Forecasting volatility with the multifractal random walk model

Abstract.

We study the problem of forecasting volatility for the multifractal random walk model. In order to avoid the ill posed problem of estimating the correlation length of the model, we introduce a limiting object defined in a quotient space; formally, this object is an infinite range logvolatility. For this object and the non limiting object, we obtain precise prediction formulas and we apply them to the problem of forecasting volatility and pricing options with the MRW model in the absence of a reliable estimate of and .

Jean Duchon, Raoul Robert

Institut Fourier, université Grenoble 1, UMR CNRS 5582,

100, rue des Mathématiques, BP 74, 38402 Saint-Martin d’Hères cedex, France

e-mail: Jean.Duchon@ujf-grenoble.fr,Raoul.Robert@ujf-grenoble.fr

Vincent Vargas

CNRS, UMR 7534, F-75016 Paris, France

Université Paris-Dauphine, Ceremade, F-75016 Paris, France

e-mail: vargas@ceremade.dauphine.fr

Key words or phrases: Random measures, Gaussian processes, Prediction theory, Multifractal processes.

MSC 2000 subject classifications: 60G57, 60G15, 60G25, 28A80

1. Introduction

In recent years, the Multifractal Random Walk (MRW) model introduced by Bacry, Delour and Muzy ([1]) has received much attention from the financial practitioners. The MRW appears as a natural extension of the basic geometric Brownian model (GB). Let be the price of an asset; in the GB model we write:

| (1.1) |

where . Here is the mean return rate , the volatility of the asset supposed to be constant, a standard Brownian motion. The GB model plays a fundamental role in finance as it enables to give a price to options (by the famous Black-Scholes formula). Nevertheless when compared with reality the model displays severe drawbacks; more precizely, the GB model does not display the following stylized facts which are largely acknowledged in the litterature ([7], [8]):

-

•

The volatility fluctuates randomly and follows approximately a lognormal distribution.

-

•

While the returns are rapidly decorrelated, the volatility exhibits long range correlations following a power law

-

•

The returns are heavy tailed.

The above stylized facts lead naturally to propose as model of volatility a random measure called the limit lognormal model. This object, introduced by Mandelbrot ([11]) in the context of turbulence, was rigorously defined and studied by Kahane in [10] under the name of gaussian multiplicative chaos. More precisely, Kahane developped a general theory for -positive kernels (see [10] for the exact definition) and suggested how to use this framework to define the object introduced by Mandelbrot in [11].

Let us give a very sketchy presentation of the gaussian multiplicative chaos. Let and be given parameters ( is the correlation length). We consider the positive kernel . To this kernel, we associate the stationary gaussian process with covariance (in a generalized sense since ). The associated multiplicative chaos is a random measure defined (formally) by:

Of course, this formula has no meaning since but it clearly suggests the limit procedure by which we can define rigorously the random measure (in [3], it is proven that the kernel is -positive in the sense of Kahane and therefore the measure is a particular case of the general theory developped in [10]).

Following an idea of Mandelbrot and Taylor ([12]), one can consider the model (for the log price) of a Brownian motion subordinated by an independent random mesure. This was first performed with the measure by the authors of [3]: this defines the MRW model. More precisely, we define the random time change . The MRW model is then the four parameter stochastic process given by:

where the Brownian motion is independent of . If is not too large (a few years for example), the drift term is in practice negligible compared to the Brownian term so the MRW reduces to the three parameter process:

From classical properties of the chaos , it follows that is a continuous process so that is also continuous. By using the scale invariance of , one can write (at least formally) as a stochastic integral:

| (1.2) |

where is the intermittency coefficient. One can then obtain rigorously as the limit of a discretized approximation scheme; more precisely, let be some positive step parameter, be a standard gaussian i.i.d. sequence and be a zero mean stationary gaussian sequence independant of with kernel (see lemma (6.1) of the appendix for the existence of ):

| (1.3) |

If , one can show the convergence in law (in a functional sense) as goes to of given by:

towards ([3]).

To what extent is relevant to model financial markets? As it gives a fat tailed distribution for the returns, long range correlations and a lognormal fluctuating volatility, the MRW appears as a rather relevant model for exchange markets. The main limitation of this model is the symmetry of the distribution of returns and therefore it can not capture the leverage effect observed on stocks and indices (see [5] for a quantitative study of the leverage effect) . One of the most important predictions of the process concerns the logvariogram. More specifically, let . Then, one defines the logvariogram by the formula:

One can show that there exists such that for all :

| (1.4) |

where and the terms do not depend on or such that:

In practice, one can neglect the last term of the above expansion since the value of for a financial asset (stock, currency, index, etc…) will typically belong to the interval .

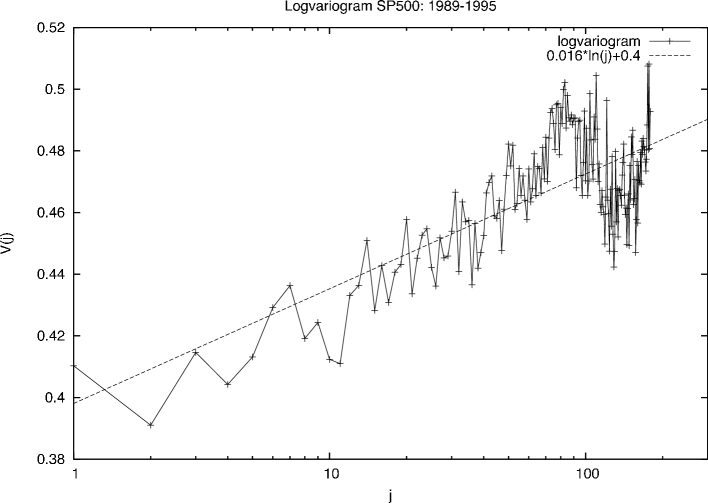

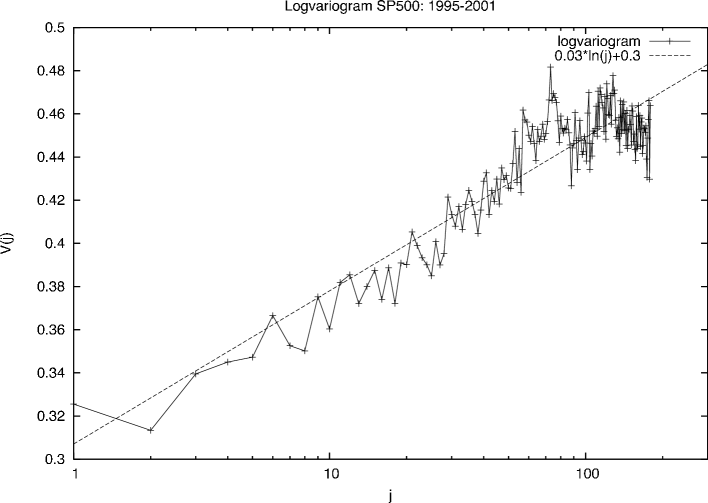

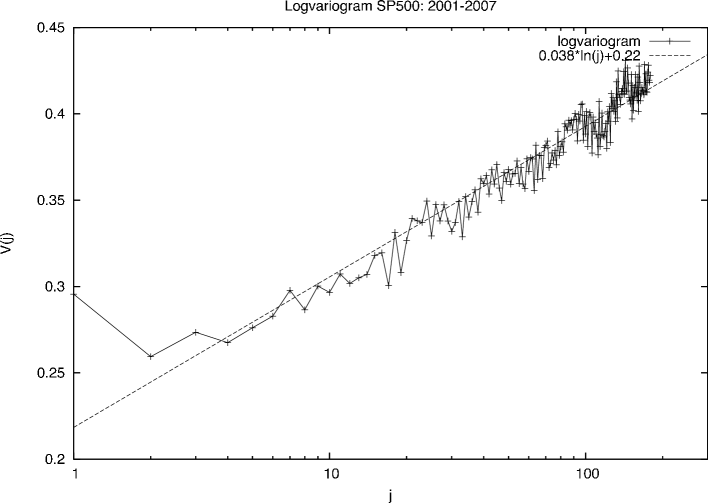

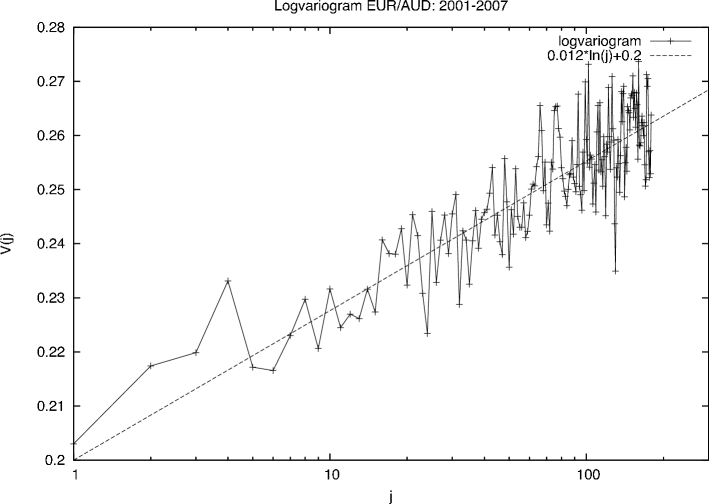

We see on the figures 1 and 2 the empirical logvariogram of the SP500 index on three disjoint periods of 6 years and the empirical logvariogram of the currency Euro/Australian dollar on the period along with the corresponding regressions of the form . One can notice that the logvariograms of the SP500 are less and less noisy as time evolves (perhaps due to the increase of liquidity: tick size, volume, etc…). We propose to estimate the intermittency parameter by the aformentionned regression: Monte Carlo simulations performed with trials of a MRW on a period of years with show that the above estimator belongs to the interval with a confidence interval of percent.

Finally, we mention the problem of the estimation of the parameter . Typically, is very hard to estimate precisely (With the financial data available, one finds huge error bars on the estimation of this parameter: for typical estimates of , see [2]). Roughly, will exceed 2-3 years for an asset. It is easy to convince oneself that beyond a window of size years, one can not assume that the sequence of returns of an asset forms a stationary sequence because markets evolve in time. In these conditions, ergodicity of the data breaks down and one can not rely on a precise estimate of . In fact, it is even impossible to determine with data on a window of size ; indeed, if and are two MRW with respective parameters and such that then the following generalized scale invariance holds:

| (1.5) |

where is a centered gaussian variable independent from and of variance . Therefore, the law of given is the law of a MRW with parameters . In conclusion, the statistical estimation of and is an ill posed problem and the most natural way to get rid of the problem is thus to let go to infinity and work with the limiting object. In doing such a procedure, one must work in a quotient space (see definition (2.3) where one views the log volatility as an element of the quotient space ).

The rest of the article is organized as follows: in section 2, we give some preliminary definitions: in particular, we introduce the log volatility processes and . In section 3, we give explicit prediction formulas on and . In section 4, we show how to use the results of section 3 to forecast volatility and price options with the MRW model with no knowledge on the value of or . Finally, in section 5, we give the detailed proof of the results of section 3.

2. Definitions and preliminaries

2.1. Definitions

For , we denote by the space of smooth functions on with compact support included in and by the space of distributions on . Let denote the space of Schwartz functions and it’s topological dual (the space of tempered distributions). The Fourier transform of an element of is defined as usual by:

where is the classical Fourier transform of :

We remind the definition of the classical Sobolev Spaces for :

The space equipped with the scalar product:

is a Hilbert space.

We also introduce the homogeneous Sobolev Spaces for :

The space equipped with the scalar product:

is a Hilbert space.

For , the homogeneous Sobolev Spaces are defined by:

For , the space equipped with the scalar product:

is a Hilbert space.

2.2. The processes , and their reproducing kernel Hilbert space

We consider the reader is familiar with the theory of gaussian processes. For a complete account on the theory, we refer to [4].

We introduce the generalized gaussian process as a gaussian measure on the space with the following characteristic functional:

It follows from Minlos’s theorem that the above formula defines a unique gaussian mesure on ([9], chapter 4). Let sinc be defined by the classical formula:

By using Parseval’s identity and lemma 6.1 of the appendix, one can deduce that:

| (2.1) |

The reproducing kernel Hilbert space ([4]) associated to is therefore the space:

Since there exists two constants such that:

| (2.2) |

the space is the space equipped with an equivalent norm.

One would like to let go to infinity in the above definition. In order to give a rigorous meaning to that procedure, one must work in the space of Schwartz functions of average zero:

The topological dual of is then the quotient space . We therefore introduce the generalized gaussian process as a gaussian measure on the space with the following characteristic function:

| (2.3) | ||||

| (2.4) |

By letting go to infinity in identity (2.1), one gets:

The reproducing kernel Hilbert space associated to is therefore the space:

The space is thus precisely the space .

Notations: In the sequel, we will use the notations and .

3. The prediction formulas for ,

3.1. Prediction formulas for

We have the following explicit formula for the conditional expectation of :

Theorem 3.1.

Let be some finite positive real number and the trace on the interval of a function in . Then, the conditional expectation is a function of that satisfies:

| (3.1) |

where the application is given by:

or

Remark 3.2.

Since a function in is locally in for all , we easily check that the integral in 3.1 makes sense.

By letting in the above formula, we get the following corollary:

Corollary 3.3.

Let be the trace on the interval of a function in . Then, the conditional expectation is a function of that satisfies:

| (3.2) |

3.2. Consequence on the prediction of

As a consequence of the above formulas on , it is possible to obtain an exact prediction formula on .This formula is no longer defined modulo constants and is valid whatever the value of the correlation length . It is obtained as a perturbation of the case .

In order to state the formula, we introduce as the unique distribution of with support in solution of:

We refer to section 5.3 for the existence and uniqueness of . In fact, the distribution is a function and it is given explicitly by the following formula:

| (3.3) |

This leads to:

Theorem 3.5.

Let be some finite and positive real number such that and the trace on of a function in . Then is a function of that satisfies:

| (3.4) |

where the kernel satisfies for in :

| (3.5) |

4. Application to volatility forecasting and option pricing

In this section, we suppose that we ignore the values of and but that the value of is known.

4.1. Forecasting volatility

Discretizing formula (3.2)

Let us first suppose that is large compared to so that the prediction kernel is given by . Suppose also that the time at which we intend to predict is small compared to . It follows that we may use the prediction formula (3.2):

Let us take some small time lag and discretize the above formula. We get:

| (4.1) |

and thus for :

Let us denote

so that the discretized formula writes:

Of course, we have for all , so for . Notice also that does not depend on .

Application of the discretized formula

We will model the (log) return at scale of a financial asset as a discretized MRW:

where is the noise process (i.i.d. standard gaussian) and the volatility process:

with given by definition (1.3).

Suppose one can observe the historical volatility (or equivalently ) on some time window (Of course this is rigorously not the case in finance and one must use filtering theory, intraday data, etc… to get a proxy of ). We can decompose the process , :

where is a centered gaussian process independent from and the coefficients are uniquely determined by the conditions:

If we suppose that and then formula appears as a discretization of formula (3.2) and we may approximate:

so that . Then we write:

from which we get the conditional expectation:

Now let us calculate . We use:

and

Therefore, we get:

If we set equal to the constant term in the above expression, we get the following simple formula:

One can notice the remarkable fact that, in the above formula, have disappeared. Nevertheless, the formula depends on and we get the following sensitivity with respect to :

| (4.2) |

Since numerically, if one considers the problem of forecasting volatility on a period of month () and is known with a precision , the above formula (4.2) implies that the forecast is correct with a very high precision of approximately percent.

4.2. Option pricing with unknown parameters

Let be the price process of a financial asset. We model the log price by the continuous MRW (with underlying parameters ) given by expression (1.2). In this subsection, we fix a real positive number . Suppose one can observe the historical (log) volatility on some time window . The price of a standard call option with maturity and exercise price is then given by (for simplicity, we suppose the risk free rate and that there are no dividends):

| (4.3) |

where is given by the approximation (4.7). For simplicity, we will also suppose that the maturity is not very large (typically, a few months) such that one can make the following approximation by an additive model:

Then, one can perform a cumulant expansion in formula (4.3) up to the kurtosis (see p. 244-245 in [6] for details) and obtain the following smile formula for the implied volatility as a function of the strike and the maturity :

| (4.4) |

where is the forecasted variance:

| (4.5) |

and the forecasted kurtosis:

| (4.6) |

We outline the computation of (4.5). Let be some small observation scale and let be the (log) return at scale . We have:

One then uses the expression of the previous subsection and the discretization:

We therefore get with :

The computation of each term

is similar to the computations of the previous subsection.

Since, in practice, is roughly found around the value , we perform an expansion of for in order to compute . We have the following scaling identity:

where is a standard gaussian variable independent of . We can derive formally the following series of approximations for (we will use for and a generalized centered gaussian variable the approximation : see [2] for an exact mathematical formulation):

| (4.7) |

where is a standard gaussian variable independent of . Using expression (4.7), standard computations give the following expression for :

| (4.8) |

If we let go to infinity, we get the following limit expression:

| (4.9) |

Remark 4.1.

5. Proof of the prediction formulas

5.1. Preliminary results and definition

In this section, we prove the theorems of section 3. Let denote the upper half plane and denote the following quotient space:

equipped with the norm

On the Hilbert space , one can define in a classical way a trace operator:

Lemma 5.1.

There exists a unique continuous linear operator that satisfies:

The operator is onto and satisfies:

We introduce the Poisson kernel by the following formula:

| (5.1) |

Notice that the existence of the above integral is not obvious: one first defines it for in and then extends it to by density.

The next lemma relates to a variational problem.

Lemma 5.2.

For all there exists a unique solution to the variational problem:

| (5.2) |

and the solution is given by the Poisson formula 5.1. Moreover, is the unique solution to the Dirichlet problem:

| (5.3) |

and the following identity holds:

| (5.4) |

Proof.

Let be fixed. A simple computation shows that the Fourier transform of is given by:

Therefore one gets:

which is precisely identity 5.4. It is straightforward to check that is solution to 5.3. One can easily show that is dense in which implies that:

and therefore, one gets for all in the following identity:

This entails that is the unique minimizer of 5.2.

∎

Corollary 5.3.

Let be some element of and an open interval . Consider the function and the associated variational problem:

Suppose is a solution of the following Dirichlet problem:

| (5.5) |

Then is the unique solution to the above variational problem.

Proof.

Let g be an element of such that . Then we have the following identity:

5.2. Proof of theorem 3.1

Let be the trace on of a function. By a general property of gaussian measures ([13]), the conditional expectation on the left hand side can be obtained as the solution of the variational problem:

By corollary 5.3, one must solve the Dirichlet problem 5.5:

The application is solution to the above Dirichlet problem if and only if given by is solution to:

where . One can solve this problem explicitly by using conformal mappings. Let be the conformal map from the half disc

to the upper half plane :

Then is harmonic in , satisfies the condition on the vertical diameter and we have the following equality for :

Since on the vertical diameter, one can extend symmetrically as a harmonic function on the unit disc. By Poisson’s formula, has the following representation:

In particular, one gets:

For greater or equal to ,

and for less or equal to ,

Therefore, one gets

where is given by the formula:

or

One gets the desired result by making the change of variable in the above integral.

∎

5.3. Proof of corollary 3.3

We take the limit in formula (3.1). It is straightforward to check the convergence in of the right hand term. Let us denote the left hand term in (3.1) and the left hand term in (3.2). We have:

and

Thus we have . Modulo a subsequence, we may suppose by the Banach-Alaoglu theorem that converges weakly in as goes to infinity to . We have the convergence of to in which implies that . Since , we get .

5.4. Proof of theorem 3.5

The minimization problems

We consider the Sobolev space equipped with the norm given by :

where is the Fourier transform of :

Let be some function of which is the restriction of some function of . We will denote by the function of solution of the minimization problem:

We can consider the function as a function of and note the unique solution of the minimization problem:

A few intermediate propositions

We will start by giving a few intermediate propositions before proving the theorem 3.5.

Proposition 5.4.

Let be some function of .There exists a unique in with support in that satisfies:

| (5.6) |

Proof.

Consider the Hilbert space of distributions in with support in . On the product , we consider the bilinear form:

By inequality (2.2), defines a norm equivalent to . The linear form is continuous on . By the Lax-Milgram theorem, there exists a unique such that:

Since , we get the desired equality. ∎

In the sequel, we will denote by the solution to equation (5.6) with and . Note that one can show the obvious scaling equality when :

| (5.7) |

with given by (cf.appendix):

We have thus the following expression for :

One can apply the above proposition to the resolution of the minimization problems and .

Proposition 5.5.

Let be the solution of the equation (5.6). Then the function is solution to .

Proof.

Let be such that on . We get:

∎

Similarly, wet get the following solution to :

Proposition 5.6.

Let be in . Let be the solution in with support in of the equation:

Then is solution to .

Proof.

First note that by the scaling relation (5.7), we have:

Thus we get that:

It is obvious by definition that is in and that on the interval . Now, if satisfies the same conditions we get:

∎

Remark 5.7.

The solution is in fact not defined modulo constants and coincides with for all as can be seen by letting go to or to infinity.

Convergence of towards as goes to infinity

We have the following exact formula:

Proposition 5.8.

Let be larger than . Then for all in the interval , we have the identity:

| (5.8) |

6. Appendix

In the appendix, we show that for all , the kernel is positive (in particular, one can define a gaussian process with kernel (1.3)) and we show how to derive (3.3).

Lemma 6.1.

The kernel is positive. More precisely, we have the following expression for the Fourier transform if :

Proof.

We have for all :

∎

In particular, one can define the gaussian process with covariance given by formula (1.3).

We now give a proof of identity (3.3). It is a direct consequence of the following lemma.

Lemma 6.2.

For all in , we have:

| (6.1) |

Proof.

We start by showing that the above quantity does not depend on in the interval . Since the left hand side of (6.1) is invariant under , we can consider the case . By performing successively the change of variables and , we get the following identities:

For all , we introduce the following functions:

Note that we have to prove that is a constant function on . As goes to zero, converges pointwise to . We will prove that tends to 0 uniformly on compact intervals which implies the result. If , we get:

Let be the rational fraction defined on by:

We get:

where:

By the formula of residues, we get that for all in :

Using the above formula, one easily derives that goes uniformly to on as goes to .

Since is a constant function on , we only need to compute to prove (6.1). The computation of is standard.

∎

Acknowledgements: The authors would like to thank Capital Fund Management (CFM) for providing them data on the SP500 Index and the currency EUR/AUD. V. Vargas would like to thank J.P. Bouchaud and the Nimbus team at CFM for useful discussions.

References

- [1] Bacry, E., Delour, J., and Muzy, J.F.: Multifractal random walks, Phys. Rev. E, 64 (2001), 026103-026106.

- [2] Bacry E., Kozhemyak, A., Muzy J.-F.: Continuous cascade models for asset returns, available at www.cmap.polytechnique.fr/ bacry/biblio.html, to appear in Journal of Economic Dynamics and Control.

- [3] Bacry, E. and Muzy, J.F.: Log-infinitely divisible multifractal process, Communications in Mathematical Physics, 236 (2003), 449-475.

- [4] Bogachev, V.: Gaussian measures, American Mathematical Society (1998).

- [5] Bouchaud, J.P., Matacz, A. and Potters, M.: Leverage Effect in Financial Markets: The Retarded Volatility Model, Phys. Rev. Lett., 87 (2001), 228701.

- [6] Bouchaud, J.P., Potters, M.: Theory of Financial Risk and Derivative Pricing, Cambridge University Press, Cambridge (2003).

- [7] Cizeau, P., Gopikrishnan, P., Liu, Y., Meyer, M., Peng, C.K., Stanley, E.: Statistical properties of the volatility of price fluctuations, Physical Review E, 60 no.2 (1999), 1390-1400.

- [8] Cont, R.: Empirical properties of asset returns: stylized facts and statistical issues, Quantitative Finance, 1 no.2 (2001), 223-236.

- [9] Gelfand, I.M., Vilenkin, N.Ya.: Generalized functions, Academic Press, New York (1964).

- [10] Kahane, J.-P.: Sur le chaos multiplicatif, Ann. Sci. Math. Québec, 9 no.2 (1985), 105-150.

- [11] Mandelbrot B.B.: A possible refinement of the lognormal hypothesis concerning the distribution of energy in intermittent turbulence, Statistical Models and Turbulence, La Jolla, CA, Lecture Notes in Phys. no. 12, Springer, (1972), 333-351.

- [12] Mandelbrot, B., Taylor, H.: On the distribution of stock price differences, Operations Research, 15 (1967), 1057-1062.

- [13] Wahba, G.: Spline Models for Observational Data, CBMS-NSF Regional Conference Series in Applied Mathematics (1990).