Finite-time singularity in the evolution of hyperinflation episodes

Abstract

A model proposed by Sornette, Takayasu, and Zhou for describing hyperinflation regimes based on adaptive expectations expressed in terms of a power law which leads to a finite-time singularity is revisited. It is suggested to express the price index evolution explicitly in terms of the parameters introduced along the theoretical formulation avoiding any combination of them used in the original work. This procedure allows to study unambiguously the uncertainties of such parameters when an error is assigned to the measurement of the price index. In this way, it is possible to determine an uncertainty in the critical time at which the singularity occurs. For this purpose, Monte Carlo simulation techniques are applied. The hyperinflation episodes of Peru (1969-90) and Weimar Germany (1920-3) are reexamined. The first analyses performed within this framework of the very extreme hyper-inflations occurred in Greece (1941-4) and Yugoslavia (1991-4) are reported. The study of the hyperinflation spiral experienced just nowadays in Zimbabwe predicts a singularity, i.e., a complete economic crash within two years.

pacs:

02.40.Xx Singularity theory; 02.50.Ng Monte Carlo methods in probability theory and statistics; 05.10.Ln Monte Carlo methods statistical physics and nonlinear dynamics; 64.60.F- Critical exponents; 89.20.-a Interdisciplinary applications of physics; 89.65.Gh Econophysics; 89.65.-s Social systemsI Introduction

Since about one decade there is significant interest in applications of physical methods in social and economical sciences stauffer99 ; stanley99 ; sornette03b . For example, it has been found that the logarithmic change of the market price in the case of a hyperinflation episode shows some universal characteristics similar to those observed in physical systems. In such a regime the price index increases more rapidly than a simple exponential law mizuno02 . Moreover, it has been shown that such a super-exponential law indeed finishes with a finite-time singularity sornette03 like several physical systems.

Let us recall that the rate of inflation is defined as

| (1) |

where is the price at time and is the period of the measurements. In economics the terminology “hyperinflation” is used in rather rough sense to specify very hight inflation that is “out of control”, a condition in which prices increase rapidly as a currency loses its property as medium of exchange, store of value, and unit of account. No precise definition of hyperinflation is universally accepted. One simple definition requires a monthly inflation rate of 20 or or more. In informal usage the term is often applied to much lower rates. In 1956, Cagan published The Monetary Dynamics of Hyperinflation cagan56 , generally regarded as the first serious study of hyperinflation and its effects. There it is defined that “inflation rates per month exceeding ” determine a scenario of hyperinflation.

During periods of very hight inflation the frequent change of prices destroys rapidly the real wages and the unknown future of the economic structure diminishes the flow of inversions. Such situations are very costly to society, the workers have to be paid more frequently (even daily) and there are rushes to spend the currency before prices rise further causing enormous “shoe-leather costs” (in economics it means: resources wasted when inflation encourages people to do more trips to banks and stores wearing out their shoes). These effects are accompanied with a strong devaluation of the currency which causes a decline in real public revenues increasing the fiscal deficit. Hyperinflation reduces real value of taxes collected, which are often set in nominal terms and by the time they are paid, real value has fallen. This feature is known as the Olivera-Tanzi effect, after Olivera olivera67 and Tanzi tanzi77 who were the first to interpret it by means of standard analytical tools canavese92 . The occurrence of the Olivera-Tanzi effect may impulse a rapid expansion of nominal money and credit. If people expect a money supply growth, then this would lead to expecting higher inflation. The expectation of higher inflation raises inflation rate even if money growth does not actually increase. Once people start to expect an inflation regime, their expectations may lead to strong positive feedbacks that make inflation run away. This scenario produce an important crisis in the population. The real investment, loans and development diminish, while the unemployment and political unrest grow significantly. Moreover, some of these effects usually continue after the hyperinflation has been stopped. Therefore, models of hyperinflation are considered very useful by macro-economists because detecting hyperinflation in an early stage might contribute to avoid such a tragedy.

There are several remarkable historical examples of hyperinflation. Some of them were originated after World Wars cagan56 . The most famous and studied cases are those occurred in Germany and Hungary in the early 1920’s after World War I and in Hungary at the end of World War II. However, there are other extreme examples, for instance, that of Greece during the military occupation () cagan56 ; palairet00 ; lykogiannis02 . On the other hand, there were other cases which are not related to wars like that in Latin America in the 1980’s imf ; sargent06 and more recently that occurred during the transition period from a Centrally Planned economy to a more Free Market oriented economy in countries of East Europe and in the successor states emerged after the dissolution of the Soviet Union imf .

As a matter of fact, the end of Central Planning in Europe - whether it came as a result of slow decay or of rapid collapse - was frequently accompanied by bursts of high inflation. An important example of such a behavior is Yugoslavia, where two periods of very hight inflation in short time were experienced. The first had a long build-up during the 1980’s and peaked in 1989 reaching high, but not very extreme inflation only briefly. The second one developed just at the end of Centrally Planed economy and enhanced by the Civil War is the worst episode of hyperinflation in History. This very severe hyperinflation occurred in the period petrovic00 ; nielsen04 .

The inflation rates at the end of extreme hyper-inflations reached very impressive amounts per month. For instance, the ratios of price indexes for the most severe known incidents of inflation quoted by Cagan cagan56 are: in Germany in 1923 (November-13th)/(October-16th)=102.556, i.e., inflation rose about percent per month; in Greece after liberation from the occupation by German troops in 1944 the ratio (November-10th)/(October-31th)=105.932 means percent per ten days and in Hungary after the end of World War II in 1946 (end-July)/(end-June)=1014.6226 corresponds to percent per month.

Despite all the unpleasant experiences with hight inflation, sometimes, it is still considered to be the apple of paradise. Since 2000 Zimbabwe exhibits an increasing high inflation rate zrb , which is already the highest in the world. Indeed, the spiral of price growth developed in that country is nowadays considered an important episode of hyperinflation.

Since a long time ago it is known that in the case of moderate inflation the prices exhibit an exponential growth cagan56 . A recent analysis of the hyperinflation in Germany, Hungary, Brazil, Israel, Nicaragua, Peru, and Bolivia performed by Mizuno, Takayasu, and Takayasu mizuno02 indicated that the price indexes or currency exchange rates of these countries grew according to a double-exponential function of time (with ). It was shown that this super-exponential growth can be obtained from a nonlinear positive feedback process in which the past market price growth influences the people’s expected future price, which itself impacts the a posteriori realized market price. This process is fundamentally based on the mechanism of “adaptive inflationary expectation” and it is similar to the positive feedbacks occurring during transmission of information due to imitative and herd behaviors sornette03b ; zimmermann00 .

The double-exponential model of Mizuno et al. mizuno02 gives a useful mathematical description of hyperinflation, however, it does not provide a rigorous determination of the end of the hyperinflation regime. More recently, Sornette, Takayasu, and Zhou sornette03 re-examined the theory developed in Ref. mizuno02 and showed that the double-exponential law is in fact a discrete-time approximation of a general power law growth endowed with a finite-time singularity at some critical time .

Let us notice that singularities occur in different sorts of dynamical systems and are spontaneously reached in finite time. Such a behavior can be found in models of either physical or other kind of systems. In the case of physics we can mention the Euler equations of inviscid fluids bhattach95 , the surface curvature on the free surface of a conducting fluid in an electric field zubarev98 , the equations of General Relativity coupled to a mass field leading to the formation of black holes choptuik99 , the vortex collapse of systems of point vortexes leoncini00 , or the Euler s disks as a rotating coin mocatt00 . On the other hand, this kind of singularity is also present in models of micro-organisms aggregating to form fruiting bodies rascle95 and in the dynamics of the world population, and the economic and financial indexes johansen00 .

The analysis of the finite-time singularity proposed in Ref. sornette03 allows to determine the theoretical end of the hyperinflation regime. However, from the practical point of view it is also important to estimate an uncertainty of in terms of variations of . An analysis of this issue is just developed in the present work.

In Sec. II we revise the theoretical formulations published in Refs. mizuno02 ; sornette03 introducing a careful treatment of the initial time of the series of data . The price index evolution is expressed explicitly in terms of the free parameters introduced along the theoretical formulation avoiding any combination of them. In addition, we propose a procedure to determine the uncertainties of the fitting parameters when an error is assigned to the measurement of the price index. Monte Carlo simulation techniques are used for the error analysis. In this way quotes for are set. A study of the hyperinflation in Peru and Germany are presented as testing cases. In Sec. III we report the first studies of the very extreme hyper-inflations of Greece and Yugoslavia performed within the framework outlined in the present work. Furthermore, on the basis of an analysis of data of the current trend of the hyperinflation in Zimbabwe, we predict an economic crash in this country in about two years. Finally, the main conclusions are summarized in Sec. IV.

II Theoretical background

In the academic financial literature, the simplest and most robust way to account for inflation is to take logarithm. Therefore, the continuous rate of change in prices is usually defined as

| (2) |

Usually the derivative of Eq. (2) is expressed in a discrete way as

| (3) |

The growth rate of price over one period is defined as

| (4) |

Here, a notation widely utilized in the academic literature, , is introduced. When takes big values over a large period of time a hyperinflation regime is to be reached.

In his pioneering work, Cagan cagan56 proposed a model of inflation based on the mechanism of “adaptive inflationary expectation” of positive feedback between realized growth of the market price and the growth of people’s averaged expectation price . These two prices are thought to evolve due to a positive feedback mechanism: an upward change of market price in a unit time induces a rise in the people’s expectation price , and such an anticipation pulls up the market price.

Cagan’s assumption that the growth rate of is proportional to the past realized growth rate of the market price is expressed by the following equation

| (5) |

| (6) |

Now, one may introduce

| (7) |

So, expressions (5) and (6) are equivalent to

| (8) |

| (9) |

whose solution is which indicates a constant finite growth rate equal to its initial value . Since the market price is given by

| (10) |

Eqs. (8) and (9) lead to a steady state exponential inflation

| (11) |

where . This form can be reduced to a linear form in

| (12) |

where

| (13) |

is the initial growth in prices.

II.1 Double-exponential growth

Mizuno et al. mizuno02 have analyzed the hyperinflation of Germany (), Hungary (), Brazil (), Israel (), Nicaragua (), Peru () and Bolivia (), and showed that the price indexes or currency exchange rates of these countries grew super-exponentially according to a double-exponential function of time (with ). These authors generalized Eq. (7) writing

| (14) |

which can be expressed as

| (15) |

Cagan’s original model is recovered for the special case . An exponent larger than avoids systematic errors of other models capturing the fact that the adjustment of the expected price is weak for small changes of the realized market prices and becomes very strong for large deviations.

The system of Eqs. (8) and (15) gives

| (16) |

In the continuous limit it becomes

| (17) |

with . The solution is

| (18) |

Upon introducing this result into Eq. (10) one gets the double exponential form for the market price

| (19) |

A straightforward calculation shows that in the limit the simple exponential of Eq. (11) is recovered. For one gets the expression of Ref. mizuno02

| (20) |

with .

II.2 Finite-time singularity

A further generalization of the Cagan’s model has been reported by Sornette et al. sornette03 . These authors proposed a different version of the nonlinear feedback process. They kept expression (5) or equivalently Eq. (8) and replaced Eq. (14) or equivalently expression (15) by

| (21) |

Note that this formulation (21) retrieves both previous proposals: the Cagan’s formulation (9) is get for and the Mizuno et al.’s form (15) is obtained for .

The authors of Ref. sornette03 claim that their formulation better captures the intrinsically nonlinear process of the formation of expectations. Indeed, if is small (explicitly, if is is smaller ), the second nonlinear term in the right-hand-side of (21) is negligible compared with the first Cagan’s term and one recovers the exponentially growing inflation regime of normal times. However, when the realized growth rate becomes significant, people’s expectations start to amplify these realized growth rates, leading to a super-exponential growth. Geometrically, the difference between the formulation of Eq. and that of Eq. consists in replacing a straight of slope larger than by a upwards convex function with slope at the origin and whose local slope increases monotonically with the argument.

This theory provides the first practical approach for predicting its future path until its end. In practice, the end of an hyperinflation regime is expected to occur somewhat earlier than at the asymptotic critical time , because governments and central banks are forced to do something before the infinity is reached in finite time. Such actions are the equivalent of finite-size and boundary condition effects in physical systems undergoing similar finite-time singularities. Hyperinflation regimes are of special interest as they emphasize in an almost pure way the impact of collective behavior of people interacting through their expectations.

II.2.1 Determination of the critical time

Putting Eq. (8) together with expression (21) leads to

| (22) |

Taking the continuous limit, expression (22) becomes

| (23) |

where is a positive coefficient with dimensions of the inverse of time. In this case the growth rate accelerates with time according to . As a consequence of this power law acceleration the solution of Eq. (23) exhibits singularities in finite-time bender78

| (24) |

The critical time is determined by the initial condition , the exponent , and the coefficient

| (25) |

We must notice that in Ref. sornette03 there are misprints: i) the coefficient should be dropped from Eq. (14) and ii) the expression for given just below that equation is incorrect. See, for instance, Eq. (17) in Ref. ike02 .

A power law singularity is essentially indistinguishable from an exponential of an exponential of time, except when the distance from the finite time singularity becomes comparable with the time step . The main difference between the formulations proposed by Mizuno et al. mizuno02 and Sornette et al. sornette03 is that the latter one contains an information on the end of the growth phase, embodied in the existence of the critical .

The time dependence of the market price exhibits the two different regimes depending on the sign of :

(i) For one gets yielding a finite-time singularity in the market price itself

| (28) |

In this regime the price exhibits a finite-time singularity at the same critical value as the growth rate. Hence, this solution corresponds to a genuine divergence of .

(ii) For one gets yielding a finite-time singularity in but the market price evolve as

| (29) | |||||

with

| (30) |

Here it holds . As time approaches the critical value the price converges to the value leading to equilibrium, this limit is reached more rapidly when .

Let us now discuss the structure of Eq. (28) written in the form

| (31) |

By fitting the measured price index to this expression one can determine the critical time together with the parameters and . However, since at the square bracket vanishes, by using explicitly the assumed (measured) , i.e. setting , one would perform a fit with a fixed point at the beginning of the hyperinflation episode which may bias the fitting procedure for . Therefore, it is convenient to consider as an additional free parameter. On the oder hand, Eq. (31) leads to Eq. (15) of Ref. sornette03

| (32) | |||||

where

| (33) |

and

| (34) |

Notice that in the formulation proposed in the present work, see Eq. (31), all the free parameters have their own physical meaning: is the logarithm of ; is the initial growth in price; is fixed by the exponent of the power law; and is the end-point time of hyperinflation. While in the case of Eq. (15) of Sornette et al. sornette03 the coefficients and are combinations of that parameters. This fact becomes important for an error analysis.

II.2.2 Estimation of uncertainties

Before analyzing hyperinflation episodes, we shall focus attention on an important issue. Indeed, the determination of the fitting parameters cannot be considered as unambiguous. Therefore, besides giving the critical time and other parameters, it is also of interest to provide an estimation of its uncertainties. Hence, in the present work we analyzed the variation of the free parameters when one takes into account an uncertainty in the measured rate of inflation . The tabulated price index at a given time is evaluated according to a formula derived from Eq. (1)

| (36) |

where is usually fixed at unity, i.e., is set zero. By assuming that each measured has an uncertainty it is possible to assign an uncertainty to . However, instead of evaluating , we preferred to estimate directly the error of the fitting parameters.

For this purpose, we assumed that each value of the inflation rate can be represented by a gaussian distribution with mean value and a standard deviation . These distributions were sampled by using Monte Carlo techniques in order to get for each a random series of values with . The size of these series was taken large enough to satisfy to a good approximation

| (37) |

and

| (38) |

In this way generations of inflation rates were built, each one is labeled by and composed of the obtained values for all . Then each generation was fitted to Eq. (31) providing sets of fitting parameters , , , and . In order to speedup the procedure programs like those included in Ref. bevington may be used. Finally, for each parameter the average value and variance were evaluated by using expressions like that of Eqs. (37) and (38). These averages , , , and were compared with the values , , , and yielded by a direct fit of the tabulated , and the corresponding differences were evaluated. When all the ratios of these differences over the corresponding standard deviations were smaller that the obtained results have been accepted.

To perform this kind of error analysis in the case of a fit to Eq. (15) of Sornette et al. sornette03 would not be appropriate because both coefficients and depend explicitly on the remaining parameters and and therefore their errors would be strongly correlated.

| Country | Currency | Period | Parameters | Ref. | ||||

|---|---|---|---|---|---|---|---|---|

| Peru111Inflation data are taken from a Table published by the International Monetary Fund (IMF) imf . | Inti | 1969-1990 | 0.322 | PW | ||||

| 1991.29 | 0.3 | 0.291 | sornette03 | |||||

| Zimbabwe222Inflation data are taken from Ref. zrb . | ZW-Dollar | 1980-2007 | 0.234 | PW | ||||

| Germany333Inflation data are taken from Ref. cagan56 . | Mark | 1920:01-1921:05 | 0.076 | PW | ||||

| 1921:05-1923:11 | 1924:01:0511 | 0.580 | PW | |||||

| 1920:01-1923:11 | 1923:12:18 | 0.6 | 0.490 | sornette03 | ||||

| Greeceb | Drachma | 1941:04-1942:10 | 0.124 | PW | ||||

| 1943:02-1944:10 | 1944:12:0213 | 0.230 | PW | |||||

| Yugoslavia444Inflation data are taken from Ref. petrovic00 . | Dinar | 1990:12-1994:01 | 1994:03:104 | 0.930 | PW | |||

| Country | Parameters | Ref. | |||

|---|---|---|---|---|---|

| Peru | year | -14.16 | 34. | PW | |

| -14.17 | 34. | 1.8 | sornette03 | ||

| Zimbabwe | year | PW | |||

| Germany | month | -5.22 | 274.555For the evaluation of this quantity time is taken in days. | PW | |

| -5.09 | 272.a | 1.6 | sornette03 | ||

| Hungary | -1.02 | 2370.a | 1.5 | sornette03 | |

| Greece | month | -21.62 | 78.a | PW | |

| Yugoslavia | month | -25.69 | 1030.a | PW | |

III Analysis and numerical results

In a first step, before beginning the analysis of the episodes announced in Sec. I, we shall describe the application of our procedure to cases already treated by Sornette et al. sornette03 . In particular, we shall report the studies of the hyperinflation cycles of Peru and Weimar Germany. The first case is a process developed over two decades, while the latter one was build-up over a couple of years only. In this way the selected checking examples cover the evolution characterizing the cases to be analyzed for the first time within the framework outlined above.

Next, we shall analyze the very extreme cases of Greece and Yugoslavia. Furthermore, we shall deal with the hyperinflation exhibited nowadays by the economic system in Zimbabwe. This case is very encouraging because the spiral of increasing prices is not finished yet. Hence, an a priori prediction for the critical time can be made.

At the end of the section we shall compare the most severe hyper-inflations.

III.1 Checking cases

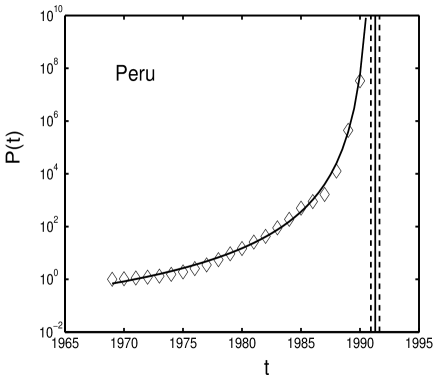

Figure 1 shows the price index of Peru during the period 1969-90. The parameters obtained from a mean-square fit of these data to Eq. (31) together with the root-mean-square residue of the fit, , are quoted in Table 1. In order to facilitate a quantitative comparison with the analysis of Sornette et al. sornette03 their values of and are included in Table 1, while that of and are quoted in Table 2 together with our evaluations by means of Eqs. (33) and (34). A glance at these tables indicates a perfect agreement between both fits. The quality of the fit can be observed in Fig. 1, this figure is to be compared with Fig. 2 of Ref. sornette03 .

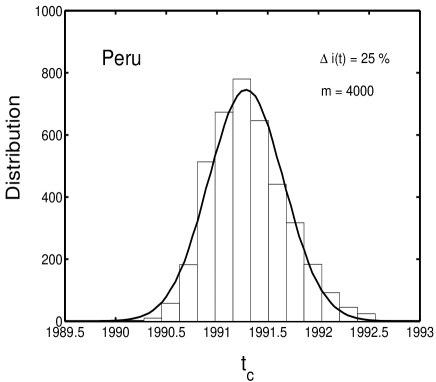

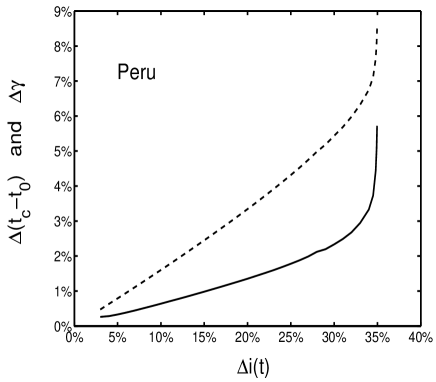

For the analysis of the uncertainties we assumed that all have the same relative error . The relative errors of the parameters were determined as a function of according the procedure outlined in Sec. II.2.2. The requirements of Eqs. (37) and (38) are reached satisfactorily well for . The distribution of results for obtained by solving Eq. (31) for each generation of built up from Monte Carlo samplings at is displayed in Fig. 2 together with the corresponding gaussian distribution. This comparison shows a fair agreement. For bigger the distribution becomes asymmetric exhibiting a repulsion towards larger and the standard deviation increases dramatically. This effect is shown in Fig. 3, where the results for “the most important parameters”, i.e., the critical time and exponent of the power law for the growth rate

| (39) |

obtained for and are plotted. These data indicate that the uncertainties of the parameters are to a good approximation linear functions up to , then increase dramatically. At a distribution equivalent to that displayed in Fig. 2 differs from a gaussian. In this work we adopted as a reasonable relative error of the measured . The uncertainties of the fitting parameters quoted in Table 1 correspond to that quote. The uncertainty of is also displayed in Fig. 1.

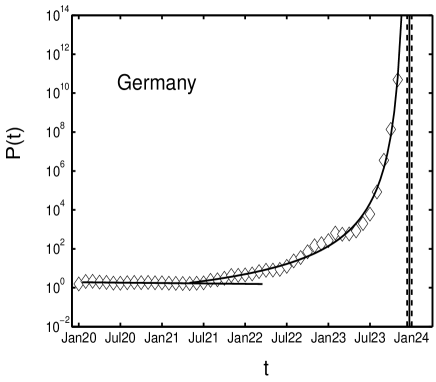

Sornette et al. sornette03 have analyzed the evolution of the exchange rate between the German Mark and the US dollar during the period 1920:01-1923:11 (from now on when dealing with monthly data the notation Year:Month:Day will be used). The fit of all that data to Eq. (32) yielded the values quoted in the present Tables 1 and 2. In order to compare these results with that provided by an alternative information, we analyzed the evolution of the price index taking the data from Table B3 of Ref. cagan56 . Figure 4 shows the price index of Germany during the period 1920:01-1923:11, the open diamonds are values normalized to . A comparison of this figure with Fig. 4 of Ref. sornette03 indicates that the cumulated price index over the considered period is similar to the total variation of the exchange rate. It is important to point out that data of the exchange rate were taken at the beginning of each month, while the values of the price index correspond to the middle of the month.

A careful analysis of price index indicates that during the period 1920:01 to 1921:05 the cumulated inflation is approximately zero. This regime can be well described by the original theory of Cagan condensed in Eq. (12), which can be cast into the form

| (40) |

A fit to this equation yielded the values of and given in Table 1, where the uncertainties corresponding to an error of in the measured are also quoted. The quality of the fit may be observed in Fig. 4. The slightly negative slope is due to the fact that in this period several months exhibit deflation. Consequently, in order to study the hyperinflation episode we fitted to Eq. (31) data of the period 1921:05 to 1923:11 only. This procedure yielded the values of the free parameters and the listed in Table 1. The quality of the fit may be observed in Fig. 4 and it is similar to that obtained in Ref. sornette03 as indicated by the values of . The evaluated results of and are included in Table 2 (for the evaluation of these quantities the time is taken in days). The agreement between the values for , , and obtained in the present work and that of Ref. sornette03 is quite good. In the case of the critical time there is a delay of about 15 days mainly caused by the shift of the date attributed to measurements.

An error analysis similar to that described in the case of Peru indicates that the uncertainties of the fitting parameters are linear functions beyond . This is due to the fact that the price index at the end of the period of measurement rose a bigger value in the case of Germany () than of Peru () and, therefore, the finite-time singularity is better defined in the former case. The photos of banknotes of hyperinflation episodes may be found in the paper money gallery at the web site chao .

For the hyperinflation regimes analyzed in the remaining part of this section the error of the free parameters are determined assuming . This uncertainty is large enough to provide a “reasonable” error quotes.

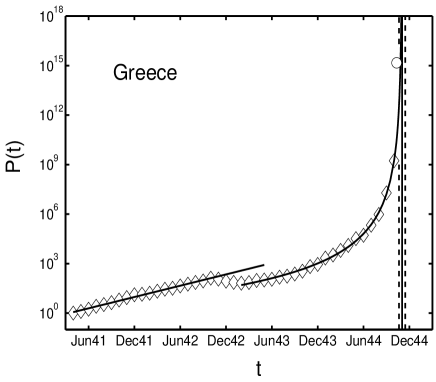

III.2 The Greek catastrophic episode

Let us begin the description of the Greek hyperinflation by citing a fragment of the talk addressed by Nicholas C. Garganas, Governor of the Bank of Greece Garganas . He said: “In April 1941, the Axis Powers occupied Greece. For several years, London became the seat of both the exiled Greek government and the Bank of Greece, with the Bank’s gold secretly transferred to South Africa. Within occupied Greece , the economic situation became increasingly grim and hundreds of thousands of Greeks died of hunger. The Axis powers forced the country to pay not only for the upkeep of the occupying troops, but also for their military operations in Southeastern Europe. The puppet regime established by the occupiers forced the Bank of Greece to resort to the printing press. As a result, the country was beset with hyperinflation; between April 1941 and October 1944, the cost of living rose times. In these difficult circumstances, the country’s economic system collapsed. To give another example of the magnitude of inflation during the occupation, let me mention that in November 1944, immediately after liberation, a so-called “new” drachma was introduced; it was set equal to “old” drachmas!”

Figure 5 shows in a semi-logarithmic plot the price index of Greece taken from Table B6 of Ref. cagan56 . The open diamonds are monthly data taken at the end of each month. The open circle is the value for 1944:11:10, i.e., it corresponds to the first 10 days of November. These data are normalized to . In this drawing one can observe the value mentioned in the previous paragraph. A simple inspection indicates two well differentiated regimes of inflation. This behavior can be understood in terms of different phases of the foreign occupation.

At the beginning conquered Greece was divided into three zones of control by the occupying powers, Germany, Italy and Bulgaria. The Germans limited themselves during the first period of the occupation to the strategically important areas as Athens, Central Macedonia, Western Crete, and the islands of the Northern Aegean, and their forces were limited. Bulgaria annexed Thrace and Eastern Macedonia, while Italy occupied the greater part of the country. Between the occupation zones no movements of goods and people was allowed. The naval blockade coupled with transfers of agricultural produce to Germany led to the gradual but firm establishment of a black market.

Over the period 1941:04 to 1942:10, a dynamics of high inflation can be observed. The cumulated inflation has been about , hence, the level of a hyperinflation was still not reached. This regime can be well described by the original theory of Cagan given by Eq. (40). A fit of the price index to that expression yielded the values of the parameters and quoted in Table 1. The quality of the fit is quite good.

Until the summer of 1942 the resistance movement was in its infancy, however, at the end of that year became strong. The spectacular destruction of the Gorgopotamos bridge by a force of Greek guerrillas and British saboteurs on 25 November caused a reaction of the Italian authorities, in spite of it, the guerrillas were largely successful in this region, creating “liberated” areas in the mountainous interior including some towns.

This initial success of the guerrilla diminished the tension in the population causing a period of small deflation over four months. This fact can be clearly seen in Fig. 5.

However, the pressure of foreign troops increased and in 1943 German elite troops were brought into the whole Greece. A heavy resistance led to German contra-attacks and reprisals. In September 1943 the Italians surrendered following the Allied invasion of Italy. Throughout late 1943 and the first half of 1944, the Germans, in cooperation with the Bulgarians and aided by Greek collaborators launched clearing operations against the Greek resistance.

During this period, the German forced the Greek treasury to pay huge amounts of “occupation expenses”. Since the government of Greece could not meet such an obligation from fiscal taxation (Olivera-Tanzi effect) new money was printed (seigniorage). The attempt to control prices failed and the fall off of production in devastated Greece’s economy led to the collapse of the normal markets and to an increase of the black market.

Due to the general scenario of the war, the Germans were forced to evacuate mainland Greece in October 1944. Their withdrew was finished on November 2 and the exiled government returned to Athens. However, already with the prospect of the liberation of Greece two resistance groups (left and right orientated organizations) began to fight for power. These tensions led almost immediately to a disastrous civil war.

The very difficult situation of the later years of the occupation caused the catastrophic hyperinflation cagan56 ; freris86 displayed in Fig. 5. The inflation reached a peak in November 1944 after liberation. As mentioned in Sec. I, in the first ten days of November the inflation rose the incredible value (see Cagan cagan56 ). The monthly data from 1942:02 to 1944:10 were fitted to Eq. (31). The results of the free parameters are listed in Table 1, the quoted uncertainties correspond to an error of in the measurements of inflation rates. The uncertainty in is also displayed in Fig. 5.

By looking at Fig. 5 one realizes that the solid curve calculated with Eq. (31) reproduces very well the measured data. Moreover, according to the solid curve the measured value on November 10 would be reached on November 25. This anticipated “explosion” of the market price has been caused by the interplay of different strongly increasing “variables”, such as lack of goods and political uncertainty mentioned above. The obtained critical time predicts the definitive crash would be on 1944:12:02. The uncertainty estimated by assuming that the inflation is measured with an error of amounts about 13 days.

The stratification of wealth caused by hyperinflation and black markets during the occupation seriously hindered postwar economic development. The Greek government undertook several stabilization efforts spread over a couple of years before price level stability was achieved. These facts are described in the books written by Palairet palairet00 and Lykogiannis lykogiannis02 . The efforts to confront the hyperinflation consisted of a currency conversion (convertibility of the new drachma into British Military Authority Pounds), the creation of an independent supra-central bank limiting the government’s overdraft at the Bank of Greece, and a few fiscal reforms to increase taxes or reduce expenditures makinen84 .

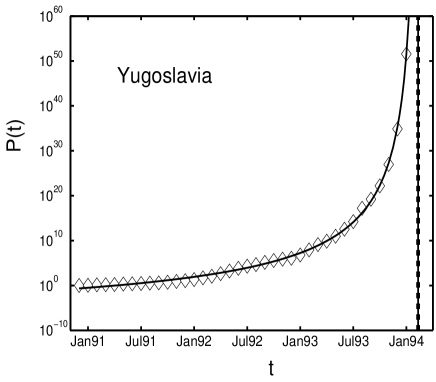

III.3 Yugoslavia - The worst episode in History

The residual Yugoslavia has experienced the highest recorded hyperinflation in History. This episode occurred during a period of two difficult circumstances like the transformation from a Centrally Planned to a rather Free Market economy and the disastrous civil war 1991-4.

Let us now present a summary of the main events of the Yugoslav civil war. A last effort to avoid Yugoslavia’s disintegration was made 3 June 1991 through a joint proposal by Macedonia and Bosnia and Herzegovina, offering to form a “community of Yugoslav Republics” with a centrally administered common market, foreign policy, and national defense. However, Serbia opposed the proposal and the former federal republic of Yugoslavia began the process of dissolution. On 25 of June 1991 Slovenia and Croatia both declared their independence from Yugoslavia. The national army of Yugoslavia, then made up of Serbs controlled by the government of Belgrade, stormed into Slovenia but failed to subdue the separatists there and withdrew after only ten days of fighting losing interest in a country with almost no Serbs. Instead, the attention was turned to Croatia, a Catholic country where Orthodox Serbs made up 12 percent of the population. The civil war started. In order to “protect” the Serbian minority the central forces aided by Serbian guerrillas invaded Croatia in July 1991. By the end of 1991, a U.S.-sponsored cease-fire agreement was brokered between the Serbs and Croats fighting in Croatia. Macedonia opted for independence on 20 November 1991. On 29 February 1992, the multi-ethnic republic of Bosnia and Herzegovina passed a referendum for independence, but not all Bosnian Serbs agreed. Under the guise of protecting the Serb minority in Bosnia, the government of Belgrade channeled arms and military support to them.

So, while the secession of Slovenia and Macedonia came relatively peacefully, in the case of Croatia and Bosnia there were devastating wars. In April 1992, the U.S. and European Community chose to recognize the independence of Bosnia, a mostly Muslim country where the Serb minority made up 32 percent of the population. On April 27, Serbia joined the republic of Montenegro in a smaller New Yugoslav Republic and responded to Bosnia’s declaration of independence by attacking their capital Sarajevo. Foreign governments responded with sanctions, an embargo was introduced by the United Nations embargo on 30 May 1992.

The disintegration of the former Yugoslavia led to decreased output and fiscal revenue, while transfers to the Serbian population in Croatia and Bosnia-Herzegovina as well as military expenditure added to the fiscal problems. Simultaneously, the economy was changing from Central Planning to Free Market. In order to finance the increasing deficit, caused among others by the Olivera-Tanzi effect, the government printed money. High inflation started to build up in 1991. The sources for the data of the complete cycle are documented in Petrović and Mladenović petrovic00 . Figure 6 shows the time series of monthly price index in the period 1990:12 to 1994:01. The monthly inflation had already risen the category of hyperinflation at the beginning of 1992 and accelerated further despite the price freeze attempted in the end of 1993:08. The overall impact of hyperinflation on the price index reached about as it is also shown in Fig. 1 of nielsen04 .

As a consequence of the hyperinflation Yugoslavia went through several currency reforms simply removing zeros from the paper money. In spite of these reforms, along this period the highest denomination reached very large values. The largest nominal value ever officially printed in Yugoslavia, a banknote of 500,000,000,000 (500 billion) dinars was released at the end of 1993 (see photo in Ref. chao ). The overall impact of hyperinflation on currency at the final reform for stabilization performed at the end of 1994:01 was: 1 Novi Dinar pre 1990 Dinar, equivalent to the cumulated price index until 1993:11 (see Fig. 6).

Many Yugoslavian businesses refused to take the Yugoslavian currency at all and the German Deutsche Mark effectively became the currency of Yugoslavia. But government organizations, government employees and pensioners still got paid in Yugoslavian dinars so there was still an active exchange in dinars. However, farmers selling in the free markets refused to sell food for Yugoslavian dinars. So, many monetary transactions were actually taking place in German Marks rather than local currency. Therefore, the hyperinflation can be also measured in terms of the black market exchange rate for German Marks and Yugoslavian Dinars. As can be observed in Fig. 1 of Ref. nielsen04 the strengths of hyperinflation given by the price index and the exchange rate are quite similar (as in the case of Weimar Germany treated above).

The Yugoslav hyperinflation has been studied in a number of papers by using methods developed in the framework of economics. For instance, we can mention the papers of Petrović and Mladenović petrovic00 and Nielsen nielsen04 . These authors consider the price indexes for 1993:12 and 1994:01 to be unreliable and choose end their analyses end at the latest 1993:11. This is in line with standard studies of hyperinflation that mostly ignore the last few observations. Such a procedure is mainly due to the fact that these models do not contain structural information over the divergence at the end of a hyperinflation and big values of price index do not match into the systematics. However, in that studies the trend of the first logarithmic differences is analyzed. For instance, Nielsen nielsen04 on the basis of his Fig. 1 states that such differences exhibit an exponential growth indicating an accelerating inflation, but the last three differences are not included in that figure either.

In standard economic theory, at equilibrium, money determines price level and implies equilibrium in markets for other variables of the system. Usually inflation is associated with money supply growth. However, for instance, there are studies suggesting that the Yugoslavian hyperinflation (19914) was not generated by excess expansion of money stock but, instead, money was accommodating in this period joselius02 .

In our study we included all the values of price index displayed in Fig. 6. A fit of these data to Eq. (31) yielded the free parameters quoted in Table 1. The value of indicates that the quality of the fit is good. The uncertainties in the parameters determined for are smaller than that obtained previously for Germany and Greece. This is due to the fact that the measured price index reached very large values determining the position of the singularity much better than in the former cases.

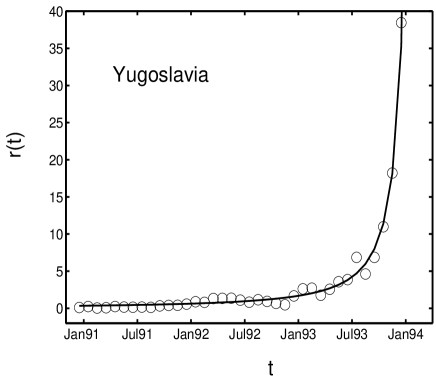

In Fig. 7 we plotted the growth rate evaluated according to Eq. (4), i.e., by calculating the first differences of the natural logarithm of the price index. These data are reproduced very well by Eq. (24) cast into the form

| (41) |

and computed with the parameters listed in Table 1. A similar plot was also given by Nielsen nielsen04 , however, he did not include the last three data.

We must emphasize that the present model is able to reproduce the whole series of measured data. The last observations match very well into the general trend towards the “explosion”. The obtained predicts a crash at the beginning of 1994:03. The hyperinflation was stopped with a successful complete currency reform at the end of 1994:01.

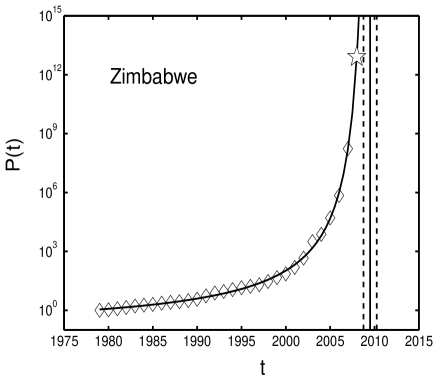

III.4 The current tragic case of Zimbabwe

In 1963 Southern Rhodesia (also known as Rhodesia) chose to remain a colony when its two partners (Zambia and Malawi) voted for independence. The country achieved independence on 17 April 1980, under the name Zimbabwe. At that time the Zimbabwe dollar (ZW-Dollar, the official symbol is ZWD) was worth about US dollar. Since the beginning there was a persistent but moderate structural inflation. Figure 8 shows the yearly price index taken from files of the Central Statistical Office (CSO) and the Reserve Bank of Zimbabwe (RBZ).

By looking at Fig. 8 one may realize that an important acceleration of the price index started with the beginning of the new century. This behavior appeared after the Zimbabwean government proceeded to finance: i) the expenditure to pay the war veterans gratitudes in 1997; ii) the intervention in the Democratic Republic of Congo’s war in 1998; and iii) the expenses of a program of land reforms based on the redistribution of properties in 2000. The latter undertaking, in practice, led to a weakling of the agricultural industry and this in turn produced a fall of export revenues. The resulting deficit was covered by seigniorage. In this way Zimbabwe started to experience hyperinflation makochekanwa07 .

Annual inflation reached about in 2003:12, then fell back to low triple digits in 2004 before rising again to at end of 2005. In 2006:02, the RBZ announced that the government had printed ZW-Dollar in order to buy foreign currency to pay off IMF arrears. In 2006:04 the year-to-year inflation reached above 1,000%. In 2006:08, the Zimbabwean government issued new currency slashing three zeros, 1 new Dollar was exchanged for 1,000 old Dollars. The highest denomination was then 1000 new Dollars. The new money did not provide relief from record inflation. Surging to a new high above 2,000% in 2007:03 and in 2007:06 rose 7,251%. Price rises have sharply accelerated in recent months. The CSO stopped providing data on inflation in October saying that key goods are not available in stores. In other words, this is a recognition that the black market already dominates the domestic economy. The denomination of the largest currency notes is increasing steadily, in 2007:12 the RBZ unveiled new currency notes with denomination as high as 750,000 ZW-Dollars. In a memo sent at the end of December to financial institutions to help them close their 2007 books, the RBZ communicated that the estimated inflation over the past 12 months has totaled 24,059.

The Consumer Council of Zimbabwe and other observers questioned whether the figures provided officially reflected the true cost of living. They stated that real figure is almost certainly much larger. Recent estimates of Zimbabwean inflation by independent economists have tended to put it substantially higher ranging from 50,000 to 100,000. In any case, the Zimbabwe’s inflation is already the highest in the world and has reached that of Latin America’s in the 1980’s. For instance, compare with the data of Peru plotted in Fig. 1.

The high inflation makes transacting in ZW-Dollars pointless. Indeed the RBZ has already confirmed that certain farmers will receive US-Dollar prices for their crops. The severely devalued currency is also causing many organizations to favor using the US-Dollar instead of ZW-Dollar. In actual fact, Zimbabwe is closely tracking Germany’s Weimar Republic in the early 1920’s. Indeed, there is a close parallel between the evolution of exchange rate of the ZW-Dollar in the period 2005-2007 and that of German Marks in 1921-1923. Nowadays, the official exchange rate is 30,739 new ZW-Dollars to a single US-Dollar. A total devaluation since 1980 amounts about a value similar to the cumulated price index plotted in Fig. 8. Therefore, it is expected that some form of “US-dollarization” will establish itself in Zimbabwe in the near future. This behavior would be in line with previous experiences. It should be remained that during the hyperinflation many monetary transactions in Yugoslavia were actually taking place in German Marks rather than local currency.

A fit of the yearly price index to Eq. (31) yielded the values of the free parameters and quoted in Table 1. The good quality of the adjustment is depicted in Fig. 8. The predicted critical time indicates that the finite-time singularity, in other words the economic explosion, will occur at mid-2009. By using the obtained parameters we calculated the price index for the end of 2008, the result is marked by a star in Fig. 8. This value yields % for the year-to-year inflation. The uncertainties were estimated by assuming a quote of for the error of measured inflation. The obtained error bars for are also displayed in Fig. 8.

Zimbabwe’s hyperinflation is spiraling to unknown places and could cause the country’s economy to completely collapse within two years. Due to continued runaway inflation, the RBZ released into circulation in 2008:01 three very high denomination bearer checks: 1 million ZWD, 5 million ZWD and 10 million ZWD (look at Ref. chao ), these banknotes will hold tender until July 2008. The latter is worth about USD at official exchange rate, but only USD in the black market. The Olivera-Tanzi effect is already present. Economic prospects are bleak, reports of extreme shortages of basic foodstuffs, fuel, and medical supplies abound. Moreover, such prospects also indicate that gross domestic product will continue to contract in 2008. Unemployment is around 80 percent and political unrest is growing (the next presidential elections are scheduled for 2008). In summary, this is the worst economic crisis since independence from Britain in 1980.

Therefore, in order to avoid a crash in the near future the government of Zimbabwe should introduce as soon as possible fundamental reforms in the economy.

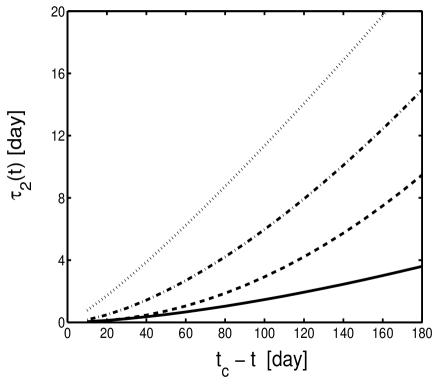

III.5 Comparison of severe episodes of hyperinflation

In order to compare the most severe cases we evaluated the time required to double the price index by using Eq. (35). In this category we included the episodes of Germany, Greece, Yugoslavia, and Hungary. In the latter case the values of and determined by Sornette et al. sornette03 were used, these data are also quoted in Table 2. The results for the last 180 days previous to the singularity are plotted in Fig. 9. This comparison indicates that at the end of the cycles Yugoslavia and Hungary suffered the worst effects.

IV Summary

A study of a few important episodes of hyperinflation is reported. The applied formulation is basically that of Sornette et al. sornette03 . One difference is that in the present work the expression for cumulated price index is written in terms of free parameters of the model instead of introducing combinations of them like quantities and defined in Eqs. (33) and (34). In this way the parameters preserve their own physical meaning. Moreover, the initial time is explicitly retained in the formulas to avoid any misunderstanding. Another difference is the implementation of a procedure for estimating uncertainties of the utilized free parameters. Since the coefficients and of Ref. sornette03 are combinations of basic parameters their uncertainties are correlated, the error analysis in such a case would be much more complicated.

In the present model the growth rate is accelerating such that the market price is growing as a power law towards a spontaneous singularity. This behavior is determined by “adaptive expectations” of the people. The effect of other quantities of standard economic theories does not contribute explicitly. It is worthwhile to notice that whole cycles are described by fixed values of the exponent , which preserve the model from possible underestimation of expectations.

On the other hand, it is well-known that nature does not have pure singularities in the mathematical sense of the term. Such critical points are always rounded off or smoothed out by the existence of friction and dissipation and by the finiteness of the system. This is a well-known feature of critical points cardy . Finite-time singularities are similarly rounded-off by frictional effects given in the case of a hyperinflation by currency and economic reforms.

The data of Peru were analyzed to check our procedures. Therefore, the error analysis is reported in detail. The study of the hyperinflation of Germany indicates that when there are reliable data then the analyses of series of price index and exchange rate lead to very similar results. This behavior confirms that foreign exchange rate of hyperinflation is positively correlated with the country s hyperinflation trend. However, once the episode is finished it is important to reestablish exchange flexibility to allow reactions to local conditions.

We showed that the very extreme cases of Greece and Yugoslavia can be well described by the present formalism. It should be emphasized that both these examples belong to the worst episodes in the hyperinflation category, where the people expectations were directly influenced by catastrophic situations described above. For completeness, we also report a comparison of the most severe cases by determining the time required to double the price index.

The last example is, hitherto, rather similar to the Latin America’s cases of the 80’s. However, according to our quantitative results the government of Zimbabwe should perform very deep changes in the economic system within one year in order to prevent very dreadful consequences for the society.

Let us finish emphasizing that these lessons should not be lost, but instead should be kept in mind to avoid the repetition of that unpleasing experiences. Moreover, one should always remain the statement of Keynes keynes30 , namely that: “even the weakest government can enforce inflation when it can enforce nothing else”.

Acknowledgements.

This work was supported in part by the Ministry of Culture and Education of Argentina through Grants CONICET PIP No. 5138/05, ANPCyT BID 1728/OC - PICT No. 31980, and UBACYT No. X298.References

- (1) S. Moss de Oliveira, P.M.C. de Oliveira, and D. Stauffer, Evolution, Money, War and Computers, Teubner, Stuttgart-Leipzig, 1999.

- (2) R.N. Mantegna and E. Stanley, An Introduction to Econophysics: Correlations and Complexity in Finance, Cambridge University Press, Cambridge, England, 1999.

- (3) D. Sornette, Why Stock Markets Crash (Critical Events in Complex Financial Systems), Princeton University Press, Princeton, 2003.

- (4) T. Mizuno, M. Takayasu, and H. Takayasu, The mechanism of double-exponential growth in hyperinflation, Physica A 308 (2002) 411-419.

- (5) D. Sornette, H. Takayasu, and W.-X. Zhou, Finite-time singularity signature of hyperinflation, Physica A 325 (2003) 492-506.

- (6) P. Cagan, The monetary dynamics of hyperinflation, in: M. Friedman(Ed.), Studies in the Quantity Theory of Money, University of Chicago Press, Chicago, 1956.

- (7) J.H.G. Olivera, Money, Prices and Fiscal Lags: A Note on the Dynamics of Inflation, Banca Nazionale del Lavoro Quarterly Review 20 (1967) 258-267.

- (8) V. Tanzi, Inflation, Lags in Collection, and the Real Value of Tax Revenue, IMF Staff Papers, 24 (1977) 154-167; and Inflation, Real Tax Revenue, and the Case for Inflationary Finance: Theory with an Application to Argentina, IMF Staff Papers, 25 (1978) 417-451.

- (9) A.J. Canavese and D. Heymann, Fiscal Lags and the High Inflation Trap, Quarterly Review of Economics and Finance, 32 (1992) 100-109.

- (10) M. Palairet, The Four Ends of the Greek Hyperinflation of 1941-1946, Museum Tusculanum Press, University of Copenhagen, Copenhagen, 2002.

- (11) A. Lykogiannis, Britain and the Greek Economic Crisis, 1944-1947: From Liberation to the Truman Doctrine, University of Missouri Press, Columbia, 2002.

- (12) Table of the International Monetary Fund, http://www.imf.org/external/pubs/ft/weo/2002/01/data/index.htm.

- (13) T. Sargent, N. Williams, and T. Zha, The conquest of South American inflation, December 2006.

- (14) P. Petrović and Z. Mladenović, Money demand and exchange rate determination under hyperinflation: Conceptual issues and evidence from Yugoslavia, Journal of Money, Credit, and Banking 32 (2000) 785-806.

- (15) B. Nielsen, Money demand in the Yugoslavian hyperinflation 1991-1994, working paper as e-print at the web site: http://www.nuffield.ox.ac.uk/economics/papers/2004/w31/NielsenYugo.pdf .

- (16) Central Statistical Office and Reserve Bank of Zimbabwe.

- (17) V.M. Egu luz and M.G. Zimmermann, Transmission of Information and Herd Behavior: An Application to Financial Markets, Phys. Rev. Lett. 85 (2000) 5659-5662.

- (18) A. Bhattacharjee, C.S. Ng, X. Wang, Finite-time vortex singularity and Kolmogorov spectrum in a symmetric three-dimensional model, Phys. Rev. E 52 (1995) 5110-5123.

- (19) N.M. Zubarev, Formation of root singularities on the free surface of a conducting fluid in an electric field, Phys. Lett. A 243 (1998) 128-131.

- (20) M.W. Choptuik, Universality and scaling in gravitational collapse of a massless scalar, Phys. Rev. Lett. 70 (1999) 9-12; M.W. Choptuik, Critical behavior in gravitational collapse, Progr. Theoret. Phys. 136 (Suppl.) 353-365.

- (21) X. Leoncini, L. Kuznetsov, G.M. Zaslavsky, Motion of three vortexes near collapse, Phys. Fluids 12 (2000) 1911-1927.

- (22) H.K. MoCatt, Euler s disk and its finite-time singularity, Nature 404 (2000) 833-834.

- (23) M. Rascle C. Ziti, Finite-time blow-up in some models of chemotaxis, J. Math. Biol. 33 (1995) 388-414.

- (24) A. Johansen and D. Sornette, Finite-time singularity in the dynamics of the world population, economic and financial indexes, Physica A 294 (2001) 465-502.

- (25) C. Bender and S.A. Orszag, Advanced Mathematical Models for Scientists and Engineers, McGraw Hill, New York, 1978.

- (26) K. Ike and D. Sornette, Oscillatory finite-time singularities in finance, population and rupture, Physica A 325 (2002) 63-106.

- (27) P.R. Bevington, Data Reduction and Error Analysis for the Physical Sciences, McGraw Hill, New York, 1969.

- (28) T. Chao, Paper Money Gallery, at the web site: http://tomchao.com/hb.html.

- (29) N.C. Garganas, Why is the role of the central bank important?, dissertation at the celebrations marking the 75th anniversary of the Bank of Greece (Athens, 3 November 2003) at the web site: http://www.bis.org/review/r031113d.pdf.

- (30) A.F. Freris, The Greek Economy in the Twentieth Century, St. Martin’s Press, Croom Helm - London , 1986.

- (31) G.E. Makinen, The Greek Stabilization of 1944-46. American Economic Review 74 (1984) 1067-74.

- (32) K. Juselius and Z. Mladenović, High inflation, hyperinflation and explosive roots. The case of Yugoslavia. October 2, 2002.

- (33) A. Makochekanwa, A Dynamic Enquiry into the Causes of Hyperinflation in Zimbabwe, e-print at the web site: http://web.up.ac.za/UserFiles/WP_2007_10.pdf.

- (34) J.L. Cardy (Ed.), Finite-size Scaling, Elsevier Science, Amsterdam, 1988.

- (35) J.M. Keynes, A Treatise on Money, vols. I-II, Harcourt, Brace and Co., New York, 1930; and The General Theory of Employment, Interest and Money, Macmillan and Co., London, 1936; both reprinted by D.E. Moggridge (ed.), in: The Collected Writings of John Maynard Keynes, Macmillan, London, 1973.