Helmut Finnerlabel=e1]finner@ddz.uni-duesseldorf.de

[Thorsten Dickhauslabel=e2]dickhaus@ddz.uni-duesseldorf.de

[Markus Roterslabel=e3]Markus.Roters@omnicarecr.com

[

German Diabetes Center

Düsseldorf, German Diabetes Center Düsseldorfand Omnicare Clinical Research

H. Finner

T. Dickhaus

German Diabetes Center

at the Heinrich–Heine–Universität

Düsseldorf

Institute of Biometrics and Epidemiology

Düsseldorf

Germany

E-mail: e2

M. Roters

Omnicare Clinical Research

Biometrics Department

Köln

Germany

(2007; 4 2006; 9 2006)

Abstract

Some effort has been undertaken over the last decade to provide

conditions for the control of the false discovery rate by the linear

step-up procedure (LSU) for testing hypotheses when test statistics

are dependent. In this paper we investigate the expected error rate

(EER) and the false discovery rate (FDR) in some extreme parameter

configurations when tends to infinity for test statistics being

exchangeable under null hypotheses. All results are derived in terms of

-values. In a general setup we present a series of results concerning

the interrelation of Simes’ rejection curve and the (limiting)

empirical distribution function of the -values. Main objects under

investigation are largest (limiting) crossing points between these

functions, which play a key role in deriving explicit formulas for EER

and FDR. As specific examples we investigate equi-correlated normal and

-variables in more detail and compute the limiting EER and FDR

theoretically and numerically. A surprising limit behavior occurs if

these models tend to independence.

62J15,

62F05,

62F03,

60F99,

Exchangeable test statistics,

expected error rate,

false discovery rate,

Glivenko–Cantelli theorem,

largest crossing point,

least favorable

configurations,

multiple comparisons,

multiple test

procedure,

multivariate total positivity of order 2,

positive regression

dependency,

Simes’ test,

doi:

10.1214/009053607000000046

keywords:

[class=AMS]

.

keywords:

.

††volume: 35††issue: 4

\pdftitle

Dependency and false discovery rate: Asymptotics

AASupported by the Deutsche Forschungsgemeinschaft.

,

and

1 Introduction

Control of the false discovery rate (FDR) in multiple hypotheses

testing has become an attractive approach especially if a large number

of hypotheses is at hand. The first FDR controlling procedure, a linear

step-up procedure (LSU), was originally designed for independent

-values (cf. r1 ) and has its origins in r3 (cf. also

r15 ). Meanwhile, it is known that the LSU-procedure controls the

FDR even if the test statistics obey some special dependence structure.

Key words are MTP2 (multivariate total positivity of order 2) and

PRDS (positive regression dependency on subsets).

More formal descriptions of these conditions and proofs can be found in

r2 and r14 . In view of testing problems with some ten

thousand hypotheses as they appear, for example, in genetics,

asymptotic considerations become more and more popular. The first

asymptotic investigations concerning expected type I errors of the

LSU-procedure, as well as for the corresponding linear step-down (LSD)

procedure for the independent case, can be found in

r9 and r10 . A first theoretical comparison of classical

stepwise procedures controlling a multiple level [or

familywise error rate (FWER) in the strong sense] based on asymptotics

is given in r5 .

Moreover, attempts to improve the LSU-procedure and interesting

investigations based on asymptotics can be found, for example, in

r12 , r11 and r22 .

The LSU-procedure is based on the critical values , , introduced in r17 in a

different context. Based on ordered -values, the LSU-procedure rejects the corresponding

hypotheses , where . The corresponding LSD-procedure

rejects , where .

Since , the LSU-procedure may reject more hypotheses than

the LSD-procedure, never less. In this paper we restrict attention to

the LSU-procedure, which can be rewritten in terms of the empirical

c.d.f. (e.c.d.f.) (say) of the ’s. Setting , is rejected iff . The rejection curve

will be called the Simes-line. Note that . The threshold will be called the

largest crossing point (LCP) between the e.c.d.f. and the Simes-line and plays

a crucial role in this paper.

FDR control for a multiple test procedure is defined as follows. Let denote the number of falsely rejected null hypotheses and let denote the number of all rejections. Then the FDR (depending on

the underlying parameter configuration , say) is

defined by

and is said to be controlled at level if

The ratio is the false discovery proportion

(FDP).

In the case of independent -values both LSU and LSD control the FDR at

level ; more precisely, if is such that

exactly hypotheses are true and the remaining ones

are false, for both LSU and LSD, the actual FDR is bounded by . Under weak additional assumptions, we have in this setting

for the LSU-procedure

Different proofs for this fact can be found in

r1 , r9 , r14 and r22 .

In r10 the expected number of type I errors (ENE), that is,

, of LSU and LSD was

investigated for the case that all hypotheses are true and -values are

independent. In this case the limiting ENE for equals for LSU and for

LSD. Moreover, in r9 the expected type I error rate (EER)

defined by was

studied if a proportion of hypotheses is totally

false, that is, with -values equal to zero with probability . For

independent -values, it was shown in r9 under quite general

assumptions that for both LSU and LSD

The worst case for the EER appears if the proportion of true hypotheses

tends to , and, for small values of , the expected type

I error rate is then approximately .

In this paper we investigate the behavior of EER and FDR of the

LSU-procedure based on dependent test statistics if the number of

hypotheses tends to infinity. It will be assumed that test statistics

are exchangeable under the corresponding null hypotheses. The main

issue will be the calculation of the limiting values of the actual EER

and FDR in some extreme parameter configurations, where a proportion

of hypotheses will be assumed to be true and the remaining

hypotheses will be assumed to be totally false. These configurations

are least favorable for the EER, that is, EER becomes largest under

these configurations if is given.

Theoretical results on least/most favorable configurations for the FDR

(configurations where the FDR becomes largest/smallest) under

dependence remain a challenging open problem. However, simulations

indicate that extreme configurations ( hypotheses true,

hypotheses totally false) are first candidates for least favorable

configurations and therefore of special theoretical interest.

Until now, not many results are available concerning the behavior of

EER and FDR under dependence. A brief discussion on expected type I

errors for single-step procedures based on exchangeable test statistics

and range statistics can be found in r8 .

In Section 2 we develop a general theory for the computation

of the limiting EER and FDR assuming that exchangeable test statistics

of the type are at hand. The results heavily

depend on the limit behavior of the e.c.d.f. of the underlying -values

given the value of the disturbance variable . Generally, the

limiting e.c.d.f. (say) of dependent -values differs

substantially from that of independent -values. Formulas for the

limiting e.c.d.f. and crossing point determination are summarized in

Lemma 2.1. For , limiting

and are computed in Theorems

1 and 3 in terms of the set of largest crossing

points (LCP’s) between and the Simes-line. The case is more complex because limiting LCP’s can be zero. For

the latter case, we derive some important technical results for the FDR

in Lemmas 4 and 5 supposing that the c.d.f. of a

proportion of -values is linear in a neighborhood of zero.

The limiting and are then

computed in Theorems 6 and 8. Moreover, we give an

example where the FDR is exactly the same as in the independent case.

By utilizing the results of Section 2, we investigate

equi-correlated normal variables in Section 3 and jointly

studentized -statistics in Section 4. The corresponding

formulas for the limiting and

are given in Theorems 9 and 10 and Theorems

13 and 14, respectively. A surprising behavior of the

FDR occurs if these models tend to independence and the proportion of

false hypotheses tends to ; see Theorem 12 and Theorem

16. Some figures in Sections 3 and 4

illustrate the limiting behavior of EER and FDR. The numerical and

computational effort for these graphs was enormous. A few concluding

remarks are given in Section 5. Short proofs are in the main

text, while more technical proofs are deferred to the

Appendix.

2 Exchangeable test statistics: general considerations

We first consider the following basic model with exchangeable test

statistics. Let , be real-valued independent

random variables with support . Moreover, let be a

further real-valued random variable, independent of the ’s, with

support and continuous c.d.f. . Denote the c.d.f.

of by .

Suppose the c.d.f. depends on a parameter , where is known. Without loss

of generality, it will be assumed that . Consider the

multiple testing problem

Suppose that (with support ) is a

suitable real-valued test statistic for testing such that tends to larger values if increases. In

Section 3 we consider statistics of the type and in Section 4 ; see Examples 2.1 and 2.2 below. The

sets , and are assumed to be

intervals. For convenience, we assume in this section that is

continuous, strictly increasing in the first and either strictly

monotone or constant in the second argument. Moreover, let

denote the inverse of with respect to the first argument of , that is, . If

is strictly monotone in the second argument, we denote the inverse of with respect to the second argument by , that is, .

In the case that is true, the c.d.f. of () will

be denoted by () and is assumed to be

continuous. For , we define -values as a

function of by

(1)

The ordered -values are given by . Under, the e.c.d.f.

of the -values is denoted by .

Remark 2.1.

It is important to note that, given , the -values ,

, can be regarded (a) as conditionally independent

random variables with values in ,

or, (b) under , as realizations of conditionally i.i.d. random

variables with a common c.d.f. (say). In the

latter case, given , it holds that in the sense of the Glivenko–Cantelli theorem. Therefore, we

refer to as the limiting e.c.d.f. [of the -values

]. In view of (1), we get , hence, since is

assumed to be continuous,

(2)

For the sake of simplicity, it will be assumed that the model implies

that is continuous in and

differentiable from the right at with for all .

In the case that a proportion of hypotheses is

true and the rest is false, that is, hypotheses are true and hypotheses are false, we make the following additional

assumption in order to avoid laborious limiting considerations as under . It will be assumed that

under an alternative , the parameter

value is possible. Moreover, for , it will be assumed that the -value has a Dirac

distribution with point mass in . We refer to this situation as the

D-EX model. As briefly mentioned in the introduction, under

suitable assumptions, EER becomes and FDR seems to become largest if for all with .

In order to calculate upper bounds for EER and FDR, we therefore

restrict attention to the D-EX model which rarely (never)

appears in practical applications.

If one is interested in EER and FDR under other parameter

configurations, one may put a prior on the ’s under

alternatives , which results in a mixture model as considered, for

example, in r12 or r22 . This makes things slightly more

complex and will not be considered in this paper. In the

D-EX model, the e.c.d.f. of the -values will be denoted by

.

The following two examples fit in the D-EX model and will be

studied in more detail in Sections 3 and 4,

respectively.

Example 2.1.

Let , , be independent

standard normal random variables and let with , , where is assumed to be known

and .

Then is multivariate normally distributed

with mean vector ,

for , and for .

Consider the multiple testing problem

versus , .

This setup includes the well-known many-one multiple comparisons

problem with underlying balanced design.

For , the distribution of is MTP2 so that the

Benjamini–Hochberg bound applies; cf. r2 or r14 . Note

that is replaced by and , where denotes the c.d.f. of the standard normal distribution. Suitable

-values for testing the ’s are given by ,

. Again, we add to the

model such that a.s. if , .

We denote this D-EX model by D-EX-N.

Example 2.2.

Let , ,

be independent normal random variables and let be independent of the ’s. Without loss of

generality, we assume and the c.d.f. of will be denoted by . Again we consider the multiple

testing problem versus , . Let , .

Then has a multivariate equi-correlated

-distribution. The c.d.f. (p.d.f.) of a univariate (central)

-distribution will be denoted by () and a -quantile of the -distribution will be denoted by

. Here is replaced by , , and . Suitable -values (as a function of

) are defined by . Again

we add to the model such that a.s.

if .

We denote the corresponding D-EX model by D-EX-t.

It is outlined in r2 by employing PRDS arguments that the

Benjamini–Hochberg bound applies in this model for .

The following obvious lemma gives explicit expressions for

(as a consequence of the Glivenko–Cantelli theorem, cf. (2) in

Remark 2.1) and characterizes crossings with the Simes-line in

the D-EX model.

Lemma 2.1

Given D-EX with , the limiting e.c.d.f. of the -values is given by

Moreover, crosses (or contacts) the Simes-line, that is, for some iff

. If is strictly decreasing in for all and if for some , then

Note that . Analogously, we

set .

Figure 1: The Simes-line for and two

realizations of the e.c.d.f. together with in the D-EX-N model for , , and (left picture with

), (right picture with ).

Figure 1 illustrates the enormous impact of

the disturbance variable and a large correlation in the

D-EX-N model on the LCP determining the number of

rejections. In this example, for only the (totally) false

hypotheses are rejected, while for we obtain false

rejections.

Remark 2.2.

Under the assumptions of Lemma 2.1, the Glivenko–Cantelli theorem yields

Moreover,

For , define

(3)

If there exists an such that for all

and for all , then will be

called the largest crossing point (LCP) of and the Simes-line. The set of LCP’s will be denoted by . Moreover, set . Note that there may be some tangent points

(TP’s) defined by (3) with in a neighborhood of . However,

it will be assumed that . In practical examples, is a finite union of intervals. For , we

always have a well defined LCP or TP . For , the LCP may be for a large set of

-values, which makes the calculation of the limiting EER and FDR

subtler.

In the following we make use of the notation

and the corresponding expressions for EER. Moreover, the notation

, will be used if is given.

2.1 All LCP’s greater than zero

We first consider the case .

Theorem 1.

Given D-EX with , for all

(4)

(5)

{pf}

With a similar technique as in the proof of Lemma A.2 in r9 , it

can be shown that the proportion of rejected hypotheses converges almost surely to . This fact

immediately implies (4) and (5).

In view of the general assumption , can be

replaced by in (4) and (5).

It remains to calculate

and

.

This may be done in two ways. The first is to integrate (4) and

(5) with respect to . In this case the main problem is

the computation of , which can be cumbersome. In

general, cannot be determined explicitly.

The second possibility seems more convenient and is summarized in the

following theorem.

Theorem 3.

Under the assumptions of Theorem 1, suppose that is strictly decreasing in for . Let , and denote the c.d.f.

of and by and ,

respectively. Then

which is (8).

Similarly, we obtain from (5) in Theorem 1 that

Therefore, similar arguments as before yield that

is given by (9).

The latter result is a key step for the computation of

and

. In practical examples it remains

to determine the sets and and to evaluate

the corresponding integrals.

2.2 Some LCP’s equal to zero

If an LCP is equal to zero, the behavior of the FDR heavily depends on

the gradient in zero of the c.d.f. of the -value distribution. The

next two lemmas cover the finite case.

Lemma 4.

Let , , , and let be i.i.d.

random variables with values in with c.d.f. satisfying

for all . Furthermore, let

be random variables with values in , independent of . For , , define and (with for ). Then

(10)

{pf}

For , denote the -dimensional random vector

by ,

define for the sets

and set , .

Then the left-hand side of (10) (cf., e.g., Lemma 3.2 and

formula (4.4) in r14 ) is equal to

Noting that for all and

for all , the assertion follows immediately.

As an application of Lemma 4, we insert a surprising

example.

Example 2.1.

Under the general framework of this section, suppose the follow

an exponential distribution with scale parameter and

location parameter and follows an exponential

distribution with scale parameter and location parameter

, and consider the model , . Under , the c.d.f. of is

given by

for and for

, while the -values (as functions of the observed -value)

are given by , . This

results in

with . For convenience, we restrict attention to

the case . In order to apply Lemma 4, set

and note that has c.d.f. if is true. Therefore, supposing that hypotheses are

true and are false with fixed but arbitrary , we obtain with and that Integrating with respect to

finally results in

It may be astonishing that the Benjamini–Hochberg upper bound for the

FDR is attained for all parameter configurations although the ’s

are dependent. Notice that the property holds in this

setting so that the Benjamini–Hochberg bound for the FDR applies. This

is a consequence of Propositions 3.7 and 3.8 in karlnott-1980 ,

because the p.d.f. of the distribution is

for any ; see karlin-1968 , page 30.

The next result extends Lemma 4 and is a helpful tool in

the case that LCP’s are in .

Lemma 5.

Under the assumptions of Lemma 4 but only

supposing that for all for some

, let , where denotes the e.c.d.f. of . Then, setting ,

(11)

{pf}

It is clear that ; hence, for , the

left-hand side of (11) is now equal to

The assertion follows similarly as in the proof of Lemma 4.

The following theorem, the proof of which is in the

Appendix, is an important step for the understanding of

the limiting behavior of both EER (or ENE) and FDR given a fixed value

such that the LCP is in .

Theorem 6.

Given D-EX with , let be such that for all . Setting it holds that

(12)

(13)

Remark 7.

In r10 the distribution and expectation of were computed

for uniform -values under the assumption that all hypotheses are true.

Assuming for all , the nesting method

in the proof of (13) together with the technique in r10

can be used to prove

It is important to note that this formula is only valid for . If tends to infinity with and , then .

To complete the picture for , the next theorem puts things

together.

Theorem 8.

Given D-EX with , suppose

that is strictly decreasing in for .

Moreover, let and be defined as in

Theorem 3 and let and . Then

(14)

(15)

{pf}

Using the disjoint decomposition , we obtain

Now, Theorem 6 immediately yields , and in analogy

to the arguments in the proof of Theorem 3, we get that

. Therefore,

(14) is proven. Applying the same decomposition (together with

Theorem 6) to and observing

that if

[similar to (5) with ] finally

proves (15).

3 Exchangeable normal variables (Example 2.1 continued)

In the D-EX-N model, assuming that the proportion of true null hypotheses tends to 1, we obtain from Lemma 2.1

that the limiting e.c.d.f. of the ’s given is

given by

and . Note

that , where denotes a standard normal variate and denotesthe corresponding -quantile. Moreover, it

is , and is convex for and concave for . Furthermore, is strictly

decreasing in for and

.

Assuming that , the

limiting e.c.d.f. is given by

Hence, for and given ,

iff

(16)

For , we get and . Moreover, starts

above the Simes-line so that there is at least one CP in . In

fact, there may be one, two or three points of intersection in . For , we get in contrast to that .

The limiting e.c.d.f. starting with may have no, one or two CP’s

in .

In order to determine the set of LCP’s, the following derivations are

helpful. Let and let

(17)

denote the distance between the transformed -curve and the

transformed Simes-line. Then the conditions

(18)

(19)

are necessary and sufficient for a TP ( touches the Simes-line).

Note that condition (19) is equivalent to

(20)

If there exists a real solution of (18) and

for given values of , then we define .

If such a solution exists in case of ,

define as the smaller solution of . Then the set of LCP’s is given by .

Note that for there exists a unique TP such that the set

of LCP’s is given by .

Furthermore, for , there may be no such TP. In the

latter case, formally interpreted as , we have .

For example, such a situation occurs in the case and iff for .

The (discontinuous) case looks somewhat paradoxical. In

this case, depending on the observed , either a small proportion

or a larger proportion of hypotheses will be rejected although

the distance between the corresponding values may be small. This

occurs, for example, for , .

The following two theorems give formulas for and . The first

theorem covers , the second one . The proof

of Theorem 9 can be found in the Appendix,

while the proof of Theorem 10 is a straightforward

application of Theorem 8.

Theorem 9.

Given model D-EX-N with , the set of LCP’s is for and for (i.e., no TP) and

where , .

Theorem 10.

Given model D-EX-N with , the set of LCP’s is

and

Remark 11.

For , we obtain an upper bound for and

, respectively, if .

From the derivations before Theorem 9, we get and consequently, .

This is helpful for the numerical determination of .

The following interesting and maybe unexpected result, which will be

discussed in Section 5, concerns a discontinuity for and . The proof is given in the Appendix.

Theorem 12.

Given model D-EX-N with and ,

(21)

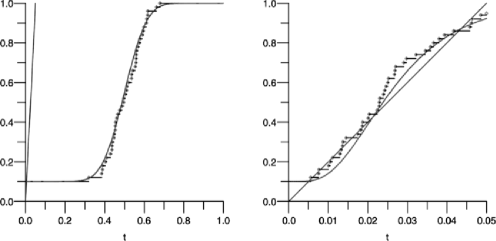

Figure 2: in the

D-EX-N model for and (left picture) and (right

picture).Figure 3: in the

D-EX-N model for and (left picture) and

(right picture).

Figures 2 and 3 display and , respectively, for various values of for . For ,

tends to as expected

(cf. r9 ) and for , tends to . Moreover, it seems that is increasing in with

largest values for large and . If is not too large

(), is largest for

. For , FDR tends to the

Benjamini–Hochberg bound for and . For , we have total dependence so that in the D-EX-N model. For large values of , the computation of is

extremely cumbersome. The main reason is that the TP’s are very close

to 0 so that an enormous numerical accuracy is required.

Finally, it is interesting to note that for , reflects the limiting behavior of the

true level of Simes’ r17 global test for the intersection

hypothesis. Our results imply that this global test has an asymptotic

level greater than zero for all correlations , which is a

new finding.

4 Studentized normal variables (Example 2.2

continued)

In the D-EX-t model with , is given by

Note that is decreasing in for and

increasing in for .

Moreover, hence, we get .

Moreover,

This condition is equivalent to

Hence, for , is convex for with and concave otherwise. For , is convex for and

concave otherwise. Notice that for all

. As a consequence, for , crosses the

Simes-line at most if , which happens if

.

Given the D-EX-t model with , the limiting e.c.d.f. is given by

For convenience, we restrict attention to in the

remainder of this section. For , we have iff

where iff . Therefore,

LCP’s are only possible in with

and . Notice that for ,

while and for . For , the set of LCP’s consists of one or two

intervals denoted by and . If there exists a TP we have

and the TP is ; otherwise . In the case the

existence of a TP (denoted by ) is guaranteed and the set of LCP’s

is given by . Hence, the situation

is quite similar to the D-EX-N model in Section 3

except that there are no crossing points at all in . With

, the distance function between and the Simes-line is defined by Necessary

and sufficient conditions for a TP ( touches the Simes-line)

are now given by

which are equivalent to and .

We summarize the behavior of EER and FDR in the following two theorems

in analogy to the results of Section 3.

Theorem 13.

Given model D-EX-t with and , the set of LCP’s is

for and for (i.e., no TP) and

where , , and .

Theorem 14.

Given model D-EX-t with and , the set of LCP’s is and

Finally, for , we consider the case that the degrees of

freedom tend to infinity. Heuristically, this means that the

model tends to independence.

In contrast to the normal case of the previous section, the solution is

more difficult. The reason is that one has to find suitable asymptotic

expansions for and given in r4fd .

Application of these expansions yields the following result, the proof

of which is given in the Appendix.

Lemma 15.

Let and define

Then, given model D-EX-t with , it holds for sufficiently large that has (i) two CP’s for all , and

(ii) no CP for all .

Application of this lemma yields the same limit of the FDR for and as in Theorem 12; cf. the

discussion in Section 5.

Theorem 16.

Let . Then, given model D-EX-t with,

(22)

{pf}

The result follows by letting in Lemma 15 and

by applying the central limit theorem. Setting , we get

\upqed

Figure 4: in the

D-EX-t model for and

(left picture) and

(right picture).

In analogy to Section 3, Figures 4 and

5 display and , respectively, for various values

of and . It seems that is decreasing in . For , again tends to the value as expected; see r9 .

Note that is already close to

this limit if is not too small. As expected, for and not too small, is largest. Except for ,

the FDR tends to the Benjamini–Hochberg bound for

increasing degrees of freedom. The limit for is not clear.

In the latter case the density of the -distribution becomes flatter

and flatter and the computation of becomes extremely difficult. As in the D-EX-N model with

, reflects the

limiting behavior of the true level of Simes’ r17 global test

for the intersection hypothesis and again, our results show

that it is asymptotically greater than zero for all .

Figure 5: in the

D-EX-t model for and

(left picture) and

(right picture).

5 Concluding remarks

The investigations in this paper show that the false discovery

proportion FDP of the LSU-procedure can be very

volatile in the case of dependent -values, that is, the actual FDP may be

much larger (or smaller) than in the independent case. The same is true

for , , and . Under mild assumptions, the

e.c.d.f. of the -values converges to a fixed curve under independence

(cf. r9 ), which implies convergence of and

to fixed values. On the other hand, the shape of the e.c.d.f. of the

-values under exchangeability heavily depends on the (realization of

the) disturbance variable ; cf. Figure 1.

In the latter case, the limit distribution of and typically has positive variance.

It is often assumed that there may be some kind of weak dependence

between test statistics (cf., e.g., r22 ), being close to

independence in some sense. The results in Theorems 12 and

16 and the numerical calculations reflected in Figures

3 and 5 suggest that for large and

small deviations from independence (small

or large ) may result in a substantially smaller FDR than the

Benjamini–Hochberg bound.

However, simulations for small and large show that

approaches its limit

only for unrealistically large

values of if . For example, in the

D-EX-N model with , and , we obtained by

simulation. For , we got .

A possible explanation may be that , , hence, the order of limits plays a

severe role. Moreover, for small , it seems that has to be

very large such that the e.c.d.f. reproduces the shape of

close to .

For , the curves in Figures

3 and 5 reflect the FDR for realistically

large (e.g., ) very well. The reason is that the shape

behavior of close to is not that crucial as for .

Example 2.1 shows that the FDR under dependence may also

have the same behavior as in the independent case. Therefore, it seems

very difficult to predict what happens with EER, FDR and FDP in models

with more complicated dependence structure, for example, in a multivariate

normal model with arbitrary covariance matrix. In any case, results of

the LSU-procedure, or more generally, of any FDR controlling procedure,

should be interpreted with some care under dependence, taking into

account that the FDR refers to an expectation and that the procedure at

hand may lead to much more false discoveries than expected.

In the models studied in Sections 3 and 4, the EER

becomes smallest if for all and tends to , where . It is not clear for which parameters

the FDR becomes smallest. However, if for all , , the FDR tends to .

Finally, with slight modifications of the methods developed in this

paper, one can also treat statistics like or

. Somewhat more effort will be necessary if the

disturbance variable is two-dimensional as, for example, in .

Appendix: Proofs

{pf*}

Proof of Theorem 6

The assumptions concerning imply that

almost surely.

Noting that for all ,

(12) is obvious.

In order to prove (13), we nest between two

c.d.f.’s being linear in a neighborhood of zero. To this end, let be fixed, , , , and

This results in for all .

For ,

let the event be defined as in Lemma 5.

Then

With , we

obtain similarly to the arguments in the proof of Lemma

4 that

Due to the pointwise order of , and , we get

Since , and

for , we obtain and . The assertion now follows

by noticing that .

{pf*}

Proof of Theorem 9

Denote the p.d.f. corresponding to by

and notice that . From Theorem 3, we get

Since and , we get

In order to compute , note that, for

,

where , . In view

of , it is

,

and . Denoting the corresponding p.d.f. of

by , we obtain

\upqed

{pf*}

Proof of Theorem 12

For any , there exists a unique solution

(say) of (18) and

(19).

In view of (20) and the shape of , satisfies

(23)

Notice that implies and

therefore, .

Now, for , we consider in

order to bound from below for . Since

has to be a real number, we obtain from (23) that

.

Defining

we get from (17) that Hence, iff . Employing the asymptotic relationship for Mills’ ratio, we get

Since independent of and , we conclude that . This finally implies

(21) and completes the proof.

{pf*}

Proof of Lemma 15

For , the unique point of inflection of

on is given by with . Hence, it

suffices to show that

for sufficiently large and that the derivative of in is less than for all for sufficiently large .

Therefore, the assertion follows if

We easily get .

As a consequence, (24) follows by noting that

An analogous calculation yields (25). Hence, Lemma

15 is proved.

Acknowledgments

The authors are grateful to a referee and an Associate Editor for their

constructive and valuable suggestions and their quick replies. Thanks

are also due to the editor M. L. Eaton for his expeditious handling

of the manuscript.

References

(1)Benjamini, Y. and Hochberg, Y. (1995). Controlling

the false discovery rate: A practical and powerful approach to multiple

testing. J. Roy. Statist. Soc. Ser. B 57

289–300.

\MR1325392

(2)Benjamini, Y. and Yekutieli, D. (2001).

The control of the false discovery rate in multiple testing under dependency.

Ann. Statist.29 1165–1188.

\MR1869245

(3)Eklund, G. and Seeger, P. (1965).

Massignifikansanalys.

Statistisk Tidskrift Stockholm3 355–365.

(4)Finner, H., Dickhaus, T. and Roters, M. (2008).

Asymptotic tail properties of Student’s -distribution.

Comm. Statist. Theory Methods37. To appear.

(5)Finner, H. and Roters, M. (1998).

Asymptotic comparison of step-down and step-up

multiple test procedures based on exchangeable test statistics.

Ann. Statist.26 505–524.

\MR1626043

(6)Finner, H. and Roters, M. (2001). Asymptotic

sharpness of product-type inequalities for maxima of random variables

with applications in multiple comparisons. J. Statist. Plann.

Inference98 39–56.

\MR1860224

(7)Finner, H. and Roters, M. (2001). On the false

discovery rate

and expected number of type I errors. Biom. J.43 985–1005.

\MR1878272

(8)Finner, H. and Roters, M. (2002).

Multiple hypotheses testing and expected number of type I errors.

Ann. Statist.30 220–238.

\MR1892662

(9)Genovese, C. R. and Wasserman, L. (2002). Operating

characteristics and extensions of the false discovery rate procedure.

J. R. Stat. Soc. Ser. B Stat. Methodol.64

499–517.

\MR1924303

(10)Genovese, C. R. and Wasserman, L. (2004).

A stochastic process approach to false discovery control.

Ann. Statist.32 1035–1061.

\MR2065197

(11)Karlin, S. (1968).

Total Positivity1. Stanford Univ. Press.

\MR0230102

(12)Karlin, S. and Rinott, Y. (1980). Classes of

orderings of

measures and related correlation inequalities. I. Multivariate totally

positive distributions. J. Multivariate Anal.10

467–498.

\MR0599685

(13)Sarkar, S. K. (2002). Some results on false discovery rate in

stepwise multiple testing procedures. Ann. Statist.30 239–257.

\MR1892663

(14)Seeger, P. (1966). Variance Analysis of Complete

Designs. Some

Practical Aspects. Almqvist and Wiksell, Uppsala.

\MR0223020

(15)Simes, R. J. (1986). An improved Bonferroni procedure for

multiple tests of significance. Biometrika73

751–754.

\MR0897872

(16)Storey, J. D., Taylor, J. E. and Siegmund, D. (2004).

Strong control, conservative point estimation and simultaneous

conservative consistency of false discovery rates: A unified approach.

J. R. Stat. Soc. Ser. B Stat. Methodol.66

187–205.

\MR2035766