Nonparametric sequential prediction of time series

Gérard BIAU ***Corresponding author., Kevin BLEAKLEY ,

László GYÖRFI and György OTTUCSÁK

LSTA & LPMA

Université Pierre et Marie Curie – Paris VI

Boîte 158, 175 rue du Chevaleret

75013 Paris, France

biau@ccr.jussieu.fr

Institut de Mathématiques et de Modélisation de

Montpellier

UMR CNRS 5149, Equipe de Probabilités et Statistique

Université Montpellier II, CC 051

Place Eugène Bataillon, 34095 Montpellier Cedex 5, France

bleakley@math.univ-montp2.fr

Department of Computer Science and Information Theory

Budapest University of Technology and Economics

H-1117 Magyar Tudósok krt. 2, Budapest, Hungary

{gyorfi,oti}@szit.bme.hu

Abstract

Time series prediction covers a vast field of every-day statistical

applications in medical, environmental and economic domains.

In this paper we develop nonparametric

prediction strategies based on the combination of a set of “experts” and show the

universal consistency of these strategies under a minimum of conditions. We perform an in-depth analysis of real-world data sets

and show that these nonparametric strategies are more flexible, faster and generally outperform

ARMA methods in terms of normalized cumulative prediction error.

Index Terms — Time series, sequential prediction, universal consistency, kernel estimation, nearest neighbor estimation, generalized linear estimates.

1 Introduction

The problem of time series analysis and prediction has a long and rich history, probably dating back to the pioneering work of Yule in 1927 [30]. The application scope is vast, as time series modeling is routinely employed across the entire and diverse range of applied statistics, including problems in genetics, medical diagnoses, air pollution forecasting, machine condition monitoring, financial investments, marketing and econometrics. Most of the research activity until the 1970s was concerned with parametric approaches to the problem whereby a simple, usually linear model is fitted to the data (for a comprehensive account we refer the reader to the monograph of Brockwell and Davies [5]). While many appealing mathematical properties of the parametric paradigm have been established, it has become clear over the years that the limitations of the approach may be rather severe, essentially due to overly rigid constraints which are imposed on the processes. One of the more promising solutions to overcome this problem has been the extension of classic nonparametric methods to the time series framework (see for example Györfi, Härdle, Sarda and Vieu [16] and Bosq [3] for a review and references).

Interestingly, related schemes have been proposed in the context of sequential investment strategies for financial markets. Sequential investment strategies are allowed to use information about the market collected from the past and determine at the beginning of a training period a portfolio, that is, a way to distribute the current capital among the available assets. Here, the goal of the investor is to maximize their wealth in the long run, without knowing the underlying distribution generating the stock prices. For more information on this subject, we refer the reader to Algoet [1], Györfi and Schäfer [21], Györfi, Lugosi and Udina [19], and Györfi, Udina and Walk [22].

The present paper is devoted to the nonparametric problem of sequential prediction of real valued sequences which we do not require to necessarily satisfy the classical statistical assumptions for bounded, autoregressive or Markovian processes. Indeed, our goal is to show powerful consistency results under a strict minimum of conditions. To fix the context, we suppose that at each time instant , the statistician (also called the predictor hereafter) is asked to guess the next outcome of a sequence of real numbers with knowledge of the past (where denotes the empty string) and the side information vectors , where . In other words, adopting the perspective of on-line learning, the elements and are revealed one at a time, in order, beginning with , and the predictor’s estimate of at time is based on the strings and . Formally, the strategy of the predictor is a sequence of forecasting functions

and the prediction formed at time is just .

Throughout the paper we will suppose that are realizations of random variables such that the process is jointly stationary and ergodic.

After time instants, the (normalized) cumulative squared prediction error on the strings and is

Ideally, the goal is to make small. There is, however, a fundamental limit for the predictability of the sequence, which is determined by a result of Algoet [2]: for any prediction strategy and jointly stationary ergodic process ,

| (1) |

where

is the minimal mean squared error of any prediction for the value of based on the infinite past observation sequences and . Generally, we cannot hope to design a strategy whose prediction error exactly achieves the lower bound . Rather, we require that gets arbitrarily close to as grows. This gives sense to the following definition:

Definition 1.1

A prediction strategy is called universally consistent with respect to a class of stationary and ergodic processes if for each process in the class,

Thus, universally consistent strategies asymptotically achieve the best possible loss for all processes in the class. Algoet [1] and Morvai, Yakowitz and Györfi [24] proved that there exist universally consistent strategies with respect to the class of all bounded, stationary and ergodic processes. However, the prediction algorithms discussed in these papers are either very complex or have an unreasonably slow rate of convergence, even for well-behaved processes. Building on the methodology developed in recent years for prediction of individual sequences (see Cesa-Bianchi and Lugosi [8] for a survey and references), Györfi and Lugosi introduced in [18] a histogram-based prediction strategy which is “simple” and yet universally consistent with respect to the class . A similar result was also derived independently by Nobel [25]. Roughly speaking, both methods consider several partitioning estimates (called experts in this context) and combine them at time according to their past performance. For this, a probability distribution on the set of experts is generated, where a “good” expert has relatively large weight, and the average of all experts’ predictions is taken with respect to this distribution.

The purpose of this paper is to further investigate nonparametric expert-oriented strategies for unbounded time series prediction. With this aim in mind, in Section 2.1 we briefly recall the histogram-based prediction strategy initiated in [18], which was recently extended to unbounded processes by Györfi and Ottucsák [20]. In Section 2.2 and 2.3 we offer two “more flexible” strategies, called respectively kernel and nearest neighbor-based prediction strategies, and state their universal consistency with respect to the class of all (non-necessarily bounded) stationary and ergodic processes with finite fourth moment. In Section 2.4 we consider as an alternative a prediction strategy based on combining generalized linear estimates. In Section 2.5 we use the techniques of the previous section to give a simpler prediction strategy for stationary Gaussian ergodic processes. Extensive experimental results based on real-life data sets are discussed in Section 3, and proofs of the main results are given in Section 4.

2 Universally consistent prediction strategies

2.1 Histogram-based prediction strategy

In this section, we briefly describe the histogram-based prediction scheme due to Györfi and Ottucsák [20] for unbounded stationary and ergodic sequences. The strategy is defined at each time instant as a convex combination of elementary predictors (the so-called experts), where the weighting coefficients depend on the past performance of each elementary predictor. To be more precise, we first define an infinite array of experts , as follows. Let be a sequence of finite partitions of , and let be a sequence of finite partitions of . Introduce the corresponding quantizers:

and

To lighten notation a bit, for any and , we write for the sequence and similarly, for we write for the sequence .

The sequence of experts , is defined as follows. Let be the locations of the matches of the last seen strings of length and of length in the past according to the quantizer with parameters and :

and introduce the truncation function

Now define the elementary predictor by

where is defined to be and

Here and throughout, for any finite set , the notation stands for the size of . We note that the expert can be interpreted as a (truncated) histogram regression function estimate drawn in (Györfi, Kohler, Krzyżak and Walk [17]).

The proposed prediction algorithm proceeds with an exponential weighting average method. Formally, let be a probability distribution on the set of all pairs of positive integers such that for all and , . Fix a learning parameter , and define the weights

and their normalized values

The prediction strategy at time is defined by

It is proved in [20] that this scheme is universally consistent with respect to the class of all (non-necessarily bounded) stationary and ergodic processes with finite fourth moment, as stated in the following theorem. Here and throughout the document, denotes the Euclidean norm.

Theorem 2.1 (Györfi and Ottucsák [20])

Assume that

-

(a)

The sequence of partitions is nested, that is, any cell of is a subset of a cell of , ;

-

(b)

The sequence of partitions is nested;

-

(c)

The sequence of partitions is asymptotically fine, i.e., if

denotes the diameter of a set, then for each sphere centered at the origin

-

(d)

The sequence of partitions is asymptotically fine.

Then, if we choose the learning parameter of the algorithm as

the histogram-based prediction scheme defined above is universally consistent with respect to the class of all jointly stationary and ergodic processes such that

The idea of combining a collection of concurrent estimates was originally developed in a non-stochastic context for on-line sequential prediction from deterministic sequences (see Cesa-Bianchi and Lugosi [8] for a comprehensive introduction). Following the terminology of the prediction literature, the combination of different procedures is sometimes termed aggregation in the stochastic context. The overall goal is always the same: use aggregation to improve prediction. For a recent review and an updated list of references, see Bunea and Nobel [6] and Bunea, Tsybakov and Wegkamp [7].

2.2 Kernel-based prediction strategies

We introduce in this section a class of kernel-based prediction strategies for (non-necessarily bounded) stationary and ergodic sequences. The main advantage of this approach in contrast to the histogram-based strategy is that it replaces the rigid discretization of the past appearances by more flexible rules. This also often leads to faster algorithms in practical applications.

To simplify the notation, we start with the simple “moving-window” scheme, corresponding to a uniform kernel function, and treat the general case briefly later. Just like before, we define an array of experts , where and are positive integers. We associate to each pair two radii and such that, for any fixed

| (2) |

and

| (3) |

Finally, let the location of the matches be

Then the elementary expert at time is defined by

| (4) |

where is defined to be and

The pool of experts is mixed the same way as in the case of the histogram-based strategy. That is, letting be a probability distribution over the set of all pairs of positive integers such that for all and , for , we define the weights

together with their normalized values

| (5) |

The general prediction scheme at time is then defined by weighting the experts according to their past performance and the initial distribution :

Theorem 2.2

The proof of Theorem 2.2 is in Section 4. This theorem may be extended to a more general class of kernel-based strategies, as introduced in the next remark.

Remark 2.1 (General kernel function)

Define a kernel function as any map . The kernel-based strategy parallels the moving-window scheme defined above, with the only difference that in definition (4) of the elementary strategy, the regression function estimate is replaced by

Observe that if is the naive kernel where denotes the indicator function and , we recover the moving-window strategy discussed above. Typical nonuniform kernels assign a smaller weight to the observations and whose distance from and is larger. Such kernels promise a better prediction of the local structure of the conditional distribution.

2.3 Nearest neighbor-based prediction strategy

This strategy is yet more robust with respect to the kernel strategy and thus also with respect to the histogram strategy. This is because it does not suffer from the scaling problems of histogram and kernel-based strategies where the quantizer and the radius have to be carefully chosen to obtain “good” performance.

To introduce the strategy, we start again by defining an infinite array of experts , where and are positive integers. Just like before, is the length of the past observation vectors being scanned by the elementary expert and, for each , choose such that

| (6) |

and set

(where is the floor function). At time , for fixed and (, the expert searches for the nearest neighbors (NN) of the last seen observation and in the past and predicts accordingly. More precisely, let

and introduce the elementary predictor

if the sum is non void, and otherwise. Next, set

Finally, the experts are mixed as before: starting from an initial probability distribution , the aggregation scheme is

where the probabilities are the same as in (5).

Theorem 2.3

Denote by the class of all jointly stationary and ergodic processes such that . Choose the parameter of the algorithm as

and suppose that (6) is verified. Suppose also that for each vector the random variable

has a continuous distribution function. Then the nearest neighbor prediction strategy defined above is universally consistent with respect to the class .

2.4 Generalized linear prediction strategy

This section is devoted to an alternative way of defining a universal predictor for stationary and ergodic processes. It is in effect an extension of the approach presented in Györfi and Lugosi [18] to non-necessarily bounded processes. Once again, we apply the method described in the previous sections to combine elementary predictors, but now we use elementary predictors which are generalized linear predictors. More precisely, we define an infinite array of elementary experts , as follows. Let be real-valued functions defined on . The elementary predictor generates a prediction of form

where the coefficients are calculated according to the past observations , , and

Formally, the coefficients are defined as the real numbers which minimize the criterion

| (7) |

if , and the all-zero vector otherwise. It can be shown using a recursive technique (see e.g., Tsypkin [29], Györfi [15], Singer and Feder [27], and Györfi and Lugosi [18]) that the can be calculated with small computational complexity.

The experts are mixed via an exponential weighting, which is defined the same way as earlier. Thus, the aggregated prediction scheme is

where the are calculated according to (5).

Combining the proof of Theorem 2.2 and the proof of Theorem 2 in [18] leads to the following result:

Theorem 2.4

Suppose that and, for any fixed , suppose that the set

is dense in the set of continuous functions of variables. Then the generalized linear prediction strategy defined above is universally consistent with respect to the class of all jointly stationary and ergodic processes such that

2.5 Prediction of Gaussian processes

We consider in this section the classical problem of Gaussian time series prediction (cf. Brockwell and Davis [5]). In this context, parametric models based on distribution assumptions and structural conditions such as AR(), MA(), ARMA(,) and ARIMA(,,) are usually fitted to the data (cf. Gerencsér and Rissanen [13], Gerencsér [11, 12], Goldenshluger and Zeevi [14]). However, in the spirit of modern nonparametric inference, we try to avoid such restrictions on the process structure. Thus, we only assume that we observe a string realization of a zero mean, stationary and ergodic, Gaussian process , and try to predict , the value of the process at time . Note that there is no side information vectors in this purely time series prediction framework.

It is well known for Gaussian time series that the best predictor is a linear function of the past:

where the minimize the criterion

Following Györfi and Lugosi [18], we extend the principle of generalized linear estimates to the prediction of Gaussian time series by considering the special case

i.e.,

Once again, the coefficients are calculated according to the past observations by minimizing the criterion:

if , and the all-zero vector otherwise.

With respect to the combination of elementary experts , Györfi and Lugosi applied in [18] the so-called “doubling-trick”, which means that the time axis is segmented into exponentially increasing epochs and at the beginning of each epoch the forecaster is reset.

In this section we propose a much simpler procedure which avoids in particular the doubling-trick. To begin, we set

where

and combine these experts as before. Precisely, let be an arbitrarily probability distribution over the positive integers such that for all , , and for , define the weights

and their normalized values

The prediction strategy at time is defined by

By combining the proof of Theorem 2.2 and Theorem 3 in [18], we obtain the following result:

Theorem 2.5

The linear prediction strategy defined above is universally consistent with respect to the class of all jointly stationary and ergodic zero-mean Gaussian processes.

The following corollary shows that the strategy provides asymptotically a good estimate of the regression function in the following sense:

Corollary 2.1 is expressed in terms of an almost sure Cesáro consistency. It is an open problem to know whether there exists a prediction rule such that

| (8) |

for all stationary and ergodic Gaussian processes. Schäfer [26] proved that, under some conditions on the time series, the consistency (8) holds.

3 Experimental results and analyses

We evaluated the performance of the histogram, moving-window kernel, NN and Gaussian process strategies on two real world data sets. Furthermore, we compared these performances to those of the standard ARMA family of methods on the same data sets. We show in particular that the four methods presented in this paper usually perform better than the best ARMA results, with respect to three different criteria.

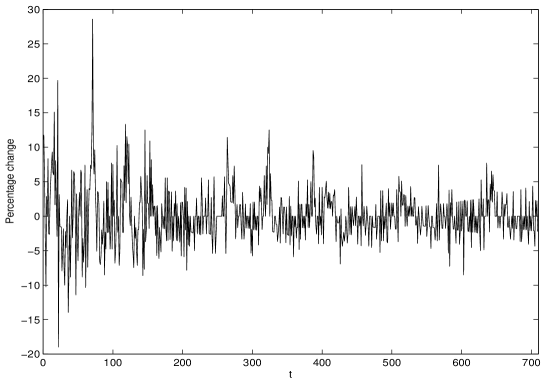

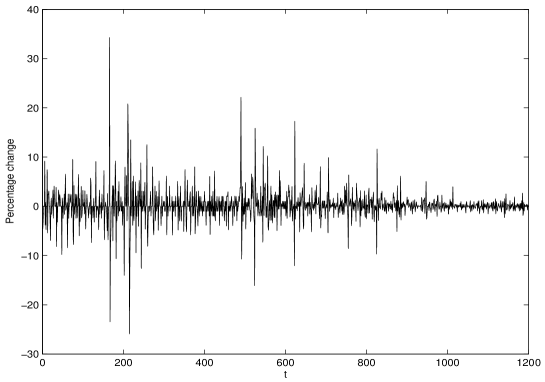

The two real-world time series we investigated were the monthly USA unemployment rate for January 1948 until March 2007 (710 points) and daily USA federal funds interest rate for 12 January 2003 until 21 March 2007 (1200 points) respectively, extracted from the website economagic.com. In order to remove first-order trends, we transformed these time series into time series of percentage change compared to the previous month or day, respectively. The resulting time series are shown in Figs. 2 and 2.

Before testing the four methods of the present paper alongside the ARMA methods, we tested whether the resulting time series were trend/level stationary using two standard tests, the KPSS test [23] and the PP test [10]. For both series using the KPSS test, we did not reject the null hypothesis of level stationarity at and respectively, and for both series using the PP test (which has for null hypothesis the existence of a unit root and for alternative hypothesis, level stationarity), the null hypothesis was rejected at and .

We remark that this means the ARIMA family of models, richer than ARMA is unnecessary, or equivalently, we need only to consider the ARIMA family ARIMA. As well as this, the Gaussian process method requires the normality of the data. Since the original data in both data sets is discretized (and not very finely), this meant that the data, when transformed into percentage changes only took a small number of fixed values. This had the consequence that directly applying standard normality tests gave curious results even when histograms of the data appeared to have near-perfect Gaussian forms; however adding small amounts of random noise to the data allowed us to not systematically reject the hypothesis of normality.

Given each method and each time series (here, or ), for each we used the data to predict the value of . We used three criteria to measure the quality of the overall set of predictions. First, as described in the present paper, we calculated the normalized cumulative prediction squared error (since we start with for practical reasons, this is almost but not exactly what has been called until now). Secondly, we calculated , the normalized cumulative prediction error over only the last 50 predictions of the time series in order to see how the method was working after having learned nearly the whole time series. Thirdly, since in practical situations we may want to predict only the direction of change, we compared the direction (positive or negative) of the last predicted points with respect to each previous, known point, to the real directions. This gave us the criteria : the percentage of the direction of the last 50 points correctly predicted.

As in [19] and [22], for practical reasons we chose a finite grid of experts: and for the histogram, kernel and NN strategies, fixing and . For the histogram strategy we partitioned the space into each of equally sized intervals, for the kernel strategy we let the radius take the values and for the NN strategy we set Furthermore, we fixed the probability distribution as the uniform distribution over the experts. For the Gaussian process method, we simply let and fixed the probability distribution as the uniform distribution over the experts.

Used to compare standard methods with the present nonparametric strategies, the ARMA algorithm was run for all pairs . The ARMA family of methods is a combination of an autoregressive part AR and a moving-average part MA. Tables 1 and 2 show the histogram, kernel, NN, Gaussian process and ARMA results for the unemployment and interest rate time series respectively. The three ARMA results shown in each table are those which had the best , and respectively (sometimes two or more had the same , in which case we chose one of these randomly). The best results with respect to each of the three criteria are shown in bold.

| histogram | 15.66 | 4.82 | 68 |

| kernel | 15.44 | 4.99 | 68 |

| NN | 15.40 | 4.97 | 70 |

| Gaussian | 16.35 | 5.02 | 76 |

| ARMA | 16.26 | 5.31 | 72 |

| ARMA | 16.68 | 4.86 | 78 |

| ARMA | 16.46 | 5.12 | 78 |

| histogram | 9.78 | 0.52 | 88 |

| kernel | 9.77 | 0.57 | 86 |

| NN | 9.86 | 0.79 | 80 |

| Gaussian | 9.98 | 0.62 | 82 |

| ARMA | 9.90 | 0.78 | 70 |

| ARMA | 10.30 | 0.60 | 82 |

| ARMA | 10.12 | 0.63 | 88 |

We see via Tables 1 and 2 that the histogram, kernel and NN strategies presented here outperform all 36 possible ARMA models () in terms of normalized cumulative prediction error , and that the Gaussian process method performs similarly to the best ARMA method. In terms of the and criteria, all of the present methods and the best ARMA method provide broadly similar results. From a practical point of view, we note also that the histogram, kernel and NN methods also run much faster than a single ARMA trial on a standard desktop computer. For example, the NN method is of the order of 10 to 100 times faster than an ARMA for a time series with about 1000 points, depending on the values of and .

4 Proofs

4.1 Proof of Theorem 2.2

The proof of Theorem 2.2 strongly relies on the following two lemmas. The first one is known as Breiman’s generalized ergodic theorem.

Lemma 4.1 (Breiman [4])

Let be a stationary and ergodic process. For each positive integer , let denote the left shift operator, shifting any sequence by digits to the left. Let be a sequence of real-valued functions such that almost surely for some function . Suppose that . Then

Lemma 4.2 (Györfi and Ottucsák [20])

Let be a sequence of prediction strategies (experts). Let be a probability distribution on the set of positive integers. Denote the normalized loss of any expert by

where the loss function is convex in its first argument . Define

where is monotonically decreasing, and set

If the prediction strategy is defined by

then, for every ,

Proof of Theorem 2.2. Because of (1) it is enough to show that

With this in mind, we introduce the following notation:

for all , where is defined to be , and . Thus, for any , we can write

By a double application of the ergodic theorem, as , almost surely, for a fixed and , we may write

Therefore, for all and ,

Thus, by Lemma 4.1, as , almost surely,

Denote, for Borel sets and ,

and set

Next, let denote the closed ball with center and radius . Let

then for any and which are in the support of , we have

as and for -almost all and by the Lebesgue density theorem (see Györfi, Kohler, Krzyżak and Walk [17], Lemma 24.5). Therefore,

Observe that

| (since ) | |||

| (by Jensen’s inequality). |

Consequently,

due to the assumptions of the theorem. Therefore, for fixed the sequence of random variables is uniformly integrable and by using the dominated convergence theorem we obtain

Invoking the martingale convergence theorem (see, e.g., Stout [28]), we then have

and consequently,

We next apply Lemma 4.2 with the choice and the squared loss

We obtain

On one hand, almost surely,

On the other hand,

Therefore, almost surely,

| (since and ). |

Summarizing these bounds, we get that, almost surely,

and the theorem is proved.

4.2 Sketch of the proof of Theorem 2.4

For fixed and , let

Then, following the proof of Theorem 2 in [18] one can show that for all ,

| (9) |

where the are defined in (7). Using equality (9) and Lemma 4.1, for any fixed and we obtain that, almost surely,

Then, with similar arguments to Theorem 2 in [18], it can be shown that

Finally, by using Lemma 4.2, the assumptions and , and repeating the arguments of the proof of Theorem 2.2, we obtain

as desired.

References

- [1] Algoet, P. Universal schemes for prediction, gambling and portfolio selection, Ann. Probab., Vol. 20, pp. 901–941, 1992.

- [2] Algoet, P. The strong law of large numbers for sequential decisions under uncertainty, IEEE Trans. Inform. Theory, Vol. 40, pp. 609–633, 1994.

- [3] Bosq, D. Nonparametric Statistics for Stochastic Processes. Estimation and Prediction, Lecture Notes in Statistics, 110, Springer-Verlag, New York, 1996.

- [4] Breiman, L. The individual ergodic theorem of information theory, Ann. Math. Statist., Vol. 28, pp. 809–811, 1957. Correction. Ann. Math. Statist., Vol. 31, pp. 809–810, 1960.

- [5] Brockwell, P. and Davis, R. A. Time Series: Theory and Methods, Second edition, Springer-Verlag, New York, 1991.

- [6] Bunea, F. and Nobel, A. Sequential procedures for aggregating arbitrary estimators of a conditional mean, (submitted), Florida State University, 2005. http://stat.fsu.edu/~flori/ps/bnapril2005IEEE.pdf

- [7] Bunea, F., Tsybakov, A. B. and Wegkamp, M. H. Aggregation for Gaussian regression, Ann. Statist., (accepted), 2007.

- [8] Cesa-Bianchi, N. and Lugosi, G. Prediction, Learning, and Games, Cambridge University Press, New York, 2006.

- [9] Devroye, L., Györfi, L. and Lugosi, G. A Probabilistic Theory of Pattern Recognition, Springer-Verlag, New York, 1996.

- [10] Durlauf, S. N. and Phillips, P. C. B. Trends versus random walks in time series analysis, Econometrica, Vol. 56, pp. 1333–1354, 1988.

- [11] Gerencsér, L. estimation and nonparametric stochastic complexity, IEEE Trans. Inform. Theory, Vol. 38, pp. 1768–1779, 1992.

- [12] Gerencsér, L. On Rissanen’s predictive stochastic complexity for stationary ARMA processes, J. Statist. Plann. Inference, Vol. 41, pp. 303–325, 1994.

- [13] Gerencsér, L. and Rissanen, J. A prediction bound for Gaussian ARMA processes, Proc. of the 25th Conference on Decision and Control, 1487–1490, 1986.

- [14] Goldenshluger, A. and Zeevi, A. Nonasymptotic bounds for autoregressive time series modeling, Ann. Statist., Vol. 29, pp. 417–444, 2001.

- [15] Györfi, L. Adaptive linear procedures under general conditions, IEEE Trans. Inform. Theory, Vol. 30, pp. 262–267, 1984.

- [16] Györfi, L., Härdle, W., Sarda, P. and Vieu, P. Nonparametric Curve Estimation from Time Series, Lecture Notes in Statistics, 60, Springer-Verlag, Berlin, 1989.

- [17] Györfi, L., Kohler, M., Krzyżak, A. and Walk, H. A Distribution-free Theory of Nonparametric Regression, Springer-Verlag, New York, 2002.

- [18] Györfi, L. and Lugosi, G. Strategies for sequential prediction of stationary time series, in Modeling Uncertainty, Internat. Ser. Oper. Res. Management Sci., Vol. 46, pp. 225–248, Kluweer Acad. Publ., Boston, 2001.

- [19] Györfi, L., Lugosi, G. and Udina, F. Nonparametric kernel-based sequential investment strategies, Math. Finance, Vol. 16, pp. 337–357, 2006.

- [20] Györfi, L. and Ottucsák, G. Sequential prediction of unbounded time series, IEEE Trans. Inform. Theory, Vol. 53, pp. 1866–1872, 2007.

- [21] Györfi, L. and Schäfer, D. Nonparametric prediction, in J. A. K. Suykens, G. Horváth, S. Basu, C. Micchelli and J. Vandevalle, editors, Advances in Learning Theory: Methods, Models and Applications, pp. 339–354, IOS Press, NATO Science Series, 2003. http://www.szit.bme.hu/~oti/portfolio/histog.pdf

- [22] Györfi, L., Udina, F. and Walk, H. Nonparametric nearest neighbor based empirical portfolio selection strategies, Technical Report, 2006. http://www.szit.bme.hu/~oti/portfolio/NN.pdf

- [23] Kwiatkowski, D., Phillips, P. C. B., Schmidt, P. and Shin, Y. Testing the null hypothesis of stationarity against the alternative of a unit root, J. Econometrics, Vol. 54, pp. 159–178, 1992.

- [24] Morvai, G., Yakowitz, S. and Györfi, L. Nonparametric inference for ergodic, stationary time series, Ann. Statist., Vol. 24, pp. 370–379, 1996.

- [25] Nobel, A. On optimal sequential prediction for general processes, IEEE Trans. Inform. Theory, Vol. 49, pp. 83–98, 2003.

- [26] Schäfer, D. Strongly consistent online forecasting of centered Gaussian processes, IEEE Trans. Inform. Theory, Vol. 48, pp. 791–799, 2002.

- [27] Singer, A. C. and Feder, M. Universal linear least-squares prediction, International Symposium of Information Theory, 2000.

- [28] Stout, W. F. Almost Sure Convergence, Academic Press, New York, 1974.

- [29] Tsypkin, Ya. Z. Adaptation and Learning in Automatic Systems, Academic Press, New York, 1971.

- [30] Yule, U. On a method of investigating periodicities in disturbed series, with special reference to Wölfer’s sunspot numbers, Philos. Trans. Roy. Soc., Vol. A 226, pp. 267–298, 1927.