On estimating covariances between many assets with histories of highly variable length

Abstract

Quantitative portfolio allocation requires the accurate and tractable estimation of covariances between a large number of assets, whose histories can greatly vary in length. Such data are said to follow a monotone missingness pattern, under which the likelihood has a convenient factorization. Upon further assuming that asset returns are multivariate normally distributed, with histories at least as long as the total asset count, maximum likelihood (ML) estimates are easily obtained by performing repeated ordinary least squares (OLS) regressions, one for each asset. Things get more interesting when there are more assets than historical returns. OLS becomes unstable due to rank–deficient design matrices, which is called a “big small ” problem. We explore remedies that involve making a change of basis, as in principal components or partial least squares regression, or by applying shrinkage methods like ridge regression or the lasso. This enables the estimation of covariances between large sets of assets with histories of essentially arbitrary length, and offers improvements in accuracy and interpretation. We further extend the method by showing how external factors can be incorporated. This allows for the adaptive use of factors without the restrictive assumptions common in factor models. Our methods are demonstrated on randomly generated data, and then benchmarked by the performance of balanced portfolios using real historical financial returns. An accompanying R package called monomvn, containing code implementing the estimators described herein, has been made freely available on CRAN.

Key words: financial time series, monotone missing data, maximum likelihood, ridge regression, principal component regression, partial least squares, lasso, factor models

1 Introduction

Missingness in data, and hence the quest if one should eliminate a part of the data or try and estimate characteristics of it, is common in statistical analysis. The missing observation problem varies in style, depending on the type of data. One example is random missingness, which may stem from erroneous data (Dempster et al.,, 1977). In financial returns data analysis, however, one problem stands out, which we will refer to as monotone missingness. This happens when the assets of interest have different lengths of historical financial data, e.g., stock prices and returns. There are several possible ways of dealing with this type of incomplete dataset. One way is by utilizing the portion of data available across all of the assets. Another approach involves estimating the missing portion, called imputation (e.g., Little and Rubin,, 2002). A third approach is the focus of this paper.

Aside from some glitches in data, which will typically give rise to unrealistic spikes or random missingness in data, the monotone style of missingness that permeates financial historical returns data can be grouped into two patterns. The first is where the histories of assets differ due to the fact that they have started being publicly traded at different times. The second is where assets close for various reasons, including corporate actions such as M&A (Merger and Acquisition) activities, or liquidation due to bankruptcy. Both are critical problems to address when conducting a multivariate analysis. In this paper, we shall focus mainly on the former. This is sensible for the application to portfolio balancing that we have in mind, since one is naturally restricted to purchasing shares of companies which have survived up to current point in time. The latter type of missingness, in absence of the former, can be handled similarly, but it is not immediately clear how this would be useful for portfolio balancing. Handling both types of monotone missingness jointly, and other types of approximately monotone missingness, requires the method of data augmentation (Schafer,, 1997; Little and Rubin,, 2002). This could potentially be useful for a descriptive analysis, but is beyond the scope of this paper.

Data with arbitrary missingness patterns typically require specialized iterative (even stochastic) estimation algorithms that can be slow and cumbersome to implement. However, data which follow a monotone missingness pattern lead to a likelihood which has a convenient factorization. If we further assume that asset returns are multivariate normally distributed (MVN), with histories at least as long as the total asset count, then maximum likelihood (ML) estimators are easily obtained by performing repeated ordinary least squares (OLS) regressions, one for each asset. In the finance literature, this approach is usually attributed to Stambaugh, (1997), but it was first described by Andersen, (1957) and has since been discussed in many texts (see Section 2). The method fails when there are more assets than historical returns. In this case the OLS regressions become unstable due to rank–deficient design matrices. This is sometimes called the “big small ” problem. It has recently received much attention in the statistics community, with ready applications in bioinformatics and genomics, for example. In the context of estimation for data with a monotone missingness pattern, it can severely limit applicability to cases with a small to modest level of missingness.

In financial applications, where there may be more assets than there are historical price observations for (some of) the assets, this essentially means that the method cannot be applied on the full set of assets of interest. This paper explores remedies to this problem. We aim to develop a method that can be applied in settings where some assets have histories which are shorter than the total number of assets, and even when there are more assets than observations. In short, our solution involves replacing OLS with “parsimonious regressions” that either make a change of basis, as in principal components or partial least squares regression, or apply shrinkage, like ridge regression or the lasso. This enables the estimation of covariances between large sets of assets with histories of essentially arbitrary (and uneven) length. Even in situations where OLS would have been sufficient, we find that the more parsimonious approach can offer improvements in accuracy and interpretation.

The parsimonious approach also motivates novel ways of exploiting factor information, e.g., the value–weighted market index, size, and book–to–market factors (Fama and French,, 1993). Traditionally, factor models require the restrictive assumption that assets are independent given the factors. This underlying assumption can be thought of as a specific type of parsimony. We show how one can use the data to decide which independence constraints are reasonable, by incorporating the factors into our proposed framework, and furthermore how this may be accomplished even under condition of monotone missingness in the historical returns and factors.

The remainder of the paper is organized as follows. Section 2 defines the monotone pattern for missing data, derives the corresponding factorized likelihood, and gives an algorithm of repeated regressions to analytically find a ML estimator for the case where the sampling distribution is assumed to be MVN. Section 3 outlines methods for dealing with the “big small ” problem in the context of regression with transformed inputs and shrinkage estimators. We highlight the benefits of increased applicability, accuracy, and interpretability obtained with these methods. Section 4 gives the details of an algorithm—for MVN data under a monotone missingness pattern—that combines the method in Section 2 with the parsimonious regressions in Section 3. We explain how the method can easily integrate factor information, generating a model that essentially mixes factor models with estimators that account for the direct dependency between returns. We then briefly describe an implementation which has been made freely available as an R package called monomvn. Section 5 shows the method in action on synthetic data and real financial data with large numbers of assets having histories of highly varying length. Our results are benchmarked against several standard comparators in the context of covariance estimation and portfolio balancing, and are accompanied by comments on interpretation, efficiency, and on the (benign) consequences of using a method that leverages an MVN assumption when that assumption not believed to hold. Finally, we conclude with a discussion in Section 6 that focuses on some of the limitations inherent in taking a maximum likelihood approach.

2 Multivariate normal monotone missing data

Let be a matrix of random observations which may not be completely observed. Denote if the sample of the covariate is missing. In other words, if the columns of a sampled : , represent a historical return series of assets indexed by and a return for asset is not available at time , then . Observed are said to follow a monotone missingness pattern [e.g., (Schafer,, 1997, Section 6.5.1) or (Little and Rubin,, 2002, Section 7.4)] if the columns can be arranged so that whenever .

Figure 1 illustrates this property diagrammatically. The row dimension , of , is equal to the number of completely observed samples of , the maximally observed column. Similarly, let collect the complete data in the column of , so that .

The monotone missingness patterns considered in this paper are assumed to be missing completely at random (MCAR) in that the pattern of missingness neither depends on the observed nor unobserved responses. Note that there may be columns with identical missingness patterns. In the case of asset return series with observed histories going back different amounts of time, the MCAR assumption may be tenuous, but it is commonly asserted anyway (e.g., Stambaugh,, 1997). In our notation, the time index () for an asset’s return history would run counter to , the index of the rows of ; i.e, , as also illustrated in Figure 1.

When the missing data pattern is monotone, the likelihood can generally be factorized by exploiting an auxiliary parameterization :

together with a mapping . With the appropriate conditioning, the are assumed to be independent and identically distributed (i.i.d.), so that

| (1) |

We are concerned with the case where the follow a multivariate normal distribution (MVN) so that the likelihood in (1) also follows a MVN with constant variance and a mean linear in . The i.i.d. and MVN assumptions may be less than ideal for financial returns data (e.g., Mills,, 1927), but we note that these are common simplifying assumptions (Stambaugh,, 1997; Chan et al.,, 1999; Jagannathan and Ma,, 2003) because they lead to tractable inference and compare favorably (see Section 5 for results and further discussion). Maximum likelihood estimators (MLEs) of , , can then be obtained by regression on the complete data:

| (2) |

where and is the design matrix

containing an intercept column, and the first observations of the first columns of . So the auxiliary parameters used in (2) are .

Figure 2 diagrams the design matrix (without the intercept term) and response vector involved in one such regression. When , and particularly when , MLEs are obtainable via the straightforward calculation:

| and | (3) |

Then, starting with comprising of , and , each can be estimated conditional on and estimates of and as (Stambaugh,, 1997):

| and | (4) |

thus implicitly describing the mapping back to –space. Observe that we do not use a bias–corrected estimator for in (3), i.e., with instead of in the denominator, to ensure that ML estimates are obtained (Schafer,, 1997, pp. 224). However, we have found it to be beneficial in practice to use in the denominator as is typical in obtaining unbiased estimates of covariance matrices in the complete data case.

When several columns , say , have equal lengths of observed histories , it is typical to use a multivariate regression to find and the empirical variance–covariance matrix . Then, several can be found at once by replacing with and with in (4). Importantly, if and are positive definite, then will be positive definite as well (Stambaugh,, 1997).

Calculating such MLEs requires having for all . That is, there cannot be an asset whose history is shorter than the number of assets whose histories have greater length. If such were the case, then would not be of full rank, and could not be inverted in Eq. (3). This is sometimes referred to in the literature as the problem of regression with “big [number of parameters] small [number of observations]”. Numerical singularities may arise whenever is less than, but nearly equal to, —especially when and are large. In the following section we illustrate how these difficulties may be overcome by methods of subset selection, coefficient shrinkage, or the use of principal components.

3 Parsimonious regression

In this section, we extract and focus on the subproblem of the linear regression in (2), in terms of a design matrix of predictor variables with an intercept term () observed for cases, with corresponding responses (, where ):

| (5) |

Ordinary least squares (OLS) gives a MLE of . Classically, there are two main reasons why one may desire a more parsimonious approach to regression than that provided by OLS. The first is that OLS tends to lead to high variance estimators. The second is a desire for model fits that have high qualitative interpretability, i.e., that describe the data adequately but assume no more causes than will account for the effect. Our reasons for seeking an alternative are related to the former more so than the latter. But, most importantly, we aim to circumvent the problem of having linear dependence in the columns of when . In this case, we are faced with an design matrix with number of columns greater than the number of observations , yielding an matrix that is singular and cannot be inverted—a so–called “big small ” () problem. We may even have that , say, when the total number of assets is far greater than the number of returns recorded for the asset with the shortest history.

Popular solutions to this problem involve methods of variable selection and coefficient shrinkage. Probably the most straightforward method is subset selection (Hastie et al.,, 2001, Section 3.4.1) which aims to find the model with the “best” size (i.e., with covariates). “Best” can be defined in a number of ways, but typically involves tests, or minimizing an estimate of expected prediction error. Searching through all possible subsets quickly becomes infeasible for . Larger can be handled by greedy methods, but these offer fewer guarantees. Such methods include forward stepwise selection which starts in the null (intercept only) model and sequentially adds predictors, and backward stepwise selection which starts at the saturated model (only applicable when ) and deletes predictors. Hybridizations also exist.

By discarding some predictors, subset selection methods can yield a model which is more interpretable, and may have lower prediction error. But this “discrete” process can produce estimators with high variance. Shrinkage methods are a popular alternative. They are hailed for being more “continuous”, and in some special cases they can have implicit behavior similar to methods like forward selection. The following subsection considers the shrinkage methods of ridge regression, and those related to the lasso. In Section 3.2 we consider another family of methods which are based on derived input directions: principal components regression, which has connections to ridge regression, and partial least squares regression. These are handy when the predictors are highly correlated.

The parsimonious regression methods outlined in this section have been chosen for familiarity, computational tractability, and implementation. In each case R packages are available on the Comprehensive R Archive Network (CRAN),

http://cran.R-project.org (R Development Core Team,, 2007),

which provide off–the–shelf implementations that will make for nice subroutines within the framework of constructing estimators for MVN data under monotone missingness. It is typical to first standardize the inputs ( and ) as the methods outlined below are not equivariant under re-scaling.

3.1 Shrinkage methods: ridge regression, and the lasso

Ridge regression and the lasso shrink the coefficients of an OLS regression by imposing a penalty on their size:

| (6) |

with for ridge regression, and for the lasso. The tuning parameter controls the amount of shrinkage. Notice that the intercept () is left out of the penalty term. Solutions to (6) can be obtained analytically in the case of ridge regression with . Quadratic programming is required for the lasso. Both methods have interpretations as Bayesian maximum a posteriori (MAP) estimators after imposing particular prior distributions. Other choices of are also possible, however the constraint region for is non-convex, which makes solving the optimization problem more difficult.

For ridge regression, the penalty parameter () is most advantageously chosen by minimizing cross validation (CV) estimates of predictive error. The commonly used HKB (Hoerl et al.,, 1975) and L–W (Lawless and Wang,, 1976) methods are computationally efficient, but require that to fit an OLS. The implementation of ridge regression used in this paper comes from the MASS library (Venables and Ripley,, 2002) for R in the form of a function called lm.ridge.

Though the form of ridge regression and the lasso are similar, there are several important differences. A large will cause the ridge estimator to have many coefficients shrunk towards zero. The lasso estimator has as similar effect, but, importantly, may contain many coefficients which are exactly zero—something which is only possible for . In the Bayesian interpretation, setting corresponds to choosing a prior which concentrates more mass on small , with the most on . In this way, the lasso implements a kind of continuous subset selection. As is increased, the decrease, eventually increasing the number of them which are identically zero, though this relationship need not be strictly monotonic.

The implementation of lasso used in this paper is contained in the lars package for R (Hastie and Efron,, 2007). Efron et al., (2004) show how the lasso, and two methods called stepwise and forward stagewise, are special cases of their method of least angle regression (LAR). LARS can calculate all possible lasso estimators with computational effort in the same order of magnitude as OLS regression applied to the full set of covariates. CV can be used to select the final model, e.g., using the “one–standard–error” rule (Hastie et al.,, 2001, Section 7.10), or a more thrifty (Mallows,, 1973) method can be used, but only when . When applicable, the method performs nearly as well as CV within the MVN setting with monotone missingness. Madigan and Ridgeway, (2004) come to similar conclusions on equally tame benchmarks. However, has also been criticized for preferring large models (Ishwaran,, 2004; Stine,, 2004) and for being slightly at odds with LARS (Loubes and Massart,, 2004). Since we are mostly interested in applying LARS methods (i.e., lasso) when OLS is not applicable, i.e., when , we shall generally rely on CV to select the final model.

3.2 Principal components and partial least squares regression

In situations where there are a large number of highly correlated inputs, a decomposition by principal components (PCs) can be used to select a small number of linear combinations of the original inputs to be used in place of . The related methods of principal component regression (PCR) and partial least squares regression (PLSR) start by performing an orthogonal decomposition of , but differ in how the linear combinations are constructed.

In PCR, singular value decomposition (SVD) is performed on , i.e., , where is an matrix of left singular vectors describing the “output basis”, is a diagonal matrix containing the corresponding singular values (a square–root of the eigenvalues) in non-decreasing order, is a matrix of right singular vectors describing the “input basis”, and and are the so–called scores and loadings defined by the decomposition. Next, is regressed on the first PCs, i.e., the scores , where the subscript indicates the extraction of the first columns of , i.e., the first columns of , , and the first rows/cols of . Since the columns of are orthogonal, the solution is just a sum of univariate regressions. Importantly, the solution can then be written in terms of the coefficients on the predictors in the columns of ,

| (arbitrary scores and loadings) | (7) | ||||

| (from SVD on ) |

a vector of length . When , the coefficients in (7) are identical to those obtained by OLS. There are many ways of choosing how many components () to keep in the final model. One way is to consider the relative sizes of the eigenvalues as a proportion of the variation explained by each principal component, and then choose so that 80–90% of the variation is explained. A less ad hoc and more reliable—but more computationally intensive—method that can be applied even when involves using CV to estimate predictive error in order to find .

PLSR, by contrast, aims to incorporate information about both and in the scores and loadings—which in this context are often called latent variables (LVs)—by proceeding iteratively. The method is initialized with the SVD of , thereby including information about the correlation between, and the variance within, and . The scores and loadings obtained by PLSR optimally capture the covariance between and , whereas PCR concentrates only on the variance of (de Jong,, 1993). There are several algorithms for obtaining the scores and loadings, but once obtained, the regression coefficients in -space are recovered by following (7), and CV can be similarly used to pick .

In situations where a minor component of is highly correlated with , PLSR may have a significant advantage over PCR. Otherwise, the methods have a more or less comparable performance record despite a few operational differences—e.g., PLSR usually needs fewer LVs, but can also yield higher variance estimators of the regression coefficients. Both have behavior similar to other shrinkage methods, particularly ridge regression. For example, it can be shown (Frank and Friedman,, 1993) that ridge regression shrinks the coefficients of principal components by a factor of , where the are from the diagonal of , whereas PCR truncates them at .

4 The monomvn algorithm

So long as for all , and , an algorithm for finding the parameters and that maximize the MVN likelihood for monotone missing data proceeds as outlined in Section 2. Initialize and to the sample mean and variance of the first column of , then iterate through the following steps for :

- 1.

-

2.

Obtain the MLEs of and from , , and as in (4).

If any , then we have a “big small ” problem, and the standard regression in step 1 above cannot be performed. In practice, it may be that and still there are columns of the design matrix which are not linearly independent, and so it is not of full rank. The chances that this may happen become increasingly more likely as approaches when finite (double–precision) computer representations make it so that the design matrix is numerically rank deficient. Both issues are addressed simultaneously by instead performing one of the parsimonious regressions outlined in Section 3. Then step 2 can proceed as usual. Observe that this approach also enables estimation when there are more assets than historical returns ().

4.1 Choosing the parsimonious proportion

Even when parsimonious regression is not strictly necessary, it can aid in interpretation, and possibly even yield more accurate and lower variance estimators. The lasso and the other LARS methods can choose to shrink so that only the intercept term is nonzero. This enables the detection of zeros in the MVN covariance matrix . In other words, it can be used as a test, of sorts, for independence between assets.

Towards building a more efficient and interpretable estimator, one may consider applying a parsimonious regression for every iteration of step 1 above. This is explored further in Section 5.3. Alternatively, one could determine a threshold, say , representing a proportion of rows to columns in the design matrix past which a parsimonious regression is applied regardless. That is, when , for . Then, the case corresponds to always using a parsimonious method, and reverts to applying one only when necessary. In Section 5.1.2 we show how easy it is to establish reliable rules of thumb for choosing .

4.2 Incorporating factors

A popular estimator for the covariance matrix of financial asset returns involves using factor models. The essential idea behind the factor model is to regress the observed returns on measured common market factors , and to derive a covariance matrix of the returns as a function of the regression equations.

For a factor space with factors, the model can be formalized as follows. Each excess return is modeled by the regression equation

| (8) |

where each is a residual term independent of . The residual terms for the instance are assumed to follow a zero–mean MVN with diagonal covariance matrix . For instance, a common one–factor model takes to be value–weighted market index (e.g., Chan et al.,, 1999). A common three–factor model augments the value–weighted market index with size and book–to–market factors (Fama and French,, 1993).

Factors are assumed, for now, to be i.i.d. and to follow a MVN with covariance matrix . Let be the matrix defined by the entries , for . It follows that the covariance matrix of the returns, as parameterized by , is given by

| (9) |

An estimate can therefore be obtained by estimating each column of by regressing on with an intercept. The mean sum of squares of the residuals of each regression forms the diagonal of , and the off–diagonal entries are zero. The estimate is the empirical covariance of the factors. Note that each regression equation requires only the data observed for the particular return , together with the corresponding observations for the factor(s). However in practice, the method is applied only to completely observed and .

The main underlying assumption is that returns are mutually independent conditioned on the factors. If the number of factors is considerably smaller than the number of returns, the model will be parsimonious and the resulting will have lower variance than the empirical covariance matrix. This assumption allows for any missingness pattern, even the extreme one where no joint observation of returns and exists. The drawback is that the independence assumptions encoded in this model might be unrealistic, and the resulting estimate will suffer from a strong bias.

Instead, we can use the data to find which independence assumptions are adequate by integrating the factor model into the monomvn framework. Consider the full regression model, where we regress on and simultaneously:

| (10) |

The term does not appear because it is not identifiable given the presence of . Since this formulation is in the same family of parameterizations of the original models used in monomvn, an analogous procedure applies with minor pre- and post-processing. First shift the labels the returns for each asset by so that becomes and the corresponding becomes . Then map to and to . If the recursion in Eq. (4) is then applied as usual, giving the estimates [an vector] and [an matrix], an estimate of the covariance matrix of the asset returns can then be extracted from the bottom–right block of , i.e., . The superscript is meant to indicate dependence on both factors and assets. Importantly, no internal changes to the workings of the monomvn algorithm are necessary.

Observe that if the (parsimonious) regression method applied within monomvn uses OLS whenever regressing onto the factors, and sets the regression coefficients to zero otherwise, then we obtain . In the context of monomvn we call this the “factor–parsimony” regression, filling a role similar to PCR, lasso, etc. If required, the covariance matrix of the factors can also be recovered as . Also observe that, within the monomvn framework, it is possible to handle factors with historical missingness.

If, instead of the factor–parsimony method, any of the other methods (outlined in Section 3) are used, then shrinkage is applied to both and in (10). In this case we obtain a generalization of the independence structure assumed in the classical factor model, allowing the data (factors and returns) to determine the appropriate mix of influence on the resulting estimator for . It is interesting to point out the link between this generalized factor model (10) resulting in , and the optimal shrinkage estimator of Ledoit and Wolf, (2002):

| (11) |

Here, is the standard covariance estimate obtained using only the portion of the data available across all assets and is an “optimal” mixing proportion chosen by CV. (Note that Ledoit’s factor–based estimator uses only completely observed joint returns.) The spirit of these two approaches is similar, but they are quite distinct. The published success of this type of shrinkage approach suggests that it is important to combine a (complete data) factor–based estimate with a traditional covariance estimate. Indeed, the estimator involves combining covariances mediated by factors with covariances that are not accounted for by factors; it can also handle historical missingness via the “factor–parsimony” regressions within monomvn. But rather than shrinking a (possibly) non–positive definite estimator towards with a single parameter as in (11), monomvn applies unique shrinkage parameters, one for each regression, while taking full advantage of all available returns.

4.3 Software

Finally, an R package called monomvn (Gramacy,, 2007) has been made freely available through CRAN. It implements the algorithm described in this section, and supports all of the parsimonious regression methods outlined in Section 3 via the stand–alone packages outlined therein. Two forms of CV are supported for choosing the number of components in the parsimonious regression: random 10–fold and (deterministic) leave–one–out (LOO). A argument facilitates parsimonious regression modeling, as described above. Incorporating factors is as straightforward as bundling them in as if they were returns, as described above.

5 Empirical results

In this section, the monomvn methods are illustrated and validated on real and synthetic data. In Section 5.1 we focus on the properties of estimates of and in a controlled setting involving synthetic data under monotone missingness. In 5.2 we turn to applying the estimators towards balancing portfolios in a mean–variance setting. We wrap up in 5.3 by using monomvn in a descriptive analysis of dependence involving thousands of assets.

5.1 Properties of the estimators on synthetic data

Here, we use a data–generation mechanism provided by the monomvn package: randmvn generates random samples from a randomly generated MVN distribution with an i.i.d. standard normal mean vector , and an Inv–Wishart sampled ; rmono imposes a uniformly distributed monotone missingness pattern. A similar method is used to generate samples with monotone missingness from a multivariate distribution (MV) as well, in order to demonstrate that the MVN–based monomvn methods still perform well in the presence of heavier tailed data.

The comparisons to follow focus on highlighting the relative strengths and weaknesses of variations of monomvn as a function of the choice of parsimonious regression method applied. Additionally, two simpler methods are devised as calibration tools, and to illustrate the advantage of the monomvn approach over those which do not leverage the structure of the monotone missingness pattern. The simplest comparator is called “complete”, where and are estimated using only the portion of data available across all assets, i.e., only the completely observed returns. Put yet another way: only the first rows of are used. Another comparator is “observed” which uses all of the available data in an obvious but naïve way:

| and | (12) |

Unfortunately, the covariance matrices provided by the “complete” and “observed” estimators are not guaranteed to be positive–definite (Stambaugh,, 1997).

As a final comparator, we consider a method of estimation for incomplete data for arbitrary missingness patterns (Dempster et al.,, 1977), using the expectation conditional maximization (ECM) algorithm (Meng and Rubin,, 1993). Consequently, this method also works when the missingness pattern is monotone, but represents a sort of overkill in this case. Two similar software packages are available for this method when the data is assumed to follow a multivariate normal distribution: the norm package (Novo and Schafer,, 2002) for R, and ecmnmle (contained in the Matlab Financial Toolbox). We prefer norm because its core is implemented in compiled Fortran, with an R wrapper. It gives nearly identical results to—but runs more than 20 times faster than—ecmnmle which is written solely in Matlab. The ECM method iterates until convergence, stopping at a local maximum when an improvement threshold is met. As a result, its computational demands and the ultimate optimality of the resulting estimator are sensitive to the initial configuration of the algorithm. Though the missingness pattern may be arbitrary, it is well–known that the method can fail due to convergence issues and/or numerical singularities that can arise due to finite machine representations when more than 15% of the data is missing (see, e.g., the ecmnmle documentation within Matlab). So it cannot handle , which precludes it from general use in our problem.

The expected log likelihood (ELL), which is related to the Kullback–Leibler (KL) divergence, is used as the main metric for comparisons. For probability distribution functions (PDFs) and , the KL divergence between and is defined as

In the particular case where is the estimated MVN with parameters and and is the “true” parameterization with and , the KL divergence can be shown to be:

The ELL of relative to data sampled from is given by

| (13) |

The integral in (13) is the entropy of . The entropy of can be shown to work out to When analytical expressions are not available it is easy to approximate (13) numerically by , where is simulated out of sample. This nicely converges to the truth for large . The ELL is good for ranking competing estimators, however actual “distances” between estimators is hard to interpret.

5.1.1 Comparing estimators

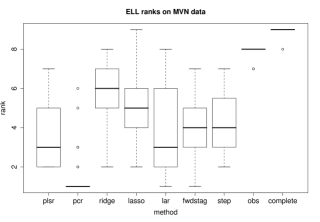

Figure 3 (left) summarizes a comparison between the different parsimonious regressions within the monomvn algorithm, using randomly generated MVN data with and , repeated over 100 trials, each time sampling new , and with uniform monotone missingness.

Parsimonious regressions were used only when necessary (i.e., ). 10–fold CV was used to choose or the number of (principal) components. As can be seen from the table, PCR emerges as the clear winner in this comparison, nearly always having the best ELL rank. The complete and observed comparators are almost always ranked worst.

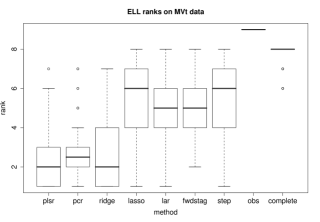

In anticipation of the application in Section 5.2 to financial returns data, which are believed to follow a heavier tailed distribution than MVN, we repeated the above experiment with synthetically generated MV data with a monotone missingness pattern. The degrees of freedom parameter was sampled as . Figure 3 (right) shows roughly similar behavior for the MVN based monomvn estimators when fit to MV data: PCR is the best and the observed and complete estimators are the worst (although the order is switched). ELL was computed numerically using the known degrees of freedom parameter(s), , which generated the data. This is a legitimate choice since the is not used in the mean–variance analysis to follow in Section 5.2. It is interesting to note the improved rank(s) of the ridge regression based estimator in this case.

These results are in line with those of previous simulation studies which compare ML estimators—that are able to leverage all of the available data by exploiting the MVN assumption—to those which use more reasonable distributional assumptions but which, for reasons of tractability, can only use the completely observed cases (e.g., Little,, 1988). The evidence suggests that making use of all of the available data in a sensible way is the crucial ingredient despite that the underlying assumptions may be violated. The dominance of PCR in both MVN and MV scenarios is in line with a recent study (De Mol et al.,, 2007) showing that PCR out–competes other shrinkage (Bayesian motivated) estimators in applications with a large number of financial asset returns.

5.1.2 Choosing the parsimonious proportion

Recall from Section 4 that determines when a parsimonious method is to be used instead of OLS in the monomvn algorithm. The experiment performed here is similar to the previous one, except that and are varied stochastically with uniform in and uniform in .

| optimal | ||||

|---|---|---|---|---|

| method | 5% | mean | 95% | improv |

| plsr | 0.12 | 0.23 | 0.37 | 0.55 |

| pcr | 0.09 | 0.27 | 0.51 | 0.69 |

| ridge | 0.04 | 0.25 | 0.67 | 0.29 |

| lasso | 0.12 | 0.24 | 0.38 | 0.76 |

| lar | 0.11 | 0.26 | 0.41 | 0.65 |

| stepwise | 0.15 | 0.26 | 0.39 | 0.74 |

Table 1 shows the mean and 90% interval for the optimal over 100 repeated trials sampling new , , etc., each time. LOO CV was used to choose , or the number of (principal) components, and the objective criteria used was ELL. The final column in the table shows the proportion of time when was better than . Observe that all methods except ridge regression work well, as a rule of thumb, with . All things being equal, a larger setting may be preferred for speed reasons.

5.1.3 Comparing to ECM

Due to the limitations of ECM–based methods, like those implemented by norm and ecmnmle, a comparison of monomvn to these approaches requires a more controlled experiment. Fixing and , 1000 repeated experiments similar to the ones described above, with uniform monotone missingness, gave that monomvn (with PCR) had higher ELL 997 times () and that ECM failed to converge 53 times (). As grows relative to , the performance of the methods converge. For example, with and the means are monomvn is better 831 times (), and ECM failed to converge 11 times (). As the dimensionality () increases modestly compared to the sample size (), the ECM–based norm algorithm consistently diverges. For example, with and norm fails to converge more than 40% of the time.

5.2 Constructing portfolios from historical returns

In this section we examine the characteristics of minimum variance portfolios constructed using estimates of based on historical monthly returns. The experimental setup is similar to ones that have been used in several recent papers on covariance estimation, and minimum variance portfolio balancing (e.g. Chan et al.,, 1999; Jagannathan and Ma,, 2003). Following these works we use the monthly returns of common domestic stocks traded on the NYSE and the AMEX from April 1968 until 1998. We require that the stocks have a share price greater than $5 and a market capitalization greater than 20% based on the size distribution of NYSE firms. Estimators of are constructed based on (at most) the most recently available 60 months of historical returns. This is in keeping with previous work and acknowledges that the i.i.d. assumption in Eq. (1) is only valid locally (in time) due to the conditional heteroskedastic nature of financial returns. Short selling is not allowed; all portfolio weights must be nonnegative. Although it is typical to cap the weights as well, e.g., at 2%, in order to “tame occasional bold forecasts” (Chan et al.,, 1999) that typically arise due to poor estimators (Jagannathan and Ma,, 2003), we specifically do not do so here. Our goal is fully expose the quality of the estimators and to illustrate that with good estimators such rules of thumb are unnecessary.

Four classes of estimators of are used in the comparisons which follow. (1) The complete estimator outlined earlier, with variations depending on how many assets have historical returns with certain lengths (more below). (2) A one–factor model using the return on the value–weighted portfolio of stocks traded on the NYSE, AMEX, and Nasdaq. (3) The monomvn method using the parsimonious regressions of Section 3 with . (4) The monomvn method incorporating the value–weighted portfolio as a factor with, as described in Section 4.2, and with . For this class we augment the collection of parsimonious regressions to include the “factor–parsimony” method. We do not compare to the ECM methods of norm or ecmnmle here, as this has proved to be both cumbersome and troublesome; the methods seem unable to handle the missingness level in this data. For example, norm consistently fails to converge even after thousands of very slow iterations of ECM (each taking several seconds on a 3.2 GHz Xeon).

To assess the quality and characteristics of the constructed portfolios we follow Chan et al., (1999) in using the following: (annualized) return and standard deviation; (annualized) Sharpe ratio (average return in excess of the Treasury bill rate divided by the standard deviation); (annualized) tracking error (standard deviation of the portfolio return in excess of the S&P500 return); correlation to the market (S&P500 return); average number of stocks with weights above 0.5%. We closely follow the experimental setup of Chan et al., (1999) and Jagannathan and Ma, (2003) by randomly subsampling from the qualifying stocks in each year, and holding the portfolios for the entire subsequent 12 months. The random subsample reduces the size of the estimation problem, and thus computational burden, so that many methods can be simultaneously benchmarked against one another. It can also serve the dual purpose of enabling the calculation of nonparametric (bootstrap–like) Monte Carlo assessments of variability, which was not a feature explored in previous work.

Specifically, in each April, starting in 1972, we randomly subsample 250 stocks (without replacement) from those which qualify (in the sense outlined above) and which have at least 12 months of historical returns. In this way our work differs slightly from our predecessors whose estimators require exactly 60 months of historical returns. We chose 12 months in order to highlight the benefit of incorporating assets in the portfolio with fewer than 60 months of returns via monomvn. Estimates of the covariance matrix of monthly excess returns (over the monthly Treasury Bill rate) are generated form the different models using at most the last 60 months of historical returns for the 250 assets. Based on the estimate(s), quadratic programming is used to find the global minimum variance portfolio(s) described by weights . Then, the weights are applied to form buy–and–hold portfolio returns until the next April, when the randomization, estimation, and optimization steps are repeated and the portfolios are reformed.

| method | mean | sd | sharpe | te | cm | wmin |

| eq | 0.149 | 0.188 | 0.432 | 0.062 | 0.949 | 0 |

| vw | 0.135 | 0.162 | 0.412 | 0.032 | 0.981 | 45 |

| min | 0.147 | 0.183 | 0.431 | 0.105 | 0.819 | 29 |

| com | 0.150 | 0.183 | 0.447 | 0.107 | 0.810 | 26 |

| rm | 0.132 | 0.129 | 0.494 | 0.094 | 0.803 | 16 |

| fmin | 0.142 | 0.146 | 0.503 | 0.086 | 0.845 | 38 |

| fcom | 0.144 | 0.146 | 0.521 | 0.087 | 0.841 | 37 |

| frm | 0.138 | 0.130 | 0.537 | 0.117 | 0.688 | 21 |

| plsr | 0.148 | 0.154 | 0.516 | 0.124 | 0.686 | 15 |

| pcr | 0.143 | 0.132 | 0.563 | 0.109 | 0.732 | 23 |

| ridge | 0.158 | 0.165 | 0.546 | 0.122 | 0.716 | 16 |

| lasso | 0.151 | 0.150 | 0.550 | 0.054 | 0.941 | 69 |

| lar | 0.151 | 0.151 | 0.545 | 0.053 | 0.944 | 71 |

| step | 0.152 | 0.155 | 0.541 | 0.052 | 0.946 | 75 |

| ffp | 0.143 | 0.132 | 0.566 | 0.113 | 0.712 | 24 |

| fplsr | 0.147 | 0.153 | 0.514 | 0.123 | 0.688 | 15 |

| fpcr | 0.142 | 0.131 | 0.560 | 0.109 | 0.732 | 24 |

| fridge | 0.158 | 0.163 | 0.554 | 0.119 | 0.726 | 19 |

| flasso | 0.152 | 0.148 | 0.561 | 0.056 | 0.936 | 69 |

| flar | 0.151 | 0.151 | 0.546 | 0.053 | 0.943 | 70 |

| fstep | 0.154 | 0.153 | 0.558 | 0.055 | 0.939 | 73 |

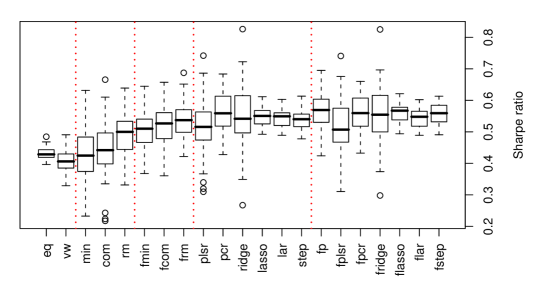

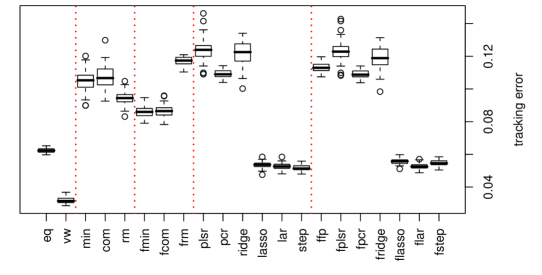

Table 2 summarizes the properties of those returns averaged over 50 repeated random paths through the 26 years in the study. The table is broken into five sections, vertically, starting with the equal– and value–weighted portfolios (for comparison), followed by global minimum variance portfolios based on estimated : complete data estimators, complete data estimators based on a one–factor model, monomvn estimators, and monomvn estimators incorporating the one–factor. Throughout, the “f” prefix indicates that the estimator uses the value–weighted factor in some way. The “min” and “fmin” estimators use only the last 12–months of historical returns, whereas the “com” and “fcom” estimators use the maximal complete history available. The “rm” and “frm” estimators focus only on those assets with completely observed returns for the last 60 months—where the weights for the other assets are set to zero (removing them from the portfolio). The annualized mean, standard deviation, and Sharpe ratio statistics for these six estimators lead one to conclude that the more historical returns (within the five–year window) that can be used to estimate the better. Tracking error is also improved, except in the case of “frm”. All in all, these results support those obtained in previous studies (e.g., Chan et al.,, 1999) showing that, in particular, factor models improve upon the naïve estimator in the complete data case. Further inspection of this part of the table reveals that the improved Sharpe ratios for “rm” and “frm” are due to the smaller standard deviation obtained under these estimators, but that this comes at the expense of a smaller mean return. This may be due to more weight being placed on fewer assets (as indicated in the “wmin” column). Both “rm” and “frm” also have the lowest correlation to the market in their cohort.

The final two groups of rows tell a similar story. The Sharpe ratios for the monomvn estimators—with and without the value–weighted factor—show marked improvements over the complete data estimators. As before, the inclusion of the value–weighted factor further adds to the improvement, e.g., yielding higher Sharpe ratios except in the case of PCR where they remain essentially unchanged. The “ffp” estimator, i.e., the one–factor model applied via monomvn using the “factor–parsimony” regression method, has the lowest standard deviation, and therefore a comparatively high Sharpe ratio despite a low mean return. We can see that, as with “rm” and “frm”, this low standard deviation is obtained by placing large weight on only a few assets. PCR, PLSR, and ridge regression—both with and without factors—show similar properties. In contrast, the LARS estimators (lasso, lar, and stepwise—both with and without the factor), obtained similar or better Sharpe ratios but with a large mean return, by assigning large weight to roughly three times more assets. As a result, these LARS estimators obtain a much lower tracking error and higher correlation to the market.

So when appropriate factors are available it makes sense to use them, and the best way to do so is via monomvn. It would seem that the one–factor LARS based monomvn estimators give the best results in the study, overall, with lasso in the top spot. It is reassuring to notice that, when an appropriate factor is not available, the LARS based monomvn methods, and PCR, give largely similar results by incorporating all of the available returns in a parsimonious way. This is not true in the case of the complete data estimators.

Figure 4 compliments Table 2 by showing the distribution (via boxplots) of the Sharpe ratios and the tracking error obtained for each of the 50 random paths through the 26 years. Recall that these were obtained by randomly sampling 250 qualifying assets in each year. The numbers in Table 2 are the means of data use to construct each boxplot, whereas the boxplots in the figure represent Monte Carlo approximations to the sampling distribution of portfolio characteristics under the various estimators of . In short, the figure reinforces the superiority of the LARS estimators which, in addition to having large Sharpe ratios and small tracking error, also exhibit small variability with respect to Monte Carlo resampling. It is interesting to note that the LARS based estimators (without the factor) show the lowest variability in their Sharpe ratios amongst all monomvn estimators.

It may be tempting to conclude that these results contradict the results of the ELL–based comparison(s) on synthetic data in Section 5.1. Indeed, in that section we saw that PCR seemed to be the best at recovering the (known) of the distribution which generated the training data. However, means, variances, Sharpe ratios, tracking error, etc., are specific statistics, and moreover they are obtained after a (highly non–linear) transformation into portfolio weights via quadratic programming. Therefore, we should expect to see different results, since these statistics represent utilities which are different from ELL. That being said, notice that PCR is still the best in terms of average annualized standard deviation (and thus Sharpe ratio) [see Table 2] when no appropriate factors are available—but with high variability [see Figure 4]. Importantly, both experiments (here and in Section 5.1) show, resoundingly, that using all of the available data via monomvn is preferred over a complete data estimator.

5.3 Examining dependence relationships between assets

For our final empirical analysis we shall demonstrate the descriptive power of monomvn. At the same time we shall take the opportunity to show how the method can be applied when there are thousands of assets.

From Thomson Financial’s Datastream (www.datastream.com), we have downloaded, in dollar terms, the total returns data of each stock in the Russell 3000 Index representing the broad United States equity universe encompassing approximately 98% of the market: 1792 weekly returns between 12/01/1973 and 11/05/2007 for 2894 assets. In order to obtain a set of clean and complete data, each series is tested for illiquidity, completeness, and stationarity, using the following methodology. We removed assets which were marked to market at a frequency other than weekly, to exclude illiquid assets that may exhibit artificial serial correlation (this essentially excludes any stock that has more than two weeks of consecutive unchanging prices at any point in time). Then, an augmented Dickey Fuller test (Dickey and Fuller,, 1979) is employed to exclude any of the assets that exhibit non–stationarity (six lags have been tested at the 99% confidence level). A total of 2461 stocks remained after applying these two filtering steps. There are 558 assets with longest history of 1792 returns; the least observed asset has only 76 returns (so the “complete” estimator(s) can use only 3% of the data); the overall proportion of missing observations was 0.472.

We consider applying the lasso version of the monomvn algorithm to this data, with , i.e., always use the lasso (never use OLS). As we have mentioned, the lasso (and other LARS methods) have descriptive (as well as predictive) power because they can provide with many coefficients set to zero. In the context of the monomvn algorithm this means that the MLE may have zero entries, indicating marginally uncorrelated assets, and moreover may have block–diagonal structure (or zeros in indicating a pairwise conditional independence of assets. Since ridge regression, PCR, and PLSR always yield , they would never produce a zero in or , and so would be less useful for creating such qualitative summaries of the relationships between asset returns. It may be tempting to interject zeros where there are small values in or , but like the “complete” and “observed” estimators, the resulting matrix would not usually be positive definite. Moreover, classical pairwise tests for independence, say via the Pearson product–moment correlation coefficient, would give unrealistic results. With return histories as short as weeks and estimated correlation less than about 0.2, a simple calculation shows that there would not be enough evidence to reject the hypothesis that the correlation is zero.

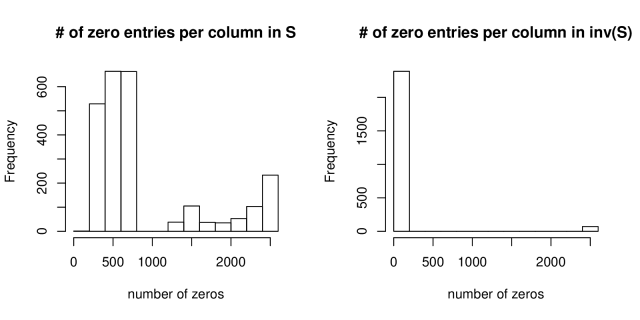

The estimator obtained using the lasso on this data yields a with 36% of its entries set to zero. Moreover, 50 of its 2641 columns (or 2%) are everywhere zero except in the diagonal position. This means that 36% of asset pairings are marginally uncorrelated. Investigating pairwise correlation between assets, conditional on all of the others, involves looking for zeros in , of which we find 140 (or 6%). This means that the rows/columns of can be reordered so that the matrix has block–diagonal structure, and that the returns of 6% of the assets are conditionally independent.

Figure 5 shows histograms summarizing the number of zeros in each column of and . Every column in both matrices had at least one zero entry. The figure clearly illustrates that the resulting correlations can be used to cluster the assets, but this is beyond the scope of this paper.

To wrap up the experiment we downloaded the market returns available from the Russel 3000 index for 1479 (of 1792) contiguous weeks ending 11/5/2007 and used them to create a residual return series for each of the 2461 assets in our study. We then re-ran the lasso experiment, above, to discover that 58% of the asset parings are marginally uncorrelated and 14% are conditionally independent when the market is taken into account. The histograms corresponding to this experiment are similar to those for the initial one, in Figure 5, and so they are not reproduced here.

6 Discussion

We have shown how the methods of Stambaugh, (1997) can be applied for large numbers of assets whose histories are (nearly) unconstrained in length. The key insight is in replacing OLS regressions with more parsimonious ones that either use derived input directions or apply some sort of shrinkage. Whereas Stambaugh demonstrated his methodology on 22 assets, we have shown how the monomvn algorithm—essentially the same methodology with a different regression method—can handle thousands. We argued that even when OLS regressions suffice, the more parsimonious ones can offer improvements in both accuracy and interpretation. We also argued that it is advantageous to let a model selection method (e.g., parsimonious regression) decide which dependencies between factors and returns exist, as opposed to assuming a classical factor model structure.

Stambaugh, (1997) showed that by applying the standard noninformative prior (e.g. Schafer,, 1997, pp. 154) it is possible to turn the MLEs and into moments and of a Bayesian posterior (predictive) distribution that, when used in the mean–variance framework, are said to take estimation risk into account. We note that, due to the notation used in that paper, it is a common misconception that these posterior moments forecast the ML estimates into the future. Since Stambaugh employs the i.i.d. assumption in the same way that we do in Eq.(1), these are only moments of the posterior for conditioned on the available historical data. Therefore, time is irrelevant, so the moments apply to the past as well without modification. Finally, to label this approach as “Bayesian” is an overstatement. While Stambaugh is correct to note that estimates of the mean vector and covariance matrix are all that are needed within the mean–variance framework, what results is a point–estimate (vector) of optimal portfolio weights, not (samples from) a Bayesian posterior distribution, as would be ideal. The challenge is that while the moments of the posterior have a nice closed form, the distribution itself does not. Further challenges limit the application of this approach in the “big small setting”. In this situation the standard noninformative prior leads to an improper posterior. This can be most easily seen in the calculation of Stambaugh’s (in our notation) in Eq. (69–71), pp. 302, where the resulting diagonal would be negative.

Stambaugh’s Bayesian approach is not the only way forward. It is possible to obtain the sampling covariance matrix of analytically. However, an analytic form for the sampling variability of is not known. The bootstrap (e.g. Hastie et al.,, 2001, Sections 7.11 & 8.2) offers a Monte Carlo method for quantifying the stability of via its component-wise confidence intervals. We took a related approach at the end of Section 5.2 to examine how variability in , arising from random subsamples of 250 assets, filters through to the properties of the balanced portfolios. However, Little and Rubin, (2002, Section 7.4.4) make a strong argument in preference for a fully Bayesian approach instead. Facilitating tractable Bayesian estimation for parsimonious regression algorithms, as would be required by monomvn, presents a serious challenge. The Bayesian lasso (Park and Casella,, 2008) and so–called Bayesian latent factor models (West,, 2003), which can be seen as a Bayesian extension of principal components and partial least squares regressions, have received much attention in the recent literature. Exploring the extent to which these can be applied within the monomvn algorithm to get samples from the posterior distribution of and is part of our ongoing work. These samples can accurately reflect the estimation risk in mean–variance portfolio allocation by filtering the uncertainty though the optimization to get a distribution on the simplex of portfolio weights.

Another interesting extension would involve relaxing the assumption of (multivariate) normality, i.e., to decouple the dependence distribution, or copula (Sklar,, 1957), from the marginals. In this regard, Patton, (2006) has made promising inroads into applying copulas to a pair of return series under a monotone missingness pattern. Although the theory for copulas (Nelsen,, 1999) naturally extends beyond two dimensions, the application of the methodology quickly becomes intractable without enforcing severely restrictive assumptions. Our ongoing work includes identifying ways in which the monomvn algorithm for high–dimensional estimation under monotone missingness may be extended to support marginal Student– distributions and GARCH models with various parametric forms of the copula. While there is plenty of evidence in the literature against the assumption of normality for asset returns (e.g. Mills,, 1927), we argued that the most important thing is to be able to make use of all of the available data with an algorithm that is computationally tractable.

References

- Andersen, (1957) Andersen, T. (1957). “Maximum Likelihood Estimates for a Multivariate Normal Distribution when Some Observations Are Missing.” Journal of the American Statistical Association, 52, 200–203.

- Chan et al., (1999) Chan, L. K., Karceski, J., and Lakonishok, J. (1999). “On Portfolio Optimization: Forecasting Covariances and Choosing the Risk Model.” The Review of Financial Studies, 12, 5, 937–974.

- Dayal and MacGregor, (1997) Dayal, B. and MacGregor, J. (1997). “Improved PLS algorithms.” Journal of Chemometrics, 11, 1, 73–85.

- de Jong, (1993) de Jong, S. (1993). “SIMPLS: An Alternative Approach to Partial Least Squares Regression.” Chemometrics and Intelligent Laboratory Systems, 18, 251–263.

- De Mol et al., (2007) De Mol, C., Giannone, D., and Reichlin, L. (2007). “Forecasting Using a Large Number of Predictors: Is Bayesian Regression a Valid Alternative to Principal Components?” Tech. Rep. 5829, C.E.P.R. Discussion Papers.

- Dempster et al., (1977) Dempster, A., Laird, N., and Rubin, D. B. (1977). “Maximum Likelihood from Incomplete Data via the EM Algorithm.” Journal of the Royal Statistical Society, Series B, 39, 1, 1–37.

- Dickey and Fuller, (1979) Dickey, D. and Fuller, W. (1979). “Distribution of the Estimators for Autoregressive Time Series with a Unit Root.” Journal of the American Statistical Association, 74, 427–431.

- Efron et al., (2004) Efron, B., Hastie, T., Johnstone, I., and Tobshirani, R. (2004). “Least Angle Regression (with discussion).” Annals of Statistics, 32, 2.

- Fama and French, (1993) Fama, E. and French, K. (1993). “Common Risk Factors in the Returns on Stocks and Bonds.” Journal of Financial Ecolomics, 33, 3–56.

- Frank and Friedman, (1993) Frank, I. and Friedman, J. (1993). “A Statistical View of Some Chemometrics Regression Tools (with Discussion).” Technometrics, 35, 2, 109–148.

- Gramacy, (2007) Gramacy, R. B. (2007). The monomvn Package: Estimation for Multivariate Normal Data with Monotone Missingness. Statistical Laboratory, University of Cambridge, Cambridge, UK.

- Hastie and Efron, (2007) Hastie, T. and Efron, B. (2007). lars: Least Angle Regression, Lasso and Forward Stagewise. R package version 0.9-7.

- Hastie et al., (2001) Hastie, T., Tibshirani, R., and Friedman, J. (2001). The Elements of Statistical Learning: Data Mining, Inference, and Prediction. Springer.

- Hoerl et al., (1975) Hoerl, A. E., Kennard, R. W., and Baldwin, K. F. (1975). “Ridge Regression: Some Somulations.” Communications in Statistics, 4, 105–123.

- Ishwaran, (2004) Ishwaran, H. (2004). “Discussion of ‘Least Angle Regression’ by B. Efron, T. Hastie, I. Johnstone, and R. Tibshiran.” Annals of Statistics, 32, 2, 465–469.

- Jagannathan and Ma, (2003) Jagannathan, R. and Ma, T. (2003). “Risk Reduction in Large Portfolios: Why Imposing the Wrong Constraints Helps.” Journal of Finance, American Finance Association, 58, 4, 1641–1684.

- Lawless and Wang, (1976) Lawless, J. and Wang, P. (1976). “A simulation study of ridge and other regression estimators.” Commonucations in Statistics – Theory and Methods, A5, 307–323.

- Ledoit and Wolf, (2002) Ledoit, O. and Wolf, M. (2002). “Improved estimation of the covariance matrix of stock returns with an application to portfolio selection.” Journal of Emperical Finance, 10, 603–621.

- Little, (1988) Little, R. (1988). “Robust Estimation of the Mean and Covariance Matrix from Data with Missing Values.” Applied Statistics, 39, 23–29.

- Little and Rubin, (2002) Little, R. J. and Rubin, D. B. (2002). Statistical Analysis with Missing Data. 2nd ed. Wiley.

- Loubes and Massart, (2004) Loubes, J.-M. and Massart, P. (2004). “Discussion of ‘Least Angle Regression’ by B. Efron, T. Hastie, I. Johnstone, and R. Tibshiran.” Annals of Statistics, 32, 2, 465–469.

- Madigan and Ridgeway, (2004) Madigan, D. and Ridgeway, G. (2004). “Discussion of ‘Least Angle Regression’ by B. Efron, T. Hastie, I. Johnstone, and R. Tibshiran.” Annals of Statistics, 32, 2, 465–469.

- Mallows, (1973) Mallows, C. (1973). “Some comments on .” Technometrics, 15, 661–675.

- Martens and Næs, (1989) Martens, H. and Næs, T. (1989). Multivariate Calibration. Chirchester: Wilely.

- Meng and Rubin, (1993) Meng, X. and Rubin, D. B. (1993). “Maximum Likelihood Estimation via the ECM algorithm.” Biometrika, 80, 2, 267–278.

- Mevik and Wehrens, (2007) Mevik, B.-H. and Wehrens, R. (2007). “The pls Package: Principal Component and Partial Least Squares Regression in R.” Journal of Statistical Software, 18, 2.

- Mills, (1927) Mills, F. (1927). “The Behaviour of Prices.” Tech. rep., National Bureau of Economic Research: New York.

- Nelsen, (1999) Nelsen, R. (1999). An Introduction to Copulas. New York: Springer–Verlag.

- Novo and Schafer, (2002) Novo, A. A. and Schafer, L. (2002). norm: Analysis of multivariate normal datasets with missing values. Ported to R by Alvaro A. Novo. Original by Joseph L. Schafer; R package version 1.0-9.

- Park and Casella, (2008) Park, T. and Casella, G. (2008). “The Bayesian Lasso.” Journal of the American Statistical Association, 103, 482, 681–686.

- Patton, (2006) Patton, A. J. (2006). “Estimation of Multivariate Models of Time Series of Possibly Different Lengths.” Journal of Applied Econometrics, 21, 147–173.

- Schafer, (1997) Schafer, J. (1997). Analysis of Incomplete Multivariate Data. Chapman & Hall/CRC.

- R Development Core Team, (2007) R Development Core Team (2007). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria. ISBN 3-900051-07-0.

- Sklar, (1957) Sklar, A. (1957). “Fonctions de répartition à dimensions et leurs marges.” Publications de l’Institut Statistique del l’Université de Paris, 8, 229–231.

- Stambaugh, (1997) Stambaugh, R. F. (1997). “Analyzing Investments Whose Histories Differ in Lengh.” Journal of Financial Economics, 45, 285–331.

- Stine, (2004) Stine, R. A. (2004). “Discussion of ‘Least Angle Regression’ by B. Efron, T. Hastie, I. Johnstone, and R. Tibshiran.” Annals of Statistics, 32, 2, 465–469.

- Venables and Ripley, (2002) Venables, W. N. and Ripley, B. D. (2002). Modern Applied Statistics with S. 4th ed. New York: Springer. ISBN 0-387-95457-0.

- West, (2003) West, M. (2003). “Bayesian factor regression models in the “large p, small n” paradigm.” Bayesian Statistics 7, 723–732.