Risk-Seeking vs. Risk-Avoiding Investments in Noisy Periodic Environments

J. E. Navarro B., F. E. Walter, F. Schweitzer

References

- [2]

- [3] \wwwhttp://www.sg.ethz.ch

- [4] \makeframing

Risk-Seeking versus Risk-Avoiding Investments in Noisy Periodic Environments

Abstract

We study the performance of various agent strategies in an artificial investment scenario. Agents are equipped with a budget, , and at each time step invest a particular fraction, , of their budget. The return on investment (RoI), , is characterized by a periodic function with different types and levels of noise. Risk-avoiding agents choose their fraction proportional to the expected positive RoI, while risk-seeking agents always choose a maximum value if they predict the RoI to be positive (“everything on red”). In addition to these different strategies, agents have different capabilities to predict the future , dependent on their internal complexity. Here, we compare ’zero-intelligent’ agents using technical analysis (such as moving least squares) with agents using reinforcement learning or genetic algorithms to predict . The performance of agents is measured by their average budget growth after a certain number of time steps. We present results of extensive computer simulations, which show that, for our given artificial environment, (i) the risk-seeking strategy outperforms the risk-avoiding one, and (ii) the genetic algorithm was able to find this optimal strategy itself, and thus outperforms other prediction approaches considered.

1 Introduction

(a) (b)

2 Model

-

1.

their budget , which is a measure of their “wealth” or “liquidity”, and

-

2.

the strategy that they employ in order to control the fraction of the budget to invest at each time step.

| (1) |

3 Agent Strategies

3.1 Reference Strategy

| (2) |

3.2 Technical Analysis

3.2.1 Moving Averages

| (3) |

3.2.2 Moving Least Squares

| (4) |

| (5) |

| (6) | |||||

| (7) |

| (8) |

| (9) |

3.3 Machine Learning Approaches

3.3.1 Incremental Update Rule

| (10) |

| (11) |

| (12) |

| (13) |

3.3.2 Genetic Algorithm

| (14) |

-

•

Elitist selection considers the best percentage of the population which is found by ranking the chromosomes according to their fitness. The best chromosomes are directly transferred to the new population.

-

•

Tournament selection is done by randomly choosing two pairs of two chromosomes from the old population and then selecting from each pair the one with the higher fitness. These two chromosomes are not simply transferred to the new population, but undergo a transformation based on the genetic operators crossover and mutation, as follows: A single-point crossover operator finds the cross point, or cut point, in the two chromosomes beyond which the genetic material from two parents is exchanged, to form two new chromosomes. This cut point is the integer part of a random number drawn from a uniform distribution .

| (15) |

4 Return on Investment

| (16) | |||||

| (17) |

![[Uncaptioned image]](/html/0801.4305/assets/x3.png)

![[Uncaptioned image]](/html/0801.4305/assets/x4.png)

![[Uncaptioned image]](/html/0801.4305/assets/x5.png)

![[Uncaptioned image]](/html/0801.4305/assets/x6.png)

(a) (b)

5 Optimal Parameter Adjustment

| Algorithm | Parameters |

|---|---|

| MA | (risk-seeking), (risk-avoiding) |

| MLS | (both risk-seeking and risk-avoiding) |

| IUR | (both risk-seeking and risk-avoiding) |

| GA | , , , |

Table 1 shows the optimal parameters that we choose for the comparison of the different strategies. Of course, the optimal parameters usually are not the same for different types and levels of noise or for risk-seeking and risk-avoiding behaviour, so at times, a compromise between several alternative values for different situations had to be found.

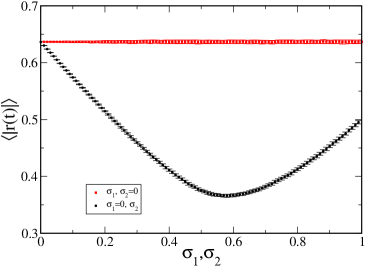

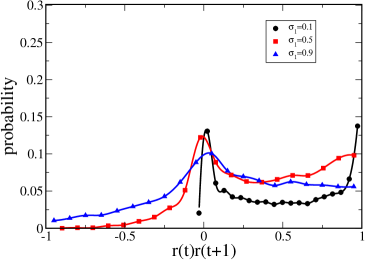

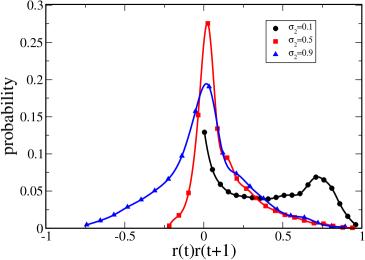

6 Results

6.1 Comparison

![[Uncaptioned image]](/html/0801.4305/assets/x10.png)

![[Uncaptioned image]](/html/0801.4305/assets/x11.png)

![[Uncaptioned image]](/html/0801.4305/assets/x12.png)

![[Uncaptioned image]](/html/0801.4305/assets/x13.png)

6.2 Optimal Strategy

![[Uncaptioned image]](/html/0801.4305/assets/x14.png)

![[Uncaptioned image]](/html/0801.4305/assets/x15.png)

![[Uncaptioned image]](/html/0801.4305/assets/x16.png)

![[Uncaptioned image]](/html/0801.4305/assets/x17.png)

| (18) |

| (19) |

6.3 “Everything on Red”

(a) (b)

7 Discussion and Conclusions

-

1.

The type of noise – whether the RoI has phase or amplitude noise – does not have a significant influence on the performance of the algorithms, while the level of noise certainly does – for increasing noise, we observe decreasing performance.

-

2.

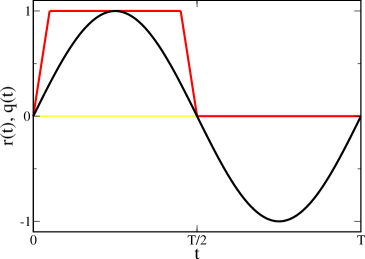

The GA performs best of all strategies for almost all scenarios; it discovers a strategy which resembles a square wave strategy and which follows the principle of always investing the complete budget or the maximum amount possible when the expected return is positive and not investing anything or the least amount possible when the expected return is negative.

-

3.

The best rule for investment is the risk-seeking behaviour of always putting the complete budget in an investment; this behaviour clearly outperforms a risk-avoiding behaviour which humans would probably apply intuitively: whilst it may seem intuitive to a human to invest an amount proportional to the expected return, this is not the approach which yields the greatest budget growth over time.

- Heterogeneity:

-

Agents in our model are homogenous with respect to the strategy employed, i.e. there is no variability in their individual strategies.[kirman05] In this respect, the model is basically a “representative agent model”, which takes into account only the limited information of the previous . More elaborated strategies, where agents are assumed to be fundamentalist or chartists [day90, farmer00price, follmer05] are also not considered here.

- Interaction:

-

Agents in our model do not interact with other agents. They rather “learn” the dynamics of the market return, in order to predict it more accurately. Important collective interactions in financial markets, such as herding behavior, is neglected here, as well as interactions between (heterogeneous) trading strategies [follmer05]. This implies the absence of emergent properties in our model, as heterogeneity and interaction are indeed basic premises for the existence of emergent properties in financial markets.

- Feedback:

-

Agents in our model have no effect upon the market, and consequently the price of an asset and the return on investment are treated as exogenous variables. This is equivalent to the ’atomistic market’ assumption. Our model also neglects the collective impact of all agents on the price and the return of an asset. Other feedbacks on the market, such as agent’s expectations about the market dynamics itself, are also not explicitely modeled here. Some artificial market models consider an endogeneous approach, where the returns are generated by means of constant trading between heterogeneous agents [day90, farmer00price].

- Microfoundation:

-

Our model is lacking an adequate economic microfoundation of the (representative) agent behaviour. The terms “risk-avoiding” and “risk-seeking” are used to denote the investment preference of the agent. However, since decisions are always taken based on just the expected return, the behaviour of the agent has to be classified as “risk neutral” – risk-adverse agents indeed account also for the “variance” of returns in their decisions. Recent literature in economics and finance presents a more realistic approach about behaviour toward risk. [hens06, Pindyck-Rubinfeld]

- Multi-assets:

-

Agents in our model can only invest in one (risky) asset, whereas in financial markets multi-asset investments and portfolio strategies play the most crucial role. [elton03, markowitz91] Multi-asset optimal investment strategies for risky assets were already discussed 50 years ago, with an interesting relation to gambling [breiman60]. More recently, investment strategies to readjust portfolios [merton90] have been extended [maslov98] for a general distribution of return per capital. Similar to our model, these contributions consider exogeneous returns which are drawn from a probability distribution or are modeled by a stochastic processes.