A Numerical Approach to the Estimation of Solutions of some Variational Problems with Convexity Constraints ††thanks: We thank Guillaume Carlier and Yves Lucet for their thoughtful comments and suggestions.

Abstract

We present an algorithm to approximate the solutions to variational problems where set of admissible functions consists of convex functions. The main motivator behind this numerical method is estimating solutions to Adverse Selection problems within a Principal-Agent framework. Problems such as product lines design, optimal taxation, structured derivatives design, etc. can be studied through the scope of these models. We develop a method to estimate their optimal pricing schedules.

Preliminary - Comments Welcome

AMS classification: 49-04, 49M25, 49M37, 65K10, 91B30, 91B32.

Keywords: Variational problems, convexity constraints, adverse selection, non-linear pricing, risk transfer, market screening.

1 Introduction

Arguably, Newton’s problem of the body of minimal resistance is the original variational problem with convexity constraints. It consists of finding the shape of a solid that encounters the least resistance when moving through a fluid. This is equivalent to finding a convex function from a convex domain (originally a disk) in to that minimizes a certain funtional (see section 2). Newton’s original “solution” assumed radial symmetry. This turned out to be false, as shown by Brock, Ferone and Kawohl in [3], which sparked new interest to the study of variational problems with convexity constraints. One can also find these kinds of problems in finance and economics. Starting in 1978 with the seminal paper of Mussa and Rosen [16], the study of non-linear pricing as a means of market screening under Adverse-Selection has produced a considerable stream of contributions ([1],[5],[17],…). In models where goods are described by a single quality and the set of agents is differentiated by a single parameter, it is in general possible to find closed form solutions for the pricing schedule. This is, however, not the case when multidimensional consumption bundles and agent types are considered. Although Rochet and Choné [17] provided conditions for the existence of an optimal pricing rule and fully characterized the ways in which markets differentiate in a multidimensional setting, they also pointed out that it is only in very special cases that one can expect to find closed form solutions. The same holds true for models where the set of goods lies in an infinite-dimensional space, even when agent types are one-dimensional. This framework was first used, to our knowledge, by Carlier, Ekeland and Touzi [5] to price financial derivatives traded “over-the-counter”. It was then extended by Horst and Moreno [11] to model the actions of a monopolist who has an initial risky position that she evaluates via a coherent risk measure, and who intends to transfer part of her risk to a set of heterogenous agents. In both cases the authors find that only very restrictive examples allow for explicit solutions.

Given that a great variety of problems, such as product lines design, optimal taxation, structured derivatives design, etc. can be studied through the scope of these models, there is a clear need for robust and efficient numerical methods that approximate their optimal pricing schedules. Note that this also provides an approximation of the optimal “products”. Most of the papers mentioned above eventually face solving a variational problem under convex constraints. This family of problems have lately been studied under different scopes. Carlier and Lachand-Robert [6] have studied the regularity of minimizers when the functional is elliptic and the admissible functions satisfy a Dirichlet-type boundary condition. Their results can be extended to of our examples. Lachand-Robert and Pelletier [15] characterize the extreme points of a functional depending only on over a set of convex functions with uniform convex bounds. In this paper we provide several variants of an algorithm, based on the idea of approximating a convex function by an affine envelope, to solve these types of problems. This deviates from previous work by Choné and Hervé [8] and Carlier, Lachand-Robert and Maury [7], where the authors use finite element methods. In the former case, a conformal (interior) method is used and a non-convergence result is given. As a consequence, the latter uses an exterior approximation method, which is indeed found to be convergent in the classical projection problem in Lachand-Robert and Oudet present in [14] and algorithm for minimizing functionals within convex bodies that shares some similarities to ours. For a particular problem, they start with an admissible polytope and iteratively modify the normals to the facets in order to find an approximate minimizer.

We estimate the minimizers for several problems with known, closed form solutions as a means of comparing the output of our method to the true solutions. These are taken from [17] and [5]. Finally, we provide an example in which we approximate the solution to a risk-minimization problem similar to the one presented in [11]. This is still based on the affine-envelope idea, but requires some additional methodology, since it involves solving a non-standard variational problem.

The remainder of this paper is organized as follows. In Section 2 we state our problem and provide some classical examples. Our algorithm and a proof of its convergence are presented in Section 3. In Section 4 we show the solutions obtained via our algorithm to several problems found in the literature. Since these problems share a common microeconomic motivation, we include a brief discussion on the latter. The examples include the well known “Rochet-Choné” problem, a one dimensional example from Carlier, Ekeland and Touzi and the risk transfer case for a principal who offers call options with type-dependent strikes and evaluates her risk via the “short fall” of her position. This section is followed by our conclusions. Finally a section devoted to technical results and all our codes are included in the appendix.

2 Setting

The aim of this paper is to present a numerical algorithm to approximate the solutions of some variational problems subject to convexity constraints. A classical example of the latter is Newton’s problem of the body of minimal resistance, which, given a smooth subset of consists of minimizing

over the set of convex functions We use the following notation throughout:

-

•

are convex and compact sets,

-

•

where is strictly convex and

-

•

-

•

Our objective is to (numerically) estimate the solution to

| (1) |

We assume is such that (1) has a unique solution (see, for example, [13]). Given the properties of and we immediately have the following

Proposition 2.1

Assume solves then there is in such that

Proof. Let (recall is compact)and define then

This would contradict the hypothesis of being a minimizer of over unless

It follows from proposition 2.1 that we can redefine to include only functions that have a root in This, together with the compactness of implies the following proposition, which we will use frequently.

Proposition 2.2

There exists such that for all in

It follows from Proposition 2.2 and the restriction on the gradients that for each choice of function problem has a unique solution, since the functional will be strictly convex, lower semi continuous and the admissible set is bounded (see [9]).

Remark 2.3

Our algorithm will still work with more general ’s as long as one can prove that the family of feasible minimizers is uniformly bounded.

3 Description of the Algorithm

From this point on, whenever we use supscripts we refer to vectors. For example On the other hand a subscript indicates a function to be evaluated over some closed, convex subset of of non-empty interior, ie, is a sequence of functions for some contained in

Assumption 3.1

We will consider

To find an approximate solution to we proceed as follows:

-

1.

We discretize the domain in the following way: We partition it into which consists of equal cubes of volume The elements of will be denoted by Now define as the set of centers of the ’s. The elements of will be denoted by The choice of a uniform partition is done for computational simplicity.

-

2.

We denote and associate such weight with

-

3.

We associate to each element of a non-negative number and an n-dimensional vector The former represents the value of and the latter

-

4.

We solve the (non-linear) program

(2) over the set of all vectors of the form and all matrices of the form such that:

-

(a)

(non-negativity),

-

(b)

for (feasibility),

-

(c)

(convexity).

If the problem in hand includes Dirichlet boundary conditions these can be included here as linear constraints that the ’s corresponding to points on the “boundary” of must satisfy.

-

(a)

-

5.

Let be the solution to We define where

-

6.

yields an approximation to the minimizer of

Remark 3.2

The constraints of the non-linear program determine a convex set.

Remark 3.3

4 (c) guarantees that is a supporting hyperplane of the convex hull of the points Note that is a piecewise affine convex function.

3.1 Convergence of the Algorithm

Proposition 3.4

Under the assumptions made on the problem has a unique solution.

Proof. The function

is strictly convex. It follows from proposition 2.2 that any acceptable vector-matrix pair must lie in which together with Remark 3.2 implies consists of minimizing a strictly convex function over a compact and convex set. The result then follows from general theory.

Proposition 3.5

There exists such that:

-

1.

The sequence generated by the ’s has a subsequence that converges uniformly to

-

2.

Proof. The bounded (Proposition 2.2) family is uniformly equicontinuous, as it consists of convex functions with uniformly bounded subgradients. By the Arzela-Ascoli theorem we have that, passing to a subsequence if necessary, there is a non-negative and convex function such that

By convexity almost everywhere (lemma A.5); since belongs to the bounded set the integrands are dominated. Therefore, by Lebesgue Dominated Convergence we have

Let be the maximizer of within Our aim is to show that is a minimizing sequence of problem in other words that

We need the following

Definition 3.6

Let be such that Given the lattice we define:

-

1.

-

2.

-

3.

and

-

4.

Notice that is also constructed as the convex envelope of a family of affine functions. The inequalities

| (3) |

| (4) |

follow from the definitions of and as does the following

Proposition 3.7

Let and be as above, then uniformly as

Proposition 3.8

For each there exist and such that

| (5) |

| (6) |

and as

| (7) |

The left-hand side of (5) can be written as

We can now prove the main theorem in this section, namely

Theorem 3.9

The sequence is minimizing for problem

4 Examples

In this section we show some results of implementing our algorithm. The first two examples reduce quadratic programs, whereas the third and fourth ones are non-linear optimization programs. All the computer coding has been written in MatLab. However, in both cases supplemental Optimization Toolboxes were used. In the first two examples we used the Mosek 4.0 Optimization Toolbox, wherease in the last two we used Tomlab 6.0. These four examples share a common microeconomic motivation, for which we provide an overview. We refer the interested reader to [2] for a comprehensive presentation of Principal-Agent models and Adverse Selection, as well as multiple references.

4.1 Some Microeconomic Motivation

Consider an economy with a single principal and a continuum of agents. The latter’s preferences are characterized by n-dimensional vectors. These are called the agents’ types. The set of all types will be denoted by The individual types are private information, but the principal knows their statistical distribution, which has a (non-atomic) density

Our model takes a hedonic approach to product differentiation. We assume goods are characterized by (n-dimensional) vectors describing their utility-bearing attributes. The set of technologically feasible goods that the principal can deliver will be denoted by and it will be assumed to be compact and convex. The cost to the principal of producing one unit of product is denoted by Products are offered on a take-it-or-leave-it basis, each agent can buy one or zero units of a single product and it is assumed there is no second-hand market. The (type-dependent) preferences of the agents are represented by the function

The (non-linear) price schedule for the technologically feasible goods is represented by

When purchasing good at a price an agent of type has net utility

Each agent solves the problem

By analyzing the choice of each agent type under a given price schedule the principal screens the market. Let

| (10) |

where belongs to Notice that for all in we have

| (11) |

Analogous to the concepts of subdifferential and convex conjugate from classical Convex Analysis, we have that the subset of where (11) is an equality is called the -subdifferential of at and is the -conjugate of (see, for example, [4]). We write

and

To simplify notation let A single pair is called a contract, whereas is called a catalogue. A catalogue is called incentive compatible if for all where is type’s non-participation (or reservation) utility. We normalize the reservation utility of all agents to zero, and assume there is always an outside option that denotes non-participation. Therefore we will only consider functions The Principal’s aim is to devise a pricing function as to maximize her income

| (13) |

Expression (13) is to be maximized over all pairs such that is U-convex and non-negative and Characterizing in a way that makes the problem tractable can be quite challenging. In the case where as in [17], for a given price schedule the maximal net utility of an agent of type is

| (14) |

Since is defined as the supremium of its affine minorants, it is a convex function of the types. It follows from the Envelope Theorem that the maximum in equation (14) is attained if and we may write

| (15) |

The principal’s aggregate surplus is given by

| (17) |

over the set

4.2 The Musa-Rosen Problem in a Square

The following structures are shared in the first two examples:

-

•

this structure will determine any possible candidate for a minimizer to in the following way: is a vector of length that will contain the approximate values of the optimal function evaluated on the points of the lattice. The vector has length and it contains what will be the partial derivatives of at the same points

-

•

is a vector of length The product provides the discretization of the integral

-

•

is the matrix of constraints. The inequality imposes the non-negativity of and and the convexity of the resulting

Remark 4.1

The density is “built into” vector and the cost function

Let and assume the types are uniformly distributed. This is our the benchmark problem, since the solution to the principal’s problem can be found explicitly [17]. In this case we have to solve the quadratic program

subject to

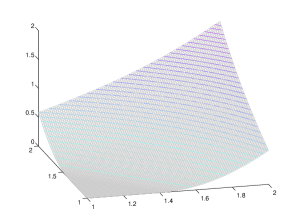

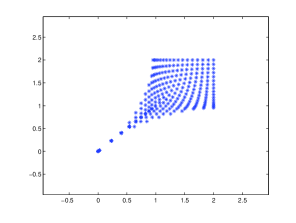

is a matrix whose first columns are zero, since does not enter the cost function; the four blocks towards its lower right corner form a identity matrix. Therefore is a discretization of Figure 1(a) was produced using a -points lattice and a uniform density, whereas Figure 2(b) shows the traded qualities.

4.3 The Musa-Rosen Problem with a Non-uniform Density

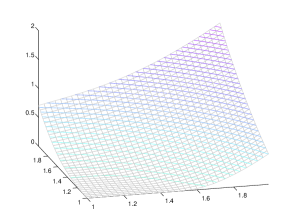

We keep the cost function of the previous example, but now assume the types are distributed according to a bivariate normal distribution with mean and variance-covariance matrix

As noted before, the weight assigned to each to each agent type is built into and so the vector remains unchanged. We obtain figure 2(a).

Remark 4.2

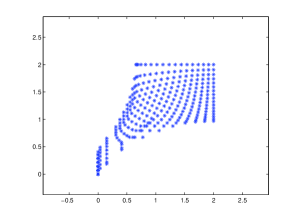

It is interesting to see that in this case bunching of the second kind, as described by Roché and Choné in [17], appears to be eliminated as a consequence of the skewed distribution of the agents. This can be seen in the non-linear level curves of the optimizing function This is also quite evident in the plot of the qualities traded, which is shown below.

The MatLab programs for the two previous examples were run on MatLab 7.0.1.24704 (R14) in a Sun Fire V480 (41.2 HGz Ultra III, 16 GB RAM) computer running Solaris 2.10 OS. In the first example 57.7085 seconds of processing time were required. The running time in the second example was 81.7280 seconds.

4.4 An example with Non-quadratic Cost

In this example we approximate a solution to the problem of a principal who is selling over-the-counter financial derivatives to a set of heterogeneous agents. This model is presented by Carlier, Ekeland and Touzi in [5]. They start with a standard probability space and the types of the agents are given by their risk aversion coefficients under the assumption of mean-variance utilities; namely, the set of agent types is and the utility of an agent of type when facing product is

Under the assumptions of a zero risk-free rate and that the principal has access to a complete market, her cost of delivering product is given by where is the variance of the Radon-Nikodym derivative of the (unique) martingale measure, and Var The principal’s problem can be written as

| (18) |

where Figure 3 shows an approximation of the maximizing using 25 agent types.

4.5 Minimizing Risk

The microeconomic motivation for this section is the model of Horst & Moreno [11]. We present an overview for completeness. The principal’s income, which is exposed to non-hedgeable risk factors, is represented by The latter is a bounded random variable defined on a standard, non-atomic, probability space The principal’s goal is to lay off parts of her risk with the agents whose preferences are mean-variance. The agent types are indexed by their coefficients of risk aversion, which are assumed to lie for some The principal underwrites call options on her income with type-dependent strikes:

If the principal issues the catalogue , she receives a cash amount of and is subject to the additional liability She evaluates the risk associated with her overall position

via the “entropic measure” of her position, i.e.

where for some The principal’s problem is to devise a catalogue as to minimize her risk exposure. Namely, she chooses a function and contracts from the set

in order to minimize

where

We assume the set of states of the World is finite with cardinality Each possible state can occur with probability The realizations of the principal’s wealth are denoted by Note that and are treated as known data. The objective function of our non-linear program is

where denotes the vector of type dependent strikes. We denote by the total number of constraints. The principal’s problem is to find

where determines the constraints that keep within the set of feasible contracts. Let be the uniformly distributed agent types, and

-

•

-

•

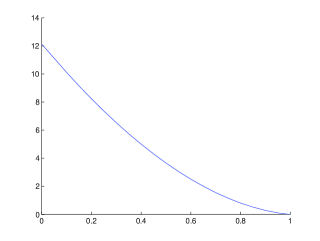

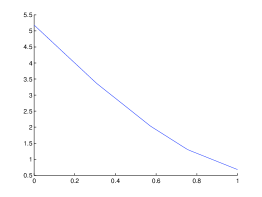

The principal’s initial evaluation of her risk is . The following are the plots for the approximating and the strikes:

Note that for illustration purposes we have changed the scale for the agent types in the second plot. The interpolates of the approximate to the optimal function and the strikes are:

| 4.196344 | |

|---|---|

| 3.234565 | |

| 2.321529 | |

| 1.523532 | |

| 0.745045 | |

| 0.010025 |

| 1.078869 | |

|---|---|

| 0.785079 | |

| 0.733530 | |

| 0.713309 | |

| 0.713309 | |

| 0.713309 |

The Principal’s valuation of her risk after the exchanges with the agents decreases from to

Remark 4.3

Notice the ”bunching” at the bottom.

5 Conclusions

In this paper we have developed a numerical algorithm to estimate the minimizers of variational problems with convexity constraints, with our main motivation stemming from Economics and Finance. Ours is an internal method, so at each precision level the approximate minimizers lie within the acceptable set of functions. Our examples are developed over one or two dimensional sets for illustration reasons, but the algorithm can be implemented in higher dimensions. However, it must be mentioned that, as is the case with the other methods found in the related literature, implementing convexity has a high computational cost which increases geometrically with dimension.

6 Appendix

Appendix A Some technical results

In order to prove convergence of our algorithm we make use of the Convex Analysis results contained in this section. We will work on an open and convex subset of

Definition A.1

A mapping (the power set of ) is said to be set valued if for each in is a non-empty subset of

Recall that if is a convex function, then the subdifferential of at defined as

is a non-empty subset of for all in Therefore, the set valued mapping

is well defined on Notice that if for some in we have then

In such case we say the subdifferential mapping is single valued at and we can simply identify it with the gradient of at

Definition A.2

Let be a set valued function. Then we say is differentiable at iff there is a linear mapping such that for all there is such that if and then

The following theorem is due to Alexandrov ( [12])

Theorem A.3

Let be convex, then se set valued function is differentiable almost everywhere.

Clearly, in the case where is single valued, definition A.2 is equivalent to the regular definition of a Fréchet differentiable function. Moreover if differentiable at and we choose in and let in definition A.2 we get

which implies is single valued at It follows from Alexandrov’s Theorem and the observation above that for almost all the set valued mapping can be identified with the single valued assignment and we have the following

Corollary A.4

Let be convex . Then the mapping

is well defined and continuous almost everywhere.

Proposition A.5

Let be a convex, open set. Assume the sequence of convex functions converges uniformly to then almost everywhere on

Proof. Denote by the derivative of in the direction of The convexity of and implies the existence of a set with such that the partial derivatives of and exist and are continuous in Let To prove that consider such that Since is convex

for all Hence

The left-hand side of this inequality is equal to

For let be such that

for Let be such that

Hence, taking we have that for all

Hence

for all The same argument shows that

for all and all which concludes the proof.

Proposition A.6

Let be a convex, compact set and let be a convex function such that for all the subdifferentials are contained in for some compact set Then there exists such that and uniformly on U.

Proof. Fix and define

Extend to be defined on Let be a family of mollifiers (see, for instance [13]), then the functions

are convex, smooth and they converge uniformly to on as long as is small enough so that

is contained in Let be such that then the sequence has the required properties.

Lemma A.7

Consider where and is a compact convex subset of Let be a family of convex functions such that for all and whose uniform limit is Let be the uniform partition of consisting of cubes of volume Denote by be the elements of and let

be the corresponding Riemann sum approximating where and Then for any there is such that

| (19) |

for any

Proof. By lemma A.6, for each there exists a sequence of continuously differentiable convex functions such that

Let be the first element in such that and for all where is continuous. Then uniformly, and by Lemma A.5 we have that a.e. It follows from Egoroff’s theorem that for every there exists a set such that:

Let be the indicator function of and define

Fix consider and let be the sequence of ’s converging to as the partition is refined. By uniform convergence, is continuous on hence

| (20) |

It follows from (20) and the continuity of that almost everywhere on Notice that as a consequence of the compactness of and and the definition of we have

and

for some and all where is continuous. Therefore

| (21) |

By Lebesgue Dominated Convergence

moreover, the definition of implies

Given take such that and such that

Then equation (19) holds for all

Appendix B MatLab code for the examples in section 4

References

- [1] Armstrong, M.: Multiproduct Nonlinear Pricing, Econometrica, 64, 51-75, 1996.

- [2] Bolton, P., Dewatripoint, M.: Contract Theory, MIT press, 2005.

- [3] Brock, F.,Ferone, V., Kawohl, B.: A Symmetry Problem in the Calculus of Variations, Calc. Var. Partial Differential Equations, 4, 593-599, 1996.

- [4] Carlier, G.: Duality and Existence for a Class of Mass Transportation Problems and Economic Applications, Advances in Mathematical Economics 5, 1-21, 2003.

- [5] Carlier, G., Ekeland, I & N. Touzi: Optimal Derivatives Design for Mean-Variance Agents under Adverse Selection, Preprint, 2006.

- [6] Carlier, G. & Lachand-Robert:Regularity of Solutions for some Variational Problems Subject to a Convexity Constraint, Communications on Pure and Applied Mathematics, vol 54-5, 583-594, 2001.

- [7] Carlier, G. & Lachand-Robert, T. & Maury, B.: A Numerical Approach to Variational Problems Subject to Convexity Constraints, Numerische Mathematik, 88, 299-318, 2001.

- [8] Choné, P. & Hervé, V. J.: Non-Convergence Result for Conformal Approximation of Variational Problems Subject to a Convexity Constraint, Numerical Functional Analysis and Optimization, 22:5, 529-547, 2001.

- [9] Ekeland, I. & Témam, R., Convex Analysis and Variational Problems, Classics in Applied Mathematics, 28, SIAM, 1976.

- [10] Föllmer, H. & A. Schied: Stochastic Finance. An Introduction in Discrete Time, de Gruyter Studies in Mathematics, 27, 2004.

- [11] Horst, U. & Moreno, S.: Risk Minimization and Optimal Derivative Design in a Principal Agent Game, Submitted, 2007.

- [12] Howard, R.: Alexandrov’s Theorem on the second derivatives of convex functions via Rademacher’s theorem on the first derivatives of Lipschitz functions, Lecture Notes, howard@math.sc.edu, 1998.

- [13] Giaquinta, M. & Hildebrandt, S.: Calculus of Variations 1, Grundlehren der mathemtischen Wissenschaften 310, Springer-Verlag, 1996.

- [14] Lachand-Robert, T. & Oudet, É.: Minimizing within Convex Bodies Using a Convex Hull Method, Siam Journal on Optimization, vol 16-2, 368-379, 2005.

- [15] Lachand-Robert, T. & Peletier, A.: Extremal Points of a Functional on the Set of Convex Functions, Proceedings of the American Mathematical Society, vol. 127-6, 1723-1727, 1999.

- [16] Mussa M. & S. Rosen: Monopoly and Product Quality, Journal of Economic Theory, 18, 301-317, 1978.

- [17] Rochet, J.-C. & P. Choné: Iroining, Sweeping and Multidimensional Screening, Econometrica,66, 783-826, 1988.