internet systems that sell ad slots on behalf of offline publishers on TV, radio or newsprint. In sponsored search, and in some other cases, ad slots are typically sold via real time auctions, i.e., when a user poses a query or visits a web page, an auction is used to determine which ads will show and where they will be placed. On the other hand, traditionally, advertisers seek ad slots in advance, i.e. to reserve their slots. Product releases (such as movies, electronic gadgets, etc) and ad campaigns (e.g., creating and testing ads, budgets) are planned ahead of time and need to coordinate with future events that target suitable demographics. The advertisers then do not want to risk the vagrancies of real-time auctions and lose ad slots at critical events; they typically like a reasonable guarantee of ad slots at a specific time in the future within their budget constraints today.

Our motivation arises from systems that enable such advanced ad slotting. In particular, our focus is on automatic systems that have to manage ad slots in many different publishers’ properties. These properties differ wildly in their traffic, targeting, price and effectiveness; consider placement in the front page of nytimes.com versus placement in an individual’s blog versus a radio slot in a local country music radio station. Also, the inventory levels are massive. Slots and impressions in web publishers’ properties as well ad slots in TV, radio, newsprint and other traditional media are in 100’s of millions and more. Not all publishers can estimate their inventory accurately: traffic to websites responds to time-dependent events, and sometimes webpages are generated dynamically so that even the availability of a slot in the future is not known a priori. Most web publishers are not able to estimate accurately a price for an ad slot, or provide sales agents to negotiate terms and would like automatic methods to price ad slots. Thus, what is desirable is a simple, automatic, online111We use the word online as in online algorithm—i.e., the input arrives over time, and the algorithm makes sequential decisions —we do not mean “on the Internet.” market-based mechanism to enable advanced ad slotting over such varied, massive inventory.

Inspired by these considerations, we study the problem of mechanism design for advanced ad slotting. The problem is quite general with many facets. Our contribution is to propose a simple model, to design a suitable mechanism and to analyze its properties. In more detail, our contributions are as follows.

(i) We propose the following simple high-level model for advanced ad slotting auctions. An auction starts at time ; the seller has a set of slots for sale that will be published at time . Bidder arrives at some time , reports which slots he is interested in, places a bid and requests an immediate response. Bidder is either accepted or rejected; if accepted, he may be removed (bumped) later, but in that case, he is awarded a bump payment. We assume that if bumped, a bidder incurs a loss of an fraction of its value. At time , each accepted bidder that has not been bumped is published in one of the slots he was interested in, and pays a price that is at most his bid.

This model lets the publisher accept a reservation at time for a slot available at a later time , and lets the advertiser get a reasonable guarantee. However, crucially, it lets the publisher cancel the reservation at a later time. Cancellation is necessary for publishers to take advantage of a spike in demand and rising prices for an item and not be forced to sell the slot below the market because of an a priori contract. In addition, in a pragmatic sense, cancellation is crucial: for example, a website might overestimate its inventory for a later date and accept ads, but as time progresses, its estimates may become smaller, and the publisher will not be able to honor all the accepted ads from the past. Finally, cancellations are very much part of the business with advance bookings, both within advertising and beyond. At the same time, it comes at a cost, which is the bump payment. This is reasonable since it compensates the advertiser for the uncertainty, and lets advertisers recoup part of their costs involved in preparing a campaign for time based on their reservation at time . We present our model formally in Section 3.

(ii) We present an efficiently implementable mechanism M for determining who is accepted, who is bumped and also the prices and bump payments. The parameter represents how much higher a new bid has to be in order to bump an older bid. A bumped bidder will be paid an fraction of their bid, making up for their utility loss due to being bumped.

(iii) We show a number of important strategic as well as efficiency- and revenue-related properties of M:

-

•

M is individually rational and winners have an incentive to bid truthfully while losers should bid at least their true value.

-

•

With respect to the bids received, the efficiency (value of assignment) of M is at least a constant factor (depending on and ) of the offline optimum. Under mild player rationality assumptions, we show that our mechanism is competitive with respect to the optimum offline efficiency on bidders’ true values.

-

•

We also consider the notion of effective efficiency which interprets social welfare as the sum of the winners’ bids minus bumped (if any) bidders’ losses. We show that for suitable , our mechanism’s effective efficiency matches a numerically obtained upper bound on the effective efficiency of any deterministic algorithm. To our knowledge, costly cancellations have not been previously studied in online bipartite matching problems.

-

•

The revenue of M is at least a constant factor (dependent on and ) of that of the Vickrey-Clarke-Groves (VCG) mechanism on all received bids.

-

•

We also study speculators, that is, ones who have no interest in the items for sale but who participate in order to earn the bump payment. We show several game theoretic properties about the behavior of the speculators, including bounding their overall profit.

To the best of our knowledge our results are the first about mechanisms with strong game-theoretic properties for advanced placement of ads (more generally, indivisible goods) with a cancellation feature. We make no assumptions on the arrival order of the bidders or on their values. Prior work has studied advanced sale of goods without cancellations, but only under a probabilistic distribution of bidders’ values [6, 8]. Under a worst case model like ours, no nontrivial results are possible without making additional assumptions; in our case, we overcome these impossibilities by allowing cancellations. In secretary problems [1], bids may be arbitrary but their order is assumed to be uniformly random (cannot be specified by an adversary).

There are specific examples of systems that implement advanced booking with cancellations. For example, this is common in the airline industry, where tickets may be booked ahead of time, and customers may be bumped later for a payment. In the airline case, the inventory is mostly fixed, sophisticated models are used to calculate prices over time, and often negotiations are involved in establishing the payment for bumping, just prior to time . In some cases, the bump payments may even be larger than the original bid (price) of the customer. Likewise, in offline media such as TV or Radio, humans are involved are in negotiating advanced prices, and often if the publisher does not respect the reservation due to inventory crunch, a payment is a posteriori arranged including possibly a better ad slot in the future. These methods are not immediately applicable to the auction-driven automatic settings like ours.

From a technical point of view, one can view our model as an online weighted bipartite matching problem (or more generally, an online maximum weighted independent set problem in a matroid). On one side we have slots known ahead of time. The other side comprises advertisers whose bids (weighted nodes) arrive online. Our goal is to find a “good” weighted matching in the eventual graph. Each time an advertiser appears we need to decide if we should retain it or discard it; retaining it may lead to discarding a previously retained bidder. Our mechanism builds on such an online matching algorithm [9] to determine a suitable bump payment and prices. It is, curiously, able to make use of such an online algorithm previously proposed in the semi-streaming model in the theoretical computer science literature.

All our results extend to a setting where the items for sale are elements of a matroid, a more general setting than slot allocation. A bidder bids on exactly one element of the matroid, which is known ahead of time and may vary across bidders. A set of bidders is then feasible if the set containing each bidder’s element forms an independent set of the matroid. In the bipartite matching setting, the seller’s matroid contains one element for each subset of slots and a set of bidders (elements) is independent if the bidders can be matched to slots such that each one receives an element from its subset. We prefer the matching language for clarity of exposition.

We have initiated the study of mechanisms for advanced reservations with cancellations. A number of technical problems remain open, both within our model, as well as in its extensions, which we describe later for future study.

2 Related Work

There is considerable work on auctions when bidders are present throughout a period of time. Of more direct relevance are the following classes of problems.

Babaioff et al. [1] address the matroid secretary problem: finding a competitive assignment when weighted elements of a matroid arrive online and no cancellations are allowed. As is common in secretary problems, while not making any assumption on bidder valuations, they assume that all orders of arrivals are equally likely. They present a -competitive algorithm for general matroids where is the rank of the matroid (the size of the largest independent sets) and a -competitive algorithm for our setting without cancellations (transversal matroids) but where each bidder can only be interested in at most items. Both these algorithms observe half of the input and then set a threshold price: per item in the transversal case and uniform in the general case. The -competitive algorithm ensures truthful bidding even when the items desired by an agent are private information. Dimitrov and Plaxton [4] extend the -algorithm and provide an algorithm with a constant competitive ratio for any transversal matroid.

Bikhchandani et al. [2] present an ascending auction for selling elements of a matroid that ends with an optimal allocation (i.e. the auction is efficient). Truthful bidding is an equilibrium of the auction. They assume however that bidders are present throughout the auction.

Cary et al. [3] show that a random sampling profit extraction mechanism approximates a VCG-based target profit in a procurement setting on a matroid.

Gallien and Gupta [6] analyze players’ strategies regarding buyout prices in online auctions. In their model, bidders’ valuations are drawn from a known distribution and their utilities are time-discounted; furthermore there are no cancellations and arrivals are assumed to follow a Poisson process. They exhibit symmetric Bayes-Nash equilibria in which buyers follow certain threshold strategies. Assuming that buyers follow the corresponding equilibrium strategies, the seller can then optimize revenue by tuning the price function.

Lavi and Nisan [8] consider online auctions for identical goods. In their model, bidders’ values are arbitrary from the interval and no cancellations are possible. They present a simple online posted-price auction based on exponential scaling. This auction is optimal among online auctions and achieves a approximation with respect to both efficiency and the VCG revenue.

Independently form us, Feige et al. [5] study an offline weighted bipartite matching problem where the seller can partially satisfy a bidder’s request at the cost of paying a proportional penalty. Accepting a bid but not providing any items results in a utility loss proportional to the bid, similar to our definition of effective efficiency in Section 5.1. They show that it is NP-hard to approximate the optimal solution within any constant factor. They propose an adaptive greedy algorithm assigning one bidder at a time (but that inspects all unassigned bidders in deciding which bidder to allocate) and that may reassign bidders. They provide a lower bound on this algorithm’s efficiency with respect to the optimal assignment.

3 Model and Mechanism

We first define our model and present our mechanism which we will study in later sections.

3.1 Model Basics

There is a seller who has a finite set of slots (items), and starts sale at time and ends sale at time .

Each bidder is interested in exactly one slot out of a set called ’s choice set. We denote by bidder ’s value for any slot in and we assume that is private information to . Each bidder places a bid (that may be different than ) as soon as it arrives, at time . As a consequence of bidding, ’s choice set becomes known to the seller. When bids, he may be accepted (i.e. promised an item from ), else rejected. If promised an allocation, he may get bumped later, losing the reservation. Any accepted bidder who is not bumped before time is allocated. We model bidder ’s utility as

| (1) |

-

•

equals if is rejected, if is accepted and granted from and if is accepted but bumped.

-

•

is ’s transfer to the seller (price). It is if is rejected, and some non-negative amount if is accepted and allocated. may be negative (e.g. the bump payment the seller makes in M).

That is, a bidder is unaffected if rejected right away, has a value of for being allocated, and incurs a loss amounting to an fraction of its value if bumped. The utility is quasilinear in money.

Note that from an algorithmic perspective, our problem is online maximum weighted bipartite matching with costly cancellations. There is a bipartite graph with items (respectively bidders) as “right”-(respectively “left”-)hand side vertices. Left-hand side vertices are fixed. One by one, a right-hand side vertex is revealed together with its weight and its edges (i.e. the set ). A decision whether to accept or not must be taken immediately. The goal is to find a matching of weight as high as possible, where cancellations are allowed, but canceling bidder of weight results in a penalty of .

However, in our setting bidders are self-interested and may alter the input to the algorithm (their bids) if it is in their interest to do so. Therefore we aim for a mechanism that is competitive while bounding the bidders’ manipulations. Note that if , then we can tentatively accept any bidder and only decide at time which bidders are truly accepted while rejecting the remainder, thus reducing the problem to finding a bipartite matching of maximum weight, a standard offline optimization. By charging each bidder its VCG (see Section 6) price, it becomes a dominant strategy for each bidder to be truthful (i.e. bid its true value).

3.2 Our M Mechanism

We present our advance-booking online mechanism M (allocation algorithm and payments). The allocation algorithm follows the Find-Weighted-Matching algorithm in [9]222Unlike [9], a bidder ’s value is the same for any slot (vertices as opposed to edges are weighted). Our mechanism may then change the slot is currently assigned to at various stages in the algorithm.. Apart from , which is specified by the model, the algorithm uses an improvement factor such that .

Denote the number of bidders by ; our mechanism is independent of . By relabeling bidders, assume that they bid in order ; time is indexed likewise.

Definition 1

We say that a set of bidders can be matched if for each there exists an item such that . We say that is a perfect matching if it can be matched and no item is left unmatched (’s cardinality must equal the number of items).

M’s pseudocode is listed in Algorithm 1. At a high level, M maintains a set of accepted bidders that form a perfect matching. For any new arriving bidder bidding , the algorithm looks if there exists some bidder in the accepted set with such that can be swapped in the matching if is swapped out. If so, accept and cancel the reservation of (bump) , the lowest weight such . Bidder is paid the bump payment . (Note that makes no payment at all and in fact gets money for free from the seller if bumped.) An accepted bidder who is not bumped by time is necessarily allocated a slot from his choice set and pays the seller an amount we define later (Eq.(2)).

At time 0, is an arbitrary matching; we introduce dummy bidders (each bidding 0) whose choice set is the whole set of items, arriving before all actual bidders. This will not affect our arguments below.333 When bidder arrives, assume where only contains dummy bidders and there exists a matching of which matches to some item . By reassigning dummy bidders, we can assume that actual bidders are matched according to . Then bidder can bump at least the dummy bidder that is matched to in .At time , we call currently accepted bidders alive, and denote the set of alive bidders as . Let can be matched; is the set of alive bidders at that can be exchanged for . Bidders still alive at the end (time ) are called survivors and denotes this set. We denote the set of bumped bidders by .

Definition 2

Let be a bidder and fix the bids of all other bidders. Let (’s acceptance weight) be the infimum of all bids that can make such that is accepted when he bids. Similarly, let (’s survival weight) be the infimum of all bids that can make such that is accepted when he bids and survives until time (the end). Clearly, . Let .

Note that always exists since it suffices to bid . Also, and are independent of ’s actual bid, but may depend on the time bids and on the other bidders’ bids or arrivals (times of bidding). Note that can be computed by the seller as soon as a bidder arrives whereas may depend on future bidders and thus can only be computed at time .

In summary, is If is a survivor, ’s price is as follows:

| (2) |

The common case is when : gets a discount amounting to the highest refund it could have otherwise obtained: . The special case of occurs when ’s acceptance is enough for its survival (in particular if is the last bidder). When , from the bidder point’s of view, M posts a price of .

This concludes the definition of M. We will now study its properties.

4 Incentive Properties

The following theorem summarizes our mechanism’s favorable incentive properties.

Theorem 1

The M mechanism is individually rational. Bidding one’s true value (weakly) dominates any lower bid. If honest, any survivor is (weakly) best-responding.

The proof follows from the two lemmas below.

Note that with bump payments (“money for nothing”) we cannot hope to have a truthful mechanism since anyone with no interest in any allocation can bid hoping to get a bump payment. It is nevertheless possible that other types of truthful competitive allocation mechanisms exist.

Lemma 1

Bidding less than one’s true value is dominated by bidding one’s true value. A bumped bidder’s best response may however be to bid more than its true value.

Proof 4.2.

If , bidder ’s highest possible bump payment is . The price of has been chosen such that prefers winning to being paid if and only if . That is, the best bid can make (’s best-response) is to bid just below if and to bid its true value otherwise.

If , then can never get a bump payment and simply faces a take-it-or-leave-it offer of .

Can a bidder ever incur a loss by participating? The following result shows that if truthful, no bidder will have a negative utility, i.e. the mechanism is individually rational.

Lemma 4.3.

If bidder bids its true value , then ’s utility after participating in the mechanism is non-negative.

Proof 4.4.

When surviving, pays at most . If is not accepted then ’s utility is 0. If is accepted and then bumped, ’s utility is .

In the following two sections we show that apart from favorable incentive properties, M is also competitive with respect to revenue and efficiency.

5 Efficiency of M

Definition 5.5.

For any vector of weights, we let be the weight of the optimal matching (recall that the seller knows any bidder’s choice set). We will overload the expression and let also denote the optimal matching (as opposed to its weight), when there is no confusion. If is a set of bidders, we will denote . Unless specified otherwise, denotes the input bids and denotes the true values. We will denote by .

From an algorithmic perspective, our mechanism is a approximation to the optimum assignment (Lemma 5.8). However, if incentives are not aligned then bidders may want to significantly alter the input to the algorithm (their bids). The allocation may then be a poor choice considering bidders’ true values. We show that this is not the case, in Theorem 5.6, our main result regarding M’s efficiency: the assignment output by our mechanism is a constant factor (depending on and ) approximation to the offline optimum on bidders’ true values if bids are "reasonable".

Theorem 5.6.

Let be a set of bids such that each bidder bids at least its true value, that is , and the sum of all bidders’ utilities is non-negative. When run on , M’s efficiency with respect to the true values is:

Note that if all bidders are truthful then the right-hand side constant can be increased to (see Lemma 5.8 below).

Recall the impossibility of making truthfulness a dominant strategy due to the use of bump payments. Theorem 5.6’s assumption allows for some bidders to have negative utility and therefore fail to best-respond (Lemma 4.3 shows that simply by being truthful, a bidder’s utility is at least 0) as long as overall, gains outweigh losses in utility. The assumption fails when, for example, bidders with value 0 for an allocation (the “speculators” of Section 7) grossly overestimate the actual bids and end up being allocated and having to pay due to bidding too high. In such a scenario, the true value of the allocation may be very small, possibly 0. We refer the reader to Section 7 for a more detailed discussion on how speculators affect incentives.

We now proceed to proving Theorem 5.6, establishing a few other important results along the way. The following bid vector will prove useful:

Note that if then .

Lemma 5.7 is used for both efficiency and revenue claims. Its proof is more involved and we defer it to the Appendix.

Lemma 5.7.

Any survivor is also in .

The following result provides an upper bound on the sum of bumped bidders’ bids and shows that is a approximation to the optimal offline matching given the same set of bids. Recall that is the set of bumped bidders.

Lemma 5.8.

We have . Also, .

Proof 5.9.

For each , let be a chain such that: bumps , . To simplify notation, assume . We will show that

The claim will follow since the set of bidders is the disjoint union of survivors’ chains.

Since bumped , we have . Since bumps , , . Thus by induction, . We get

We have . Each inequality is implied by the fact that no bidder’s contribution decreases when going from the left hand side to the right hand side. The equality follows from Lemma 5.7: is an optimal basis for , i.e. .

An analogous lemma can be found in [9]. Our constants are tighter because in our model, a bidder’s value for any slot is the same, and all edges incident to a bidder arrive simultaneously. These bounds are almost tight:

Example 5.10.

Consider truthful bidders competing on one item; bidder is the -th to arrive and has value unless , whose value is . Bidder bumps , . Only the -st bidder survives. The bumped bidders have total weight . is .

Proof 5.11 (of Theorem 5.6).

By assumption, bidders’ total utility is non-negative:

We have from Lemma 5.8 that . We prove that

The theorem then follows by algebraic manipulation.

Let . Clearly, , otherwise they would not have survived. Also, by definition. If everyone in bids instead of , the outcome does not change (they still bid above their survival thresholds). By Lemma 5.8, and by definition, giving the claim.

5.1 Effective Efficiency

Efficiency is usually measured as the sum of winning bidders’ values. An alternative definition which also takes into account the losses of bumped bidders and may be more appropriate when cancellations are allowed is the following:

Definition 5.12.

Let be a sequence of bids and an online allocation algorithm, possibly with cancellations. Let (resp. ) be the set of winners (resp. bumped bidders) when is run on . We define the effective efficiency of on as

’s effective efficiency competitive ratio is

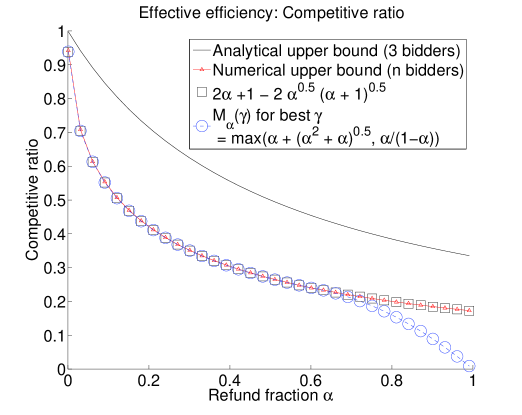

We present an upper bound (obtained numerically) on the competitive ratio of any deterministic algorithm. For and a certain , matches this upper bound.

For a fixed , let a positive integer and : we aim for bidders and a competitive ratio of . Consider one item and a sequence of bids on it (bidder bids ) such that and

| (3) |

We will look for a such that

| (4) |

Unfortunately, does not have a nice closed form for (in addition, may be not be unique - the smallest is then of interest).

Theorem 5.13.

Proof 5.14.

On any input, the offline optimum with respect to effective efficiency is simply the highest weight assignment, and it results in bumping no bidders.

Assume that the bids that arrive are for some . Then at each , the algorithm must accept , or its competitive ratio will be smaller than when . This is clear for . Fix . Let be the highest (i.e. the offline optimum) of . If does not accept then the competitive ratio on input will be at most

where the equality follows from Eq. (3). Now we claim that whether or not accepts , its competitive ratio will be at most . If is accepted, has been lost due to bumping bidders ; if is rejected the effective efficiency is . By Eqs. (3) and (4), both quantities are a fraction of , which in turn is at most , the optimal (effective) efficiency.

Figure 1 strongly suggests that the competitive ratio of any algorithm cannot be higher than , shown as squares in the figure. Note that for this the characteristic equation of Eq. (3) has a double root.

The triangles plot the minimum found for the corresponding for different values of (we used Fibonacci values up to rank 12, i.e. largest was 144). The values were found via binary search. It was true in general, although not always, that the higher , the lower . We suspect that one can always find an increasing sequence of integers such that a solution to Eqs. (3) and (4) converges from above to as .

Lemma 5.8 implies that for our algorithm

Let . Subject to the constraint , is maximized for . is displayed in Fig. 1 by circles. The value 0.618 (the golden ratio) is where becomes higher than . If , , which matches the numerical upper bound. Recall that this is just a worst-case lower bound on the effective efficiency, but likewise, so are the upper bounds. The top curve plots .

Recall that when all bidders can be tentatively accepted (by letting ) since they incur no loss and do not have to be refunded. Then, the optimal matching can be found via a one-shot (offline) algorithm at time .

6 Revenue of M

We show that apart from favorable incentive and efficiency properties, M is also competitive with respect to revenue.

As a revenue benchmark, we consider the offline VCG mechanism because it generates the highest revenue among truthful efficient allocation mechanisms [7]. We show that our mechanism is competitive with respect to revenue with VCG on bidders’ true values.

Let be a sequence of bids - when defining VCG on we will assume that all bids are received at once by VCG. Let denote the set of all bids in except bidder ’s. The VCG mechanism implements an efficient allocation and thus the matching it outputs is optimal. If then VCG charges bidder its externality on the other bidders:

| (5) |

We will use the following known (see e.g. [3], Fact 3.2) combinatorial property of our setting: , if then .

Lemma 6.15.

A winning bidder’s VCG payment is a losing bid. Also, the VCG revenue can only increase if some bids in are increased.

On bids we denote the VCG revenue by and the net revenue of M (payments from survivors minus bump payments) by .

Theorem 6.16.

Assume , i.e. no one bids below their true value, since that would be dominated. Then

This theorem shows the tradeoff between , the improvement factor required for bumping an accepted bidder and , the fraction returned as the bump payment. For instance, for (refund of 1/4th the bid), if we choose then the constant in Theorem 6.16 becomes , i.e. our mechanism obtains at least a quarter of the VCG revenue.

We will now prove Theorem 6.16.

Lemma 5.8 implies that payments received by M are at least (since only survivors pay) and that bump payments sum to at most . It will suffice to show that .

Let

Lemma 5.7 states that , . Since on VCG payments cannot be higher than its efficiency, . Also, Lemma 6.15 implies

since when going from to only VCG winners may increase their bid, and for all , .

Note that unlike the analogous efficiency result (Theorem 5.6), this result makes no assumption on bidders’ utilities.

7 Speculators

Since money is given away, speculators, that is, bidders without interest in any item are likely to enter the mechanism looking for bump payments. For a speculator , utility is also given by Eq. (1), but with . Speculators may bid (under false identities) more than once or collude. Their bids can effectively induce reserve prices, since actual bidders will have to bid a factor higher than a competing speculator. If speculators bid judiciously on high-demand items, they can garner payment from the auctioneer, who gets even more revenue via larger prices for high-value bidders. So, it is clear that speculators are impactful.

In this section we address the question of how speculators affect the mechanism. In Section 7.1, we show two positive results

-

•

We show that the M algorithm has good overall efficiency, as long as the speculators have positive overall surplus and the survivors are best-responding.

-

•

We prove a bound on the overall revenue that speculators can obtain.

In Section 7.2 we give a more detailed discussion of speculator strategy. Along the way, we show that many natural simplifying assumptions regarding speculators’ or bidders’ strategies are unfortunately false. Specifically, we show that:

-

•

the profits available for speculators may depend on the arrival order of actual bidders (Example 7.20);

-

•

there may be no pure Nash equilibrium for actual bidders or speculators (Example 7.20);

-

•

speculators may prefer to induce a suboptimal perfect matching of actual bidders (Example 7.23);

-

•

a colluding set of speculators may be able to get higher bump payments if some of them survive (Example 7.24).

7.1 Impact on Efficiency and Revenue

The following result gives a competitive ratio of our algorithm’s efficiency with respect to the optimum efficiency given bidders’ true values. It only requires that total speculator utility is non-negative: this is particularly applicable if speculators are coordinated and can make monetary transfers between them.

Proposition 7.17.

Let be a set of bids such that actual survivors are best-responding and total speculator surplus, i.e. the sum of speculators’ payments minus the sum of speculators’ prices, is non-negative. Then the M algorithm with true values has efficiency

The proof is mostly algebraic and deferred to the Appendix. This result is a strengthening of Theorem 5.6: Prop. 7.17’s constant is larger and its preconditions are less general. Note that Prop. 7.17 requires that actual survivors are best-responding; a speculator’s best response cannot induce it to survive.

Next we prove an upper bound on speculators’ profit:

Proposition 7.18.

Speculators’ total profit is at most .

Proof 7.19.

Let be the sum of survival weights for speculators that have survived. Denote speculators’ profit by , where are the participants who obtain bump payments (some may be true bidders).

By Lemma 5.8, , where is the total weight of survivors that are actual bidders. We get

The claim follows since and .

7.2 Speculator Strategies

At first glance, it would seem that it is in the speculators’ best interest to induce an assignment of actual bidders of weight as high as possible in the survivor set, since then overall bump payments would be maximized. This is true in some cases but not always (Example 7.23). The reason for such a distinction is that the order of bidders arriving also influences the maximum refunds attainable by speculators as shown below.

Example 7.20.

Consider two bidders, one bidding , the other , on two items and assume that speculators cannot collude. If arrives first, no speculator can have higher revenue if bumped than when bidding on both items: this is actually a Nash equilibrium (NE) for them. If however arrives first, then speculators could participate with two identities bidding and on both items, both being bumped. One can show via a case analysis that there is no pure strategy NE for speculators.

This example also shows that there may not be a pure strategy NE when only actual bidders participate: if two bidders with low values arrive, followed by the 1 bidder and after that the bidder, then the two low value bidders are essentially speculators and the argument in the example applies.

Observe that a speculator who is bumped with a bid of could have obtained more bump payment by entering an earlier bid of at most ; likewise, he could have obtained yet more by bidding earlier ; and so on. This is formalized as follows.

Definition 7.21.

Let . We say that the speculator is an -geometric speculator with choice set if places bids as follows on choice set . Let be the minimum strictly positive bid that can be made and

Then participates with different identities, placing consecutive bids of on .

If speculators have full information on bidders’ values and bidders in arrive in increasing order of their values, the outcome has many desirable properties:

Lemma 7.22.

Fix a set of actual bids such that bids arrive in increasing order. Suppose that speculators collude and want to maximize their joint revenue. Then optimal speculator bidding has the following consequences:

-

•

no speculator survives, no actual bidder is bumped; all bidders and only them are accepted.

-

•

speculators can achieve the highest payoff possible as given by Lemma 7.18.

-

•

truthful bidding is a NE for all actual bidders.

This is a further strengthening of Theorem 5.6. Optimal speculator bidding in this case is as follows. For each bidder with choice set there will be one -geometric speculator with the same choice set. The proof is deferred to the full version.

This result has an appealing interpretation. If very well informed, speculators can overcome the efficiency loss due to late bidders not being able to improve by a factor over their earlier competitors.

In general however, speculators may prefer to induce a suboptimal perfect matching:

Example 7.23.

Consider two items and three bidders arriving in this order; bidder is interested in item , while bidder is interested in any of or . Note that any matching that does not match all three bidders is valid. Assume that and . The following analysis shows that speculators prefer the suboptimal set of actual bidders and to the optimal one with and .

-

•

If both and survive, then speculators’ profit is at most : the speculator bumped by must have a lower weight than the one bumped by , which is at most . Even if speculators are geometric, speculator profit can only go as high as .

-

•

If however and are alive when arrives, cannot bump . By simply having one geometric -speculator which is bumped by , speculator profit is .

The following example shows that speculators may be able to make more money if they “sacrifice”, i.e. some of them intentionally survive so that others obtain high refunds:

Example 7.24.

Let there be items, actual bidders bidding all arriving before an actual bidder bidding ; all bidders bid on all the items. If speculators coordinate and participate with identities as -geometric speculators on all the items then total speculator payoff is

since will be bumped, but one will survive. If no speculator survives, the most money speculators can make is , by participating as -geometric speculators. For any , for a large enough , speculators’ profit is higher when one of them is sacrificed.

8 Other Game-Theoretic Claims

We will now show that several appealing statements regarding incentives in our algorithm are false.

The algorithm may be more appealing for incentive purposes if we paid a bumped bidder instead of as bump payment. The following example shows why this may result in a deficit:

Example 8.25.

Fix and consider an early bidder bidding and a late bidder bidding on one item where . Bidder survives and pays . If we were to refund an fraction of , would get . The choice of ensures that is paid more than pays, i.e. the mechanism runs a deficit.

We assumed throughout that as soon as a bidder arrives, its choice set is known. If however that is private information as well, incentives become weaker: in Example 8.26, no bid by on its true item is a best-response if bidding on different item(s) instead is allowed. This example also suggests why a naive generalization of M to the setting where bidders have a different value for each of several items would not be able to incentivize bidders to bid at least their true value for each item.

Example 8.26.

Consider two items and the following set of three bidders (arriving in this order): with value for any of (only demanding one of them), who has value for item and bidding 1 on item . Assume and bid truthfully. We will show that, whenever bids on , it can do strictly better by bidding on only.

We claim that if bids on then its utility is at most . This is clear if it survives. If it is bumped by , then its bid cannot be higher than (’s bid), since can replace any of and . But then ’s compensation is at most . Let . By bidding on only and being bumped by , can get utility .

We have however the following conjecture: if a bidder prefers surviving to being refunded, they are better off bidding on their true choice set.

If bidders myopically and simultaneously best-respond then these dynamics may lead to bid vectors where the sum of their utilities is negative:

Example 8.27.

Let there be items and bidders (interested in any item) arriving in increasing order of their values: bidders have value , bidders have value and bidder has value . Assume they all bid truthfully initially.

Bidders are best-responding by Lemma 1 and they will not change their bids. Each bidder ’s, , myopic best-response is to bid . Only one of them will be bumped by and the others will survive: the sum of their utilities is at most . No bidder between and will be accepted. Since ’s utility is at most , for large the sum of all bidders’ utilities will be negative.

This example does not preclude good performance for other dynamics.

9 Concluding Remarks

Advertisers seek a mechanism to reserve ad slots in advance, while the publishers present a large inventory of ad slots with varying characteristics and seek automatic, online methods for pricing and allocation of reservations. In this paper, we present a simple model for auctioning such ad slots in advance, which allows canceling allocations at the cost of a bump payment. We present an efficiently implementable online mechanism to derive prices and bump payments that has many desirable properties of incentives, revenue and efficiency. These properties hold even though we may have speculators who are in the game for earning bump payments only. Our results make no assumptions about order of arrival of bids or the value distribution of bidders.

Our work leaves open several technical and modeling directions to study in the future. From a technical point of view, the main questions are about designing mechanisms with improved revenue and efficiency, perhaps under additional assumptions about value distributions and bid arrivals. Also, mechanisms that limit further the role of speculators will be of interest. In addition, there are other models that may be applicable as well. Interesting directions for future research include allowing bidders to pay more for higher (making it harder for future bidders to displace this bidder) or higher (being refunded more in case of being bumped). Other mechanisms may allow to be a function of time between the acceptance and bumping. Accepted advertisers may be allowed to withdraw their bid at any time. There may be a secondary market where bidders may buy insurance against cancellations. Finally, advertisers may want a bundle of slots, say many impressions at multiple websites simultaneously, which will result in combinatorial extension of the auctions we study here. We believe that there is a rich collection of such mechanism design and analysis issues of interest which will need to inform any online system for advanced ad slotting with cancellations.

Acknowledgments. We would like to thank Stanislav Angelov for pointing us to [9] and the EconCS research group at Harvard for helpful discussions.

References

- [1] M. Babaioff, N. Immorlica, and R. Kleinberg. Matroids, secretary problems and online algorithms. In Proceedings of SODA, 2007.

- [2] S. Bikhchandani, J. Schummer, S. de Vries, and R. Vohra. An ascending Vickrey auction for selling bases of a matroid. November 2006.

- [3] M. C. Cary, A. D. Flaxman, J. D. Hartline, and A. R. Karlin. Auctions for structured procurement. In Proceedings of SODA, 2008.

- [4] N. B. Dimitrov and C. G. Plaxton. Competitive weighted matching in transversal matroids. UT Austin, Technical Report T-08-03, January 2008.

- [5] U. Feige, N. Immorlica, V. Mirrokni, and H. Nazerzadeh. A combinatorial allocation mechanism for banner advertisement with penalties. In World Wide Web Conference (WWW), 2008.

- [6] J. Gallien and S. Gupta. Temporary and permanent buyout prices in online auctions. Management Science, 53(5):814–833, May 2007.

- [7] V. Krishna. Auction Theory. Academic Press, 2002.

- [8] R. Lavi and N. Nisan. Competitive analysis of incentive compatible on-line auctions. In ACM Conference on Electronic Commerce, pages 233–241, 2000.

- [9] A. McGregor. Finding graph matchings in data streams. In Proceedings of APPROX-RANDOM, pages 170–181, 2005.

A.1 Proof of Prop. 7.17

Assume that actual survivors bid honestly: ; at the end of the proof we will eliminate this assumption.

Let .

As can only be if bumps or if is bumped instead of , the set of survivors will still be if the mechanism is run on instead of . We have

| (6) |

The first inequality follows from Lemma 5.8. Each actual bidder bids at least its true value: and there is the additional competition of speculators; this fact yields the second inequality. Also,

Again, the first inequality follows from Lemma 5.8. By assumption, speculator payments (a fraction of their survival weights) cannot be higher than speculator refunds:

By combining the last two relationships, we get

Adding to both sides we get

The last equality follows since actual survivors are bidding truthfully. This last inequality, together with Eq. (6) imply the proposition’s claim.

Lemma 1 shows that bidding truthfully is a (weak) best-response for survivors. Let be an actual survivor. Any bid above its true value is also a best-response for . In the claim, as we increase ’s bid, the right-hand side quantity increases (if at all) at a constant rate which is less than 1, the left-hand side quantity’s increase rate.

A.2 Proof of Lemma 5.7

We will denote by the minimum bid bidder must make in order to survive up to and including time . Then and . It is clear that .

Definition A.28.

Let be a set of bidders. We say that is tight for a bidder at time if all bidders in are alive at , can be matched but cannot be matched. We say that -dominates a bidder at time in the algorithm if is tight for at and , .

Lemma A.29.

is tight for at .

Proof A.30.

can be matched since .

Suppose for a contradiction that can be matched. Then since is a perfect matching by assumption. Therefore there exists such that can be matched. There exists exactly one bidder and we have that is a perfect matching, implying , contradiction.

Let be the time step when ceases to be alive (i.e. if is not accepted or the time is bumped if was accepted). We inductively construct a sequence as follows: if is not accepted, ; if is bumped by then . At time ,

-

•

if no bidder in is bumped, then we let .

-

•

if bumps some then we let

We will prove inductively on that

Lemma A.31.

-dominates at time .

Proof A.32 (of Lemma A.31).

Note that by definition, all bidders in are alive at .

Base case :

If is not accepted (), cannot bump any bidder in : therefore . is tight for at by Lemma A.29.

If is bumped, then . can be matched since they are all alive at . cannot be matched since otherwise would not need to bump .

Inductive step: Assume that -dominates at . If at time , no bidder in is bumped, then the claim obviously holds by the induction hypothesis. Otherwise, let be the bidder that is bumped by .

Clearly, can be matched since they are alive at . Suppose for a contradiction that could be matched. since is no longer alive. can be matched since they are all alive at . As , either or can be matched. The first case is not possible since a subset, , cannot be matched (by the induction hypothesis); the second case is not possible since cannot be matched (Lemma A.29). We have reached a contradiction, so must be tight for .

By the induction hypothesis, . As noted before, survival thresholds can only increase from to and . ∎

We are ready for

Proof A.33 (of Lemma 5.7).

Let be the [] assignment (where ties are broken in favor of bidders in ). Suppose for a contradiction that there exists a non-survivor . By Lemma A.31 for time , is dominated by a set at time . Since , but , in any bidder in has a higher weight than .

Since is a perfect matching and can be matched there must exist ( if is a perfect matching) such that is a (perfect) matching. We know that cannot be matched, therefore . However, therefore . can be matched and has size . Therefore there , such that can be matched. That implies , i.e. . But then is a perfect matching of higher weight than , contradiction.

That is, , i.e. since both are perfect matchings.