Short-time behaviour of demand and price viewed through an

exactly solvable model for heterogeneous interacting market agents

Gunter M. Schütz1,2, Fernando Pigeard de Almeida Prado3,

Rosemary J. Harris4, Vladimir Belitsky5

(1) Institut für Festkörperforschung, Forschungszentrum

Jülich, 52425 Jülich, Germany

(2) Interdisziplinäres Zentrum für Komplexe Systeme, Universität Bonn,

Römerstr. 164, 53117 Bonn, Germany

(3) Departamento de Física e Matemática, FFCLRP, Universidade de São Paulo,

14040-901, Ribeirão Preto, SP, Brazil

(4) School of Mathematical Sciences,

Queen Mary University of London,

Mile End Road, London, E1 4NS, United Kingdom

(5) Instituto de Matemática e Estatística,

Universidade de São Paulo, Rua do Matão, 1010, CEP 05508-090,

São Paulo, SP, Brazil

E-mail: g.schuetz@fz-juelich.de

June 16, 2009.

Abstract: We introduce a stochastic heterogeneous interacting-agent model for the short-time non-equilibrium evolution of excess demand and price in a stylized asset market. We consider a combination of social interaction within peer groups and individually heterogeneous fundamentalist trading decisions which take into account the market price and the perceived fundamental value of the asset. The resulting excess demand is coupled to the market price. Rigorous analysis reveals that this feedback may lead to price oscillations, a single bounce, or monotonic price behaviour. The model is a rare example of an analytically tractable interacting-agent model which allows us to deduce in detail the origin of these different collective patterns. For a natural choice of initial distribution the results are independent of the graph structure that models the peer network of agents whose decisions influence each other.

Keywords: heterogeneous interacting-agent model, asset market, social interaction, collective behavior, temporal fluctuations, price oscillations, exactly solvable models of an asset market

JEL Classification codes: G14, C02, D70, D84.

1 Introduction

Heterogeneous Interacting-Agent Models (HIAMs) are stochastic processes that are intensively employed to analyse and explain complex systems in diverse disciplines. In this paper, we propose a HIAM for analysing short-time fluctuations of an asset price in a single risky asset market which is a stylized model of the real asset market. Even though our model may describe quite diverse situations – as any other HIAM does – we have chosen to discuss it in the framework of the asset market because this setting facilitates the exposition and because of the broad interest in understanding market behaviour. In this setting the model explains the emergent behaviour of a large population of heterogeneous individual traders, where the behaviour of any single one is affected directly (not just indirectly via the asset price) by the behaviour of the whole population or a selected part of it.

We wish to point out that most HIAMs proposed in the literature have been studied by numerical simulation or by some heuristic approximation scheme and often these models are studied primarily in the stationary regime. In contrast, both time-dependent and stationary properties of our model are tractable by exact analytical methods. This allows us to derive rigorously a number of non-trivial dynamic phenomena appearing in the non-equilibrium collective behaviour of agents and thus to obtain a detailed understanding of their origin. Before presenting (in Section 2) the rigorous mathematical construction of our model, we describe it informally and position it in the world of HIAMs (which are extensively reviewed in [11] and [18]).

Basic notions: In our model, agents are market traders that at every time may behave in two ways: they either order to buy or order to sell a unit of a single asset (without knowing if their orders will be fulfilled or not). For simplicity of language, however, we shall just say that an agent “buys/sells” a unit of the asset, although we in fact mean “orders to buy/sell”. We shall also say that an agent is a buyer (seller) if her current order is a buy-order (respectively, a sell-order). According to the above, the excess demand of the asset is the difference between the number of buyers and sellers. We use the term relative excess demand for the difference between buyers and sellers divided by the total number of market agents (number of buyers plus the number of sellers).

A very important assumption of the model is that (intermediate) transactions may occur out of equilibrium, that is, when the excess demand is not zero. More specifically, we assume that (intermediate) transactions are permanently occurring in the market, independently of whether supply equals demand or not.

Price evolution: The price evolution of an asset in many regulated trading markets is determined by a series of rules known as the continuous double auction (see Ref. [30] or Ref. [8], the latter exposes these rules from a perspective linked to the ideas that form the basis of our model). Thus, when modeling this evolution, the principal question encountered is how precise these rules should be mirrored. Very faithful HIAMs of the continuous double auction are not analytically tractable (see [16] and references therein). Being aware of this fact, we resorted to an alternative approach for mimicking price dynamics.

There is a natural choice between two approaches to model price dynamics that “dominate” in the HIAM area. They do not contradict the features that result from the rules of the continuous double auction; they just reflect this dynamics at different time scales mainly because they discard from consideration a part of those orders that are not fulfilled. Accordingly, by adopting these approaches, one can distort in a model some properties of the real flux of orders. A particularly common distortion is the use of Poisson point processes: If a model would aim at mimicking faithfully the continuous double auction then it should incorporate that order arrival times do not form a Poissonian flow (see [30]). However, Poisson point process appear in almost all HIAMs because they underly the construction of continuous-time Markov processes which makes the model more amenable to analytical analysis.. For this reason, also we use a Poisson point process in our model. In Ref.[16] one finds some heuristics that suggests that a Poissonian flow is close to the flow of orders that are executed in the continuous double auction.

One of the two dominating approaches mentioned above is grounded on the market-clearing condition which requires that the current excess demand is zero at the current asset price. Indeed, this may seem to be a reasonable criterion for the determination of the current asset price. Examples of works that have adopted this approach are [10], [9] and [15]. However, since the current price is in fact a transaction price, the market-clearing condition would exclude transactions occurring out of equilibrium.

In the second type of approach, the increment of the asset price (or its logarithm) increases with the relative excess demand. Among the papers pioneering this approach (within the HIAM setup) is [3]. As the title of that work indicates, this approach is appropriate for studying a market out of equilibrium. The principal reason for that is that the price resulting from this rule does not enforce equality between the numbers of the asset units bought and sold. The adoption of this approach requires additional assumptions like the presence of a market maker that adjusts the price, rather than the market-clearing condition as the determinant of the price. In the present work we choose this second approach because it usually leads to simpler stochastic and dynamical systems from which the price process produces stylized trajectories. Moreover, our focus is on the short-time market behavior where a market may indeed be far from equilibrium.

We use the term “price increment” as a shorthand for the increment between the current price and the price that will be negotiated in the next transaction. This price increment will depend on the negotiation powers of sellers and buyers. A natural assumption is that the negotiation power of sellers over buyers increases when the relative excess demand does (the fewer sellers there are, the more power they have). We account for this relationship by assuming that the current price return is a linearly increasing function of the relative excess demand (price return is the increment of the price logarithm). This price update mechanism is already proposed by several authors, see e.g., [25], [19] and [6]. These considerations lead to the price update rule

| (1) |

Here the positive model parameter is the feedback strength of the demand on the price. This relationship reproduces the approximately linear part of the hyperbolic tangent relation reported in Ref. [29] for various stocks.

Social interactions: The interaction between agents in our model is based on the notion that individual agents include in their judgement whether to buy or sell, the decisions of peer traders, see e.g., [20] and [26] for a brief survey and discussion. It is fair to assume that agents do not simply follow the whole crowd. Instead, we postulate a herding mechanism that is proportional to the buying (resp., selling) decisions only of trusted peers of an agent. The strength of this influence is quantified by a non-negative parameter , called the social susceptibility. The peer groups are modelled by a graph structure: the agents are the nodes of a graph, and the bonds pointing into a node define the peers of this node. Notice that the individual structure of peer groups allows for modelling highly heterogeneous and directed social interaction, unlike e.g., in the work [7] where undirected graphs are considered.

It is worth noting that our theoretical result (Proposition 1) describing the dynamics of the expected relative excess demand, holds for any graph of social interactions. This independence is an interesting property of our model. It adds information to the understanding of how the topology of interactions influences the generic properties of the HIAM. For example, if the graph topology is such that the system (indexed by agents positions) is ergodic, then, by evoking the system ergodicity, we can approach the dynamics of the relative excess demand by the dynamics of its expected value (described with Proposition 1). Our references for these issues are [23] and [17].

The agent interaction discussed above is just one of many possible forms of social interaction generically called strategic complementarity or positive externality and thoroughly described in the reviews [11] and [18]. The particular form reflected in our model was chosen for the following two reasons. (1) Since we intend to model an asset market, we include a chartist behaviour: market agents have the tendency to buy when the price increases and to sell otherwise. Since in our model the price increment is coupled to the relative excess demand, our interaction mechanism makes agents behave in just this manner. (2) Our construction is also inspired by previous successful work that used proportions of diverse market groups for modelling the formation of strategies. This notion allows us to diversify the structure of influences by attributing different peer groups to different agents. This reflects market agents that try to draw information about the best strategy (buy or sell) from the behaviour of their peers. Accordingly, market agents will have the tendency to buy when the majority of their peers buy and to sell otherwise. Of particularly significant impact on this construction were the papers [25] and [4].

Individual heterogeneity: Another important characteristic of contemporary HIAMs is the heterogeneity of agents. This means that agents behave differently under similar circumstances. That this phenomenon is present in real market agent behaviour has been substantiated by firm arguments which are grounded on empirical facts and on economic and psychological considerations, see e.g., [14]. In our model agents are heterogeneous not only in the structure of their individual peer groups but also in their evaluation of the fundamental value of the traded asset. This individual heterogeneity is quantified by a probability distribution function in the following way. Each time when an agent has to make up her mind about the fundamental value, we sample , the “noise” in the evaluation of agent at time , from a mean-zero distribution, add an amount and interpret this sum as the logarithm of the evaluation of the fundamental value of this agent. This implies that is the average – taken over the whole population – of the individual evaluations and that the cumulative distribution of has the following interpretation:

| (2) |

The behaviour of the model will depend on the function , which for brevity we shall sometimes refer to as the “average fundamental value evaluation”. The form of depends on all kinds of information which in the framework of the efficient market hypothesis would be fully accounted for by the market price , i.e., one would set if on average the agents believed in an efficient market. To allow for in principle arbitrary deviations from this idealized view we make a general ansatz

| (3) |

where is a function which may be explicitly time-dependent due to possible exogeneous influence that changes the average evaluation. An appropriate choice of then enables us to model a real asset market in which the average evaluation of the fundamental value changes in time, caused by endogenous factors and/or by exogenous factors. Two simple choices of this dependence are discussed in more detail in Sec. 4. The distribution does not change in time and, as a working hypothesis, it appears reasonable to assume finite moments. In fact, we choose uniform i.i.d. noise so that the parameter is a direct measure of the heterogeneity of the population of market agents.

We realize purely fundamentalist trading by the simplest, but still widely modelled, behaviour: to buy when the current price is lower than the estimated fundamental value, and to sell otherwise. Thus, in our model, agents have both speculative and fundamentalist traits in their trading strategies. These components are combined in the following way. An agent will buy (resp., sell) at time , if the following expression is positive (resp., negative):

| (4) |

We shall refer to this expression as the individual asset evaluation (IAE). Here, denotes the position of the agent at time : if (), then the agent is a buyer (seller) at time . Thus the second term of the IAE (4) corresponds to the fundamentalist strategy described in the previous paragraph, where stands for the logarithm of the fundamental value evaluation of individual at time . The first term corresponds to the speculative strategy, because denotes the position ( buys, sells) of the agent at time . So the relation of the “strengths” of these terms determines whether an agent acts more like a speculator or like a fundamentalist.

This completes the informal description of our model. The main result (Proposition 1) to be discussed and derived below contains the following: (1) Under some average uniformity assumptions (detailed below) the expectation of the decision of agent at some time is the same for all agents for any network topology. The time up to which we can prove this result rigorously depends on the choice of model parameters. (2) For some natural choices of this expectation satisfies a linear second order ODE (short for ordinary differential equation) even though the model is intrinsically highly non-linear. The statements (1) and (2) demonstrate that our model provides a rare example of an non-trivial HIAM that is exactly solvable, at least within some time interval . Numerical Monte Carlo simulations indicate an approximate validity of this result for much longer times, but this is not really our concern, since we are mainly interested in non-equilibrium short-time properties of the model. More significantly, the simulations demonstrate that the collective patterns revealed by the expectation are clearly recognizable in a single realization of the dynamics even though the process is noisy and the peer groups may be small and highly heterogeneous.

These mathematical results are proved for two qualitatively different assumptions on , viz. constant average fundamental value evaluation (irrespective of the actual evolution of the asset price) and an average fundamental value evaluation that follows the price up to some systematic bias. The ODE reveals interesting collective behaviour of the agents since its solution may be either a monotonic function, or a function with unique extremal point, or a damped oscillating function. From this we deduce under which circumstances the demand and the price will be monotone in time, when they bounce once, and when they oscillate. We give the conditions for each one of these three possibilities in terms of the relation between the market parameters that are reflected in our HIAM: the strength of social susceptibility , the heterogeneity of the fundamental value evaluations parametrized by , and the strength of the demand feedback and the initial mismatch between market price and average value evaluation.

The paper is organized as follows. In Section 2, we present a precise definition of our HIAM and further comment on some of its salient features. In order for this section to be self-contained, we repeat some of the definitions already introduced above. In Section 3, we state the central result – Proposition 1. In the main part of the paper, Section 4, we elucidate some consequences of Proposition 1 to analyse short-time behaviour of demand and price in an asset market. We also present the simulation results and discuss the role of the topology of peer groups. A concluding Section 5 very briefly summarizes our main results and points to some open questions and further related work. In the more technical Appendix A, we present the proofs. This section can be skipped by a reader interested in the results rather than their proofs. 111Note that occasionally in the paper we will draw on analogies with spin systems for the benefit of readers familiar with the statistical mechanics literature. However, we stress that no extensive use of physics connotations is made and a reader without the relevant background can safely ignore such references.

2 The Model

We start by establishing the structure of social influences among agents. It is described by a finite directed graph that we denote by . Each node represents an agent in the asset market. The cardinality of the set of nodes is the total number of agents in the market. We put a bond pointing from to when we want to model that the decision of the agent represented by node is influenced by the opinion of the agent represented by node . The set of such nodes forms the peer group of agent which we assume to be non-empty. That is, our model has no “lonely” traders whose decisions are entirely unaffected by their peers. All bonds in the graph form the bond set . The actual structure of will not be specified now because it does not affect the validity of our main result (Proposition 1). Note that in the special case where, for all pairs of nodes , “ influences ” “ influences ”, we have an undirected network.

For each node and each time , we introduce the binary variable and call it the state of at time . Sometimes we will also refer to it as the “position” or “decision” of the agent – as outlined earlier, we interpret (respectively, ) as “the agent wishes to buy (resp., sell) one unit of stock at time ”. The quantity denotes the set of all and we postulate that flips between as time goes on.

The time evolution of our model is a stochastic process with a family of random variables , (logarithm of the asset price), (logarithm of the average evaluation of its fundamental value). In slight abuse of language we shall, from now on, omit to state the logarithmic relation between our model quantities and market prices or values, and simply speak about price or fundamental value respectively.

In order to define the stochastic dynamics we first recall that in order to allow heterogeneity in the individual evaluations of the fundamental value, we assume that , , are independent and identically distributed random variables, where for each , is an arbitrary strictly increasing sequence of times. We remark that this use of annealed disorder (as opposed to quenched disorder where would not change in time) is appropriate for the absence of the market-clearing condition: if a bid or ask of an agent has not been satisfied, she may withdraw it and substitute it later by a bid or ask with another price. For a discussion of quenched and annealed disorder see [13] and [28]. In our model with uniform distribution in the individual evaluation of the fundamental value at a given time , is a random variable from the set . The quantity , proportional to the standard deviation of the distribution, is a measure of the heterogeneity of the population of agents.

Now we are in position to define the stochastic process . Consider first the model parameter which reflects what the average of agents thinks what the fundamental value of the asset is. Technically, the relation (3) in which we may choose the parameter to depend on the random variable turns itself into a random variable even if is deterministic. Two specific deterministic choices of the relationship will be examined in detail in Section 4. For such deterministic the stochastic dynamics can be defined in terms of the random variables and alone.

It remains to define the stochastic evolution of and . Formally, the discrete decision process in our model is the first component of the stochastic process . Given we define the evolution of using the Harris graphical approach, which is very popular in the Interacting Particle Systems field (see [22]). We employ the method here because it can be easily understood.

To each node we attribute a Poisson point process (PPP), that is, a set of marks on the “time” semi-line such that are independent random variables, each one having an exponential distribution with mean . The PPP’s are postulated to be independent across the population . Each agent , at each mark of “her” PPP, draws a value from the random variable and sets her position at time according to the following rule (see (4):

| (5) |

In terms of the individual asset evaluation (4), the decision rule takes the simple intuitive form

| (6) |

In order to define for , we assume that does not vary during two subsequent decision times, that is, for , . The independence of the PPPs ensures that the probability of two or more marks to coincide is zero and hence, for fixed and , the decision rule (5) and the preceding assumption define uniquely the value of (except on a measurable set of probability zero). Notice that we assume a PPP in order to keep the model simple and analytically tractable. For a discussion of non-exponential interarrival times of decisions see, e.g., [30].

Using (1) we can now define the evolution of as

| (7) |

This is the time-integrated form of the widely used assumption (1) that the price change at time is proportional to the excess demand at that instant of time, which we discussed in the introduction. In the previous graphical construction the value of entering (5) is understood as the price immediately before the decision taken at time .

We remind the reader that the determination of , according to (7), does not result from the market-clearing condition which would instead require that the current excess demand is zero at the current asset price. Although, in general, the market-clearing condition must be satisfied at equilibrium prices, it excludes an important factor which is crucial for price dynamics in speculative markets. Namely, that some transactions occur – and consequently transaction prices are registered – out of equilibrium, that is, at prices where demand and supply do not match. Since in speculative markets, demand and supply are strongly influenced by the observed price history, this apparently harmless fact leads to completely different price dynamics to those resulting from a market-clearing condition – see [32] for an interesting discussion. In fact, it can be shown that the adoption of a market-clearing condition in our model would make our asset price fluctuate around (the average evaluation of the fundamental value). This would exclude stylized facts like price bubbles ( moving away from ) and price crashes. In order to study the effect of transactions occurring out of equilibrium on price dynamics, we assume that the observed transaction prices change little by little in accordance with the pressure of non-zero excess demands divided by the trading volume. The simplest way to model this dependence is given by (7). Similar price mechanisms are also considered in [25], [19] and [6].

The process that we have just constructed is Markov. This is worth noting because the markovness is essentially employed in the proof of our main result (Proposition 1). This property is yielded by the very construction. Let us be more specific in respect. The first cornerstone that supports the markovness is the lack of memory property of each one of the Poisson point processes that we use to determine the times of position updates of the agents. The second cornerstone is the rule (5) that is tailed so to ensure that an update of an agent’s position, when its time comes, depends solely on the state of the process’s entities at the time of update (namely, and ) and of the entities that are independent of everything else (namely, ). The third cornerstone for the markovness of our process is the following fact: given the history of the process on some time interval , the distribution of at some given depends solely on the process’ state at ; this fact follows readily from eq. (7) since it can be re-written as using the additivity of the integral. The same fact holds true for , but now it is a direct consequence of our definition (3). This is the fourth and the last cornerstone that supports the markovness of the process . We shall only add in respect that none of the components of these triple process – if taken separately – would be a Markov process.

3 Exact results

The result to be formulated in the present section applies to our model when the initial distribution of the node states satisfies a particular property. This property is formulated in the paragraph below, and we shall also argue that it naturally holds for a wide class of real agent market position distributions.

We say that a random -valued element has network homogeneous mean, if the expectation is the same for each (recall, that denotes the value of at the site ). The simplest example of a network homogeneous mean distribution is the product measure on that assigns the same probability, say, to for each . We believe that one would take this product measure for the initial node state distribution, if one wished to express that initial decisions of the agents in a market are similar and independent.

Note, however, that network homogeneous mean does not require that the random variables , , are stochastically independent from each other. As a simple counterexample, consider an Ising model on the torus in (for some ) with a non-vanishing nearest neighbour potential and an external field . Its equilibrium distribution, the Gibbs measure, is known to have correlated spins and, as it may be shown easily, has net homogeneous mean in the sense of our definition.

We have so far introduced all the concepts necessary for the formulation of our main result (Proposition 1 below). At this point we remind the reader of the meaning of the working parameters of the model and its output quantities:

-

is the state of node at time . We say that the node buys [resp., sells] one unit of the asset at time , if [resp., ]. The quantity denotes the whole configuration of states at time . The evolution is defined in (5).

-

denotes the price of the asset at time . The evolution is defined in (7).

-

denotes the average evaluation of the fundamental value of the asset at time . The evolution is defined by the function in (3) and is further specified below.

-

is proportional to the standard deviation of the heterogeneity of agents, i.e., of the deviations from of the individual evaluations of the fundamental value.

-

is the strength of social susceptibility and means the non-negative weight with which the decision of an agent is influenced by her peer group.

-

is the strength of the demand feedback on the price.

We now state the main result for our model (see the appendix for the proof).

Proposition 1.

Consider the continuous-time stochastic process defined in Section 2, on an arbitrary finite oriented graph where each node has at least one peer. Suppose the model satisfies the following conditions:

-

(i) the distribution of the initial node states is a network homogeneous mean distribution;

-

(ii) is the cumulative distribution with uniform density on for some (recall that ).

Assume there exists such that

| (8) |

Then,

-

(a) for every and for each , it holds that , where is the solution of the following integral-differential equation:

(9) with the initial condition

(10) -

(b) and, in particular, the distribution of the node states has network homogeneous mean.

Phrased in statistical mechanics language we solve with Proposition 1 the evolution for a class of stochastic Ising-type processes in which the external field is coupled with the magnetization. As suggested by Brock [5], understanding the dynamical evolution of such a class of systems would be important in modelling price processes with complex systems. The interesting property of Proposition 1 is that it does not impose much restriction on the topology of spin interactions under consideration. In fact, Proposition 1 holds for very complex topologies of (local) interactions: for usual lattice topologies or even more complex structured graphs of social influences. The only essential assumption of Proposition 1 is that , , have network homogeneous mean, and that the noise density of the noise distribution is uniform and symmetric around zero.

The reason for this independence of the network structure is the proportionality of the social interaction of an agent to the relative excess demand observed in her peer group. Therefore the actual size of the peer group (as reflected in the network structure) is not relevant for the decision of an agent. In order to avoid confusion we stress, however, that the use of the expectation value in the proposition does not automatically imply that the typical behaviour of a single realization of the process is described independently of the network structure. This is guaranteed only after applying an ergodicity argument for a given network. Then equation (9) describes ultimately the dynamics of the external field (the dynamics of price) when the number of agents goes to infinity. In the next section we shall examine more closely the behaviour of relative excess demand for a single realization and also supply numerical evidence that, in applications, our results remain valid with great accuracy at times beyond .

4 Collective behaviour

4.1 Preliminaries

In the following two Subsections 4.2 and 4.3 we deduce some corollaries of Proposition 1 that reveal interesting patterns for the dynamics of the relative excess demand and asset price in our model. We consider two particular choices of the fundamental value dynamics (recall that as defined in 3)):

| The average fundamental value evaluation of the asset remains fixed all the time: | (11) | ||||

| The difference between the price and the average fundamental value evaluation | (12) | ||||

| remains fixed: | |||||

Since we are interested in short-time behaviour we do not consider an explicit time-dependence of the parameter .

Our attention to these cases is motivated by a somewhat simplified view according to which the fundamental value of an asset is determined by the “health” of the firm that issued the asset. In this view, an abrupt change of the fundamental value may occur upon the arrival of news regarding the firm. It is then plausible to admit that the average evaluation of the fundamental value of the asset does not change in the time interval between two consecutive arrivals. Such a real market situation is thus appropriately modelled by case (A). Another situation that might be realistic from our point of view, is when the lack of information about the firm’s health makes investors infer the fundamental value of the asset from its market price. For this situation, we consider that the individual asset evaluations will “follow” the asset price with a fixed, but maybe non-zero difference . For positive [negative] this parameter represents a systematic mean overrating [underrating] of the market price from the point of view of the agents, i.e., on average the agents may consider the market to overrate [underrate] what each of them believes to be the actual fundamental value of the asset. This situation corresponds to the case (B).

Obviously, neither of the two situations described above can last for a long time in a real market. However, this fact does not constrain the applicability of our results because the real market situation in question has as its model counterpart the short-time behaviour to which our proposition applies. (Mathematically speaking we mean by short-time behaviour the behaviour on a finite time interval starting at ).

Recall that Proposition 1 is concerned with the behaviour of the expected relative excess demand . For notational brevity we shall henceforth denote this quantity as (our choice of letter is inspired by the analogy with magnetism in a spin system). For a given choice of fundamental value dynamics, Proposition 1 allows us to equate on the interval with the solution of an ODE. For the choices (A) and (B) above this leads to the explicit results presented below as Corollaries 1 and 3 respectively.

Thus far our analysis has been mathematically rigourous. However, in order to make statements about the relative excess demand in a single realization we need to make an additional assumption. The assumption is that for each the random variable

| (13) |

is close to a constant that is equal to the common mathematical expectation of each variable . This property would indeed follow if the sequence obeyed the Law of Large Numbers, or if it were an ergodic sequence. However, to justify the assumption in this way, we need to consider our model on an infinite graph. Moreover, to use the ergodic theory, we would need to impose that the peer groups are finite, of a finite range and of a regular structure; this would allow us to construct a sequence of imbedded graphs , which, in turn, would allow us to formulate the ergodic property assumption in terms of the convergence of to the common expectation of the ’s. The reader can find the details of this approach in, for example, [15]. We did not pursue it here because we found the mathematical formalism to be unnecessarily cumbersome for our purposes. In our work, the additional assumption is instead “verified” by computer simulations (see Section 4.4).

The argument that (with exact equality in the limit of infinite system size) allows us to write down an expression for the asset price defined in (7). Specifically, under the foregoing assumption, we have

| (14) |

where, by Proposition 1,

| (15) |

Moreover, may be calculated or estimated from the relation

| (16) |

which is equivalent to (8)).

Corollaries 2 and 4 below present conclusions about the behaviour of the asset price obtained using (14) for the cases (A) and (B) respectively.

4.2 Case A: Fixed average fundamental value evaluation

Applying the ideas described in Section 4.1, we get the following two corollaries. The formulation employs the following shorthand notations:

| (17) |

-

Corollary 1. If the average fundamental value evaluation is constant in time, i.e., if the condition (11) holds, the time pattern of the expected relative excess demand, , depends on the sign of the determinant expression and is for as follows:

-

(a) If then

(18) -

(b) If then

(19) -

(c) If then

(20)

-

This Corollary arises from (15), Proposition 1 and (11) by noting that (9) may be rewritten as a second-order ODE

| (21) |

This is the evolution equation for the damped harmonic oscillator. The well-known general form of the solution of (21) is

| (22) |

where (below )

| (23) |

With the initial conditions

| (24) |

the corollary follows.

Corollary 1 provides us with precise information about the short-time behaviour of the expected relative excess demand in our model. Under the additional assumption that , this also yields information about the asset price (7). By close detailed inspection of the solutions for the three cases we may rephrase Corollary 1 as applied to the price as follows.

-

Corollary 2. If the average fundamental value evaluation is constant in time, i.e., when the condition (11) holds, the pattern of the asset price, on the time interval depends on the sign of the determinant expression . In particular,

-

(a) If then the price is either a monotonic function, or exhibits a single extremum;

-

(b) If then the price is a monotonic function;

-

(c) If then the price is a -like function damped by an exponential function; there is a large set of parameter values for which more than one oscillation of this function fit into the time interval .

-

This result for the number of extrema in each of the three cases is proved in the appendix. It is non-trivial because of the limitation to the finite time-interval .

To demonstrate the significance of the corollaries we first note that the parameter has no influence on the qualitative properties discussed in Corollary 2. In the following we analyse how each of the parameters and affects the fluctuation pattern of the asset price in the non-equilibrium time range . This analysis provides clear results – albeit not trivial – because of a particular feature of the determinant expression: changing the value of one of the parameters while keeping all other parameters fixed, the expression changes its sign exactly once. The borderline case is excluded from our consideration because obviously one cannot expect a real market to fit perfectly our model and have parameter values fitting exactly this equation.

Social susceptibility: Here we consider the dependence on the parameter which reflects the strength of the social susceptibility. Note that, by definition, is non-negative and that, from (8), the existence of positive implies . Hence the value range for to be considered here is . The consideration splits into two cases. The first case is . In this case, the inequality holds for all values of , and, according to Corollary 2, the price fluctuates indefinitely. In the opposite case, , we can find a critical value such that where while leads to . By the corollary, this implies that the price may bounce at most once when the social influence is weak, while it oscillates indefinitely when the social influence is strong.

This conclusion is not a totally novel discovery since it may be deduced by a simple argument which is well known from interacting agent models for asset markets (see [25]): the strong social influence causes the herding behaviour, which expresses itself in that an agent buys (resp., sells) when the majority buy [resp., sell], so that the price grows (resp., falls) beyond the fundamental value. When the asset price is much beyond the fundamental value the fundamentalist trading component makes the agents change their positions, which reverses the price trend. Interestingly, the exact analysis of our model suggests that a market asset price may be forced to oscillate by strengthening solely the social influence.

The main novelty of our conclusion is that it indicates that the price may bounce when the interaction between agents is low or even when it is totally absent. Another novel aspect is that under weak interactions the price can bounce no more than once, whereas under strong interactions it may oscillate. This alternative could hardly be explained by a heuristic argument on the basis of the herding effect.

Heterogeneity of agents: Here we consider the influence on the price pattern of the value of , the parameter that expresses the heterogeneity of the agents. Due to the constraint (8), the value range to be considered is . Clearly, for any and , there is a finite critical value within this range such that is negative if , and is positive if . By Corollary 2, this means that a low heterogeneity of agents may cause the price to oscillate many times, while under a high heterogeneity, the price can bounce only once. This effect agrees with a traditional explanation of how the heterogeneity influences the ups and downs of price. The essence of that explanation is the following. If the heterogeneity is low almost all agents have almost the same individual opinion with respect to the fundamental value. Suppose now that the asset price is not very high. Then almost all agents wish to buy if they obey their fundamentalist trading strategy. The social interaction makes these “wishes” even stronger. Thus a majority will be buying which makes the price grow. It will be growing until it becomes higher than the maximal evaluation of the fundamental value of the bulk of the population. At this moment, the situation is inverted and the predominant majority will be selling. Thus the fluctuations of the demand and price arise. This line of reasoning has been employed by various authors to justify a phenomenon that is phenomenologically similar to the effect described by our model, but concerns the long-time fluctuations of the price. However, this qualitative explanation could not distinguish whether the up-and-down would occur once or several times.

Market feedback: Here we discuss the influence of the parameter on the asset price function, again paying particular attention to whether this function can bounce once or more. To the best of our knowledge there is no analytically tractable HIAM for which this aspect of a market has been studied thoroughly.

We could argue as in the previous discussions and deduce that for any and , there is a critical value such that when the price can bounce at most once, while when the price can oscillate. However, we would like to concentrate our arguments on another conclusion that we found to be deeper, more important and striking: it is the presence of the linear feedback of the relative excess demand on the price increment that enables the price to behave in time in two different ways; either it is a damped -like function, or it is a function that may have at most one extremum. We note that we do not claim that only linear feedback is able to cause such a dichotomy. A complex time behaviour of the price function is a general consequence of the circular relation chain “pricedecisionsdemandprice”. Our conclusion concerns the “demandprice” link, saying that in this chain it is the main reason for the dichotonomy of the price time behaviour. One more factor in its favour will be given in the next subsection.

4.3 Case B: Systematic market overrating

We now consider the second scenario for where, on average, the traders assume that the fundamental value of the asset and the market price follow each other, but in their average opinion there may be some constant offset between the two quantities. We refer to overrating (corresponding to positive ) throughout even though may take negative values, with the obvious interpretation that negative overrating means underrating. Since under real circumstances a constant systematic overrating cannot be expected to be very “large” in any sense, we arrive at

-

Corollary 3. In the case of systematic market overrating, that is, for a constant for all , the condition

(25) ensures that the expected relative excess demand on the time interval is given by

(26) where .

From (7), combined with the assumption , we then obtain

| (27) |

where the limit relative excess demand

| (28) |

determines the limit growth rate of the asset price. Hence rephrasing Corollary 3 in terms of the asset price and analysing the number of extrema, we find

-

Corollary 4. If a systematic market overrating prevails, that is, if for a constant for all time, then the additional condition (25) ensures that and the asset price of the model behaves on as follows:

(29)

Before discussing the significance of the model parameters in this setting we remark that the unbounded growth (or decay) of the price is correct for the model, but not claimed to exist in a real market since the model assumption cannot remain true for a long period of time.

Market Feedback: To illustrate the significance of this second set of corollaries we first note that the feedback parameter has no influence on the qualitative properties discussed in Corollary 4. This demonstrates that if strategies on average assume fundamental value and market price to match (up to some constant bias), then the feedback between price and relative excess demand becomes irrelevant for the behaviour of the market. As a consequence, the asset price cannot exhibit more than one bounce. This observation strengthens our previous conclusion that this feedback is the main factor that determines whether the asset price can oscillate or not.

This might appear surprising at first sight, but it can be easily derived from the mathematical treatment of the model. If the average evaluation of the fundamental value follows the market price, the decision rule (5) of the agents takes the following form:

| (30) |

Observe that neither the asset price nor the average evaluation of the fundamental value of the asset appear in (30). The connection “pricedecisions” from the generic circular relation chain “pricedecisionsdemandprice” is manifestly broken. Mathematically this causes the absence of the asset price in the ODE (9) (for the link between the rule (5) and (9), see the proof of Proposition 1 in the appendix). Then this ODE takes the following form:

| (31) |

This is an ordinary differential equation of first order and it is easy to check that in the range of the allowed parameter values, its solution has at most one root, i.e., at most one for which . Thus, since is proportional to the derivative of the asset price function, the asset price cannot have more than one extremal point.

For the remaining model parameters we note that only the combinations and occur in (31) and thus we need not explicitly consider the dependence on .

Social susceptibility: We remind the reader that throughout our treatment the condition for mild herding behaviour is assumed. Corollary 3 tells us that the expected relative excess demand is a monotonic function in time, and that its limiting equilibrium value is (28). This means that in the equilibrium limit of our model, the proportion of those who buy exceeds the proportion of those who sell by . In our non-equilibrium setting, however, it is more interesting to ask how fast converges to its limit. The answer is in Corollary 3: the larger the social susceptibility relative to the heterogeneity , the slower is this convergence. This gives some insight into how the heterogeneity and the social influence compete in a market.

Market overrating: The sign of determines whether in the long run the price will be growing or falling; asymptotically . Since therefore can become negative, it may be useful to remind the reader that really means the logarithm of the price, and that the asymptotic linear behaviour corresponds to exponential growth or loss of the value of the asset with rate . Note that this does not depend on the initial relative excess demand . However, the initial distribution does play a role for the short-time non-equilibrium behaviour, since to first order in time . The dichotomy (29) of Corollary 4 agrees with the general understanding of how the fundamentalist trading effect might affect the dynamics of the price. Indeed, determines whether the majority “mood” is to buy or to sell if the social interaction is absent. The social interaction by itself makes an agent agree with the majority’s mood. In our model, the initial majority mood is given by . Thus, if then our heuristics suggests that the majority mood must be same all the time. In fact, if , then , i.e., the price is less than the average evaluation of the fundamental value, accordingly, the majority is inclined to buy, that is, . On the contrary, if , then the price is higher than the average evaluation of the fundamental value, so that the majority is inclined to sell, that is, . This suggestion is confirmed by the corollary.

The opposite case, where , is more tricky in the sense that it is difficult to predict from a purely heuristical argument whether the initial mood will pertain for ever or whether it will be reversed. Our model suggests that fundamentalist thinking will eventually win over any initial mood, even if the herding effect (which slows down the relaxation to the asymptotic behaviour) tends to preserve the initial mood for some time. The time of mood reversal (i.e., when reaches again ) grows with increasing social susceptibility.

4.4 Computer simulation tests

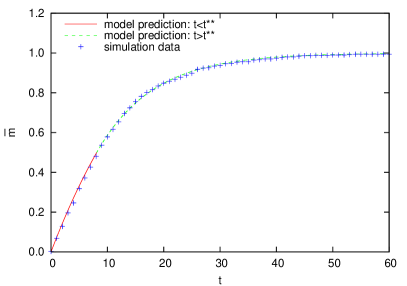

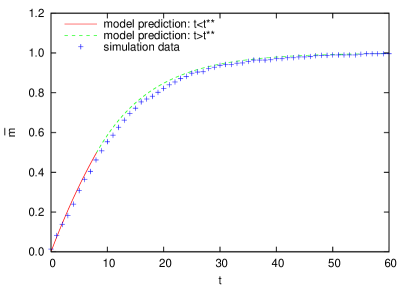

To complement the preceding theoretical analysis, we here present the results of Monte Carlo simulations using random sequential update as discretization of the continuous-time process. We first discuss results corresponding to the case with fixed fundamental value (model (A)) before treating the systematic market rating case (model (B)). In both cases we choose some specimen parameter values and compare the observed behaviour of the relative excess demand to that described by the solution of the ODE (9). As demonstrated above, this solution is exact only in the time interval given by (16). However, for a large ensemble of strongly-connected traders we expect it also to be a good approximation outside this regime. To test this assumption we deliberately choose the worst-case scenario with parameter values so that . We consider fully-connected networks and undirected random networks with a constant small connectivity which is the number of peers of each agent.

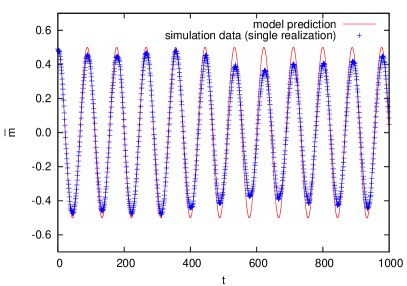

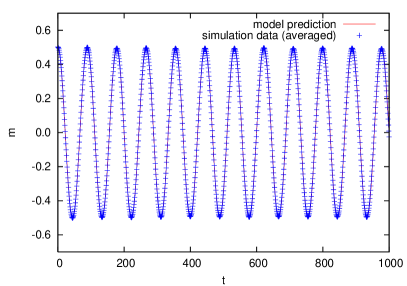

For model (A) we concentrate on the case of strong feedback and strong social susceptibility at the point, , for which the treatment of section 4.2 predicts undamped oscillations of the excess demand. We note that periodic oscillations were previously seen in simulations of a different model combining price adjustment and interactions between heterogeneous agents [33].

Figure 1(a) shows results for a single history on a large fully-connected network of agents. We see immediately that even a single history is well described by the ODE (9) with, for large system sizes, only a slight fluctuation in the amplitude of the oscillations. The average over histories shown in Fig. 1(b) is essentially indistinguishable from the theoretical prediction of (20) with .

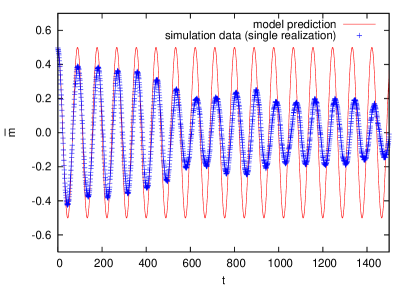

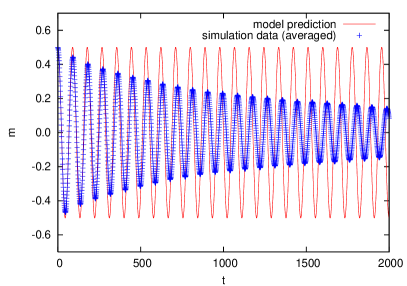

The situation for networks with lower connectivity is more subtle, as demonstrated in Fig. 2 for an undirected random network with connectivity small relative to the system size. Oscillations are still clearly seen but the frequency is slightly lower than predicted and there is an initial decay before fluctuation about some lower amplitude. (For the averaged case the amplitude decreases still further due to fluctuations in the frequency for each history.) We believe this effect is a result of the build-up of correlations—a hypothesis which is supported by observations that the discrepancy from prediction is larger for a nearest-neighbour network (with the same connectivity) but smaller for a directed network. Real trader networks would be expected to have small-world or scale-free properties but to show qualitatively the same behaviour. A more detailed account of the dynamics of our model on such networks will be published elsewhere.

We have also simulated the overdamped case (i.e., ). Here again, results for a fully-connected network show excellent quantitative agreement with the theoretical prediction (20) but there is a slight discrepancy for less-connected networks. However, in this case there appears to be less dependence on the network structure for given connectivity.

Let us now turn to the systematic market rating case of model (B). As argued at the start of section 4.3, if the condition is obeyed then . On the other hand, if this condition is not fulfilled, it is straightforward to show that . In this case the following heuristic picture emerges for a strongly connected network where the average number of trusted friends of each trader is of the order of the network size . Since we expect , up to fluctuations of order , we argue that the solution (26) should be approximately valid until some time determined by the condition . From then on all traders opt to buy (if ) or sell (if ). Consequently the system continues to evolve according to

| (32) |

with unit relaxation time which is just the intrinsic decision timescale of the continuous-time dynamics. In other words, after the crossover time the system begins quickly to freeze in the non-fluctuating equilibrium state, i.e., the uniquely-given frozen state with .

Figure 3

shows results of simulations for model (B) with (small social heterogeneity, large market under rating) on two different networks. As predicted we find that the relative excess demand evolves towards an equilibrium value of . In fact, the evolution of for a single history of the process is very well described by the predictions of Eqs. (26) and (32) for the expectation . The agreement is excellent in the fully-connected case but still good when the connectivity is low compared to the system size. As expected, fluctuations were found to be larger for smaller system sizes, these fluctuations can be smoothed out by averaging over a number of histories.

4.5 Peer network

A perhaps surprising result is the equality of the expectation of decision for all agents for any network provided that the initial distribution was network mean homogeneous. We point out that for a fully connected network this is less surprising. To see this, imagine a discrete-time version of the model where all agents are updated simultaneously in one time-step following the decision rule of our model. Then, in order to initiate our model, that is, in order to be able to construct the opinion distribution over the population at time , it is sufficient to give – the relative populational excess demand at time . Then, in accordance with our model definition, the measure on will be network mean homogeneous. Consequently, the measure that rules for any will also be network mean homogeneous.

In other words, in the fully connected mean-field case of our model, the distribution of the agent opinions is network mean homogeneous, when the model is initiated as described above. The opposite case for initiating the model is to give the distribution of . This distribution may have non-homogeneous mean. But since each agent is influenced by other agents solely through the relative populational demand, then the measure on will already have network homogeneous mean after one time step. Therefore, for fully connected networks only network mean homogeneous measures are of interest.

For a fully connected network we can also explain the numerical observation that for a large population a single realization of the process essentially coincides with the analytically computed mean. One may invoke the law of large numbers for the peer excess demand to argue that the social interaction becomes deterministic. Then the stochastic dynamics is solely driven by the uncorrelated annealed randomness of the individual evaluation of the fundamental value and, from ergodicity arguments, one expects individual histories to follow the analytical result for the expectation.

A greater surprise then is the observation that individual realizations of the process capture the main features of the average over histories even for random networks with small connectivity. For small connectivity the first step (large numbers for the peer excess demand) of the previous reasoning fails and it remains unclear why also histories on graphs with small and heterogeneous connectivity are reasonably well described by the analytical results. We rationalize this observation by closer inspection of the two-fold origin of external randomness in the model, viz. (i) the quenched random graph structure representing the (highly heterogeneous) peer groups of each agent, and (ii) the annealed randomness of the individual evaluation of the fundamental value. We note that in each individual decision the randomness coming from the graph structure adds to the randomness of the individual evaluation of the fundamental value an amount of at most the same order (since ) and hence does not qualitatively change the strength of the total external noise that drives the stochasticity of the model. Making the natural assumption that the uncorrelated annealed noise of the individual evaluation of the fundamental value dominates over the quenched noise then explains why the “mean-field” model of a fully connected network approximates quite well a weakly-connected quenched random network.

We stress that our observations should not be interpreted as suggesting that network topology would generally not matter for anything of interest in the dynamics of general HIAMs. Many studies of the Ising model on a variety of networks have revealed interesting network phenomena, for example, for recent work on Barabási-Albert networks see [31, 24] and more generally on phase transitions and critical behaviour in networks, see e.g. [27, 1, 21, 12]. Very recent mean-field and numerical work on a HIAM which is constructed in a spirit similar to ours (similar in general terms, but quite different in its details) has shown that its equilibrium finite-size effects depend strongly on the topology of the underlying network [2]. It would be very interesting to see whether the presence of phase transitions and strong finite-size effects in the equilibrium distribution is reflected in the short-time dynamics of stochastic models with these equilibrium properties.

5 Some further issues

In summary, we have presented a heterogeneous interacting-agent model for the short-time non-equilibrium dynamics of an asset price. This model is analytically tractable and thus provides detailed insight into the interplay of individual fundamentalist heterogeneity and social interaction leading to herding behaviour for a variety of scenarios of the relation between market price and average evaluation of the fundamental value of the asset. Quite independently of the underlying structure of the peer network, interesting collective behaviour emerges, including oscillations, a single bounce, or monotonic evolution of the price. These features can be traced back to the relative strength of the factors that determine the time evolution of the HIAM, as discussed in detail in Sec. 4.

An open question with respect to the random graph structure of the peer network is the robustness of the assumption of domination of the collective stochastic dynamics by annealed noise that explains why our results have a fair degree of independence of the topology of the peer groups. There is indeed much further scope for simulation studies looking at different aspects of our model on more complex networks. The present results for simple topologies confirm the relevance of our analytical approach and provide a starting point for future work probing systematically various classes of network topologies for correlations, inhomogeneous initial distributions, and finite-size effects in these quantities. One may even attempt to study its stationary distribution for gaining insight in the relation between stationary and early-time dynamical properties.

An anonymous referee pointed out that while our manuscript was under review for publication, there appeared work of Horst and Rothe [16] that seems to be closely related to ours. Indeed, our Proposition 1 and Corollaries 1 – 4 appear to be very similar to conclusions of Horst and Rothe that may be summarized as follows: The trajectories of the price in the model of Horst and Rothe from [16] converge to a solution of a differential equation (Theorem 2.5 from [16]) and, depending on choice of parameters of the model, this solution looks like that of the damped harmonic oscillator, or oscillates almost chaotically, or “bounces” once and then converges exponentially fast to a constant (the examples of Section 3 from [16]).

Let us point out the differences between our work and that of Horst and Rothe. The first is that in our model, the agents can have different peer groups while in the model of Horst and Rothe “… all other individuals influence one particular trader in the same way” (the citation from Remark 2.2 of [16]). Second, the feedback of excess demand on the price increment is a free parameter in our model while it is a constant (equal to ) in [16]. This may be not a principal difference since one can normalize all the free parameters by the feedback value, but such a normalization would make impossible the analysis that we make in Sections 4.2 and 4.3 concerning how this feedback affects the evolution pattern of asset price. Next, in Horst and Rothe’s model, agents can have different strategies that depend on the states of process in the past. This structure is much richer than that of our model since where an agent decides whether her order is to sell or to buy on the basis of the state of the process at the moment of decision. Certainly, a dependence structure as general as that of Horst and Rothe requires the imposition of constraints so as to allow for analytical treatment of the model. Horst and Rothe impose that all the order fluxes as well as the moments at which agents change their strategies are determined by Poisson point processes. In particular, every agent “carries with herself” two independent Poisson point processes, one of which determines the instances of the sell orders and the other one the instances of the buy orders. The rates of the processes change in time, but the processes are independent by the construction. This is different from our model: if we re-write the decision rule (described in Section 2) in a form similar to that of Horst and Rothe then the resulting Poisson point processes will be dependent through the dependence of their rates. One more difference lies in the definition of how the price dynamics depends on the excess demand. In Ref. [16], the price raises [resp., diminishes] when a buy [resp., sell] order is put. In our model, if an agent puts an order after she has put an order of the same type, the excess demand does not change and thus, the price continues to grow or decay at the same rate as it has been growing or decaying.

It is worth mentioning that Horst and Rothe consider the law of the deviation of the stochastic trajectories from their limit (given by the solution to a deterministic differential equation); this issue is not addressed by us here. In summary, our model and that of Horst and Rothe are different, the result of neither of the two works follow from the results of the other one, and the methods used in the proofs are different. The similarity of results then suggests that they reveal a quite general phenomenon, but we do not possess tools and results that would allow us to discuss this suggestion in mathematical detail.

Acknowledgments

This work was initiated through and supported by an DAAD/CAPES exchange grant (GMS and FP). We also acknowledge support by FAPESP (FP) and CNPq and FAPESP (VB). We thank M. Hohnisch, T. Lux and D. Stauffer for useful comments on a preliminary version of the manuscript.

Appendix A Proofs

In this appendix we provide the details of two key proofs. Specifically, in Section A.1 we prove Proposition 1 and in Section A.2 we prove Corollary 2. With respect to our other assertions, note that the proof of Corollary 1 is outlined in Section 4.2 of the main text; Corollary 3 follows by a similar argument and Corollary 4 is a direct consequence of Corollary 3.

A.1 Proof of Proposition 1

The statement of Proposition 1 can be found in section 3. Here we shall deduce this result from a general property of continuous-time Markov processes. In our case, the Markov process is and its state space is denoted by . The finite-dimensional counterpart of the Hille-Yosida theorem (see [22], Chapter I) then states that for a continuous and bounded function

| (33) |

where is the infinitesimal generator of the process whose application to functions of interest to us may be constructed as follows.

Let us fix arbitrarily a node from , and let be the function that attributes the value of at to any triple :

| (34) |

We now choose arbitrarily and let it be the initial state of our process. Since the times of the updates of the position of any agent form a Poisson point process with rate , and since the Poisson point processes related to different agents are independent, then the following is true: during a short time interval , the probability that the model’s agent decides once to update her position is , the probability that she does not decide to update her position is , and the probability of all other events is . Let us consider the event when a single update decision is taken during . Let denote the decision time (). Then, in accordance with the construction of our model, the sign of determines the resulting position. Thus, since is the distribution function of the random variable

| (35) |

Unfortunately, we have no control on the exact position of . This causes a difficulty in the use of (35) for the derivation of . Nevertheless, the latter may be estimated with sufficient precision using the following facts which are true by construction/definition: (i) conditioned on the occurrence of the considered update event, the probability that any other agent has changed its position by time is ; (ii) each trajectory of is a continuous function; (iii) each trajectory of is a continuous function; (iv) , the distribution function of , is a continuous function; (v) is a continuous and bounded function. Then, using the shorthand , we have

| (36) |

and consequently

| (37) |

Now let be an arbitrary real number from the interval . The definition (8) of ensures that . This inequality and the obvious bound together imply that

| (38) |

By the assumption (i) of Proposition 1, when . This fact combined with (38) allows us to write the generator

| (39) | |||||

for and for from (34). Combining (39) with (33), we finally get

| (40) |

Since was an arbitrary site of , then the equation (40) holds for every . Hence we have a system of differential equations with the initial condition , (recall that, by assumption (ii) of the proposition, the distribution of has network homogeneous measure so that does not depend on ). It is straightforward to check that one of the solutions of the system of equations with this initial condition is

| (41) |

where is the solution of

| (42) |

However, then (41) is the only solution, in accordance with the theory of ODEs. Finally, (41) and the definition of imply that and (42) acquires the form of (9). This completes the proof of Proposition 1.

A.2 Proof of Corollary 2

To prove Corollary 2 of section 4.2 we shall need the auxiliary result of Proposition 2 as stated below. In the formulation, we use the shorthand notation established in (17) and to simplify notation below we also introduce

| (43) |

Proposition 2.

Let , , , , , and be arbitrary real numbers. Let the function , be the solution of the ODE

| (44) |

with the following initial conditions

| (45) |

Define

| (46) |

and

| (47) |

With these definitions the proposition consists of two cases.

(a) If the parameter values satisfy the inequality

then the extremum points of on the interval222We consider

and not because we are not

interested in the function’s extrema at the interval’s boundary.

obey the following rule.

If

| (48) | |||

| (49) | |||

| (50) | |||

| (51) |

are all satisfied, then and has a unique extremum point on the interval ; the abscissa of this point is of (43). If, on the contrary, at least one of the conditions (49)–(51) fails then either , or but has no extrema on . In particular, for any parameter values, the inequality is sufficient for .

(b) If the parameter values satisfy the inequality then

| (52) |

If then . Otherwise, the extremum points of on are the positive solutions of the equation

| (53) |

and the number of the extremum points of on the interval obeys the following rule. Let denote the non-negative solutions of the equation (53). If the inequalities

| (54) | |||

| (55) | |||

| (56) |

are all valid then (and consequently, all the non-null ’s belong to ). If (54) and (55) are valid but (56) is invalid, then is finite and may be null; in this case, ensures that and that is the abscissa of the unique extremum point of on . If (54) is valid and both (55) and (56) are invalid then is finite but may be null, and has no extrema on . If (54) is invalid, then . Again, for any parameter values, the inequality is sufficient for .

How Corollary 2 follows from Proposition 2. Recall that Corollary 2 concerns the behaviour of the model if the assumptions of Proposition 1 are satisfied, when the average fundamental value evaluation is fixed (i.e., the condition (11) is satisfied), and when the initial value coincides with (all the expectations are equal because of the proposition’s assumption about the initial distribution of the model). Under these conditions, the definition (8) of and the definition (9-10) of , both from Proposition 1, acquire the forms of (47) and (44-45) respectively from Proposition 2. Thus – by the arguments of Section (4.1) – , the price function considered in Corollary 2, coincides on the interval with the function defined and studied in Proposition 2. Consequently,

-

(I) The first of the three “if” cases of Corollary 2 follows from Proposition 2(a), if we show that

The assertion (I-ii) follows straightforwardly and we now demonstrate (I-i). Let be such that . We take any . Then, the condition (49) is automatically satisfied, and the condition (51) is satisfied because . Next, we take any . Then, the condition (48) is satisfied. Moreover, for any pair of chosen values of and , the condition (50) is satisfied because . This proves (I-i).

Let us now prove (II-i). The proof builds upon the following identity:

| (58) |

where and . Obviously, for a non-empty set of parameter values, the inequality (54) and the inequality may be satisfied simultaneously. However, since , then the validity of the latter inequality ensures that (55) and (56) hold true independently of the actual values of and . This proves (II-i).

Hence we have shown how Corollary 2 follows from Proposition 2.333 The middle “if” case of Corollary 2 can be treated in a similar manner, but since it is of no interest for the purpose of this work we omit the proof. The rest of the appendix is devoted to proving Proposition 2 itself. We will do this in two parts.

Proof of Proposition 2(a). The definition (47) of and the fact that is continuous ensure that when . This proves the last statement of item (a). The same definition of ensures that when . So, from now on, we assume the contrary, i.e., that (48) holds.

We recall from Corollary 1 that the validity of the inequality implies that , the function that solves (44)–(45), is given by (18). Assume first that . It then follows from (18) that either (when ), or the equation has a unique solution which is . Since , then in both cases, is a monotonic function on , and thus, it is necessarily so on whatever may be.

For the remainder of the proof of item (a), we consider the case where . It then follows from (18) and from the inequalities , , (all of which hold true because the values of satisfy the proposition’s assumption and the inequality ) that the equation has a unique solution on if and only if

| (59) |

This inequality is trivially equivalent to (50). Thus, we have proved that if (50) fails then is a monotonic function on , and must be so on whatever may be.

From now on we assume that (50) (or, equivalently, (59)) holds. This assumption ensures that has a unique extremum point on whose abscissa is the positive solution of . We denote this solution by ; from (18), it follows readily that satisfies (43).

Let us now prove that the validity of (51) ensures that , i.e., that the unique extremum of on actually belongs to . (Note that, by proving , we also ensure that since .) First of all, we observe that is the abscissa of the unique extremum point of the function (because the derivative of this function is ). This observation, the fact that is a continuous function, and the inequality together imply (via the definition of ) that

| (60) |

To complete the proof of item (a), we thus have to show that the inequality in the right hand side of the implication (60) is equivalent to (51). We now proceed with the argument establishing this equivalence. From the expression (18) for the function we obtain that

| (61) |

The right hand side of (61) may be significantly simplified since

where in the last but one step we used that . Thus,

| (62) | |||||

Here we have also used the identity

| (63) |

which follows from simple algebraic calculation. The equality (62) shows that the inequality (51) is equivalent to the inequality in the right hand side of the implication (60). The proof of (a) is thus completed.

Proof of Proposition 2(b). The definition (47) of and the fact that is continuous ensure that when . This proves the last statement of item (b). The same definition of ensures that when . So, from now on, we assume the contrary, i.e., that (54) holds.

We recall from Corollary 1 that the validity of the inequality implies that , the function that solves (44)–(45), is given by (20). It then follows by integration that

| (64) |

Here we have used the identities

| (65) |

and

| (66) |

which are straightforwardly checked (recall ). From (64) and the definition (46) of we deduce the expression (52) for . From this expression, , when . Thus, for the rest of the proof, we assume that at least one of and is non-zero.

Since the equation acquires the form of (53) and since then the solutions of (53) are the abscissa of the extremum points of . This proves the second assertion of item (b).

By definition is the set of the abscissa of the extremum points of the function on . We now turn to the question of which of the ’s lie in the interval . Assume for the present that ; the case will be considered later. Using this assumption, together with the definition of , the fact that is continuous, and the inequality (as assumed above), we find that

| (67) | |||||

| (68) |

Let us now assume that (55) holds but (56) does not hold. From (64) this implies that and , or, in other words, that (67) holds for . Since (67)(68), we then conclude that . Since then is the unique point in at which attains an extremum.

Let us now prove that the validity of (54), (55) and (56) ensures that . For this, we re-write (20) so that acquires the following form

| (69) |

Here and , although these expressions are nowhere needed in our proof. The form of (69) shows that is damped by with . Combining this fact with the fact that the ’s are the non-negative solutions of the equation we get that the numbers

| (70) |

decrease in absolute value (i.e., ) and form a sign-alternating sequence (i.e., ). Now note that (55) and (56) state

| (71) |

These inequalities and the properties of the sequence (70) imply that

| (72) |

or, in other words, that for . Thus, , but since then .

It only remains to consider the case in which (55) reduces to (54). We recall that our proof is already working under the assumption that (54) holds true. Hence there are only two sub-cases to be analysed: when (56) is valid and when it is invalid. In the first sub-case, we argue as in the above paragraph and deduce that . This argument works here because the sequence is still decreasing and sign-alternating. Actually, the only modification necessary for the argument to work here is the substitution of by . Consider now the second sub-case, i.e, assume (56) is invalid. Arguing as for the implication (67)(68), we get that in this sub-case. Note that this double inequality does not exclude the possibility . It will indeed occur, if (or, ) and is positive (resp., negative) in the neighbourhood of . Otherwise, . However, since then has no extremum points on , when .

This completes our proof of Proposition 2 and therefore also Corollary 2.

References

- [1] Aleksiejuk, A., Hołyst, J.A. and Stauffer, D., Ferromagnetic phase transition in Barabási-Albert networks. Physica A, 2002, 310, 260–266.

- [2] Alfarano, S. and Milakovic M., The network structure and -dependence in agent-based herding models? J. Econ. Dyn. Control, 2009, 33, 78–92.

- [3] Beja, A. and Goldman, M.B., On the Dynamic behaviour of Prices in Disequilibrium. J. Finance, 1980, 35, 235–248.

- [4] Bikhchandani, S., Hirshleifer, D. and Welch, I., A Theory of Fads, Fashion, Custom, and Cultural Change as Informational Cascades. J. Polit. Econ., 1992, 100, 992–1026.

- [5] Brock, W.A., Understanding macroeconomic time series using complex systems theory. Structural Change and Economic Dynamics, 1991, 2, 119–141.

- [6] Challet, D., Marsili, M. and Zhang, Y-C., From Minority Games to real markets. Quant. Finance, 2001, 1, 168–176.

- [7] Cont, R. and Bouchaud J.-P., Herd behavior and aggregate fluctuations in financial markets. Macroecon. Dyn., 2000, 4, 170–196.