Mathematical analysis of long tail economy using stochastic ranking processes

ABSTRACT

We present a new method of estimating the distribution of sales rates of, e.g., book titles at an online bookstore, from the time evolution of ranking data found at websites of the store. The method is based on new mathematical results on an infinite particle limit of the stochastic ranking process, and is suitable for quantitative studies of the long tail structure of online retails. We give an example of a fit to the actual data obtained from Amazon.co.jp, which gives the Pareto slope parameter of the distribution of sales rates of the book titles in the store.

Key words: long tail; online retail; internet bookstore; ranking; Pareto

JEL Classification: C02

1 Introduction.

Internet commerce has drastically increased product variety through low search and transaction costs and nearly unlimited inventory capacity. With this new possibility a theory [Anderson, 2006] has been advocated which claims that a huge number of poorly selling products (long tail products) that are now available on internet catalogs could make a significant contribution to the total sales. In this paper, we refer this theory as the possibility of long tail business.

In studying the possibilities of long tail business, we need a precise, quick, and costless quantitative method of analyzing the long tail structure, but there we encounter a problem. For example, online bookstores have millions of books on their electronic catalogues, but many of the books have average quarterly sales less than . This means that if we start collecting the sales record, we will end up, after waiting for months, with a list which has ten thousand lines with sale and another ten thousand with sale, and so on. Moreover, the result will not mean that a particular book with sale has a better potential sales ability than a book with sale: A problem characteristic of quantitative analysis of long tail business is, that for product items of low sales potentials, fluctuations dominate in the observed data. Even though we want to suppress fluctuations, since each item produces very little profit, we cannot afford to spend time and money in collecting extensive data over a long period required from the law of large numbers.

If we hope to estimate the total sales of a store, we could obtain it from an observation in a short period with less relative fluctuations, thanks to the law of large numbers. For a revenue officer, this may be sufficient. But for those who we are interested in the long tail business, for example, an executive running the online store or a stockholder waiting for disclosure, as well as an observer for research purpose, a detailed structure of the contribution of less sold items would be important. More specifically, we would like to know the distribution of sales potentials of the products at an online store, such as the ratios of the number of items with average sales rate below any given number. As discussed in the previous paragraph, extracting the average sales rate of an item would require a long time of observation. One would then consider observing sufficiently many items of relatively low sales and calculate an average, to suppress statistical fluctuation, but then one faces a problem of selecting product items of similar sales potential, and we come back to the problem of statistical fluctuation for the data on a single item in the long tail regime.

On web pages, various ranking data can be found. An example is the sales rankings of books at online bookstores such as Amazon.com. On the web page of each book, we see, as well as the title, price, and description of the book, a number ranging from 1 to several millions which indicates the book’s relative sales ranking at the online store. In this paper, based on the analysis of a mathematical model defined and studied in [K.&T. Hattori, 2008a, K.&T. Hattori, 2008b], we propose a new and simple method, using the ranking data, to overcome the problem of statistical fluctuations of the data on items with low sales potential. Our method allows us, by observing how the sales ranking of a single product develops with time, to reproduce the distribution of sales potentials of all the products sold at the online store, free of statistical fluctuations. Our theory could serve as an efficient and inexpensive method of a prompt analysis of long tail sales structure.

The plan of the paper is as follows. In Section 2 we review the model of stochastic ranking process, and explain the main theorems in [K.&T. Hattori, 2008a, K.&T. Hattori, 2008b]. To test the applicability of our theory in practical situations, we apply in Section 3 the formulas summarized in Section 2 to the rankings at Amazon.co.jp. In Section 4 we discuss further implications of the theory of the stochastic ranking process and possible implications of the results obtained at Amazon.co.jp.

2 Formulation.

In this section, we summarize the main results in [K.&T. Hattori, 2008a] on the stochastic ranking process. It is a simple model that describes the time development of sales rankings at online bookstores.

Consider a system of items (say, book titles), each of which has a ranking ranging from to so that no two items have the same ranking. Each item sells at random times. Every time (a copy of) an item sells, the item jumps to rank immediately. If its ranking was before the sale, all the items that had rank through just before the sale shift to rank through , respectively. Thus, the motion of an item’s ranking consists of jumps to the top and monotonous increase in the ranking number between its own sales, caused by the sales of numerous other items.

We prove that under appropriate assumptions, in the limit , the random motion of each item’s ranking between sales converges to a deterministic trajectory. This trajectory can actually be observed as the time-development of a book’s sales ranking at Amazon.co.jp’s website. Simple as our model is, its prediction fits well with observation and allows the estimation of the Pareto slope parameter. We also prove that the (random) empirical distribution of this system (sales rates and scaled rankings) converges to a deterministic time dependent distribution.

To formulate the model mathematically, let us introduce notations and state assumptions. Let be the labels that distinguish the items. We denote the sales ranking of item at time by , for . Assume that a set of initial rankings , satisfying for , and sales rates are given (non-random). Namely, items with various sales rates (selling well or poorly) start with these given initial rankings , and set out to motion according to their sales rates. Let and , , , be the -th sales time of item , which is a random variable. Assume that sales of different items occur independently, and furthermore, for each , the time interval between sales are independent and have an identical exponential distribution to that of given by

A property of exponential distributions implies that corresponds to the average number of sales per unit time. In the time interval the ranking increases by every time one of other items in the tail side of the sales ranking (i.e., with larger ) sells. Thus, the stochastic ranking process is defined as follows: for ,

-

(i)

-

(ii)

, ,

-

(iii)

for each and , if then , where means ‘just before’ time ,

-

(iv)

otherwise is constant in .

Since sales rankings are determined by random sales times, sales rankings are also random variables.

Let , where denotes the number of the elements of a set . is the number of the items which has sold at least once by time . Note that in the ranking queue of items, the item with rank marks a boundary; all the items with (‘higher’ rankings) has experienced a sale, while those with (‘lower’ rankings) have not sold at all by time .

We can also see , as the trajectory of the sales ranking of an item that started with rank 1 at time and has not sold by time . It is convenient to consider the scaled trajectory defined by , for it is confined in the finite interval . The scaled trajectory is random, but the following proposition shows that this random trajectory converges to a deterministic (non-random) one as .

Recall that item has sales rate . This determines the empirical distribution of sales rate as , where with denotes a unit distribution concentrated at . Namely, for any set ,

Proposition 1

Assume that the empirical distribution of sales rate converges as weakly to a distribution . Then

| (1) |

in probability, where

| (2) |

This proposition is a straightforward result of the law of large numbers. Intuitively, the stochastic process converges to the deterministic curve because a trajectory of an item between the point of its sales is determined by the independent sales of numerous others (towards the tail side of the book in observation in the ranking). The popularity of the observed book is reflected in the length of sojourn in the sequence before it makes next jump (i.e., ordered for sales.)

-

Remarks.

-

(i)

The random variable converges as to a deterministic quantity . It implies that if is large enough, the scaled trajectory provides us with fluctuation-free information. If we try to know the sales rate of each product by counting the sales for a certain period of time, we cannot avoid fluctuation. The more precise data we want, the more time is needed to count the sales, especially for items that rarely sell, say, once a month. This proposition ensures that by observing the time development of the sales ranking of a single item, we can reproduce the distribution of sales rates, free of statistical fluctuation.

-

(ii)

on the right-hand side of (2) is the Laplace transform of the distribution . There is a uniqueness theorem according to which the Laplace transform completely determines the distribution [Billingsley, 1995].

-

(i)

Intuitively, we can guess that near the top of the ranking, there are more items with large sales rates than in the tail regime. This intuition can be made mathematically precise and rigorous:

Theorem 2

Assume the following:

-

(1)

The combined empirical distribution of sales rate and the initial scaled sales rankings

converges as to a distribution on which is absolutely continuous with regard to the Lebesgue measure on .

-

(2)

D

-

(3)

.

Then the combined empirical distribution of sales rate and scaled rankings

converges as to a distribution which is absolutely continuous with regard to the Lebesgue measure on .

In particular, the ratio of items with and rankings in at time is given by

| (3) |

where is the inverse function of the strictly increasing continuous function :

| (4) |

and is the inverse function of , which is a strictly increasing continuous function of .

Furthermore, the trajectory , time-shifted by , converges as to given in Proposition 1 up to the next jump time ( ).

-

Remarks.

-

(i)

Assumption (1) says that in actual applications we are considering a long tail economy with a large number of items , and that we may regard the empirical distribution at the starting point of observation as a continuous distribution.

-

(ii)

Assumption (2) implies that all the items sell. With extra notations Theorem 2 essentially holds without Assumption (2), but we will keep it to avoid complications.

This assumption implies that is a strictly increasing function of , and the inverse function exists. Under Assumption (2), is a strictly increasing function of , thus the inverse exists.

-

(iii)

Assumption (3) assures the explicit form of the limit (3) in the following Theorem to hold also for . For the Theorem holds without Assumption (3). (Hence the only essential assumption is the Assumption (1).)

-

(iv)

The last statement in the Theorem implies that by observing the time development of the ranking of any single item from the moment of its sales point (), we can, by equating with (2), obtain the information on the distribution of sales potential , of all the items listed in the rankings.

-

(v)

This Theorem is mathematically nontrivial in the sense that a law of large numbers of ‘dependent’ random variable is the key to the proof.

It is also known that satisfies the following set of partial differential equations: For any measurable set ,

For mathematical details, see [K.&T. Hattori, 2008a, K.&T. Hattori, 2008b].

-

(i)

In the subsequent sections we consider the stochastic ranking process as a model for the rankings found, for example, at the web sites of an online bookstore. We regard an item in the model as a book title, and the jump time to rank as the time that the title is ordered for sale. According to the definition of the model, we assume that each time a book is ordered the ranking of the title jumps to , no matter how unpopular the book may be. At first thought one might guess that such a naive ranking will not be a good index for the popularity of books. But thinking more carefully, one notices that well sold books (items with large , in the model) are dominant near the head of the ranking, while books near the tail are rarely sold. Hence, though the ranking of each book is stochastic and has sudden jumps, the spacial distribution of jump rates are more stable, with the ratio of books with large jump rate high near the top position and low near the tail position. Seen from the bookstore’s side, it is not a specific book that really matters, but a totality of book sales that counts, so the evolution of distribution of jump rate is important. Theorem 2 says that we can make this intuition rigorous and precise, with an explicit form of the distribution when the total number of titles in the catalog of the bookstore is large (i.e., in the large limit).

3 Application to sales analysis of Amazon.co.jp.

In this section, we give an explicit example of how the theoretical framework in Section 2 could be applied to realistic situations. We will focus on the sales ranking data found at the websites of Amazon.co.jp, the Japanese counterpart of the online bookstore Amazon.com.

We first give in Section 3.1 a brief explanation about the sales ranking number found at the web pages for Japanese books at Amazon.co.jp, and summarize in Section 3.2 the method of applying Section 2 to actual ranking data, and give an explicit result of statistical fits of the distribution of sales rate of the books at the online bookstore.

3.1 Amazon.co.jp book sales ranking.

The web sites of Amazon (irrespective of countries) have a web page for each book title, where we find, as well as its title, author and price, a number which represents the sales ranking of the book. It has been noticed [Chevalier etal., 2003, Brynjolfsson etal., 2003] that this number serves as an important data for quantitative studies of the economic impact of online bookstores. This is because the number reflects the sales rate of the book, and especially in the situation that, in terms of [Brynjolfsson etal., 2003], ’Internet retailers are extremely hesitant about releasing specific sales data’, it can be one of the scant data publicly available.

We refer to [Chevalier etal., 2003] for general structure of the web pages, and to [Rosenthal, 2006] for a summary based on apparently a long and extensive observation of the ranking number at Amazon.com, and in particular, discussion on its relation to the actual sales of the book at Amazon.com. Here we focus on observed facts about the time evolution of ranking numbers at Amazon.co.jp. Firstly, it is said that Amazon.com adopts an involved definition of the ranking numbers than the stochastic ranking process. Secondly, Amazon.co.jp is easier for the authors to find appropriate data (it is our home country).

If we keep observing the ranking number of a book, we soon notice that it is updated once per hour regularly. For a relatively unpopular book title, the corresponding ranking number increases steadily and smoothly for much of the time as the number is updated, but once in a while we see a sudden jump to a smaller number around ten thousand. This happens when a copy of the book is ordered for purchase, which can be checked by personally ordering a copy at Amazon website; at the update time which is – hours after the order, the ranking number is observed to jump. Actually, except for the top ten thousand sellers out of a few million Japanese book titles catalogued at Amazon.co.jp, a book sells less than per hour on average, hence the qualitative motion just described hold for percent of the book titles at Amazon.co.jp.

Note that this behavior of the time evolution of a ranking number is similar to that of stochastic ranking model in Section 2. The correspondence is also natural from an observation by [Rosenthal, 2006] that the Amazon’s ranking number system ‘is based almost entirely on “what have you done for me lately”’. For seldom sold books, any natural definition of the ranking number satisfying such a criterion would be in the order of latest sales time, because any sales record before the latest one should be further remote past and would have only a small effect on any reasonable definition of the ranking number. Hence the definition of the stochastic ranking process in Section 2, even though it may have sounded over-simplified, has a chance of being a good theoretical basis for modelling the ranking numbers on the web, especially for probing a large collection of titles in the long tail regime of the catalog, which is of interest in this paper.

If we further assume as usual that the point of sales are random, then we will have a full correspondence between the stochastic ranking model and the time evolutions of ranking numbers at Amazon.co.jp. Based on the correspondence, we give, in the next subsection Section 3.2, explicit formulas which relate a time evolution of a ranking number to a distribution of average sales rate of the book titles at the bookstore, and then using the formulas we give results of fits with observed data.

3.2 Stochastic ranking process analysis of book sales ranking.

We start with a standard assumption, as, for example, in [Chevalier etal., 2003, Brynjolfsson etal., 2003], that the probability distribution of book sales rate is a Pareto distribution (also called a power law or a log–linear distribution). In the notations of Section 2 this means that we assume the probability measure to be

| (5) |

where and are positive constants. Its probability density function is given by

| (6) |

In terms of books, denotes the average sales rate of a book on the list of a bookstore; a book with sells on average in the long run copies per unit time. is the distribution of ; for example, is the ratio of the number of book titles with sales rate or more to the total number of titles. Alternatively we could start with another (discrete) formulation of the Pareto distribution

| (7) |

where the constant in (7) (or in (5)) denotes the lowest positive sales rate among the book titles at the store. Note that the books that never sell should be omitted in applying our theory. is the total number of such titles as actually sell catalogued at the online bookstore, and is the average sales rate of the -th best seller. The ratio of titles with or more average sales rate is then

for , reproducing (5).

The exponent ( corresponds to the Pareto slope parameter) is crucial in the analysis of economic impact of the retail business in question. In fact, previous studies using the ranking numbers at the online bookstores [Chevalier etal., 2003, Brynjolfsson etal., 2003] use the data for extracting the exponent , which then was used to study various aspects of economic impact of the online bookstores. An intuitive meaning of the exponent can be seen, for example, by taking ratio of (7) for and , to find

| (8) |

which roughly says that for large if is small then is very large compared to , so that the greatest hits dominate the sales, while if is large the contributions are more equal, and since there are many unpopular titles, their total contribution to the sales may dominate (the ‘long tail’ possibility). We will discuss further on the implications of the parameter in Section 4.

Our method of obtaining the parameters and is to observe a time development of the ranking of any single book title, which contains information of , with statistical fluctuations strongly suppressed. (One may be curious why a data from a single title could have fluctuation suppressed. This is because the time development of the ranking, during the book in question is not sold, is a result of the total sales of the the large amount of titles in the tail side of the observed book in the catalog of an online bookstore, hence the statistical fluctuation is suppressed by a law-of-large-numbers mechanism. This is a practical meaning of the deterministic motion appearing as an infinite particle limit stated in Section 2.) Substituting (5) in (2) we have

| (9) |

where is the incomplete Gamma function defined by Since is positive as . This divergence is mathematically harmless because of the factor , but from a practical point of view, it is convenient to use the integration-by-parts formula

| (10) |

to obtain

| (11) |

This formula is satisfactory for . For use (10) again to obtain

| (12) |

In principle, we may perform integration by parts as many times as required, though we did not come across values in the literature or in our data. For , we need a slightly different formula with ‘logarithmic corrections’, but we have not observed any practical evidence that the exact value of occurs, so we will always assume in the following, to simplify the formulas.

Note in particular, that (11) implies that for we have a concave time dependence for short time,

while (12) implies that for we have linear short time dependences. According to the results in Section 2, is the relative position (i.e., ) at time in the ranking of the title which was at the top position (i.e. sold) at . The corresponding ranking number is given by

| (13) |

where is the total number of the catalogued titles that actually sell. We cannot control subleading order in because of the statistical fluctuations. (The limit theorems in Section 2 assures that the leading order is free of statistical fluctuations.) However, since Amazon has a huge ‘electronic bookshelf’ of order , we will omit the statistical fluctuations of relative order .

Incidentally, we can alternatively start from (7) and use the empirical distribution for , where is a unit distribution concentrated at . Then from (2) we have, by elementary calculus,

reproducing (9).

Before closing this subsection, we recall that (2) implies that the ranking of an item is, as a function of time , essentially the Laplace transform of the underlying distribution of the jump (sales) rates. If we have a accurate and long enough ranking data (i.e., observation of the time evolution of the ranking for a very long period and with very fine intervals), the uniqueness of inverse Laplace transform assures in principle the determination of non-parametrically, i.e., without assumptions on such as assuming Pareto distribution (5). This approach however requires a very fine data, because the Laplace transform has smoothing effect through factor, and a small irregular differences in the Laplace transform could result in a large difference in the original function. In the case of Amazon.co.jp, which we see in Section 3.3, the ranking is updated only once per hour and we cannot expect fine enough data (as is also the case of Amazon.com), so we will follow a standard approach assuming a Pareto distribution for . (Needless to say, the managers in the Amazon company have access to precise real-time data, hence our methods will help them analyze and plan the inventory controls and evaluate the sales.)

If long tail economy expands in the future, and our methods turn out to be of practical use, it would be preferable to have real time spontaneous updates of the ranking data, which will make our methods more efficient and accurate. (It will not cost any more than the current Amazon’s ranking data updates with hourly intervals; in fact, the title listings at the 2ch.net adopt such algorithms [K.&T. Hattori, 2008b].)

3.3 Results from Amazon.co.jp.

By performing a statistical fit to (13) of ranking time evolution data, we can in principle obtain the parameters and which determine the distribution of average sales rates of the book titles at Amazon.co.jp. In the practical situations, it turns out that the total number of the book titles also needs to be determined from the data.

We are aware that Amazon.co.jp publicizes at their website the total number of book titles on their catalog, which can be reached by making an unconditioned search at the Amazon website. However, the book catalogs at Amazon websites contain books which are not available and therefore do not sell, hence, as we noted below equation (7) while describing the Pareto distribution, should be discarded from our analysis. We have experienced more than once that we order a book at the website and receive a note after a while that the book has not been found and that the order is cancelled. At the same time, we observe the ranking number of that cancelled title making jumps to the tail side. We thus realize that the claimed number of titles at the website contains those with and is therefore strictly larger than what we should use for in our formulation. As an explicit example, the number from Amazon.co.jp search results was 2,587,571 on Oct. 4, 2007, while our fits indicates to be strictly less than million (see (14)).

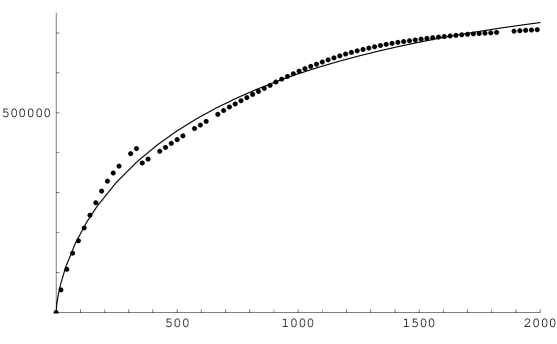

Now we turn to our results of observation. The plotted points in Fig. 1 show the time evolution of the ranking of a book we observed between the end of May, 2007 (at which point the book was ordered for sales) and mid August, 2007 (at which point the book was bought again). The solid curve is a least square fit of these points to (13). The best mean-square fit for the parameter set is:

| (14) |

Note that is large, hence the fluctuations arising from randomness in the sales are relatively suppressed (), as expected, while the number is smaller than that found by performing a search at the Amazon website (), so that a fit of is necessary. is in units of and corresponds to months for , which is longer than the interval of observation ( months). Our method allows the determination of time constants longer than the interval of observation because there are a large amount of (mostly unpopular) titles which theoretically allow a law-of-large-numbers mechanism. (The obtained value of does not mean that there are no books at all which sells, say, only one copy a year on average; it says that such books are much less than would be expected from a log-linear (Pareto) distribution and have a negligible economic impact.)

The total variance of the data from this fit is , hence the statistical fluctuation of the relative ranking is roughly of order

This seems a little larger than an expectation from the Gaussian fluctuation which would be of order . Fig. 1 suggests that a possible reason of the deviations of data from the fit is caused by a small jump at about hours. We suspect this as a result of inventory controls at the web bookstore, such as unregistering books out of print. Apparently, Amazon.co.jp in the year 2007 was updating their catalogs manually and only occasionally, making it a kind of unknown time dependent external source for our analysis.

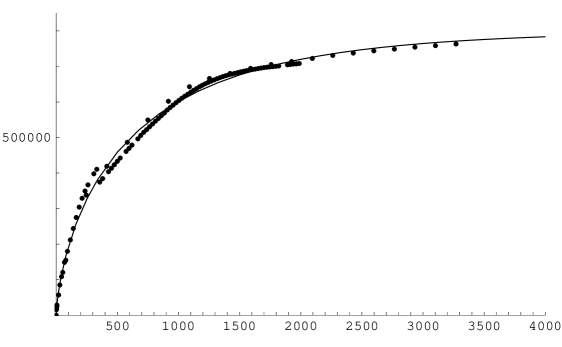

Concerning the stability of the parameters, we made another series of observation between November, 2007 and March, 2008. This time, having less time to spare we recorded only once a week resulting in points. The solid curve in Fig. 2 is a least square fit of the combined points and the points in Fig. 1 to (13). The best mean-square fit for the parameter set is:

| (15) |

() effectively remained same as (14). The parameters have changed somewhat; change in the total number of active books is not large (about 7%), months which is somewhat shorter than (14). The exponent is larger, but note that we again have exponent strictly less than .

Though we clearly and consistently have (also seen from the concave figure in Fig. 1 and Fig. 2), its value has changed. The change of and between (14) and (15) is consistent with a hypothesis that Amazon.co.jp performed inventory controls (as they should do) and got rid of books with low sales between the two series of observations, so one explanation is that the exponent also changed. Another possible reason is that the new data of once per week are too sparse and that we need finer data for stable fits. In fact, as pointed out at the end of Section 3.2, a fit to the distribution may be sensitive to small changes in the ranking data, and a data finer than once per week may be required. This problem could be overcome by automated data acquisition through computer programming.

The values in (14) and in (15) are both less than . The result, obtained from our data may also be convincing by a look at Fig. 1 and Fig. 2, because, as we noted below (12), the short time behavior of the ranking is proportional to for (which implies the graph is tangential to the ranking axis), while is linear for . Previous studies [Chevalier etal., 2003, Brynjolfsson etal., 2003] adopt values . (The correspondences of the notations are for [Brynjolfsson etal., 2003] and for [Chevalier etal., 2003]. In statistics textbooks and are also used.) According to what we remarked below (8), this implies that, in general, the economic impact of keeping unpopular titles at online bookstores may be overestimated in the previous studies. We will continue on this point in Section 4.

4 Discussions.

4.1 Formulas for the long tail structure of online retails.

In Section 3 we dealt with an application of a formula (2) in a practical situation, a prediction on the time evolution of the ranking of a book. The theoretical framework in Section 2, introducing the main results of [K.&T. Hattori, 2008a], contains more than this, and predicts the total amount of sales (per unit time) that could be expected from the items (e.g., books, in the case of an online bookstore) on the tail side of any given ranking number .

Note that this is not equal to the total contribution to the sales from the tail side aligned in order of potential (average) sales rate, which is in the notations in Section 3. This is because, since the ranking number jumps to the head each time the item sells at a random time, and since there are a very large number of items (), we always have some lucky items with low potential sales around the head side of the rankings, and according to a similar argument, we also must have some ‘hit’ items towards the tail side. The main theorem in [K.&T. Hattori, 2008a], as explained in Section 2, states that the ratio of such (un-)lucky items having ranking numbers very different from those expected from their potential sales ability is non-negligible even in the limit.

An explicit formula can be derived from (3). Note that (2) and Assumption (2) for Theorem 2 imply , hence after a sufficiently long time since the start of the bookstore and its ranking system, one may assume that the ranking reaches a stationary phase and the first equation in (3) holds for all . Letting and in (3) we have

| (16) |

Let , and denote by the contribution to the total average sales per unit time from the items with ranking number between and . For a very large , we may let and use (16) to find

| (17) |

This is valid for an arbitrary sales rate distribution ; for the Pareto distribution (6) we have, using the incomplete Gamma function as in (9),

| (18) |

where is given by (4) with (11):

| (19) |

For , a better expression using (10) as in (12) would be

| (20) |

with

| (21) |

is to be compared with the contribution to the total average sales per unit time from the items between and ordered in decreasing order of potential sales rate , as in (7). We have,

| (22) |

Note that and . The latter is from (9):

The last term is a convergent integral for , which is proved by (19) for and by (21) for . It converges to as .

The special case of corresponds to the contribution from the tail side in the ranking for and the tail side in the potential sales rate for (the ‘long tail’), which are (after some elementary calculus as above)

| (23) |

with given by (19) or (21), and

| (24) |

Concerning the contributions from the head side (‘great hits’), we note that the cases and are different. This is easy to see in (22), where we find if , while for , we can safely take limit to find

This quantity represents an average sales rate per unit time per unit item, which is finite for the realistic situations. For great hits dominate in the total sales, which theoretically becomes infinitely large as (see (7)), while for all the items contribute non-trivially, and that with a large number of items, the contribution from the ‘long tail’ would dominate, which intuitively explains the difference in the behavior. The divergence is a result of limit. We will consider cases and separately and discuss the implication of the value of in detail.

4.2 Implications of the Pareto exponent .

We noted at the end of Section 4.1 and also below (8) that large means that the ‘long tail’ is important while small means that great hits dominate. Intuitively, there are great hits and long tail items, so the ratio of the contribution of the former to the latter is, using (8), , hence when the total number of items is large, the dominant contribution to the total sales change between and .

4.2.1 Case : The long tail economy.

Let and assume is large.

For , the contribution to the total sales per unit time of the items (out of the total ) with low sales potentials is given by (24):

| (25) |

In particular, the total sales per unit time at the online store is

| (26) |

Subtraction gives us the total sales amount from the top hits per unit time:

| (27) |

Similarly, (23) gives the contribution to the total sales per unit time from the items in the tail side of the ranking:

| (28) |

In particular, noting and

we have for , which is equal to (26) as expected, because all the items in the store are listed on the ranking. Subtraction gives us the total sales amount from the top items in the ranking (at any given time, if the ranking is stationary) per unit time:

| (29) |

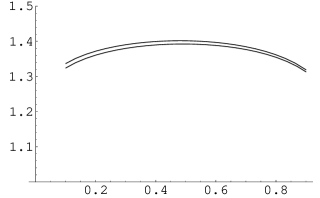

The large implies that there is a good chance in the long tail business. For example, for a extreme case of , (27) implies , so that top 20% of hit items contribute only 45% of total sales, far less than 80% , challenging the widespread ‘20–80 law’. This is, however, too extreme, and we should use realistic values. Concerning the analysis based on the rankings of Amazon.com, Chevalier and Goolsbee [Chevalier etal., 2003] explored a number of sources of information, including their own experiment, and obtained values for the exponent ranging from to , and adopted the value for their subsequent calculations, to find, for example, that the online bookstores have more price elasticity than the brick-and-mortar bookstores and have a significant effect on the consumer price index. Brynjolfsson, Hu, and Smith [Brynjolfsson etal., 2003] uses ( in their notations), to evaluate the increase in consumer welfare by the introduction of large catalogues of books by the online bookstores. They also quote the values in [Chevalier etal., 2003] and report a result of similar experiment to obtain . For and we have and , respectively, behaving more or less like ‘20–80 law’. Of course, we are considering of order of million (or more, with the advance in the web 2.0 technologies and online retails expected in the close future) distinct items as in (14) or (15), and top 20% also means a large number. The term ‘possibility of the long tail business’ makes sense for , in the sense that, with a drastic decrease in the cost for handling a large inventory through online technology, a retail with a million items on a single list produces a large profit.

Let us return to (28) and consider the role of the stochastic ranking process in inventory controls. As an example, consider a situation where an online store is to open a new brick-and-mortar store with items out of item sold at the online store. If the manager knew the average sales rate of each item (for example, based on past records at the online store), he would choose the top items and the expected decrease in the total sales (per unit time) compared to the online store will be . ( will usually be estimated based on past record of sales, and there is a potential problem, as expressed in the Introduction, that for items with small , one would have small sales records, and statistical fluctuations obscure precise determination of in the long tail regime. How the managers find way out in this approach is beyond the scope of this paper.) Now if the manager considered it quicker to select top items in the ranking at the online store, what would be the extra loss? In this case, the expected decrease in the total sales (per unit time) will be , so the ratio measures the extra loss from the use of ranking number in place of sales rate. Fig. 3 shows this ratio as a function of for , calculated using (28). As a value of we adopted the values from [Chevalier etal., 2003, Brynjolfsson etal., 2003]. The ratio turned out to be insensitive to in this range and shows 35% to 40% increase. (For near and , the ratio approaches , and the use of ranking data is better. For large the ratio also approaches , and we also found that the ratio is not sensitive up to close to .) This shows an example of the use of ranking data as simple and effective measure of analyzing sales structure of the long tails.

4.2.2 Case : The great hits economy.

Now let and assume is large.

As noted at the end of Section 4.1, when we are considering sales for , taking limit results in unrealistic infinities on average sales (sales per item), arising from divergence of great hits. Explicitly, from (7) we have as for each fixed . Divergence from a single item does not cause the divergence of the average, but for , there are many such items which affect averages.

Before studying this problem, we note that the time evolution of the ranking of a single item which we discussed in detail in Section 3 has no problem. Theoretically, this reflects the fact that we assume nothing on the distribution in Proposition 1. The problem of divergence of the average sales rate is theoretically reflected only in the fact that for the Assumption (3) to Theorem 2 fails. As remarked below Theorem 2, this affects the distribution at , the top end of the rankings, but no theoretical problem occurs for . Intuitively speaking, if there are (fictitious) book titles which sell ‘infinitely many copies per unit time’, they keep staying at the top end of the ranking, and the rest of ‘realistic’ book titles follow the evolution of ranking as predicted by Proposition 1. Also, the contribution to the total sales from the tail side (both and for ) has no problem of divergence, i.e., asymptotically proportional to as in (25) or (28). In other words, formulas not containing contributions from the ‘greatest hits’ remain valid: For , the contribution to the total sales per unit time from the items (out of total ) of low sales potentials is as (25), and that from the items in the tail side of the ranking is as (28) with (19),

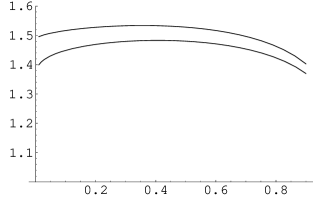

In particular, we can perform a similar analysis as that concerning Fig. 3 using (28). The loss in total sales per unit time caused by selecting top items in the ranking instead of selecting top items in the sales rate can be measured in terms of their ratio . Fig. 4 shows this ratio as a function of for , calculated using (28). As a value of we adopted the values in (14) and (15). The ratio is below and insensitive to in this range. For near , the ratio approaches , and the use of ranking data is good. (Unlike the case in Section 4.2.1, the ratio remains strictly greater than as .)

Returning to the problem of unrealistic infinity, a simple modification for our approach would be to introduce a cut off. Taking logarithms of (7) we have

| (30) |

This formula shows that plotting the sales rates against on a log–log graph, the points will fall on a single line. (This suggests a reason why Pareto distribution is also called log-linear distribution and that the exponent is called the Pareto slope parameter.) When one assumes Pareto distributions in social and economic studies, the argument would be in reverse direction; one probably first observes data aligned close to a single line on a log–log graph, and then arrive at a idealized theoretical model (30) or (7). The line actually ends in realistic situations, and (30) denotes the tail end by and the head end by . We let in our formulation and as a result lost the head end, which causes trouble in average sales rate for . A simple remedy is therefore to introduce a cut-off parameter or , and assume a modified Pareto distribution,

| (31) |

or extend (7) as

| (32) |

or is the original Pareto distribution. We assume Pareto distribution to be basically applicable, so we assume ().

Using (32) in the left hand side of (22), we have

| (33) |

If we reproduce (24). We can safely let in (33) and find

| (34) |

In particular,

| (35) |

(The left hand side is obtained by taking leading term in .) Note that we cannot let for .

Other quantities can also be derived if we replace (7) by (32). Following the argument below (7), we have, in place of (6),

| (36) |

Substituting (36) in (2) we have, in place of (9),

| (37) |

We note that we can take limit in (37) and reproduce (9). In other words, the effect of is small for the evolution of ranking , if is small. In Section 3 we assumed the original Pareto distribution, and performed a fit to (11) which is equal to (9). That this works implies that is actually small and that (9) is a good approximation to (37). In fact, as noted at the beginning of this subsection Section 4.2.2, the effect of ‘greatest hits’ on the ranking is that they keep the top positions constantly. The ranking data at Amazon websites are updated only once per hour, and since there are many books which sell more than one per hour, we never observe ranking by tracing (as we do) a book which sells only once per months. For such observations it is intuitively clear that taking causes no singularities regardless of the value of .

Reversing this argument, we see that since small difference in does not affect the evolution of ranking , we cannot estimate the value of from . The dependence on of the total sales in (35) cannot be removed, hence for , we cannot estimate the total sales of the online store from the ranking data. Our method is effective in studying the tail structures, but is weak at great hits for . Standard methods, such as estimating from press reports about top hits, should be combined, if the online store is not willing to disclose the total sales.

Returning to (35), we see that for the total sales could be very large (if the cut-off parameter is very small) while (25) implies that , the contribution from the tail side, is constant in , hence the ratio could be very small. This is in contrast to the case discussed in Section 4.2.1, where the ratio is significantly away from . In this sense, the contribution to the sales from the long tail would be modest in general, and the impact of long tail business on economy would be also modest, if . Our calculations for Amazon.co.jp in Section 3 supports , in spite of the Amazon group’s reputation for their long tail business. We are however aware that when we talk about possibility of long tail business, there are other aspects than the contribution to the total sales or the direct economic impact of long tails. For example, the phrase ‘the leading retail store’ is a highly effective advertisement, and being number one, would be quoted by mass media, thereby drastically reduce advertisement cost. We therefore will not be amazed if an online bookstore takes a strategy to advertise their long tail business model, but is hesitant about disclosing its actual sales achievement, and makes profit largely from advance orders of ‘great hits’ such as Harry Potter series.

4.3 Conclusions.

In this paper, we gave a mathematical framework of a new method to obtain the distribution of sales rates of a very large number of items sold at an internet retail site which disclose sales rankings of their items. We gave explicit formulas for practical applications and an example of a fit to the actual data obtained from Amazon.co.jp. The method is based on new mathematical results [K.&T. Hattori, 2008a, K.&T. Hattori, 2008b] on a infinite particle limit of the stochastic ranking process, and is theoretically new and quantitatively accurate.

The method is suitable especially for quantitative studies of the long tail structure of online retails, which has been expanding commercially with the advance in computer networks and web technologies. Calculation algorithm of the ranking numbers is very simple (simplest is the best, from the theoretical side), and will be relatively easy to implement online. Hence our theory could serve as an efficient and inexpensive method for disclosure policies and regulation purposes, as well as for providing the online store business a method of prompt analysis of long tail sales structure. (We have heard from a book publisher that Amazon.co.jp are not willing to open their sales results. The publisher was amazed to know that we could estimate Amazon’s sales structure from their rankings.) With a possible future increase in online long tail business, the role of our theory in the business disclosure policies may increase its significance.

Since the result is based on mathematical results, it is in principle applicable to general situations such as retail stores with POS systems, blog page view rankings, or the title listings of the web pages in the collected web bulletin boards. In fact, we collected a preliminary data from 2ch.net, one of the largest collected web bulletin boards in Japan, performed a fit to (13), and obtained a value for the Pareto exponent, which is close to (14). See [K.&T. Hattori, 2008b] for details. In the 2ch.net title listing page, the titles are ordered by ‘the last written threads at the top’ principle, which matches the definition of the stochastic ranking process in Section 2.

The method would be useful for marketing purposes as well as studies in social activities in general, thus we consider it worthwhile to disclose the method for free use in practical situations.

Acknowledgements. We thank Prof. K. Takaoka for his interest in the work and kindly giving opportunity to talk at a meeting for mathematical finances.

The research of K. Hattori is supported in part by a Grant-in-Aid for Scientific Research (C) 16540101 from the Ministry of Education, Culture, Sports, Science and Technology, and the research of T. Hattori is supported in part by a Grant-in-Aid for Scientific Research (B) 17340022 from the Ministry of Education, Culture, Sports, Science and Technology.

References

- [Anderson, 2006] C. Anderson, The Long Tail: Why the Future of Business Is Selling Less of More, Hyperion Books, 2006.

- [Billingsley, 1995] P. Billingsley, Probability and Measure, 3rd ed., New York, Wiley, 1995.

- [Brynjolfsson etal., 2003] E. Brynjolfsson, Y. Hu, M. D. Smith, Consumer surplus in the digital economy: Estimating the value of increased product variety at online booksellers, Management Science 49-11 (2003) 1580–1596.

- [Chevalier etal., 2003] J. Chevalier, A. Goolsbee, Measuring prices and price competition online: Amazon.com and BarnesandNoble.com, Quantitative Marketing and Economics, 1 (2) (2003) 203–222.

- [K.&T. Hattori, 2008a] K. Hattori, T. Hattori, Existence of an infinite particle limit of stochastic ranking process, preprint, 2008.

- [K.&T. Hattori, 2008b] K. Hattori, T. Hattori, Equation of motion for incompressible mixed fluid driven by evaporation and its application to online rankings, preprint, 2008.

- [Rosenthal, 2006] M. Rosenthal, What Amazon Sales Ranks Mean, http://www.fonerbooks.com/surfing.htm, 2006.