Sliced Inverse Moment Regression Using Weighted Chi-Squared Tests for Dimension Reduction

Abstract

We propose a new method for dimension reduction in regression using the first two inverse moments. We develop corresponding weighted chi-squared tests for the dimension of the regression. The proposed method considers linear combinations of Sliced Inverse Regression (SIR) and the method using a new candidate matrix which is designed to recover the entire inverse second moment subspace. The optimal combination may be selected based on the p-values derived from the dimension tests. Theoretically, the proposed method, as well as Sliced Average Variance Estimate (SAVE), are more capable of recovering the complete central dimension reduction subspace than SIR and Principle Hessian Directions (pHd). Therefore it can substitute for SIR, pHd, SAVE, or any linear combination of them at a theoretical level. Simulation study indicates that the proposed method may have consistently greater power than SIR, pHd, and SAVE.

keywords:

Dimension reduction in regression , pHd , SAVE , SIMR , SIR , Weighted chi-squared test1 Introduction

The purpose of the regression of a univariate response on a -dimensional predictor vector is to make inference on the conditional distribution of . Following Cook (1998b), can be replaced by its standardized version

| (1) |

where and denote the mean and covariance matrix of respectively assuming non-singularity of .

The goal of dimension reduction in regression is to find out a matrix such that

| (2) |

where “ ” indicates independence. Then the -dimensional can be replaced by the -dimensional vector without specifying any parametric model and without losing any information on predicting . The column space is called a dimension reduction subspace. The smallest applicable is called the dimension of the regression.

Based on the inverse mean , Li (1991a) proposed Sliced Inverse Regression (SIR) for dimension reduction in regression. It is realized that SIR can not recover the symmetric dependency (Li, 1991b; Cook and Weisberg, 1991). After SIR, many dimension reduction methods have been introduced. Sliced Average Variance Estimate (SAVE) proposed by Cook and Weisberg (1991) and Principle Hessian Directions (pHd) proposed by Li (1992) are another two popular ones. Both pHd and SAVE refer to the second inverse moment, centered or non-centered. Compared with SAVE, pHd can not detect certain dependency hidden in the second moment (Yin and Cook, 2002; Ye and Weiss, 2003) and the linear dependency (Li, 1992; Cook, 1998a). Among those dimension reduction methods using only the first two inverse moments, SAVE seems to be the preferred one. Nevertheless, SAVE is not always the winner. For example, Ye and Weiss (2003) implied that a linear combination of SIR and pHd may perform better than SAVE in some cases. It is not surprising since Li (1991b) already suggested that a suitable combination of two different methods might sharpen the dimension reduction results. Ye and Weiss (2003) further proposed that a bootstrap method could be used to pick up the “best” linear combination of two known methods, as well as the dimension of the regression, in the sense of the variability of the estimators, although lower variability under the bootstrap procedure does not necessarily lead to a better estimator. Li and Wang (2007) pointed out that linear combinations of two known methods selected by the bootstrap criterion may not perform as well as a single new method, their Directional Regression method (DR), even though the bootstrap one is computationally intensive.

This article aims to develop a new class of, instead of a single one, dimension reduction methods using only the first two inverse moments, as well as the corresponding large sample tests for the dimension of the regression and an efficient criterion for selecting a suitable candidate from the class. Theoretically, it can cover SIR, pHd, SAVE and their linear combinations. Practically, it can achieve higher power in recovering the dimension reduction subspace. In Section 2, we review the necessary dimension reduction context. In Section 3, we introduce a simple candidate matrix which targets the entire inverse second moment subspace. It is indeed the candidate matrix of an intermediate method between pHd and SAVE. In Section 4, we propose a new class of dimension reduction methods called Sliced Inverse Moment Regression (SIMR), along with weighted chi-squared tests for the dimension of the regression. In Section 5, we use SIMR to analyze a simulated example and illustrate how to select a good candidate of SIMR. Simulation study shows that SIMR may have consistently greater power than SIR, pHd, and SAVE, as well as DR and another new method Inverse Regression Estimator (Cook and Ni, 2005). In Section 6, a real example is used to illustrate how the proposed method works. It is implied that a class of dimension reduction methods, along with a suitable criterion for choosing a good one among them, may be preferable in practice to any single method. We conclude this article with discussion and proofs of the results presented.

2 Dimension Reduction Context

2.1 Central Dimension Reduction Subspace (CDRS)

Cook (1994b, 1996) introduced the notion of central dimension reduction subspace (CDRS), denoted by , which is the intersection of all dimension reduction subspaces. Under fairly weak restrictions, the CDRS is still a dimension reduction subspace.

In this article, we always assume that is a dimension reduction subspace and that the columns of is an orthonormal basis of . In practice, we usually first transform the original data into their standardized version by replacing and in (1) with their usual sample estimates and . Then we can estimate by

where is an estimate of . Therefore, the goal of dimension reduction in regression is to find out the dimension of the regression and the CDRS .

2.2 Candidate Matrix

Ye and Weiss (2003) introduced the concept of candidate matrix, which is a matrix satisfying . They showed that any eigenvector corresponding to any nonzero eigenvalue of belongs to the CDRS . Besides, the set of all candidate matrices, denoted by , is closed under scalar multiplication, transpose, addition, multiplication, and thus under linear combination and expectation.

They also showed that the matrices and belong to for all , where and . They proved that the symmetric matrices that SIR, SAVE, and -pHd estimate all belong to :

3 Candidate Matrix

3.1 A Simple Candidate Matrix

The matrices and are actually two fundamental components of , , and (see Section 2.2). only involves the first component , while both and share the second component . Realizing that this common feature may lead to the connection between SAVE and pHd, we investigate the behavior of the matrix . To avoid the inconvenience due to , we define

Note that takes a simpler form than the rescaled version of sirII (Li, 1991b, Remark R.3) while still keeping the theoretical comprehensiveness. It also appears as a component in one expression of the directional regression matrix (Li and Wang, 2007, eq.(4)). We choose its form as simple as possible for less complicated large sample test and potentially greater test power. To establish the relationship between and , we need:

Lemma 1

Let be a random matrix defined on a probability space , then there exists an event with probability , such that,

A similar result can also be found in Yin and Cook (2003, Proposition 2(i)). The lemma here is more general. By the definition of ,

Corollary 1

, where is the support of .

Based on Corollary 1, Ye and Weiss (2003, Lemma 3), and the fact that for all , matrix is in fact a candidate matrix too. Corollary 1 also implies a strong connection between and :

Corollary 2

.

To further understand the relationship between and , recall the central -th moment dimension reduction subspace (Yin and Cook, 2003), . The corresponding random vector contains all the available information about from the first conditional moments of . In other words, . Similar to

the subspace is also contained in . Parallel to Yin and Cook (2002, Proposition 4), the result on is:

Proposition 1

(a) If has finite support , then

(b) If is continuous and is continuous on ’s support , then

According to Proposition 1 and Yin and Cook (2002, Proposition 4), the relationship between and is fairly comparable with the relationship between and . Both and actually target the central mean (first moment) dimension reduction subspace (Cook and Li, 2002), while and target the central -th moment dimension reduction subspace given any , or equivalently the CDRS as goes to infinite. In order to understand the similarity from another perspective, recall the inverse mean subspace of (Yin and Cook, 2002):

Similarly, we define the inverse second moment subspace of :

By definition, matrices and are designed to recover the entire inverse mean subspace and the entire inverse second moment subspace respectively, while and are only able to recover portions of those subspaces. We are therefore interested in combining matrices and because they are both comprehensive.

3.2 SAVE versus SIR and pHd

Proposition 2

Corollary 3

Corollary 3 explains why SAVE is able to provide better estimates of the CDRS than SIR and -pHd in many cases.

4 Sliced Inverse Moment Regression Using Weighted Chi-Squared Tests

4.1 Sliced Inverse Moment Regression

In order to simplify the candidate matrices using the first two inverse moments and still keep the comprehensiveness of SAVE, a natural idea is to combine with as follows:

where . We call this matrix and the corresponding dimension reduction method Sliced Inverse Moment Regression (SIMR or SIMRα). Note that the combination here is simpler than the method (Li, 1991b; Gannoun and Saracco, 2003) while retaining the least requirement on comprehensiveness. Actually, for any , SIMRα is as comprehensive as SAVE at a theoretical level based on the following proposition:

Proposition 3

Combined with Corollary 3, we know that any linear combination of SIR, pHd and SAVE can be covered by SIMRα:

Corollary 4

, where , and are arbitrary real numbers.

Note that the way of constructing SIMRα makes it easier to develop a corresponding large sample test for the dimension of the regression (Section 4.3).

From now on, we assume that the data are i.i.d. from a population which has finite first four moments and conditional moments.

4.2 Algorithm for SIMRα

Given i.i.d. sample ,…,, first standardize into , sort the data by , and divide the data into slices with intraslice sample sizes , . Secondly construct the intraslice sample means and :

where ’s are predictors falling into slice . Thirdly calculate

where and

Finally calculate the eigenvalues of and the corresponding eigenvectors . Then is an estimate of the CDRS , where is determined by the weighted chi-squared test described in the next section.

4.3 A Weighted Chi-Squared Test for SIMRα

Define the population version of :

| (8) | |||||

where is a slice indicator with for all observations falling into slice , is the population version of , and (8) is the singular value decomposition of .

Denote . By the multivariate central limit theorem and the multivariate version of Slutsky’s theorem, converges in distribution to a certain random matrix as goes to infinity (Gannoun and Saracco, 2003). Note that the singular values are invariant under right and left multiplication by orthogonal matrices. Based on Eaton and Tyler (1994, Theorem 4.1 and 4.2), the asymptotic distribution of the smallest singular values of is the same as the asymptotic distribution of the corresponding singular values of the following matrix:

| (9) |

Construct statistic

which is the sum of the squared smallest singular values of . Then the asymptotic distribution of is the same as that of the sum of the squared singular values of (9). That is

where denotes for any matrix . By central limit theorem and Slutsky’s theorem again,

for some nonrandom matrix . Thus,

where is a matrix. Combined with Slutsky’s theorem, it yields the following theorem:

Theorem 1

The asymptotic distribution of is the same as that of

where the ’s are independent random variables, and ’s are the eigenvalues of the matrix .

Clearly, a consistent estimate of is needed for testing the dimension of the regression based on Theorem 1. The way we define allows us to partition into

The asymptotic distribution of the matrix has been fully explored by Bura and Cook (2001), resulting in a weighted chi-squared test for SIR. The similar techniques can also be applied on the matrix , and therefore the matrix as a whole, although the details are much more complicated.

Define the population versions of and ,

Then , and .

Let , and be vectors with elements , and respectively; let and be diagonal matrices with diagonal entries and respectively; and let

Finally, define four matrices

and their corresponding sample versions , , , and . By the central limit theorem,

for a nonrandom matrix . As a result,

Theorem 2

The only difficulty left now is to obtain a consistent estimate of . By the central limit theorem,

where is a nonrandom matrix, with details shown in the Appendix. On the other hand,

for a certain mapping such that

Thus the close form of can be obtained by Cramér’s theorem (Cramér, 1946):

| (11) |

where the derivative matrix

| (14) |

with .

In summary, to compose a consistent estimate of matrix , one can (i) substitute the usual sample moments to get the sample estimate of ; (ii) estimate by substituting the usual sample estimates for , and in (11) and (14); (iii) obtain the usual sample estimates of and from the singular value decomposition of ; (iv) substitute the usual sample estimates for , , , and in Theorem 2 to form an estimate of . Note that both and do not rely on . This fact can save a lot of computational time when multiple ’s need to be checked.

To approximate a linear combination of chi-squared random variables, one may use the statistic proposed by Satterthwaite (1941), Wood (1989), Satorra and Bentler (1994), or Bentler and Xie (2000). In the next applications, we will present tests based on Satterthwaite’s statistic for illustration purpose.

4.4 Choosing Optimal

Ye and Weiss (2003) proposed a bootstrap method to pick up the “best” linear combination of two known methods in terms of variability of the estimated CDRS . The bootstrap method works reasonably well with known dimension of the regression, although less variability may occur with a wrong (see Section 5 for an example). Another drawback is its computational intensity (Li and Wang, 2007).

Alternative criterion for “optimal” is based on the weighted chi-squared tests developed for . When multiple tests with different report the same dimension , we simply pick up the with the smallest -value. Given that the true dimension is detected, the last eigenvector added into the estimated CDRS with such an is the most significant one among the candidates based on different . In the mean time, the other eigenvectors with selected tend to be more significant than other candidates too. Based on simulation studies (Section 5), the performance of the -value criterion is comparable with the bootstrap one with known . The advantages of the former include that it is compatible with the weighted chi-squared tests and it requires much less computation.

When a model or an algorithm is specified for the data analysis, cross-validation could be used for choosing optimal too, just like how people did for model selection. For example, see Hastie et al. (2001, chap. 7). It will not be covered in this paper since we aim at model-free dimension reduction.

5 Simulation Study

5.1 A Simulated Example

Let the response , where are i.i.d sample from the distribution. Then the true dimension of the regression is and the true CDRS is spanned by , , and , that is, , and .

Theoretically, , , and have rank one and therefore are only able to find a one-dimensional proper subspace of the CDRS. The linear combination of any two of them suggested by Ye and Weiss (2003) can at most find a two-dimensional proper subspace of the CDRS. On the contrary, both SAVE and SIMR are able to recover the complete CDRS at a theoretical level.

5.2 A Single Simulation

We begin with a single simulation with sample size . SIR, -pHd, SAVE and SIMR are applied to the data. Number of slices are used for SIR, SAVE, and SIMR. The R package dr (Weisberg, 2002, 2009, version 3.0.3) is used for SIR, -pHd, SAVE, as well as their corresponding marginal dimension tests. SIMRα with , paced by , are applied.

For this typical simulation, SIR identifies only the direction . It is roughly , the linear trend. -pHd identifies only the direction , which is roughly , the quadratic component. As expected, SAVE works better. It identifies and . However, the marginal dimension tests for SAVE (Shao et al., 2007) fail to detect the third predictor, . The -value of the corresponding test is .

Roughly speaking, SAVE with its marginal dimension test is comparable with SIMR0.1 in this case. The comparison between SAVE and SIMRα suggests that the failure of SAVE might due to its weights combining the first and second inverse moments. As increases, SIMRα with between and all succeed in detecting all the three effective predictors , and . The CDRS estimated by those candidate matrices are similar to each other, which implies that the results with different are fairly consistent. The major difference among SIMRα is that the order of the detected predictors changes roughly from to as increases from to . As expected, SIMRα is comparable with SIR if is close to .

For this particular simulation, SIMRα with between and are first selected. If we know the true CDRS, the optimal is the one minimizing the distance between the estimated CDRS and the true CDRS. Following Ye and Weiss (2003, p. 974), the three distance measures arccos(), , behave similarly and imply the same for this particular simulation. Since the true CDRS is unknown, bootstrap criterion and -value criterion (Section 4.4) are applied instead.

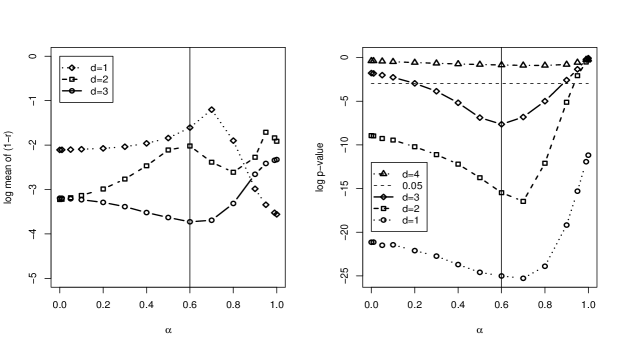

The left panel of Figure 1 shows the variability of bootstrapped estimated CDRS. Distance is used because it is comparable across different dimensions. The minimum variability is attained at and , which happens to the optimal one based on the truth. Another 200 simulations reveal that about “optimal” based on bootstrap fall in . SIMR with chosen by bootstrap criterion attains away from the true CDRS on average. Note that low variability not necessarily implies that the estimated CDRS is accurate. For example, SIMR1 or SIR can only detect one direction . However the estimated one-dimensional CDRS is fairly stable under bootstrapping (see Figure 1).

The right panel in Figure 1 shows that the -value criterion also picks up for this single simulation (check the line , which is the highest one that still goes below the significance level ). Based on the same simulations, about of the “best” selected by -value criterion fall between and . On average, SIMR with selected by -values attains , which is comparable with the bootstrap ones.

5.3 Power Analysis

We conduct 1000 independent simulations and summarize in Table 1 the empirical powers and sizes of the marginal dimension tests with significance level 0.05 for SIR, SAVE, -pHd, and SIMRα with chosen by the -value criterion. For illustration purpose, we omit the simulation results of -pHd because there is little difference between -pHd and -pHd in this case. The empirical powers and sizes with significance level 0.01 are omitted too since their pattern is similar to Table 1.

In Table 1, the rows , , and indicate different null hypotheses. Following Bura and Cook (2001), the numerical entries in the rows , , and are empirical estimates of the powers of the corresponding tests, while the entries in the row are empirical estimates of the sizes of the tests.

As expected, SIR claims in most cases. -pHd works a little better. At the significance level 0.05, -pHd has about chance to find out (Table 1). At level 0.01, the chance shrinks to about . Both SAVE and SIMR perform much better than SIR and pHd. Compared with SAVE, SIMR has consistently greater powers for the null hypotheses , and across different choices of sample size, number of slices and significant level. For example, under the null hypothesis with sample size , the empirical powers of SIMR at level 0.05 are under 5 slices and under 10 slices, while the corresponding powers of SAVE are only and respectively (Table 1). Those differences become even bigger at level 0.01. The empirical sizes of SIMR are roughly under the nominal size 0.05 although they tend to be larger than the others.

For comparison purpose, the methods inverse regression estimator (IRE) (Cook and Ni, 2005; Wen and Cook, 2007; Weisberg, 2009)) and directional regression (DR) (Li and Wang, 2007) are also applied. Roughly speaking, IRE performs similar to SIR in this example. Given that the truth dimension is known, both DR and SIMR are among the best in terms of mean(). For example, at , DR achieves mean() with , with and with , while SIMR’s are , , and . Nevertheless, the powers of the marginal tests for DR are between SAVE and SIMR in this case. Roughly speaking, DR’s power tests are comparable with SIMRα’s with between and . For example, at and level , the empirical powers of DR against are with , with , and with .

Among the six dimension reduction methods applied, SIMR is the most reliable one. Besides, the chi-squared tests for SIMR do not seem to be very sensitive to the numbers of slices. Nevertheless, we suggest that the number of slices should not be greater than 3%-5% of the sample size based on the simulation results.

6 A Real Example: Ozone Data

To examine how SIMR works in practice, we consider a data set taken from Breiman and Friedman (1985). The response Ozone is the daily ozone concentration in parts per million, measured in Los Angeles basin, for 330 days in 1976. For illustration purpose, the dependence of Ozone on the following four predictors is studied next: Height, Vandenburg 500 millibar height in meters; Humidity in percents; ITemp, Inverse base temperature in degrees Fahrenheit; and STemp, Sandburg Air Force Base temperature in degrees Fahrenheit.

To meet both the linearity condition and the constant covariance condition, simultaneously power transformations on the predictors are estimated to improve the normality of their joint distribution. After replacing Humidity, ITemp, and STemp with , , and respectively, SIR, -pHd, SAVE and SIMR are applied to the data. For SIR, SAVE, and SIMR, various numbers of slices are applied, and the results are fairly consistent. Here we only present the outputs based on .

At significance level , SIR suggests the dimension of the regression , while -pHd claims . Using the visualization tools described by Cook and Weisberg (1994) and Cook (1998b), the first pHd predictor appears to be somewhat symmetric about the response , and the second pHd predictor seems to be similar to the first SIR predictor, which are not shown in this article. The symmetric dependency explains why SIR is not able to find the first pHd predictor. The resulting inference based on pHd is therefore more reliable than the inference based on SIR.

When checking the predictors of SAVE, visual tools show a clear quadratic or even higher order polynomial dependency between the response and the first SAVE predictor. The second SAVE predictor is similar to the second pHd predictor, and the third SAVE predictor is similar to the first pHd predictor. Both SIR’s and pHd’s tests miss the first SAVE predictor.

Now apply SIMR to the ozone data. Bootstrap criterion picks up while -value criterion suggests . Nevertheless, both SIMR0.2 and SIMR0 lead to very similar estimated CDRS in this case (see Table 2). As expected , they recovers all the three SAVE predictors. Actually, those three estimated CDRS appear to be almost identical.

7 Discussion

SIMRα and SAVE are theoretically equivalent since that the subspaces spanned by their underlying matrices are identical. Nevertheless, simulation study shows that SIMRα with some chosen may perform better than SAVE. The main reason is that SAVE is only a fixed combination of the first two inverse moments. The simulation example in Section 5 implies that any fixed combination can not always be the winner. Apparently, SIMR0.6 can not always be the winner either. For example, if the simulation example is changed to , SIMRα with closer to will perform better. For practical use, multiple methods, as well as their combinations, should be tried and unified. SIMRα with provide a simple solution to it.

As a conclusion, we propose SIMR using weighted chi-squared tests as an important class of dimension reduction methods, which should be routinely considered during the search for the central dimension reduction subspace and its dimension.

Appendix

Proof of Lemma 1: By definition, , if . On the other hand, for any ,

Since only has finite dimension, there exists an with probability 1, such that,

Thus,

Proof of Corollary 2:

Proof Proposition 1: Define and for , then and . The rest of the steps follow the exactly same proof as in Yin and Cook (2002, A.3. Proposition 4).

Therefore, the asymptotic distribution of is determined only by the asymptotic distribution of .

The detail of , :

where ; ; ; ; ; ; ; ; .

References

- Bentler et al. (2000) Bentler, P.M., Xie, J., 2000. Corrections to test statistics in principal Hessian directions. Statistics and Probability Letters. 47, 381-389.

- Breiman et al. (1985) Breiman, L., Friedman, J., 1985. Estimating optimal transformations for multiple regression and correlation. J. Amer. Statist. Assoc. 80, 580-597.

- Bura et al. (2001) Bura, E., Cook, R.D., 2001. Extending sliced inverse regression: the weighted chi-squared test. J. Amer. Statist. Assoc. 96, 996-1003.

- Cook (1994a) Cook, R.D., 1994a. On the interpretation of regression plots. J. Amer. Statist. Assoc. 89, 177-189.

- Cook (1994b) Cook, R.D., 1994b. Using dimension-reduction subspaces to identify important inputs in models of physical systems. Proceedings of the Section on Physical and Engineering Sciences. Alexandria, VA: American Statistical Association. 18-25.

- Cook (1996) Cook, R.D., 1996. Graphics for regressions with a binary response. J. Amer. Statist. Assoc. 91, 983-992.

- Cook (1998a) Cook, R.D., 1998a. Principal Hessian directions revisited (with discussion). J. Amer. Statist. Assoc. 93, 84-100.

- Cook (1998b) Cook, R.D., 1998b. Regression Graphics, Ideas for Studying Regressions through Graphics. Wiley, New York.

- Cook et al. (2000) Cook, R.D., Critchley, F., 2000. Identifying regression outliers and mixtures graphically. J. Amer. Statist. Assoc. 95, 781-794.

- Cook et al. (2002) Cook, R.D., Li, B., 2002. Dimension reduction for conditional mean in regression. Annals of Statistics. 30, 455-474.

- Cook et al. (1999) Cook, R.D., Lee, H., 1999. Dimension-reduction in binary response regression. J. Amer. Statist. Assoc. 94, 1187-1200.

- Cook et al. (2005) Cook, R.D., Ni, L., 2005. Sufficient dimension reduction via inverse regression: A minimum discrepancy approach. J. Amer. Statist. Assoc. 100, 410-428.

- Cook et al. (1991) Cook, R.D., Weisberg, S., 1991. Discussion of ‘sliced inverse regression for dimension reduction’. J. Amer. Statist. Assoc. 86, 328-332.

- Cook et al. (1994) Cook, R.D., Weisberg, S., 1994. An Introduction to Regression Graphics. Wiley, New York.

- Cook et al. (2001) Cook, R.D., Yin, X., 2001. Dimension reduction and visualization in discriminant analysis (with discussion). Australian & New Zealand Journal of Statistics. 43, 147-199.

- Cramér (1946) Cramér, H., 1946. Mathematical Methods of Statistics. Princeton University Press, Princeton.

- Eaton et al. (1994) Eaton, M.L., Tyler, D.E., 1994. The asymptotic distributions of singular values with applications to canonical correlations and correspondence analysis. Journal of Multivariate Analysis. 50, 238-264.

- Gannoun et al. (2003) Gannoun, A., Saracco, J., 2003. Asymptotic theory for SIRα method. Statistica Sinica. 13, 297-310.

- Hastie et al. (2001) Hastie, T., Tibshirani, R., Friedman, J., 2001. The Elements of Statistical Learning: Data Mining, Inference, and Prediction. Springer.

- Li et al. (2007) Li, B., Wang, S., 2007. On directional regression for dimension reduction. J. Amer. Statist. Assoc. 102, 997-1008.

- Li (1991a) Li, K.-C., 1991a. Sliced inverse regression for dimension reduction (with discussion). J. Amer. Statist. Assoc. 86, 316-327.

- Li (1991b) Li, K.-C., 1991b. Rejoinder to ‘sliced inverse regression for dimension reduction’. J. Amer. Statist. Assoc. 86, 337-342.

- Li (1992) Li, K.-C., 1992. On principal Hessian directions for data visualization and dimension reduction: another application of Stein’s lemma. J. Amer. Statist. Assoc. 87, 1025-1039.

- Satorra et al. (1994) Satorra, A., Bentler, P.M., 1994. Corrections to test statistics and standard errors in covariance structure analysis. In: von Eye, A., Clogg C.C. (Eds.), Latent Variables Analysis: Applications for Developmental Research, 399-419, Sage, Newbury Park, CA.

- Satterthwaite (1941) Satterthwaite, F. E. (1941). Synthesis of variance. Psychometrika. 6, 309-316.

- Shao et al. (2007) Shao, Y., Cook, R.D., Weisberg, S., 2007. Marginal tests with sliced average variance estimation. Biometrika. 94,285-296.

- Weisberg (2002) Weisberg, S., 2002. Dimension reduction regression in R. Journal of Statistical Software. 7. Available from http://www.jstatsoft.org.

-

Weisberg (2009)

Weisberg, S., 2009.

The dr package.

Available from http://www.r-project.org. - Wen et al. (2007) Wen, X., Cook, R.D., 2007. Optimal sufficient dimension reduction in regressions with categorical predictors. Journal of Statistical Inference and Planning. 137, 1961-79.

- Wood (1989) Wood, A., 1989. An F-approximation to the distribution of a linear combination of chi-squared random variables. Communication in Statistics, Part B - Simulation and Computation. 18, 1439-1456.

- Yin et al. (2002) Yin, X., Cook, R.D., 2002. Dimension reduction for the conditional kth moment in regression. Journal of the Royal Statistical Society, Ser. B. 64, 159-175.

- Yin et al. (2003) Yin, X., Cook, R.D., 2003. Estimating central subspaces via inverse third moments. Biometrika. 90, 113-125.

- Ye et al. (2003) Ye, Z., Weiss, R.E., 2003. Using the bootstrap to select one of a new class of dimension reduction methods. J. Amer. Statist. Assoc. 98, 968-979.

| n=200 | ||||||||||

| SIR | SAVE | SIMRα | -pHd | |||||||

| Slice | 5 | 10 | 15 | 5 | 10 | 15 | 5 | 10 | 15 | - |

| 0.996 | 0.967 | 0.933 | 1.000 | 0.994 | 0.885 | 1.000 | 0.999 | 0.985 | 1.000 | |

| 0.050 | 0.053 | 0.102 | 0.561 | 0.379 | 0.152 | 0.892 | 0.855 | 0.760 | 0.277 | |

| 0.004 | 0.003 | 0.003 | 0.061 | 0.025 | 0.007 | 0.489 | 0.441 | 0.354 | 0.027 | |

| 0.001 | 0.000 | 0.000 | 0.003 | 0.001 | 0.000 | 0.032 | 0.022 | 0.026 | 0.005 | |

| mean() | 0.124 | 0.127 | 0.119 | 0.045 | 0.060 | 0.077 | 0.033 | 0.033 | 0.039 | 0.111 |

| n=400 | ||||||||||

| SIR | SAVE | SIMRα | -pHd | |||||||

| Slice | 5 | 10 | 15 | 5 | 10 | 15 | 5 | 10 | 15 | - |

| 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | |

| 0.039 | 0.050 | 0.108 | 0.983 | 0.974 | 0.888 | 1.000 | 1.000 | 0.993 | 0.293 | |

| 0.003 | 0.001 | 0.012 | 0.399 | 0.213 | 0.091 | 0.939 | 0.943 | 0.860 | 0.026 | |

| 0.001 | 0.000 | 0.000 | 0.015 | 0.013 | 0.010 | 0.052 | 0.040 | 0.033 | 0.002 | |

| mean() | 0.127 | 0.129 | 0.120 | 0.016 | 0.025 | 0.038 | 0.009 | 0.009 | 0.011 | 0.109 |

| n=600 | ||||||||||

| SIR | SAVE | SIMRα | -pHd | |||||||

| Slice | 5 | 10 | 15 | 5 | 10 | 15 | 5 | 10 | 15 | - |

| 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | |

| 0.054 | 0.062 | 0.053 | 1.000 | 1.000 | 0.998 | 1.000 | 1.000 | 1.000 | 0.328 | |

| 0.001 | 0.000 | 0.002 | 0.841 | 0.601 | 0.371 | 0.996 | 1.000 | 0.992 | 0.040 | |

| 0.001 | 0.000 | 0.000 | 0.021 | 0.019 | 0.013 | 0.048 | 0.034 | 0.031 | 0.006 | |

| mean() | 0.123 | 0.123 | 0.125 | 0.008 | 0.010 | 0.016 | 0.005 | 0.005 | 0.005 | 0.108 |

| First | Second | Third | Fourth | First | Second | Third | Fourth | |||

|---|---|---|---|---|---|---|---|---|---|---|

| -.113 | 0.333 | ( 0.183) | (-.194) | 0.635 | 0.126 | 0.096 | (-.124) | |||

| -.049 | 0.084 | ( -.018) | (-.012) | -.026 | -.031 | 0.015 | (-.026) | |||

| 0.826 | 0.939 | ( -.642) | (-.030) | -.665 | -.621 | -.664 | (-.143) | |||

| -.551 | -.031 | ( 0.745) | (0.981) | -.392 | -.773 | 0.741 | (0.981) | |||

| 0.652 | 0.169 | 0.092 | (0.125) | 0.685 | 0.204 | 0.092 | (-.125) | |||

| -.025 | -.032 | 0.015 | (0.026) | -.024 | -.031 | 0.015 | (-.026) | |||

| -.662 | -.803 | -.645 | (0.137) | -.653 | -.708 | -.653 | (-.141) | |||

| -.369 | -.571 | 0.758 | (-.982) | -.322 | -.676 | 0.751 | (0.982) |

Note: “()” indicates nonsignificant direction at level .