Approximating Perpetuities

Abstract

We propose and analyze an algorithm to approximate distribution functions and densities of perpetuities. Our algorithm refines an earlier approach based on iterating discretized versions of the fixed point equation that defines the perpetuity. We significantly reduce the complexity of the earlier algorithm. Also one particular perpetuity arising in the analysis of the selection algorithm Quickselect is studied in more detail. Our approach works well for distribution functions. For densities we have weaker error bounds although computer experiments indicate that densities can also be approximated well.

Keywords: perpetuity, theory of distributions, approximation of probability densities, perfect simulation

1 Introduction

A perpetuity is a random variable in that satisfies the stochastic fixed-point equation

| (1) |

where the symbol denotes that left and right hand side in (1) are identically distributed and where is a vector of random variables being independent of , whereas dependence between and is allowed.

Perpetuities arise in various different contexts: In discrete mathematics, perpetuities come up as the limit distributions of certain count statistics of decomposable combinatorial structures such as random permutations or random integers. In these areas, perpetuities often arise via relationships to the GEM and Poisson-Dirichlet distributions; see Arratia, Barbour, and Tavaré (2003) for perpetuities, GEM and Poisson-Dirichlet distribution in the context of combinatorial structures; see Donnelly and Grimmett (1993) for occurrences in probabilistic number theory. In the probabilistic analysis of algorithms, perpetuities arise as limit distributions of certain cost measures of recursive algorithms such as the selection algorithm Quickselect, see e.g. Hwang and Tsai (2002) or Mahmoud, Modarres, and Smythe (1995). In insurance and financial mathematics, a perpetuity represents the value of a commitment to make regular payments, where represents the payment and a discount factor both being subject to random fluctuation; see, e.g. Goldie and Maller (2000) or Embrechts, Klüppelberg, and Mikosch (1997, Section 8.4).

As perpetuities are given implicitly by their fixed-point characterization (1), properties of their distributions are not directly amenable. Nevertheless, various questions about perpetuities have already been settled. Necessary and sufficient conditions on for the fixed-point equation (1) to uniquely determine a probability distribution are discussed in Vervaat (1979) and Goldie and Maller (2000). The types of distributions possible for perpetuities have been identified in Alsmeyer, Iksanov, and Rösler (2007). Tail behavior of perpetuities has been studied for certain cases in Goldie and Grübel (1996).

In the present article, we are interested in the central region of the distributions. The aim is to algorithmically approximate perpetuities, in particular their distribution functions and their Lebesgue densities (if they exist).

For this, we apply and refine a method proposed in Devroye and Neininger (2002) that was originally designed for random variables satisfying distributional fixed-point equations of the form

| (2) |

where are independent with being identically distributed as for and random coefficients , , and .

The case of perpetuities, i.e., , structurally differs from the cases : The presence of more than one independent copy of on the right hand side in (2) often has a smoothing effect so that under mild additional assumptions on the existence of smooth Lebesgue densities of follows, see Fill and Janson (2000) and Devroye and Neininger (2002). On the other hand, the case often leads to distributions that have no smooth Lebesgue density; an example is discussed in Section 5.

Our basic approach to approximate perpetuities is as follows: A random variable satisfies the distributional identity (1) if and only if its distribution is a fixed-point of the map on the space of probability distributions, given by

| (3) |

where is independent of , and . Under the conditions and for some , which we assume throughout the paper, this map is a contraction on certain complete metric subspaces of . Hence, can be obtained as limit of iterations of , starting with some distribution .

However, it is not generally possible to algorithmically compute the iterations of exactly. We therefore use discrete approximations of , which become more accurate for increasing , to approximate by a mapping , defined by

where again is independent of and .

To allow for an efficient computation of the approximation, we impose a further discretisation step , introduced in Section 2, defining

where is independent of and .

In Section 2, we give conditions for to converge to the perpetuity given as the solution of (1). To this aim, we derive a rate of convergence in the minimal metric , defined on the space of probability measures on with finite absolute th moment by

| (4) |

where denotes the -norm of random variables. To get an explicit error bound for the distribution function, we then convert this into a rate of convergence in the Kolmogorov metric , defined by

where denote the distribution functions of . This implies explicit rates of convergence for distribution function and density, depending on the corresponding moduli of continuity of the fixed-point.

For these moduli of continuity we find global bounds for perpetuities with in Section 4. For cases with random , we have to derive these moduli of continuity individually. One example, connected to the selection algorithm Quickselect, is worked out in detail in Section 5.

We analyze the complexity of our approach in Section 3. As a measure for the complexity of the approximations for distribution function and density, we use the number of steps needed to obtain an approximation that has distance, in supremum norm, of at most to the true function. Although we generally follow the approach in Devroye and Neininger (2002), we can improve the complexity significantly by using different discretisations. For the approximation of the distribution function to an accuracy of in a typical case, we obtain a complexity of for any . In comparison, the algorithm described in Devroye and Neininger (2002), which originally was designed for fixed-point equations of type (2) with , would lead to a complexity of , if applied to our cases. For the approximation of the density to an accuracy of , we obtain a complexity of for any in the case of -Hölder continuous densities, cf. Corollary 3.2.

An extended abstract of this article appeared in Knape and Neininger (2007+).

2 Discrete approximation and convergence

Recall that our basic assumption in equation (1) is that and for some . To obtain an algorithmically computable approximation of the solution of the fixed-point equation (1), we use an approximation of the sequence defined as follows: We replace by a sequence of independent discrete approximations , converging to in th mean for . To reduce the complexity, we introduce a further discretisation step , which reduces the number of values attained by :

| (5) |

We assume that the discretisations , and satisfy

| (6) |

for some error functions , and , which we specify later.

Furthermore, we assume that there exists some , such that for all ,

| (7) |

which in applications is easy to obtain, since .

By arguments similar to those used in Fill and Janson (2002) and Devroye and Neininger (2002) we obtain the following convergence rates for the approximations to converge to the corresponding characteristics of the fixed-point . We use the shorthand notation .

Lemma 2.1.

Proof.

We have

| (9) |

The first summand is bounded by (6) and for the second summand we have

where in the last step we use that and as well as and are independent by assumption.

To make these estimates explicit we have to specify bounds for , , and . We do so in two different ways, one representing a polynomial discretisation of the corresponding random variables and one representing an exponential discretisation. Better asymptotic results are obtained by the latter one.

Corollary 2.2.

Proof.

To see that the second summand is of order , note that for all and . This implies that for ,

where the last equality is obtained by differentiating the geometric series times. ∎

Remark 2.3.

Corollary 2.4.

Proof.

Using Lemma 2.1 we get

| (13) |

and the assumption on implies that both summands are with the constant given in the lemma. ∎

Lemma 2.5.

Remark 2.6.

In some cases, we can give a similar bound, although the density of is not bounded or no explicit bound is known. Instead, it is sufficient to have a bound for the modulus of continuity of the distribution function of , cf. Knape (2006).

To approximate the density of the fixed-point, we define

| (16) |

where is the distribution function of . For this approximation we can give a rate of convergence, depending on the modulus of continuity of the density of the fixed-point, which is defined by

Lemma 2.7.

Proof.

For any , we have

The assertion follows since is monotonically increasing. ∎

Corollary 2.8.

Remark 2.9.

If is bounded and bounds for the density and its modulus of continuity are known explicitly, the last result is strong enough to construct a perfect simulation algorithm based on von Neumann’s rejection method. Corollary 2.8 can be turned into such an algorithm as done in Devroye (2001) for the case of infinitely divisible perpetuities with approximation of densities by Fourier inversion, Devroye, Fill, and Neininger (2000) for the case of the Quicksort limit distribution and Devroye and Neininger (2002) for more general fixed-point equations of type (2).

3 Algorithm and Complexity

In this section, we will give an algorithm for an approximation satisfying the assumptions in the last section for many important cases. We assume that the distributions of and are given by Skorohod representations, i.e. by measurable functions , such that

| (17) |

being uniformly distributed on . Furthermore, we assume that and that both functions are Lipschitz continuous and can be evaluated in constant time. Now we define the discretisation by

| (18) |

where can be either polynomial, i.e. or exponential, . Defining

the conditions on and ensure that Corollary 2.2 and 2.4 can be applied.

We keep the distribution of in an array , where

for . Note however, that as and are bounded, at least for , where can be computed recursively as and .

For simplicity we assume that and that for all . The core of the implementation is the following update procedure:

Furthermore, we use a procedure , which creates as vector with components with for .

The whole algorithm then looks like this:

| (19) |

The complete code for polynomial discretisation for the example in Section 5, implemented in C++, can be found in Knape (2006).

To approximate the density as in (16) with for some , we compute a new array by setting

To measure the complexity of our algorithm, we estimate the number of steps needed to approximate the distribution function and the density up to an accuracy of . For the case that has a bounded density which is Hölder continuous, we give asymptotic bounds for polynomial as well as for exponential discretisation. We assume the general condition (17).

Lemma 3.1.

Assume that has a bounded density , which is Hölder continuous with exponent . Using polynomial discretisation with exponent , cf. Corollary 2.2, we can calculate for any approximations of the distribution function and the density of with

in time and respectively with

Using exponential discretisation with parameter as in Corollary 2.4, approximation to the same accuracy takes time

for the distribution function and the density of respectively.

Proof.

In one execution of update(), the outer loop is executed times. The assumptions on and ensure that , so we have runs of the inner loop and the whole procedure takes time . Hence, for any , finding costs time

| (20) |

Corollary 3.2.

Assume (17) and that has a bounded density , which is Hölder continuous with exponent . Then, using exponential discretisation as in Corollary 2.4, approximation to an accuracy of takes time for the distribution function and time for the density of for all .

Proof.

Note that and for some implies that for all . Thus, in Lemma 3.1, can be chosen arbitrarily large. ∎

4 A simple class of perpetuities

In order to make the bounds of Section 2 explicit in applications, we need to bound the absolute value and modulus of continuity of the density of the fixed-point. For a simple class of fixed-point equations, we give universal bounds in this section. For more complicated cases, bounds have to be derived individually, which we work out for one example in Section 5.

For fixed-point equations of the form

| (21) |

where and are independent, we can bound the density and modulus of continuity of using the corresponding values of .

Lemma 4.1.

Let satisfy fixed-point equation (21) and have a density . Then has a density satisfying

| (22) |

and otherwise.

Proof.

From the fixed-point equation we can see that almost surely. Now let be the distribution of . Conditioning on , we get for any Borel set :

where we can use Fubini’s theorem in the last step, because the integrand is product measurable. The claim follows, as this is just the definition of a Lebesgue density. ∎

Corollary 4.2.

Let have a bounded density . Then has a density satisfying

Proof.

Corollary 4.3.

Let have a density , and be its modulus of continuity. Then the modulus of continuity of satisfies

This result is only useful if the density of is continuous, but we can extend it to many practical examples, where has jumps at points in a set . We use the jump function of , defined by

and a modification of where we remove all jumps,

Since , we now denote by the modulus of continuity of the restriction of to .

Lemma 4.4.

Let have a bounded càdlàg density . Then, for all ,

Proof.

We give the proof for the case that has only one jump, say in . The general case then follows similarly. For , we have

We define

and divide the range of integration into the three intervals and . Now, in the first and third interval, differences of values of and coincide. Moreover, for we have

Putting everything together we obtain

We now bound the latter integral by as in Corollary 4.3, and the claim follows by taking the supremum over all . ∎

5 Example: Number of key exchanges in Quickselect

In this section, we apply our algorithm to the fixed-point equation

| (24) |

where and are independent and is uniformly distributed on . This equation appears in the analysis of the selection algorithm Quickselect. The asymptotic distribution of the number of key exchanges executed by Quickselect when acting on a random equiprobable permutation of length and selecting an element of rank can be characterized by the above fixed-point equation, see Hwang and Tsai (2002).

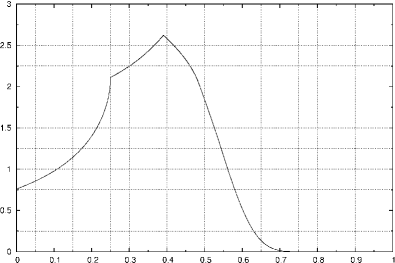

We use our algorithm to get a discrete approximation of the fixed point. The plot of a histogram, generated with iterations of the algorithms using for the discretisation , can be found in Figure 1.

In the following, we specify how the bounds in Section 2 can be made explicit for this example.

Lemma 5.1.

Let be a solution of (24). Then, we have almost surely, and the moments are recursively given by and

in particular, .

Proof.

Both claims follow directly from the fixed-point equation in (24), using that the solution is unique. To compute the moments, note that is equal to the Beta function , so we have

and the assertion follows. ∎

Lemma 5.2.

Let be a solution of (24). Then, for all and ,

Proof.

Using that is supported by , it is easy to show that for all ,

and this inequality can be translated into

| (25) |

Lemma 5.3.

Proof.

Let be the distribution of . Then we get for any Borel set by conditioning on as in the proof of Lemma 4.1,

where is a Lebesgue density of . The last step is valid by Fubini’s theorem as is product measurable, cf. (28).

Hence, has a Lebesgue-density satisfying

| (27) |

To find , we observe that and get

To get a density, we differentiate with respect to and rewrite as a function of yielding

| (28) |

Plugging this into (27) we get the stated integral equation. ∎

Remark 5.4.

The integral of with respect to can explicitly be evaluated:

| (29) |

Remark 5.5.

We will see in Lemma 5.7 that has a version that is continuous on . For this version we have

In order to use Lemma 2.5 to bound the deviation of our approximation, we need an explicit bound for the density of . We derive a rather rough bound here and see later, that we can use the resulting bound from our approximation to improve it.

Lemma 5.6.

Let be the density of as in Lemma 5.3. Then

Proof.

To get an explicit bound for we simplify the integral equation and obtain

| (30) |

We know for , and we can bound , if is bounded away from . Hence we split the integral into a left part for which we already have a bound for and a right part, in which we can bound . For any , we have

| (31) |

where in the second integral, we can use that is decreasing in for any fixed and bound .

For , we can use that is negative, and set . So the first integral vanishes and only the second remains and we obtain

| (32) |

We can calculate the first integral using the integral of given in (29),

| (33) |

and for the second integral, we obtain

Putting everything together we get

| (34) |

For we have , and by (32), so

| (35) |

From the integral equation we get for

so is strictly increasing on . Therefore, the bound for extends to all . To go on, we recursively define and

and

For each interval we find a corresponding bound for , using that and therefore .

Furthermore we get for by differentiating the function defined in (33)

where . But the first summand is negative and for the second observe that

hence is decreasing.

So for we have

| (37) |

Evaluating this we obtain

But for we have so the sequence is decreasing for . ∎

Lemma 5.7.

Let be the density of as in Lemma 5.3. Then is Hölder continuous on with Hölder exponent :

| (38) |

Remark 5.8.

The latter lemma cannot be substantially improved, as in , the density is not Hölder continuous with Hölder exponent for any , see Knape (2006).

6 Explicit error bounds for

We can now combine the bounds for the density and its modulus of continuity with Lemma 2.5 and Lemma 2.7 to bound the deviation of an approximation from the solution of the fixed-point equation.

To approximate the density we set

where is given in Remark 5.5 and denotes the distribution function of .

Corollary 6.1.

We have , and . Furthermore, we can improve the bound of Lemma 5.6 and bound .

Proof.

We have , hence combining Lemma 5.6 and Lemma 2.5, we obtain

The moments of can be computed using Lemma 5.1 and we set , hence

Optimizing over for , , and yields

| (40) |

for .

Using for the value given in Remark 5.5, we obtain for the density

and optimizing over , using for the Kolmogorov metric the bound in (40), yields

for (averaging values).

We can now use this to improve our bound for : Reading off the maximal value of our approximation (), we can now bound

and this in turn enables us to improve our bounds for the approximation, leading to and for . Repeating this strategy a few times, we get the stated values for and (averaging values). ∎

Remark 6.2.

Using the realistic (but yet unproven) bound of would give () and . Hence, our approach works well for the distribution function. However, we cannot show strong error bounds for the approximation of densities with our arguments.

However, in the next section we see that for another example the algorithm approximates the densities much better than the error bounds indicate.

In Table 1, the resulting error bounds for several possible discretisations with similar running time can be found.

| Discret. | opt. | |||

|---|---|---|---|---|

| 22000 | 0.00178 | 14 | 22000 | |

| 430 | 0.00025 | 16 | 184900 | |

| 80 | 0.00012 | 13 | 512000 | |

| 30 | 0.00050 | 3 | 810000 | |

| 35 | 0.00070 | 3 | 1456110 | |

| 27 | 0.00187 | 2 | 1667712 |

7 An experimental view on error bounds

We now apply our algorithm to another fixed-point equation for which the solution is explicitly known. We can then compare the approximation of our algorithm with the true density and distribution function and evaluate the actual error to get an idea of the quality of the error bounds proven in Section 2. Further examples can be found in Knape (2006). It appears that the error bounds in Section 2 are rather loose and that the approximation is much better than indicated by our bounds.

In the analysis of certain random interval splitting procedures the following fixed-point equation characterizes the distribution of a point to which a random sequence of nested intervals shrinks:

where , , and are independent, is distributed and is uniformly distributed on , see Chen, Goodman, and Zame (1984), Chen, Lin, and Zame (1981), Devroye, Letac, and Seshadri (1986), and Neininger (2001) for details of the interval splitting context.

To approximate the fixed-point, we use a symmetric discretisation for instead of (18), setting

| (41) |

and .

To compute the bounds as given in Section 2, we can set , , and is uniformly distributed on , so

It is known that is distributed, so we have the moments:

Furthermore, has the density , so . We can now use Lemma 2.5 and Corollary 2.2 to obtain

For we minimize over and get and

| (42) |

As we know the limit distribution, we can read off the true error from the output of our simulation and find

It is quite exactly of the order expected for a discretisation of step size . Note that when approximating a differentiable function by a step function, step size and derivative impose an unavoidable error. Comparing our approximation to a direct discretisation by a step function of the same step size, the deviation is at most .

Now we look at the density. The modulus of continuity of the density of the distribution can be bounded by for all positive . So for the function , which we get by averaging over as in (16), we get with Lemma 2.7

We evaluate for , use the bound in (42), and minimizing over we obtain

for , so we take the average over values.

Reading off the true error from the simulation we obtain

and for or . The larger errors at the boundary are caused by the averaging procedure used to obtain .

Acknowledgements: We thank the referee for careful reading, pointing out some inacurracies and helping improve the presentation of the paper.

References

- (1)

- Alsmeyer et al. (2007) G. Alsmeyer, A. Iksanov, and U. Rösler (2007) On distributional properties of perpetuities. Preprint.

- Arratia et al. (2003) R. Arratia, A. D. Barbour, and S. Tavaré (2003) Logarithmic combinatorial structures: a probabilistic approach. EMS Monographs in Mathematics. European Mathematical Society (EMS), Zürich.

- Chen et al. (1984) R. Chen, R. Goodman, and A. Zame (1984) Limiting distributions of two random sequences. J. Multivariate Anal. 14, 221–230.

- Chen et al. (1981) R. Chen, E. Lin, and A. Zame (1981) Another arc sine law. Sankhyā Ser. A 43, 371–373.

- Devroye (2001) L. Devroye (2001) Simulating perpetuities. Methodol. Comp. Appl. Probab. 3, 97–115.

- Devroye et al. (2000) L. Devroye, J. A. Fill, and R. Neininger (2000) Perfect simulation from the quicksort limit distribution. Elect. Comm. in Probab. 5, 95–99.

- Devroye et al. (1986) L. Devroye, G. Letac, and V. Seshadri (1986) The limit behavior of an interval splitting scheme. Statist. Probab. Lett. 4, 183–186.

- Devroye and Neininger (2002) L. Devroye and R. Neininger (2002) Density approximation and exact simulation of random variables that are solutions of fixed-point equations. Adv. Appl. Prob. 34, 441–468.

- Donnelly and Grimmett (1993) P. Donnelly and G. Grimmett (1993) On the asymptotic distribution of large prime factors. J. London Math. Soc. 47, 395–404.

- Embrechts et al. (1997) P. Embrechts, C. Klüppelberg, and T. Mikosch (1997) Modelling extremal events. For insurance and finance. Applications of Mathematics (New York), 33. Springer-Verlag, Berlin.

- Fill and Janson (2000) J. A. Fill and S. Janson (2000) Smoothness and decay properties of the limiting quicksort density function. Mathematics and Computer Science (Versailles, 2000), pp. 53–64. Trends Math., Birkhäuser, Basel.

- Fill and Janson (2002) J. A. Fill and S. Janson (2002) Quicksort asymptotics. J. Algorithms 44, 4–28.

- Goldie and Grübel (1996) C. Goldie and R. Grübel (1996) Perpetuities with thin tails. Adv. Appl. Probab. 28, 463–480.

- Goldie and Maller (2000) C. Goldie and R. Maller (2000) Stability of perpetuities. Ann. Probab. 28, 1195–1218.

- Hwang and Tsai (2002) H.-K. Hwang and T.-H. Tsai (2002) Quickselect and the Dickman function. Comb. Probab. Comput. 11, 353–371.

-

Knape (2006)

M. Knape (2006) Approximating perpetuities.

Diploma thesis, J.W. Goethe-Universität Frankfurt a.M.

URL http://publikationen.ub.uni-frankfurt.de/volltexte/2007%/3859/ - Knape and Neininger (2007+) M. Knape and R. Neininger (2007+) Approximating perpetuities. Proceedings of 2007 Conference on Analysis of Algorithms (AofA’07) Juan-les-pins, France, June 17-22, 2007. To appear in Discrete Math. Theor. Comput. Sci.

- Mahmoud et al. (1995) H. Mahmoud, R. Modarres, and R. Smythe (1995) Analysis of QUICKSELECT: an algorithm for order statistics. RAIRO Inform. Théor. Appl. 29, 255–276.

- Neininger (2001) R. Neininger (2001) Rates of convergence for products of random stochastic matrices. J. Appl. Probab. 38, 799–806.

- Vervaat (1979) W. Vervaat (1979) On a stochastic difference equation and a representation of non-negative infinitely divisible random variables. Adv. Appl. Prob. 11, 750–783.