Theory of market fluctuations

Abstract

We propose coalescent mechanism of economic grow because of redistribution of external resources. It leads to Zipf distribution of firms over their sizes, turning to stretched exponent because of size-dependent effects, and predicts exponential distribution of income between individuals.

We present new approach to describe fluctuations on the market, based on separation of hot (short-time) and cold (long-time) degrees of freedoms, which predicts tent-like distribution of fluctuations with stable tail exponent ( for news). The theory predicts observable asymmetry of the distribution, and its size dependence. For financial markets the theory explains first time “market mill” patterns, conditional distribution, “D-smile”, z-shaped response, “conditional double dynamics”, the skewness and so on.

We propose a set of Langeven equations for the market, and derive equations for multifractal random walk model. We find logarithmic dependence of price shift on the volume, and volatility patterns after jumps. We calculate correlation functions and Hurst exponents at different time scales. We show, that price experiences fractional Brownian motion with chaotically switching of sub- and super-diffusion, and calculate corresponding probabilities, response functions, and risks.

pacs:

05.40, 81.15.Aa, 89.65.GhI Introduction

First question behind any research is why do we need it? There are no unique approach in econophysics, and the number of different approaches grows exponentially with time. How can we decide, which of them is “correct”, if by construction, any one well describes empirical facts?

The answer is simple: in no way. All of them are equivalent at regions of their applicability. But these regions are very different, and only several theories able to describe a large variety of empirical facts. Extrapolating, one can assume that only one theory can predict all important phenomena: Market mill patterns, multifractality of fluctuations, volatility patterns, different Hurst exponents above and below a time , and many other facts. Some of them can be described in different ways, but not the hookup of all facts.

What criteria should satisfy such theory? At first sight, it is mathematical rigor. The most striking example is the Flory approach in polymer physics, which is absolutely “wrong” mathematically, but extremely well describing all known situations. All multiple attempts to (im)prove it were failed. We conclude, that the rigor of the theory is usually “inversely proportional” to intuition.

Well, what kind of the theory should not be? If any new fact or their series need to introduce additional terms or ideas into the theory, the later can be considered as a collection of facts, arbitrary ordered according to the test of the author. We think, the real theory must predict in future yet unknown facts (at present this criterium is equivalent to extremely wide region of its applicability), to be as rigor as possible, and use minimum of initial assumptions.

We do not know other criteria of the “validity” of the theory, and this is the reason why the theory must describe all known trustable facts. Present paper can be considered as an attempt to follow this criteria. Only one main idea lays in the basis of our theory of market fluctuations: we assume, that they can be described as random walk motion at all time scales. In the case of financial market, it is random trading at all time horizons from seconds to tenths years.

Our theory can be considered as an attempt to make a step from numerous descriptive approaches toward a physical Langeven formulation of the “econophysical” problem. This is why we emphasize analogies with other branches of physics, which may confuse econo-physicists otherwise. Although we show, that multi-time random trading allows to explain most of market dynamics, it may be extended later in many directions.

As a strategy line, for each problem we try to construct a simplified model of such multi-time random motion, capturing the most of physics. As the result, we left with several parts of the whole puzzle, strongly inter-correlated with each other. It is the reason of unusual length of this paper, which can not be cut into several independent small parts.

II Firms, cities and income distributions

II.1 Is there thermodynamics of the market?

Econophysics studies physical problems in economics, and most of its results were obtained from analogy with thermodynamics. One of classical problems of econophysics, the firm grow, is usually described by the model of stochastic firm growingGibrat . In order to explain empirically observed Zipf distribution of firm sizesPe-PRE-96 it is proposed to introduce the lower reflecting boundary in the space of firm sizes, which stabilizes the distribution to a power lawLS-96 . Unfortunately, this explanation is inconsistent for firms of one or several employers, well described by the same empirical Zipf distribution.

Different models of internal structure of firms were proposed for the stochastic mechanism of firm growing. Hierarchical tree-like model of firm was studied in Refs. Am-PRL-98 ; Le-PRL-98 . A model of equiprobable distribution of all partitions of a firm was introduced in Ref.Su-Ph-02 . Both models neglect the effect of competition between different firms. The random exchange of resources between firms was taken into consideration in “saving” modelsSa-80 . In Refs. Cha-95 ; Dra-00 ; Cha-04 ; Sl-04 the process of stochastic firm grow and loss was considered by analogy with scattering processes in liquids and gases. The distribution of firms over their sizes in different countries was studied in Ref.Ra-Ph-00 .

The theory of firms is usually called microeconomics, and from economical point of view it is hard to consider the stochasticity as the moving force of economic grow. While in thermodynamics the stochasticity originates from interaction with a huge “thermostat”, there are no such thermostat for the market, which subsists only because of activity of its direct participants.

This puzzle forces us to develop a “mean field” theory of firm growing, neglecting any fluctuation processes. We show, that the moving force of evolution on the market are not thermal-like excitations, but the supply of external resources, which are (re-)distributed between different firms. Exhaustion of the resource kills this (part of the) market, while appearance of a new resource gives rise to a new market. The process of firm growing and mergence is similar to coalescence of droplets of a new phase, when stochasticity plays only minor role.

In section II.2 we show that the coalescence theory predicts Pareto power low for the distribution of firm sizes. We propose self-similar tree-like model of firms in section II.2.2. This model is solved in Appendix B, and we show, that it explains empirically observable time dependence of the Pareto exponent for the world income.

The formal resemblance of observable exponential distribution of the income between individuals to Boltzmann statistics was used in Ref.DY-01 to justify the applicability of methods of equilibrium thermodynamics. But how can all sectors of country economics and services always be in thermal equilibrium? In section II.2.3 we propose an alternative explanation, based on unified tax policy in the whole country: the coalescent approach predicts, as a by-product, the exponential income distribution, even without invention of thermal equilibrium. This distribution is valid for the majority of the population, and statistical fluctuations are only responsible for power tails of its upper part (1–3%).

Countries with different financial policy have different “effective temperature” of the distribution, which can be equilibrated only after unification of their financial policies, even without establishment of a “heat death” – global thermal equilibrium. Although one may consider the perpetual trade deficit of US as consequence of the fundamental second law of thermodynamicsDY-01 , it would be more natural to explain it by financial policy, directed on attraction of resources to the country.

Econophysics is not only one field, deceptively resembling thermodynamics, we have to mention also a sand, turbulence and other macroscopic systems, which form complex dissipative structures in the response on some external forces. Although such “open systems” can not be characterized by thermodynamic potentials, the process of dissipation is accompanied by the rise of information entropy. We calculate the entropy of the market and show, that it can only increase with time, since the market irreversibly absorbs external information (there is deep analogy with physics of decoherence, discussed in Conclusion).

“Thermodynamic-type” models predict asymptotically Gaussian distribution of firm grow rates, while the real distribution has tent-like shape. In order to reproduce it, in Ref. St-JPh-97 an artificial potential was introduced in diffusion equation, restoring the firm size to a certain reference value, at which the grow rate abruptly changes its sign. In this paper we elaborate a new approach to study dynamics of temporal dissipative structures on the market, which do not use these artificial assumptions.

In section II.3 we introduce new general approach to study market fluctuations. Main ideas of this approach will be first formulated for the problem of firm grow. The market is the system with multiple (quasi-) equilibrium states, characterized by extremely wide spectrum of relaxation times. By analogy with glasses, for given observation (coarse graining) time interval we can divide all degrees of freedom of the market into “hot” and “cold” ones, depending on their relaxation times. Hot degrees of freedom are in equilibrium, and they generate high frequency fluctuations because of uncertainty on the market, while cold degrees of freedom are not equilibrated, and evolve on times large with respect to . As in the case of spin-glasses, high degeneracy of quasi-equilibriums in the market is reflected in the presence of a gauge invariance. Any averages should be defined in two stages: first, the annealed averaging over hot degrees of freedom, and then quenched averaging over cold degrees of freedom.

We demonstrate, that our theory reproduces empirically observable (in general, asymmetric) tent-like distribution of firms over their grow rates. In section II.3.4 we show, that this distribution has fat tail with stable exponent , equals to the number of essential degrees of freedom of the noise ( for Markovian statistics of hot degrees of freedom, and for uncorrelated noise).

II.2 Mean field theory

Dynamics of firm growing is similar to kinetics of growing of droplets of a new phase. Large firms can absorb smaller ones, and they can grow or leave the business, by analogy with resorption and growing of droplets in the supersaturated solution. Below we use this analogy to construct a new theory, not relying on stochastic mechanisms of firm growth. Entropic and microeconomic interpretations of our theory are discussed in Appendixes A and C.

II.2.1 Zipf distribution

For definiteness sake we define the firm size as the number of its employees. In general, it could be any resource, shared between different firms on the market. According to economic approach (analog of the mean field approach in physics) firms can hire or loose the staff only through the “reservoir” of unemployments of value at time . Diffusion processes lead to finite value of the “natural unemployment”. “Actual unemployment” is the sum of Fr–68 and the “market unemployment”, :

The equation of the resource balance can be written in the form

| (1) |

where is the supply of external resources. The probability distribution function (PDF) of firm sizes is determined by the continuity equation,

| (2) |

where is the rate of ordered motion in the space of firm sizes. Diffusion contribution in Eq. (2) is negligible in coalescent regime. According to the famous Gibrat’s observationGibrat the relative grow rate of the firm,

| (3) |

do not depend on its size, . In the case of full employment, , the average numbers of people getting a job and leaving it are the same, and there are no source for firm grow, . At small we can hold only linear term in the series expansion of the grow rate in powers of with constant .

To solve the set of equations (1) – (3) we substitute Eq. (3) with into Eq. (2), and find its general solution

where is the firm size at initial time and is arbitrary function. Substituting this solution into the balance equation (1) and introducing new variable of integration , we find

| (4) |

Consider the case of power growing of external resources,

| (5) |

For general time dependence its logarithmic rate is determined by expression

| (6) |

In the case of small unemployment value, , general solution of Eq. (4) takes exponential form, . Substituting this expression into Eq. (4) and taking into account that the distribution can not depend on initial firm size, , we find and

where and are maximal and minimal firm sizes on the market. The solution of this equation has the form

| (7) |

First of Eqs. (7) predicts, that the economic grow, see Eq. (5), leads to less actual unemployment, , in qualitative agreement with the famous macroeconomic “Fillips curve”. Close quantitative relation between the coalescent theory and the Fillips low is established in Appendix C.

We conclude, that for any monotonically increasing function the distribution of firms over their sizes has Zipf form:

| (8) |

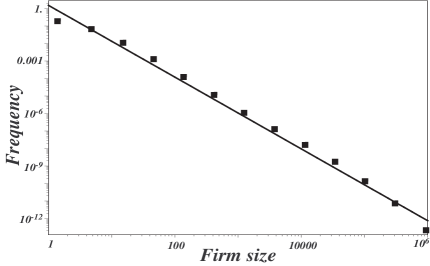

This dependence was really observed for extremely wide range of firm sizes, see Fig. 1, where empirically observable distribution

| (9) |

is plotted. The Zipf distributionPe-PRE-96 (8) is valid for the entire range of US firmsAx-01 (from to ) with Pareto exponent very close to unity.

The same mechanism may be responsible for power distribution function of cities over their population, the amount of assets under management of mutual fundsGa-03 , banksPuHa-04 and so on. In the analysis of city population in different countries, the exact form of Zipf’s law (9) was confirmed in 20 out of 73 countriesSoo-02 . Deviations from this low will be studied in next section.

II.2.2 Stretched exponent

The Pareto exponent (9) can deviate from because of ineffective management, strong influence of industry effects on small firms and so on. With increasing size, these effects gradually trail off, while remaining international, national and regional shocks equally affect all firms. Assuming self-similiarity of firm structure, the variation of the firm size can be described by Master equation

| (10) |

with constant and .

To derive Eq. (10), consider the firm as the self-similar treeSt-JPh-97 of generations, each of branches. The size of each subdivision is described by the same type of equation (10),

| (11) |

Substituting the estimation for the size of the whole tree in Eq. (10) and comparing with Eq. (11), we find the relation between coefficients of Master equations (10) and (11):

In Appendix C we show that while the Gibrat grow rate is fixed by economic factors, the coefficient of job destruction can experience strong random fluctuations . Neglecting fluctuations of in Eq. (10) we find that fluctuations in size are inversely correlated to the size with an exponent :

| (12) |

In order to estimate the exponent , consider a hypothetical structureless firm with of the size . Fluctuations of its size are characterized by Gaussian exponent . The exponent of real firms takes small values Le-PRL-98 , corresponding to the number of tree generations . Using Eq. (12) we find the dependence of the standard deviation of grow rate on the firm size,

| (13) |

where does not depend on firm size . This relation is in excellent agreement with empirical dataSt-JPh-97 ; St-Na-96 .

The condition (10) determines the critical firm size

| (14) |

Small firms with collapse with time and may leave from the business (or reach a certain fluctuation size), while large firms with grow. In Appendix A we find the entropy of the firm of size , and show that corresponds to its minimum, and also to the minimum point of a “U-shaped” average cost curve in the conventional economic theory (Appendix C). We also derive maximum entropy principle for the market (Appendix A), which is known as the most foundational concepts of Gibbs systems.

In Appendix B we show that the solution of Eqs. (1), (2) with the rate (10) has stretched exponent form:

| (15) |

Taking the limit we reproduce Eq. (9). It is shown that stretched exponent is the best fitting approximation for many observable distributions (size of cities, population of different countries, popularity of executors, lifetime of different species, strength of earthquakes, indices of quoting, number of coauthors, relative rates of protein synthesis and many othersLa-98 ; Da-02 ; Ne-01 ), which are determined by the competition of units for common resources. At small but finite expanding in Eq. (15) we find

| (16) |

We conclude, that the exponent of Pareto distribution is, in general, not universal and depends on current rate of external supply, Eq. (6). This conclusion can be verified by empirical observations: typically, the value of this exponent is in the interval . For example, the size distribution of Danish production companies with ten or more employees follows a rank-size distribution with exponent KN-01 .

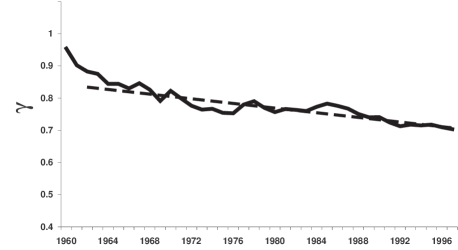

To confirm the dependence of the exponent on the supply rate , consider the distribution of world income across different countries. We assume, that countries could be described by the same Master equation (10) as large firms. Exponential growing of consumable resources leads to linear time dependence of , see Eq. (6). As the result, the exponent linearly decreases with time, in good agreement with empirical observations, see Fig. 2. Assuming, that doubles every 12 years, we estimate , corresponding to a reasonable number of hierarchical management ranks in the “typical” country.

II.2.3 Income distribution

In order to find the distribution of income between individuals we first introduce the most important economic terms. The total income per state, , is shared between all individuals and the state expenses, , according to the balance equation (1). There are some minimal expenses of the state, , and the inequality is usually regulated indirectly, through taxes, which determine the relative income rate, , of individuals. Therefore, the income can be described by a generalization of the Master equation (3),

| (17) |

The last term describes the rate of losses (living-wage), the same for all individuals (linear in losses renormalize ). Since Eq. (17) has the form of Eq. (10) with , from Eq. (15) we get exponential distribution of the income:

| (18) |

According to Eq. (144) of Appendix C the average income (the “temperatureSY-05 ”) linearly grows with time, in good agreement with empirical observationsSY-05 , and also rises with the supply rate (6). It is small for countries with low living wage , producing high inequality in incomes.

Analysis of empirical data showsDY-01 , that for approximately of the total population, the distribution is exponential, while the income of the top individuals is described by a power-law (16) with time dependent Pareto index . This tail is because of speculation in stocks, when the income is proportional to the volume of sale/buy . The distribution of large volumes is power tailed, . The exponent is not universal, it depends on individual stocks with typical value , in good agreement with observable valuesSY-05 (changing of the most profitable stocks leads to variations in ).

In general, the income may come from different sources. In the case of independent sources convolution of exponential distributions gives the Gamma distribution , which better describes Russian Rosstat data of salary distribution.

II.3 Fluctuation theory

II.3.1 Cold and hot degrees of freedom

Our approach to the description of fluctuations on the market is related to the main idea of microeconomic theory, based on independent study of “short-time” and “long-time” periods of firm growth. The separation of time scales also has deep analogy with methods of study of complex physical systems with a wide spectrum of relaxation times, as glasses. For given observation time degrees of freedoms of such systems can be divided into “hot” and “cold” ones. Hot degrees of freedoms fluctuate in the short-time period () given that cold degrees of freedoms are fixed and can only vary in the long-time period (). Instead of consideration of slow dynamics of one system in the long-time period one usually study statistical properties of an ensemble of such systems at the given time .

We apply this approach to find PDF of grow rates of firms, which have different dynamics in “short-time” and “long-time” periods. In order to establish general expression for oscillations of the parameter (10) it is instructive to consider first single-harmonic case. General expression can be expanded over two basis functions and :

| (19) |

which are orthogonal:

| (20) |

Here means time average. Instead of two real basis functions it is convenient to introduce one complex function and complex amplitude , in terms of which the scalar product in Eq. (19) is given by expression . In the following we use bold notations both for vectors and complex numbers.

In general case, the frequency of quick oscillations of (as well as its amplitude) randomly varies with time. Real and imaginary parts of can be considered as random values normalized by condition (20), where has the meaning annealed averaging over the noise . Complex amplitude is fixed in the short-time period, and can be considered as random variable in the long-time period (or for the ensemble of different firms for given time ). The random function and the amplitude describe hot and cold degrees of the freedom of the market, respectively.

Notice, that (19) is invariant with respect to “gauge” transformation

| (21) |

with constant , reflecting high degeneracy of market quasi-equilibrium states.

II.3.2 Double Gaussian model

We first calculate PDF of fluctuations ,

| (22) |

The bar means ensemble (quenched for the time ) averaging over amplitudes of fluctuations of different firms. The main assumption of “Double Gaussian model” is extremely simple: since tactics of firms at the short-time period is determined by large number of essentially independent factors, we assume Gaussian statistics of random variable at time horizon (due to centeral limit theorem). But two different firms (or the same firm at two different time intervals ) will have, in general, different amplitude of fluctuations at the long-time strategy horizon. Since the strategy of firms is also determined by large number of independent random factors, we assume Gaussian statistics of the random amplitude with dispersion .

Due to the gauge invariance (21) the noise and the amplitude PDFs could depend only on moduli and . In this section we assume, that hot () and cold () random variables are independent with zero average and Gaussian weights

| (23) |

respectively.

Fourier transform can be used to calculate the averages:

We first calculate the average over Gaussian normalized and and get . Calculating the average over and , we get . The last step – is to take the inverse Fourier transform of this :

| (24) |

Exponential distribution of firm grow rates (24) was really observed for typical fluctuations , see Eq. (12), with the exponent . We conclude, that tent-like exponential distribution of firm grow rates is the consequence of Gaussian statistics of all degrees of freedom (hot and cold) of the market.

II.3.3 Asymmetry of PDF

The assumption of Double Gaussian model about independence of cold and hot variables is, in general, too strong, and the noise is (anti)correlated with the amplitude . Taking such anticorrelations into account, we can write general expression for the noise, satisfying gauge transformation (21):

| (25) |

where is the dimensionless correlation factor and random variable is not correlated with , and has zero average, . In the case positive and negative fluctuations of firm grow rate, , have equal probability, while in the case of positive firms will in average grow (because of grow of external resources, see section II.2).

At economic level anticorrelations between firm tactics and strategy (25) reflect the fact that firms prefer to have tactical losses with the hope to get a profit at strategy horizons (say, by pressing out business rivals). And firms (and countries), aimed at the maximum instant profit without significant investments in the short time period will eventually get losses in the long time period.

Repeating our calculations for the model (25), we again find exponential distribution (24)

| (26) |

but with different widths () of positive and negative PDFs, and the dispersion :

| (27) |

The average of this distribution is shifted to negative , corresponding to systematic tendency to grow:

| (28) |

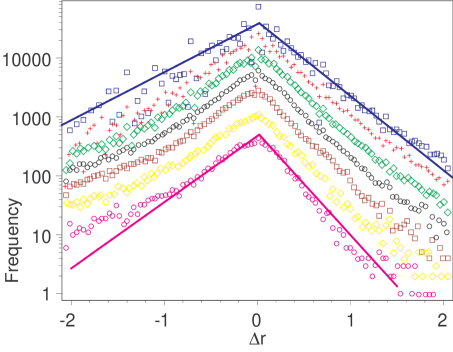

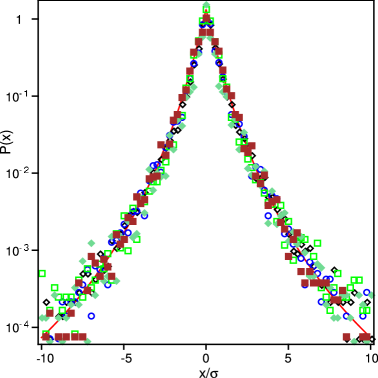

Such asymmetrical exponential distribution was really observed in the analysis of empirical data in Ref.PeAxTe-06 for large averaging intervals ( years, see Fig. 3). In Fig. 3 the -axis is in units of (12), and not . Empirical value , and for typical we reproduce the observed mean .

II.3.4 Fat tails

One of the most prominent features of PDF, the fat tail, is usually attributed to large volatility fluctuations (in different stochastic volatility and multifractal models). In this section we show, that the tail originates from large jumps of the noise, and not of the volatility. This new mechanism predicts universal tail exponent for stock jumps, independent on the coarse graining time interval .

Fluctuations of the Double Gaussian model are characterized by random variable , which is Gaussian at the time interval and normalized by the condition (20). The problem is that even if we normalize Gaussian variable for given time interval , this normalization will be broken at next time intervals because of the intermittency effect: relatively rare, but large picks of fluctuations. The only way to normalize for all times is to divide it

| (29) |

by the mean squared average

| (30) |

slowly varies at time interval , and therefore, random variable leaves Gaussian at time scale . The division of by removes from general Gaussian process the long-time (at the time scale ) trend (long-time variations of the amplitude), leaving only high frequency components.

Standard definition of the mean square assumes that weights in Eq. (30) do not depend on , and we reproduce our previous result (24) for PDF. But this definition must be corrected, since there are no any fundamental value of dispersion , which can only be estimated from the knowledge of past values of . As the first step, we have to put at and get

| (31) |

In the case of totally uncorrelated events is determined only by the “reference” value of at previous time interval, and all at . Terms with describe the effect of correlations of events, leading to variations .

Second, hot variable can vary only on the time scale small with respect to . Therefore, all at , and random variable has Markovian statistics with correlations only between neighbour time intervals . Otherwise it will depend on many time intervals time in the past, which is prohibited by definition of hot variable .

And the last: the only information known in future about past fluctuations, is the very increment , which depends only on one component of along the vector . The information about corresponding “perpendicular” component do not enter to the increment, and is lost. Therefore, we should drop the contribution of from correlation terms with in Eq. (31): . After all these corrections we left with expression for the mean square in Eq. (29):

| (32) |

Although we get similar results for any quickly decaying weights , calculations are much simplified in the case of equal weights and all at . In order to calculate PDF of the noise (29), we rewrite it in the form

| (33) |

where we take the average over Gaussian variable . The probability distribution of the random variable (32) is . Using exponential representation of this -function, we get

Substituting this expression into Eq. (33), we come to Student noise distribution:

| (34) |

Using this distribution function, we finally get

| (35) |

where is the parabolic cylinder function. The central part of this distribution has exponential shape (24), while its tale has power dependence:

| (36) |

with the tail exponent , well outside the stable Lévy range (). One can show, that this exponent does not depend on relation between weights and in Eq. (32) for Markovian noise. But in the absence of noise correlations, , we get the effective exponent .

If we take into account correlations between the noise and the amplitude (see Eq. (25) and discussion therein), , and after some calculations we get simple expression for PDF:

| (39) |

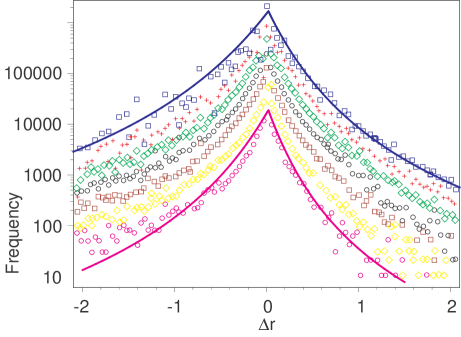

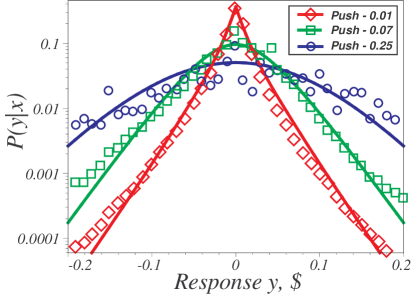

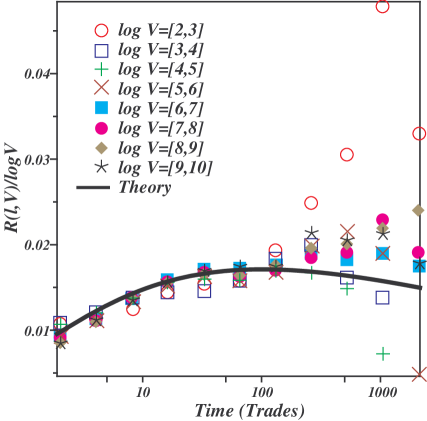

where functions and are defined in Eqs. (26) and (35), and are given in Eq. (27). We show in Fig. 4 that Eq. (39) with allows to explain both the asymmetry and the shape of empirical PDF for different size groups. The size dependence of both Fig. 3 and Fig. 4 follows Eq. (12) with exponent and universal .

Now we study the stability of the exponent for different time periods . The total increment for two joint intervals is the sum of corresponding increments for each of these intervals. Since the amplitude in Eq. (19) slowly varies on the time scale , we take it the same for both intervals, , and so the noise is proportional to the sum of noises for these intervals. Each of can be represented in the form of Eq. (29), and corresponding dispersions and depend on the same (but shifted over time) series of Gaussian variables , Eq. (32). Calculating the distribution function of the sum , we find

| (40) | ||||

where

| (41) |

The tail of the distribution (40) is determined by small , corresponding to large . As the result we find, that the distribution for the time interval is characterized by the same exponent , as each of for the time interval . The only difference is that this asymptotic behavior can be reached at larger , with respect to the distribution function of .

This observation explains why the fat tail in Fig. 3 for five year period is shifted to higher , with respect to Fig. 4 for one year period data. Experimental observation of the stability of the exponent for widely different economies, as well as for different time periodsSGPS-02 , gives strong experimental support of our theory. The stability originates in nonlinear correlations of the noise, see Eq. (29), while linear correlations vanish, . To demonstrate the importance of such correlations, assume, that the noise has tail exponent , and is uncorrelated at neighboring intervals . Than the exponent of for the interval is equal , and not , as follows from our model.

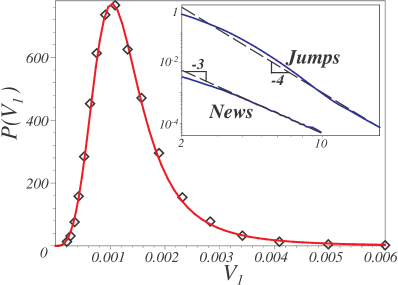

The systematic study of the distribution of annual growth rates by industry was performed in Ref. TeAx-SB-05 using Census U.S. data. It is shown, that all sectors but finance can be fitted by exponential distribution (24). We checked the data for finance sector, and show that they can be well fitted by Eq. (35) with exponent .

II.4 Main results

In this section we considered evolution of the market as the result of competition of different firms for external resources, by analogy with coalescent regime in physics of supersaturated solutions. This analogy allows to find informational entropy of the market, and prove the principle of maximum entropy.

We demonstrate that in coalescent regime for Gibrat mechanism of firm growing the distribution of firms over their sizes follows the Pareto power low with the exponent (Zipf distribution). Taking into account size effects, it turns to stretched exponent distribution, which also describes different processes, related to competition of units for common resources. Coalescent mechanism is also responsible for observable exponential distribution of the income between individuals. The production of real firms can be taken into account by vector models, by analogy with multicomponent solutions.

We propose the theory of market fluctuations, based on separation of all degrees of freedom of the market into cold and hot ones. For Gaussian statistics of all degrees of freedom such separation leads to experimentally observable exponential PDF of firm grow rates. We also prove, that this distribution has power tail with universal stable exponent .

We find analytical expression for PDF, and show, that it reproduces observable shape and asymmetry of the distribution of firm grow rates, which is related to existing anticorrelations between tactics of firms at short-time horizon and their strategy at long-time horizon. In next section we apply this approach to study price fluctuations on financial markets.

III Financial market

Dynamics of fluctuations is determined by the spectrum of relaxation times of the system. When all times are small with respect to the observation time interval , the state of the market at time depends only on its state at previous time , and dynamics is Markovian random process. Short-range correlations of price fluctuations on the market can be studied using stochastic volatility modelsARCH , but in order to describe real markets with multi-time dynamics, the model should take infinite-range correlations into accountBoBo-05 , and has “infinite” number of correction terms. In addition, to take empirically observable excess of volatility into account, one has to go at the boundary of stability of such models.

The real market has enormous number of (quasi-) equilibrium states and extremely wide spectrum of relaxation times, by analogy with turbulenceTurbul and glasses. Multifractal properties of time series can be described by phenomenological Multifractal Random Walk modelMRW . Although this model well characterizes scaling behavior of price fluctuations, it can not capture correlations at neighboring time intervals, which determine “conditional dynamics of the market” and can be described by the bivariate probability distribution of price incrementsMaHu-04 .

In previous section II.3 we show, that the increment of the random value of the time series

| (42) |

has the form of scalar product of two-component random vectors – the noise and its amplitude :

| (43) |

Hot variables vary at the scale small with respect to , while characteristic times of cold variables are large with respect to . The time plays the role of the effective temperature: at minimal trade-by-trade time, , the price is almost frozen, while in the opposite limit it has random walk statistics. In the intermediate time interval (of many decades) the market has “restricted” ergodicity: only hot degrees of freedom are exited, while cold degrees of freedom are frozen and determine the amplitude of price fluctuations.

Here we apply this approach to calculate PDF of price increments, as well as various conditional distributions and their moments. The dependence of parameters of these distributions on observation time will be studied later, in section IV. In section III.1 we introduce hot and cold degrees of freedom of the market. Two simplified models are formulated and solved in sections III.2 and III.3. “Markovian” model takes short-time correlations into account and neglects the effect of long-time challenges. “Effective market” model captures such effects, but neglects any short-time correlations because of trader activity. Although both these models capture essential part of observable phenomenons of price fluctuations (extremely small linear correlations – the Bachelier’s first law, “dependence-induced volatility smile”, “compass rose” patternCL-96 and so on), they can not describe all the variety of such “stylized facts”Styl .

In section III.4 we introduce Double Gaussian model, that takes all correlation effects into account, and show that it allows to explain the behavior of different types of stocksLe3-06 . Analytical solution of this model is derived in Appendix D. We demonstrate, that this solution reproduces all observable types of “market mill” patterns and gives the mysterious -shaped response of the market for all kinds of asymmetry of bivariate PDF, as well as other fine characteristics of this distribution. We also show that our theory allows to explain empirically observable Markovian “double dynamics” of signs of returns on the marketBoMa-06 .

III.1 Cold and hot degrees of freedom

The idea of hot and cold degrees of freedom of the market is qualitatively supported by empirical observations: It is shown in Ref. LM-01 , that the amplitude of fluctuations for ensemble (quenched) averaging significantly exceeds the amplitude of fluctuations for time (annealed) averaging. This observation can be interpreted as the result of the presence of cold degrees of freedom, which remain “frozen” when considering time fluctuations of hot degrees of freedom. In the case of ensemble averaging such cold degrees of freedom become “unfrozen”, increasing the amplitude of price fluctuations with respect to its time average value.

Following Ref. Le2-06 consider two consecutive price increments, (push) and (response) for the time intervals :

According to Eq. 43 price increments can be written in the form of the scalar products:

| (44) |

of complex noises and complex amplitudes . Complex random walk in the “tactic” space describes “impatient” agents. Complex random walk in the “strategy” space can be thought of as a result of slow variation of composition of the population of such agents on the market, as well as the activity of “patient” agents.

Moduli of complex variables and are normalized as:

| (45) |

is the dispersion of price fluctuations

| (46) |

Eqs. (44) are invariant with respect to “gauge” transformation of noise and amplitude variables, Eq. (21).

We will characterize correlations of price increments by uni- and bivariate PDFs:

| (47) | ||||

| (48) |

Using exponential representation of -function, these expressions can be rewritten in the form

| (49) | ||||

| (50) |

where is the Fourier component of PDF

| (51) |

The variable may be interpreted as the response on initial push , which is characterized by conditional PDF

| (52) |

The average conditional response is

| (53) | ||||

The width of the conditional PDF is characterized by the conditional mean-square deviation

| (54) | ||||

Large correspond to a large variety of the behaviors, the “volatility”. The dependence of on reflects the volatility clustering: should not depend of if there is no volatility clustering.

III.2 Markovian model

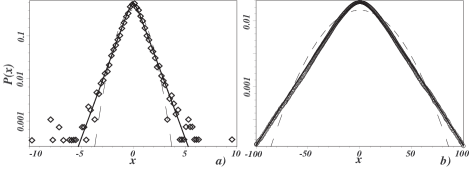

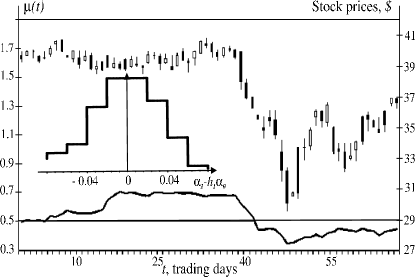

We first consider the case when the amplitude is not correlated with external challenges at strategy horizons, and for two neighboring time intervals. We also assume that the noise is not correlated with the amplitude, but take into account short range correlations of the noise, . For this Markovian model we find Eq. 35 for the probability distribution, which describes very well Russian financial market for , see Fig. 5.

For Gaussian noise we find exponential PDF (24) of price fluctuations, which is really observed for high frequency fluctuationsSPY-04 .

Averaging the Fourier component of PDF (51) over fluctuations of Gaussian amplitude and noise we find . Calculating the Fourier transformation of this function (50), we get the distribution function

| (55) |

where is the Bessel function. Calculating the integral (53) with function (55), we find the conditional response

| (56) |

Linear dependence (56) with well agrees with data for Russian market, what can be interpreted as indication that Russian investors are oriented only on current benefits, mostly ignoring opening possibilities at strategy horizons. Although linear response (56) is typical for ACOR group of stocks with (according to classification of Ref. Le3-06 ), this model can not describe essentially nonlinear response of other groups of stocks.

III.3 Effective market model

In general, the amplitude is varied in response to unpredictable external challenges. We first study this effect in the model of “Effective market”, neglecting correlations between noise in two consecutive time intervals , but taking into account random variations of its amplitude :

| (57) |

where is dimensionless correlation parameter, . As in Markovian model we ignore (anti)correlations between noise and amplitude. Correlations of the noise are induced by trader activity, while the change of a stock price in the model of Effective market is determined only by an external information, which may be considered as uncorrelated random process.

PDF of this model is proportional to the parabolic cylinder function with power tail exponent (see Eq. (36)). Non Gaussian character of the noise PDF can be ignored when considering the central parts of price distributions, when takes exponential form (24). In order to calculate bivariate PDF, we substitute equation (44) in (51) and perform the averaging over fluctuations of Gaussian variables :

| (58) |

The averaging over noise is performed with Gaussian PDF (23), and the integral over and in expression (50) is calculated expanding the function in powers of :

| (59) |

Here is given by Eq. (24), and functions are defined by:

| (60) |

PDF is symmetrical with respect to independent transformations of its variables, , and also with respect to time reversal transformation, which corresponds to push-response interchange, . This function is not analytical in origin, and the geometry of equiprobability levels can be approximated by , where near origin and far away from it.

Profiles of conditional distribution (52) are shown for different in Fig. 6. With the rise of the push the response becomes more flat in origin, in good agreement with empirical data. Slight deviations between the theory and data at large are related to non-Gaussian character of the noise (leading to power tail), see Eq. 35 for more details. Calculating integral (54) in the case of Gaussian noise, we get the conditional mean-square deviation,

| (61) |

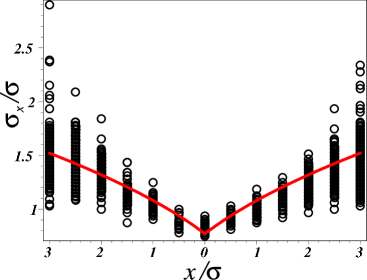

This function is plotted in Fig. 7. It demonstrates the so called “dependence-induced volatility smile” (“D”– smile), well known from empirical dataLeTr-06 . At small the standard deviation of the response (61) is smaller than the unconditional standard deviation , while at large it is larger.

The shape of conditional PDF can also be characterizes by the kurtosis, proportional to fourth momentum. One can show that, in agreement with empirical data, the kurtosis of theoretical conditional PDF decreases with the rise of . We conclude, that Effective market model captures main features of the market behavior, but it is enable to describe finite response of real stocks.

III.4 Double Gaussian model

In this section we generalize Effective market model to take into account short-range correlations at strategy horizon because of activity of traders. Such correlations lead to the exponent of the power tail of PDF (section II.3.4), and relatively weakly affects the central part of PDF: for time interval about several minutes it is estimated as about Le2-06 . We assume normal distribution of noise fluctuations for the central part of PDF, and neglect the effect of noise-amplitude anticorrelations, which is small at short , and leads to gain/loss asymmetry (see section III.4.4).

For given noise variables we introduce random variables of Effective market model, which form orthogonal basis in the space of random functions , see Eq. (57). Expanding price fluctuations and over this basis, we get:

| (62) | ||||

| (63) |

We consider amplitudes of Effective market as Gaussian random variables, Eq. (57). Non-diagonal amplitudes describe the shift of equilibrium on the market because of trader activity. Since there are only two independent amplitudes, and , for two time intervals, the amplitudes and , can be expanded over two diagonal amplitudes and :

| (64) |

In the case or this Double Gaussian model is reduced to Markovian model (section III.2), and in the case – to the model of Effective market (section III.3).

PDF of this model is calculated in Appendix D:

| (65) |

where is PDF of Effective market model, Eq. (59). The distribution (65) depends on only four independent parameters: the dispersion , the correlator of the amplitude (), and two angles and , depending on starting parameters of our model. The correlator describes the “elasticity” of the market to external challenges at the strategy horizon. The angles and control the feedback between trader expectations and real price changes at the tactic horizon. Their difference, , is taken as small parameter of our theory, which controls the correlator of neighboring price increments

| (66) |

Eq. (65) turns to corresponding expression (55) for Markovian model in the limit , and reproduces Eq. (59) of Effective market model for .

The sum (59) goes only over even because of neglect of noise-amplitude correlations, . In general, there are correlations between noise and amplitude, described by a factor (see section II.3.3). Such correlations (studied in section III.4.4) break the symmetry of the conditional average with respect to positive and negative , and are responsible for the so called Leverage effectLeverage .

In our theory we have an hierarchy of small parameters, . PDF of Double Gaussian model with all nonzero has no symmetries at all. In the case but there is a symmetry , corresponding to rotations on the angle in the plane . In the case but , when there are no linear correlations of price (66) at adjacent time intervals, PDF (59) remains symmetrical only with respect to mixed transformation, , corresponding to rotations by the angle in the plane . The change of sign of in the above equation is related to reversion of the time: on reversed time scale one can think about losses in future, , as about gains in the “past”. This approximate push-response invariance was established first time from the analysis of empirical dataLe1-06 . And finally, in the case the function acquires the total symmetry and of Effective Market model.

III.4.1 Market MILL, ACOR and COR stocks

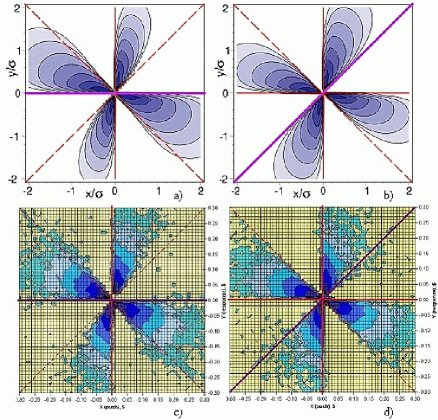

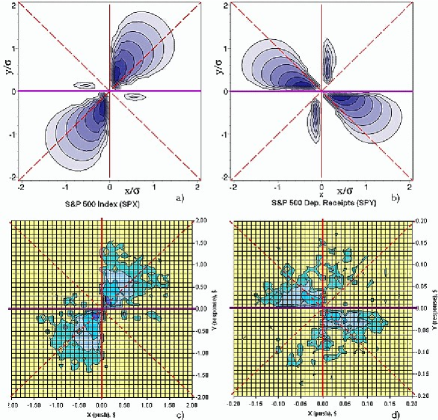

It is convenient to describe the symmetry of PDF with respect to the axes by antisymmetric component, . In Fig. 8 a) we plot equiprobability levels of positive part of this function, .

For small the plot demonstrates four–blade mill–like pattern (the “market mill” pattern), that was observed first time in Ref. LeTr-06 , see Fig. 8 c). To analyze these pictures it is convenient to divide the push-response plane into sectors numbered counterclockwise from I to VIII. In agreement with empirical data at the blades in II and IV quadrants of the plane are thinner than their counterparts, which extend out of I and III quadrants. The situation is reversed at . With the rise of the market mill pattern becomes distorted and only two corresponding blades of the mill pattern left well expressed.

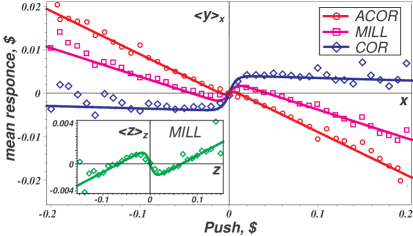

In Figs. 9 a) and b) we show how the market mill pattern is deformed with variation of . Varying the angle for fixed and , we get good qualitative agreement with observable patterns, shown in Figs. 9 c) and d). We conclude that the theory allows to explain all the variety of basic patterns for different stocksLe3-06 , and may be considered as the basis for their quantitative classification: Fig. 8 with () corresponds to the mill pattern (MILL), Fig. 9 a) with () corresponds to negative autocorrelation (ACOR), and Fig. 9 b) with () corresponds to positive autocorrelation (COR). Anti-mill pattern (AMILL) with was never observed in Ref.Le3-06 .

Similar patterns are obtained for symmetry properties of the bivariate PDF with respect to different axes , or . As example we show in Fig. 8 b) equiprobability levels of positive part of the function . The blades of this market mill are more symmetric than those in Fig. 8 a), in agreement with empirical pictures in Figs. 8 c) and d).

An attempt to explain market mill patterns for the asymmetry with respect to the axis was made in Ref.Le-07 , where “hand-made” analytical ansatz for conditional PDF was proposed. It was explicitly assumed, that the response depends only on push at previous time, and no long-range correlations were taken into account. We do not think, that such Markovian model can give adequate description of real market with extremely wide spectrum of relaxation times.

III.4.2 Univariate PDF

Now we calculate one-point PDF, Eq. (49), of Double Gaussian model. Expression (153) of Appendix D for the Fourier component can be represented in the form

| (67) | ||||

with the angle defined by

| (68) |

Calculating the integral over in Eq. (52) with this function we find one-point PDF

| (69) |

As one can see from Fig. 10 this distribution is in good agreement with observable PDF of the Standard&Poor 500 (S&P500) index, that is one of the most widely used benchmarks for U.S. equity performance.

III.4.3 Conditional response

Calculating the integral (53), we find the mean conditional response

| (70) |

where , and are defined in Eqs. (67) and (68). In Fig. 11 a) we show how the dependence (70) of mean conditional response on push depends on the angle . This dependence has zigzag structure for MILL group (), it is almost monotonic for ACOR group (), with linear limiting dependence (56)), and is essentially nonlinear for COR group (). Similar calculations of conditional mean absolute response (which shows how the response volatility is grow with the amplitude of the given push ) show that in the case to a good accuracy it is linear in the absolute value of the push , , in good agreement with empirical dataLe1-06 .

To analyze the asymmetry of PDF with respect to time reversion in the case of MILL group (), it is convenient to introduce the total increment of price during the two time intervals, and also the difference of these increments and . PDF of these random variables takes the form of Eq. (65) with the substitution , describing the rotation of the push-response plane by the angle . Therefore, both PDF and all conditional averages are given by above expressions under the substitution and , where

Conditional response also has -shaped structure, and it is shown in Insert in Fig. 11 in comparison with empirical data.

Nonvanishing of average responses and (Fig. 11) allows one to make some “nonlinear” predictions (70) about future price changes on the market, which can not be obtained from the knowledge of only linear correlations: the response in the next time interval is correlated with initial increment of the price at small , and is anticorrelated with it at large . The order of price increments is also important for given total increment : for small the average initial variation is larger than next one, , and the situation is reverted at large .

III.4.4 Conditional double dynamics

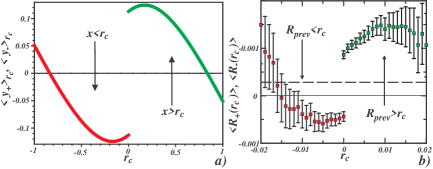

In this section we discuss the hypothesis of Ref.BoMa-06 , that the average return is actually the result of composition of two independent signals with Markovian statistics: one of them positive, and another one negative. It is proposed to characterize this effect by average daily returns and given that the previous day had a return greater than and smaller than :

| (71) | ||||

| (72) |

Calculating integrals (71) and (72) for Double Gaussian model in MILL case , we find at :

| (73) |

This function is shown in Fig. 12 in line with empirical data. As one can expect from Fig. 12 a) the average response is correlated with at small and is anticorrelated with it at larger . We added horizontal dotted line in Fig. 12 b), shifting the -axis by unconditional average returnBoMa-06 . This shift and remaining difference in shape between Figs. 12 a) and b) is related to the buy/sale asymmetry, discussed below.

At the average daily return for given sign of the previous day return is finite, reproducing the effect of “double dynamics” of the market, attributed in Ref.BoMa-06 to “propagation” of two independent signals in “Markovian” market.

In fact, the market is not Markovian, but the sign of price increments is determined only by the noise . Markovian “double dynamics” of signs is direct consequence of Markovian statistics of noise correlations, see section II.3.4. Anticorrelations between the noise and the amplitude are responsible for small systematic trend of the price, (28), reproducing empirical dataBoMa-06 for . This positive trend leads to corresponding increase of the probability to have positive price increment, with . Conditional probabilities of the two-state modelBoMa-06 can be expressed through the angle , which determines the amplitude of the response on previous price increment ():

Empirical observation of “double dynamics” may be considered as direct confirmation of Markovian statistics of noise fluctuations, but not of the whole market, as conjectured in Ref.BoMa-06 . We show in section IV.3.7, that multifractal evolution of the amplitude is strongly non-Markovian. But consideration of only signs of returns “erases” information about the amplitude from the time series.

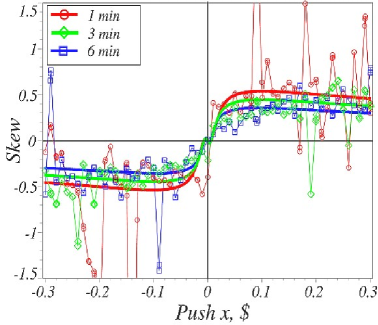

III.4.5 Skewness

Asymmetry of the conditional distribution with respect to the average (53) is characterized by the skewness of the conditional response:

The conditional mean-square deviation is defined in Eq. (54). Positive value of indicates that only few agents perform great profits, while many of them have small losses with respect to the mean. A negative describes a complementary case. As one can see from Fig. 13, the skewness has the sign of initial push in accordance with the empirical dependence. Notice that although the skewness is very sensitive characteristic of PDF, our theory reproduces both observed shape and values of .

In this section we show, that separation of hot and cold degrees of freedoms allows to reproduce numerous empirical data, known for high-frequency fluctuations on financial markets. For Gaussian statistics of all degrees of freedom this model captures main features of all groups of stocks, including “market mill” patterns, “dependence-induced volatility smile”, -shaped response function and so on. Correlations between hot and cold variables are responsible for observable double dynamics of the market, mixing propagating signals of opposite signs and providing systematic positive trend of prices.

III.5 Results and restrictions

In this section we demonstrate, that the idea of hot and cold variables allows to capture main features of price fluctuations, which can be described by Double Gaussian model – a generalization of the random walk model for the case of multiscale fluctuations. For different sets of parameters the analytical solution of this model reproduces the behavior of all kinds of stocks on financial market, as well as the market as a whole.

Consider some restrictions of this approach. Using coarse-grained description of price fluctuations at times min we loose information about sale/buy mechanismsRo-01 ; WeRo-03 . This knowledge (see, for example, Minority and Majority GamesMinor ) is important to derive parameters of our models for particular markets. We also considered only uni- and bivariate distribution functions, while market dynamics is described by the whole family of -point correlation functions. In next section we present alternative description of the market at different time scales using ideas of renormalization group approach.

IV Multiscale dynamics of the market

Standard thermodynamics can describe only ergodic systems, while the market is the system with “restricted ergodicity”: during the time it can explore only small part of the total configuration space near current local equilibrium. Increasing the time , this equilibrium is shifted because of long-time variations. The resulting multi-time dynamics of fluctuations on the market is not ergodic, and can only be described by continuous set of Langevin or Fokker-Planck-type equations for all time scales.

Note, that this is not exclusive, but standard behavior of complex physical systems. As we will show, different local equilibriums on the market are organized into tree cascades (“self-organized criticality”), by analogy with “hot spots” in Quantum ChromodynamicsQCD , and dynamics of unergodic spin-glasses, which is government by continuous set of Fokker-Planck equationsSG . Continuous set of equilibriums was also predicted for incomplete marketsBC-89 .

The behavior of the market at the trade by trade level was studied in many detailsBiHiSp-95 ; BoMePo-02 ; MaMi-01 . At larger times collective effects become important, and financial time series display long-time nonlinear correlationsMa-St-99 ; DaGeMu-01 ; Co-01 , which puzzle many researchersBoCo-98 ; Interm ; KrHoHe-02 . Different models have been proposed in order to reproduce some “stylized facts”Styl of empirical time series. Lévy flight processesLevi were used to model jumping character of price variations. Volatility (the amplitude of fluctuations) clustering effects have been studied in frameworks of stochastic volatility modelsTa-86 and GARCH-type modelsGARCH . Mixed effect of jumps and stochastic volatility was taken into account in some modelsCGM-03 . A key to study multiscale properties of price fluctuations is provided by phenomenological multifractal models, see Refs. CaFi-04 ; FiCaMa-97 . Renormgroup approach, describing evolution of multiscale systems, was first proposed for glass systemsRenorm ; Do-85 , and in present work we extend it to the market.

The key question is the source of price fluctuations. Assumption about totally random activity of tradersBaPaSh-97-Ph ; DaFaIo-03 leads to Brownian motion of prices. Although random trading model predicts many qualitative and quantitative properties of the order booksBoMePo-02 ; SmFaGi , it can not describe existing correlations in price fluctuations. An alternative “efficient market hypothesis” assumes, that the price can be changed only because of unanticipated and totally unpredictable news. This hypothesis lays in the basis of the model of fully rational agentsFa-70 , which also predicts Brownian walk statistics of prices. Observed volatility of the market is too high to be compatible with the idea of fully rational pricingSc-AER-81 , and can only be reproduced by introducing an artificial random source – “sunspots”CS-83 . In addition, the analysis of Ref.GLGB-08 shows, that most of large fluctuations in the market are due to trading activity, independently of real news.

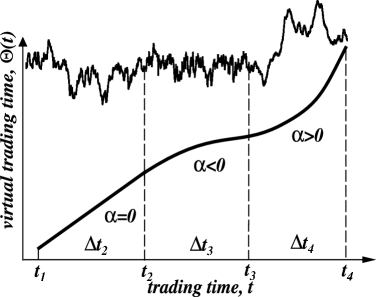

The main idea of this paper is that market activity can be described as random trading at all time horizons from a minute to tenths years. The market tends to reach equilibriums on extremely wide baseband of time scales, and all these equilibriums are continuously changed both because of long-time modes and external events. Multiple local equilibriums can be represented by an hierarchical tree, see Fig. 14. Each generation of this tree is characterized by its relaxation time . For any observation time interval , all states with times smaller than are in equilibrium, and fluctuations near this equilibrium are described by hot degrees of freedoms. The states with times larger are frozen, and are described by cold degrees of freedom.

In this section we derive an analog of renormgroup equations for the market, which relate fluctuations at different coarse grained time scales . With decrease of the time interval , which can be thought of as effective temperature, the market experiences a cascade of dynamic phase transitions of broken ergodicity, when some hot degrees of freedom become frozen. This cascade can be graphically shown as the hierarchical tree, each branching point of which represents “phase transition” to a state with frozen degrees of freedom with relaxation times , see Fig. 14. We show in section IV.1.1, that the topology of this tree reflects ultrametricity of the time “space”.

In section IV.1.2 we demonstrate, that fluctuations at given time scale are determined by contributions of all “parent” time scales of the hierarchical tree in Fig. 14, what is the reason of non-Markovian dynamics of the market. Cumulative contribution of all time scales allows to explain extremely high volatility of the market (section IV.2.1), and is responsible for power low decay of correlation functions (section IV.3.1) and their multifractal properties. In section IV.3.1 we formulate self-consistency condition, under which the hierarchical tree in Fig. 14 describes coarse-graining dynamics at all levels of the coarse graining time , and find the -dependence of parameters of our Double Gaussian model, section III.4.

In section IV.3.3 we derive a set of Langevin equations, describing dynamics of the market with extremely wide range of characteristic times – from minute to tenths years, and calculate the price shift in the response on imbalance of trading volumes (section IV.3.4).

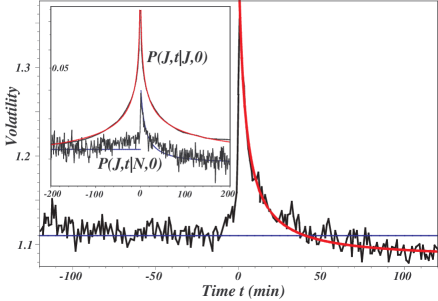

We also calculate PDF of volatility (section IV.3.5) and show, that it has fat tail with stable exponent for stock jumps and for news jumps. We derive, that coarse grained dynamics of the market can be reduced to the multifractal random walk modelMuDeBa-00 ; BaDeMu-01 , which determines multifractal properties of price fluctuations, related to the ultrametric structure of the tree in Fig. 14. We calculate volatility patters after news and stock jumps, and find their conditional probabilities. In section IV.3.6 we show, that the price behaves as fractional Brownian motion. We demonstrate in section IV.3.7, that Brownian motion, sub- and super-diffisive regimes change each other at the long-time scale. The knowledge of history can be used to estimate the tendency and risks of future price variations.

Main results of this section are summarized in section IV.4. In Appendix E we show details of calculations of the volatility distribution.

IV.1 Renormalization group transformation

Consider statistics of price increments (returns)

| (74) |

as the function of the coarse-graining time interval . Here is the price or its logarithm at time . For definiteness sake, we consider only ACOR group of stocksLe3-06 , when can be represented as scalar product of complex amplitude and complex noise , Eq. (43). By analogy with renormgroup consideration, cold variable slowly varies at time scale , while hot variable quickly fluctuates at this scale, see Fig. 14 a).

IV.1.1 Ultrametricity and restricted ergodicity

In order to establish an analog of renormgroup transformation for the market we first introduce corresponding partitioning of the time “space”. At elementary step of the renormgroup each “parent” interval of time axis can be divided into “child” time interval , see Fig. 14 b). Repeating such division, we arrive to the hierarchical tree with functionality , shown schematically in Fig. 14 c). For this tree the time

| (75) |

depends exponentially on the current rank , is maximal relaxation time. Minimal time ( is the number of generations of the tree) is about average time between trades. Typically, is about several years and is about minute for liquid markets, and so .

We define the “distance” between events at times and by the condition :

| (76) |

which can be identified with the distance (number of generations) along the tree in Fig. 14 c) between these points. One can show, that for three different times

and, therefore, the metric (76) generates ultrametric time “space” (with only isosceles and equilateral triangles), which can be really mapped to the tree. For example, in Fig. 14 c) the distance between points and is , , and .

Note, that Eq. (75) gives standard relation between time scales of discrete wavelet transformation. The tree in Fig. 14 can be thought of as a skeleton of the wavelet transformation of time series. We turn to wavelet interpretation of our approach in section IV.3.3.

Each of horizontal levels at the time on the tree in Fig. 14 c) corresponds to course-grained description of fluctuations at the time scale . Hot degrees of freedom are “melted”, and described by complex noise with continuum spectrum of relaxation times extended from through . Cold degrees of freedom are characterized by complex amplitude of the noise, which is frozen at the time , see Eq. (43).

By analogy with glasses, the states of real market are highly degenerated, what is reflected in the presence of gauge transformation (21) of complex noise and amplitude variables, which do not affect price variations , Eq. (43). The degeneracy is the reason of high sensibility of the market to external events. Recall, that in spin glasses any observable are not affected by “non-serious” part of disorder, which can be removed by gauge transformation of glass degrees of freedoms.

Following this analogy, the time plays the role of the temperature . With decrease of the temperature from the market experiences a cascade of dynamic phase transitions of broken ergodicity, when some hot degrees of freedom become frozen (the system is unergodic if its fluctuations can not explore the whole configuration space). This cascade proceeds continuously down to the time , and can be graphically shown as hierarchical tree, each branching point of which represents phase transition to a state with frozen degrees of freedom with relaxation times , see Fig. 14. The parameter determines the probabilities of such transitions, which are relatively rare for real markets.

In this sense at any the market is just at the point of dynamic phase transition of broken ergodicity, and has, therefore, increased amplitude of fluctuations – the volatility. This observation supports the idea that the market is always operating at a critical point as the result of competition between two populations of traders: “liquidity providers”, and “liquidity takers”Bo-Ch-05 ; Bak . Liquidity providers correspond to hot degrees of freedom, creating antipersistence in price changes, whereas liquidity takers correspond to cold degrees of freedom, and they lead to the long range persistence in prices.

Since such separation of the market into hot and cold degrees of freedom takes place at any time scale, , there could not be any unique classification of traders, which can be divided also into “positive feedback” traders and “fundamentalists”Positive , “contrarian” traders and “trend followers”Ma-01 and so on. There is, however, important difference between market and spin-glass hierarchical trees: while the states of the glass are not ordered, there is strong time ordering of all “points” of the market tree at any level of the hierarchy.

IV.1.2 Recurrence relation

General recurrence relation between amplitudes and at levels and of the hierarchical tree can be written through the random transition matrix :

| (77) |

In general, there could be a term in the rhs of this equation, but it is not invariant with respect to gauge transformation, Eq. (21), and should be dropped. The term describes the inheritance of the amplitude of the “parent” levels of the hierarchy, and gives the contribution of “newborn” during the transition unfrozen degrees of freedom to the “child” amplitude .

The recurrence relation (77) can also be rewritten in the multiplicative form, introducing relative increment :

| (78) |

Random variables and () are determined by degrees of freedom with characteristic times , while is formed by degrees of freedom with times larger . Assuming independence of fluctuations of different time scales, do not depend on and . We estimate the mean squared amplitudes of fluctuations of and as

| (79) |

There is important difference of Eq. (79) from the case of usual diffusion, when is the consequence of independence of fluctuations at different times . In contrast, diffusion-like dependence (79) with effective coefficient is the consequence of independence of fluctuations of different time scales . The time -dependence of price fluctuations is strongly non-diffusive.

IV.2 Amplitude of fluctuations

IV.2.1 Excess of volatility

In the mean field approximation we neglect fluctuations of , and find the solution of Eq. (77) in the form of the sum of independent random signals from time intervals , obtained by multiplicative merging of previous time intervals :

| (80) |

Weights of these signals exponentially fall with the distance in time hierarchy from the current rank . Simulated time series (80) for the amplitude in the model with random are shown in Insert in Fig. 15. This picture demonstrates multiscale character of resulting price fluctuations.

Averaging the square of the recurrence relation (77), we find difference equation

| (81) |

for the dispersion of the amplitude , which has the solution

| (82) |

where is the constant of integration and is the effective diffusion coefficient:

| (83) |

From Eqs. (82) and (75) we find the dependence of the dispersion of price increments on the coarse-graining time :

| (84) |

The dependence (84) for different stocks is in good agreement with empirical data, see Fig. 15. Although at small ,

| (85) |

it looks like diffusion with apparent diffusion coefficient (83), price fluctuations do not really have diffusive behavior. As the sign of it, the amplitude of price fluctuations is anomalously large due to the presence of a big prefactor for in Eq. (83). It was shown by SchillerSh-00 , that even accounting the volatility of dividendsSh-81 leaves the empirical volatility at least a factor too large with respect to the random walk model. Such anomalous “excess of volatility”, , originates from the superposition of signals from all time scales, see Eq. (80). Similar effect (by 10 orders of value) is well known in spin glasses, where the parameter in Eq. (76) is extremely small.

IV.2.2 Cross-over time and Hurst exponents

The term in Eq. (84) appears as a constant of integration of the recurrence equation (81), which is determined by the “boundary condition” at trading time . Therefore, is not universal and determined by microstructure of the market.

At small the first term in Eq. (84) gives the main contribution, , with effective Hurst exponent close to . At large the second term in Eq. (84) gives dominating contribution to the Hurst exponent:

| (87) |

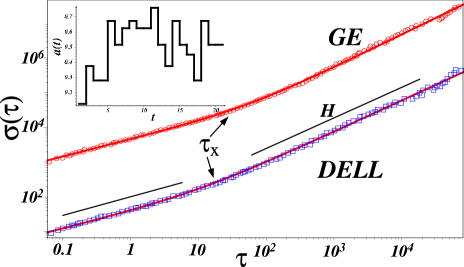

Such behavior with different exponents at and was really observed for S&P 500 stock index (1984-1996)LGCMPS-99 with different values of the cross-over time for individual companies, see Fig. 15.

The removalLGCMPS-99 of the largest 5 and 10% events kills correlations of the noise at small time scales, reducing the constant . According to the prediction (85) of our theory, it shifts to lower values, and strongly increases . Excluding the shift of from variations of both and , we find linear relation between two these shifts: . Comparison with empirical dataLGCMPS-99 gives the estimation , in good agreement with observable exponent for the regime , see Eq. (87). Similar behavior is observed for different stocks with typical transition times about several days.

IV.2.3 Parameters of Double Gaussian model

Let us show, that in order to represent coarse grained dynamics of price fluctuations for the time interval , noise variables at different “child” subintervals of the same “parent” interval should be (anti)correlated. According to the idea of the coarse grained description, the price increments for the time interval is the sum

| (88) |

of price increments for all adjacent time intervals . Substituting Eq. (43) into Eq. (88), this last equation can be rewritten in the form

| (89) |

where we substituted Eq. (77) for the amplitude to the right hand side of Eq. (89). Calculating the average (both quenched and annealed) of the square of this equation, we find the self-consistency equation

where is the noise correlator at neighboring time intervals,

Substituting here (82) with we find in the case

This value is always negative and small at .

IV.2.4 Time and size dependence of fluctuations

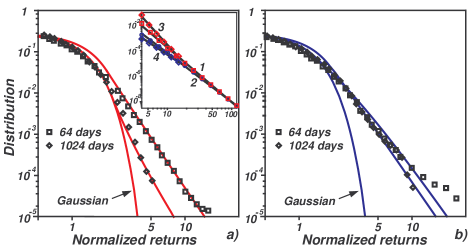

The effect of noise/amplitude anticorrelations, studied in section II.3.4, is small in the parameter , and leads to the asymmetry of the tails of probability distributions (see Fig. 4), observed for PDF of individual companies in Ref.PGMNS-99 . It is also responsible for different apparent exponents for positive () and negative () power tails. This effect is illustrated in Insert in Fig. 16, where we show, that the function at is indistinguishable at about two decades in from power tails with exponents and . Increasing leads to larger deviations of these exponents from the universal value , see Insert.

Simple analytical expression for the whole distribution for general can be easily constructed by consecutive matching Gaussian, exponential and power distributions, , at some points and , respectively. The resulting expression well reproduces most of empirical data for PDF . Below we use this expression to explain main features of PDF at and :

We can estimate the effective exponents re-expanding about correlation induced systematic shift (see Eq. 28), and find near cross-over points . At small the central part of the distribution has exponential shape (26) with maximum at . Matching it at with power tails we find and , in good agreement with Ref.PGMNS-99 .

At large the central part has Gaussian shape. Matching it at with power tails, we get . With increase of (at ) Gaussian region of the positive distribution is progressively extended, while negative distribution remains fat-tailed, explaining corresponding mysterious behavior of empirical dataPGMNS-99 , see Fig. 16.

The size dependence of the volatility was studied for individual companies in Ref.PGMNS-99 . It is shown, that Eq. (13), , well describes the dependence of dispersion of returns on market capitalization. For day , while it gradually decreases with the rise of , approaching the value for days. This effect supports our self-similar model of companies (see section II.2.2), when the index is determined by the number of generations of the hierarchical tree. The effective number of tree generations logarithmically depends on relaxation time , Eq. (75), and for the dependence on can be approximated by

| (90) |

From equation we find that the Hurst exponent (87) should grow logarithmically,

with market capitalization , in good agreement with empirical dataEisler .

IV.3 Nonlinear dynamics of fluctuations

IV.3.1 Correlation functions: multifractality

From Eqs. (77) and (82) we find simple analytical expression for the correlation function of amplitudes:

| (91) |

where is the logarithmic distance (76) in the ultrametric space, see Fig. 14. Therefore, observed power autocorrelations in the time series are the consequence of the self-similiarity of the hierarchical tree in Fig. 14. Neglecting the term at large enough (small coarse-graining time ) in Eq. (91) we find that amplitude correlation function decays as the power of the time

Now consider fluctuations of the modulus of the amplitude . The solution of the multiplicative recurrent relation (78) for the coarse graining time is

| (92) |

From expansion (92) we find

| (93) |

with

where we expanded over irreducible correlators of , , and used Eq. (86) to find the linear in term. For Gaussian there are only two first terms in this expansion, and we get . We also find

In the case of Gaussian this gives us the generalized Hurst exponent , see also Ref.Sh-03 . The intermittence parameter characterizes the uncertainty on the market, and we expect, that is relatively large for emerging markets with large uncertainty, and small for well-developed markets (see section IV.3.3).

We conclude, that hierarchical structure of market times, see Fig. 14, generates multifractal time series with -dependent generalized Hurst exponent. The amplitude of fluctuations is randomly renewed with time : with the probability for the root of the hierarchical tree in Fig. 14, …, and with the probability for maximum rank of the tree. This random process generalizes the Markov-Switching Multi-Fractal processCaFi-04 with . The multiplier is renewed with probability exponentially depending on its rank within the hierarchy of multipliers.

IV.3.2 Volume statistics

In this section we introduce an analog of canonical action-angle variables, in which coarse-grained market dynamics can be described by a set of linear Langeven equations for all time scales in the market. The “thermodynamic force” of price variations is the imbalance of trading volumes, , which can be considered as random function of time (volume time series). The increment of the volume at the time interval can be written by analogy with price increment (Eq. 92) in the form:

| (94) |

Normalized random noise is proportional to the sign of the increment . Gaussian random variable slowly varies at the time scale , and can be expanded over modes covering the frequency band from to . Explicit expression for can be obtained expanding its variation over normalized wavelet functions with expansion coefficients ( describes regular trend):

| (95) |

Similar equations relate modes (92) with the volatility . In the case of random activity of traders at all time horizons should be considered as uncorrelated random values:

| (96) |

The noise function in Eq. (94) can be presented in the form , where is the phase of corresponding complex amplitude (see Eq. 43). Random function can be expanded over wavelet modes (Eq. 95). Assuming that corresponding expansion coefficients are independent random values at all time horizons,

| (97) |

we find:

Calculating the integral over we arrive to

| (98) |