(Date: First version December 15th, 2006, last revision )

Abstract.

A mathematical framework for Continuous Time Finance based on

operator algebraic methods offers a new direct and entirely

constructive perspective on the field. It also leads to new

numerical analysis techniques which can take advantage of the

emerging massively parallel GPU architectures which are uniquely

suited to execute large matrix manipulations.

This is partly a review paper as it covers and expands on the

mathematical framework underlying a series of more applied articles.

In addition, this article also presents a few key new theorems that

make the treatment self-contained. Stochastic processes

with continuous time and continuous space variables are defined

constructively by establishing new convergence estimates for Markov

chains on simplicial sequences. We emphasize high precision

computability by numerical linear algebra methods as opposed to the

ability of arriving to analytically closed form expressions in terms

of special functions. Path dependent processes adapted to a given

Markov filtration are associated to an operator algebra. If this

algebra is commutative, the corresponding process is named Abelian,

a concept which provides a far reaching extension of the notion of

stochastic integral. We recover the classic

Cameron-Dyson-Feynman-Girsanov-Ito-Kac-Martin theorem as a

particular case of a broadly general block-diagonalization

algorithm. This technique has many applications ranging from the

problem of pricing cliquets to target-redemption-notes and

volatility derivatives. Non-Abelian processes are also relevant and

appear in several important applications to for instance snowballs

and soft calls. We show that in these cases one can effectively use

block-factorization algorithms. Finally, we discuss the method of

dynamic conditioning that allows one to dynamically correlate over

possibly even hundreds of processes in a numerically noiseless

framework while preserving marginal distributions.

I would like to thank my collaborators in the past 8 years

with whom this work would not have been possible. In particular

Joseph Campolieti, Peter Carr, Oliver Chen, Alexei Kuznetsov,

Sebastian Jaimungal, Paul Jones, Harry Lo, Stephan Lawi, Alex

Lipton, Alex Mijatovic, Adel Osseiran, Dmitri Rubisov, Stathis

Tompaidis, Manlio Trovato and Alicia Vidler. Special thanks go to

Paul Jones and Adel Osseiran for reading previous versions of this

manuscript and correcting errors. All remaining mistakes are the

solve responsibility of the author.

1. Introduction

The goal of this paper is to attempt to consolidate and present a

number of mathematical methods developed over several years by

myself and collaborators while addressing concrete problems in

derivative pricing theory. The results scattered across a number of

papers which are collected here have been complemented with a

rigorous ab initio treatment and a few key theorems which make

the framework mathematically self-contained. This results in a quite

comprehensive approach to the theory of Stochastic Processes and

Mathematical Finance which is novel in that it is fully constructive

and perhaps has applications beyond the realm of Financial

Engineering.

There are several traditions of Constructive Mathematics. One

attempts to re-derive classical results of real and functional

analysis based on a restrictive constructivist logic according to

which no mathematical object can be considered unless one specifies

explicitly how to construct it, see [BR1987] and

[Bishop1967]. Along another tradition, Constructive Field

Theory, see [GJ1987], aimed at establishing the existence of

interacting quantum field theories by providing a constructive

procedure for computing -point functions and demonstrating that

they satisfy a set of axioms. Measure theoretic probability and the

related theory of stochastic processes, [Doob1953], does not

seem to be understandable constructively. The PDE approach in

[Feller] and the harmonic analysis approach in

[Bochner1987] are instead essentially constructive but do not

delve into the theory of stochastic integrals and path dependent

processes and into lattice discretization schemes.

The main motivation that guided this research is the creation of an

engineering framework for exotic financial derivatives. Efficient

computability on current hardware has been and remains throughout

this article our key motivating concern. To this end, we work

towards an algebraization of Probability Theory that reduces all

calculations to matrix manipulations which can be performed

efficiently and in particular to matrix multiplications. Similarly

to the standard framework of algebraic topology, [Spanier1966],

we consider processes taking values in separable topological spaces

and approximate continuous domains by means of simplicial sequences.

To establish convergence in the continuous limit, we directly

estimate convergence rates for probability transition kernels in the

continuous space limit following an approach similar in spirit to

Constructive Lattice Field Theory, see [GJ1987]. Similarly to

constructive field theory, sets of axioms on -point functions are

used to identify processes and renormalization group transformations

are used to control the continuous limit. Following

[Naimark1959], the approach is grounded upon the algebraic

theory of integration on locally compact Hausdorff separable

topological spaces.

Calculations with stochastic processes are carried out using

operator methods developed in Quantum Mechanics,

[LandauLifshits] and systematized in Mathematical Physics

references such as [ReedSimon]. In Finance, operator methods

have been developed along two independent and

non-overlapping streams of research, one by Ait-Sahalia,

Hansen and Scheinkman who focused on econometric estimations in a

series of papers reviewed in [AHS2005], see also

[Ait-Sahalia96], [HST98], [HS95]. The second stream

of research is by the author and collaborators who instead worked on

derivative pricing for path dependent and correlation derivatives,

see [ACDV], [AChen4], [AChen5], [AKusnetsov5],

[AL2004], [ALoMijatovic], [ATrovato3],

[ATrovato2], [AVidler], [AJones] and

[AOsseiran]. In this paper, we attempt to systematize the

mathematical framework of pricing theory in the operator formalism

from our own viewpoint, reserving to future work the task of

pursuing overlaps with the econometric literature.

The references quoted above are all relevant to our undertaking and

provided motivations on many levels. However, in an effort to keep

this writing self-contained, we are not going to assume any previous

knowledge of the reader.

To ground the mathematical framework, we obtain sharp pointwise

convergence estimates for probability kernels and its derivatives.

More precisely, we show that probability kernels converge pointwise

at rates of order , where is the lattice spacing. The

result applies to a large class of diffusion processes and

extensions thereof including smooth space inhomogeneities, regime

switching, finite activity jumps and some degree of time

inhomogeneities. We also prove similar convergence results for the

fast exponentiation method, our preferred numerical method for

exponentiating Markov generators, showing that errors in this scheme

are also of order , in the sense of pointwise convergence

for the probability kernel. In the particular case of Brownian

motion, we show that similar pointwise error estimates

apply also to derivatives of the probability kernels and that

the power 2 in the bounds is actually sharp.

The interest in convergence estimates was prompted by the desire of

understanding the mechanisms behind the empirically observed

smoothness and robustness in the calculation of price sensitivities

with the methods in our applied papers. We also observed empirically

that the fast exponentiation algorithm is stable under single

precision floating point arithmetics. We find that key to a high

precision numerical framework for sensitivities is handling the time

coordinate either as continuous or very finely discretized. A

sufficiently fine discretization is defined as one for which

explicit differentiation schemes are stable and typically correspond

to a hourly time scale in applications. Typically, weekly time steps

would permit stable implicit differentiation schemes but would not

allow for as much stability in the calculation of price

sensitivities and the probability kernels we require to evaluate and

manipulate. This motivates us to avoid implicit differentiation

schemes on coarse time intervals.

Measure changes and time changes are defined constructively and a

version of the Fundamental Theorem of Finance is re-obtained. The

Cameron-Martin-Girsanov’s theorem, see [CameronMartin], and

Ito’s lemma, see [Ito1951], are proved twice in different ways

with operator methods. We also derive the Feynman-Kac formula, see

[Feynman1948] and [Kac1950]. One of the key results is an

extension of the Feynman-Kac-Ito formula in three different

directions. This formula concerns the characteristic function of a

stochastic integral over a diffusion process. In our formalism, this

formula becomes a block-diagonalization algorithm for large matrices

associated to path-dependent processes. The extension we discuss (i)

covers Markov processes more general than diffusions, (ii) allows

for a class of path-dependent processes we name Abelian which

extends the notion of stochastic integral and (iii) generalizes the

harmonic analysis framework to include extensions of trigonometric

Fourier transforms. The theory of Abelian processes finds numerous

practical applications to path dependent options and is applicable

to the great majority of path-dependent payoffs, from volatility

swaps to cliquets, range accruals, lookback options, target

redemption notes and more. We also give a version of Dyson’s formula

to accelerate the pricing of path-dependent options given by Abelian

processes by means of a moment expansion. Non-Abelian processes are

more difficult to handle but we single out a class admitting

block-factorizations (as opposed to a block-diagonalizing

transformation) and which are also amenable to numerical analysis by

matrix algebra. Finally, we illustrate the method of dynamic

conditioning that allows one to correlate possibly numerous

processes by means of kernel manipulations while preserving

marginals and not incurring into dimensional explosion.

The mathematical methods in this article are particularly efficient

as they lend themselves to transparent hardware acceleration on the

emerging multi-core GPU hardware platforms. These massively parallel

architectures are based on low-cost technologies that have been

developed for the games and high definition markets and are uniquely

suited to implement BLAS Level 3 routines such as matrix-matrix

multiplications with high efficiency. See also [GotoGeijn] for

a state of the art account on matrix-matrix multiplication software

on CPUs.

The paper is organized as follows. In Section 2, we introduce the

notion of simplicial sequence which is key to devising approximation

schemes for continuous valued process by means of a sequence of

Markov chains. In Section 3, we consider a general definition of

path functional and in Section 4 we give a general description of a

stochastic process by means of an -point function. Markov

Processes are introduced in Section 5, martingales and monotonic

processes in Section 6. In Section 7, we derive the Fundamental

Theorem of Arbitrage Free Pricing Theory. The classical results on

weak convergence of Markov generators by Bernstein, Bochner,

Kyntchine and Levy are re-obtained in Section 8. Time homogeneous

Markov Processes, fast exponentiation and spectral methods are

described in Section 9. In Section 10, we carry out a constructive

analysis of Brownian motion and prove convergence estimates. In

Section 11, we study the spectrum of diffusion generators. Sharp

pointwise kernel estimates are extended to general diffusion

processes in Section 12. In Section 13, we give estimates for the

convergence rate of time discretisation schemes of the type we

advocate for applications, i.e. based on fast exponentiation.

Section 14 reviews the derivation of hypergeometric Brownian motion

and particular cases such as the CEV model. In Section 15, we study

stochastic integrals and obtain Ito’s formula for diffusion

processes and of Girsanov’s theorem. Section 16 contains a

derivation of the Feynman-Kac formula for bridges over general

Markov processes. The general notion of Abelian process in

continuous time is introduced in Section 17. In Section 18, we

discuss the discrete time case. In this section, we introduce also

the notion of non-resonant block-diagonalisation scheme which

provides a numerically useful extension of Fourier analysis based on

trigonometric functions. Dyson’s formula and moment expansions are

in Section 19, covering the uni-variate case, and Section 20,

covering the multivariate case. These two sections include

applications to exotic volatility derivatives. Block factorizations

and applications to snowballs and soft calls are in Section 21.

Dynamic conditioning and multi-factor correlation modeling is

discussed in Section 22. Conclusions end the paper.

2. Measure Theory on Simplicial Sequences

Let be an integer, consider the space and the

sequence of lattices where .

Definition 1.

(Lattices.)

If , the convex hull of in is

denoted by . The interior of is denoted with and is defined as the set of

all sites contained in along with each one its

neighbors in at distance .

Definition 2.

(Simplicial Sequences.)

A bounded simplicial sequence is given by an integer ,

and a sequence of subsets defined for all

such that

•

whenever .

•

for all and all internal points there is a and an such that, for

all and for all with we have that .

We follow a constructivist logic paradigm according to which in

order to identify a set or a sequence of sets one has to explicitly

state how to construct it, possibly with a recursive algorithm, and

it must be possible to decide each step of the recursion in a finite

number of logical steps.

Definition 3.

(Lattice Functions.)

Let , be a bounded simplicial sequence. A real valued simplicial function, denoted by , is

defined as a sequence of functions such that

for all and all . The function is said uniformly

bounded if there is a constant such that for all . The function is uniformly continuous if it is uniformly bounded and

for all there is a such that if and we have that .

Definition 4.

(Equivalence of Lattice Functions.)

Let , , be a bounded simplicial sequence and and are two uniformly continuous real valued

functions on . We say that these series provide equivalent

representations of the same function in case, for all and all

all we have that .

Let be the set of all continuous functions on

endowed with the natural structure of algebra given by the

operations of sum, multiplication by a scalar and pointwise

multiplication.

Definition 5.

(Integrals.)

Let , , be a bounded simplicial sequence. An

integral is given by a sequence where is a

linear functional on the linear space of functions such that

•

whenever for all .

•

The following limit exists for all continuous functions :

(2.1)

•

The functionals defined above satisfies the following bound:

(2.2)

for some constant and all functions .

An integral is said to correspond to a probability measure if

.

Definition 6.

(Equivalent Integrals.)

Let , , be a bounded simplicial sequence and

let and be two integrals. We say that these series

provide equivalent representations of the same integral if

for

all uniformly continuous functions .

Given an integral on the simplicial sequence , for all

, one defines the following semi-norm on the space of

continuous functions :

(2.3)

Let be the linear space obtained by completing

with respect to the semi-norm and identifying equivalence classes of

functions at zero distance. More precisely, is the

linear space of the Cauchy sequences in

with respect to the norm modulo

the linear space of the Cauchy sequences converging to a limit of

zero -norm.

Definition 7.

(Summable Functions.)

A function is called summable if it is in and square

summable if it is in .

Theorem 1.

(Monotonic Sequences.)

Let be a non-decreasing sequence of summable

functions and consider the function and

the limit . Then either or is summable and .

Proof.

If , then whenever we have that . Since the sequence

is uniformly increasing, it is Cauchy. Hence the sequence

is Cauchy in . Its limit therefore belongs to

since this space is complete.

∎

Definition 8.

(Measurable Functions.)

A function is called measurable if it can be represented as the

limit of a non-decreasing sequence of summable functions.

Theorem 2.

(Dominated Convergence.) Let be a sequence of measurable

functions, suppose there is a summable function such that

and suppose also that

the limit exists in a pointwise

sense. Then is a summable function and .

Proof.

Consider the sequence constructed iteratively so that and . The sequence

is uniformly non-decreasing and converges to .

Furthermore, for all

. Hence is summable and .

∎

Let be the linear space of all functions which can be

expressed as the limit of a non-decreasing sequence of continuous

functions such that the following

norm is finite

(2.4)

is defined as the completion of the linear space

with respect to the uniform norm.

Definition 9.

(Essentially Bounded Functions.)

A function is called essentially bounded if it is in

.

Definition 10.

(Absolute Continuity.)

Let and be two integrals on the simplicial sequence . is said absolutely continuous with respect to if

these two integrals admit simplicial representations and

and there exists a summable function

such that for all summable functions

.

3. Path Functionals

To introduce processes we need to specify the notion of measure on a

set of paths. One could possibly introduce simplicial sequences in

space-time but we refrain from doing so and consider instead the

time coordinate as a continuous variable. In the time direction, we

are only going to be using Riemann integrals for piecewise smooth

functions, so that the underlying time discretisation one might

possibly imagine is quite straightforward and keeping track of it

would only lead to notational complexities.

Let us consider a bounded simplicial sequence and let

be a fixed finite time interval. Let us

consider the sequence where .

Given an integer , let denote the set of all

functions which are constant on a family

of mutually disjoint sub-intervals of the form with and ,

spanning the interval . Notice that for

fixed is itself a finite dimensional manifold with boundaries. In

fact, a function is characterized by the ordered

sequence of time points

between which is constant and a set of values such that, for all and

for all .

The path spaces for can be regarded as nested

into each other . In

fact, a path in is also a path in

if . Let be the union

of all path spaces containing paths with a finite number of jumps.

Definition 11.

(Function Algebras.)

Let us denote with , the algebra of all

uniformly continuous sequences of simplicial functions endowed with the operations of sum,

multiplication and with respect to the uniform norm defined as

follows:

(3.1)

Definition 12.

(Path Functionals.) A path functional is a sequence

of continuous simplicial functions satisfying the following mutual

compatibility condition:

(3.2)

Definition 13.

(Non-anticipatory Path Functionals.)

Let be a

one-parameter family of path functionals. One says that this is a

non anticipatory path functional if

(3.3)

whenever for all .

Intuitively, non-anticipatory path functionals are indifferent to

information about the realization of the path in the

argument at future times . An elementary example of

non-anticipatory path functional is given by a function of two

arguments

(3.4)

where is a piecewise smooth

one-parameter family of functions. Applications typically call for

functions which are piecewise smooth in for each

with possibly a discrete set of jump discontinuities.

We follow the usual convention according to which if jumps occur,

then the discontinuity is of cadlag type, i.e. right

continuous and with a left limit.

A less elementary example of non-anticipatory path functional one

often encounters is given by integrals of the form:

(3.5)

where the , , are

one-parameter families of lattice functions and also is a function of the time coordinates. Applications typically

call for functions which are piecewise smooth in for

each with possibly a discrete set of jump

discontinuities. Also in this case, we follow the convention

according to which at the points of jump discontinuity the function

is cadlag. The same regularity assumptions will be postulated

for the functions with respect to each of its

arguments. Although the regularity assumption for these path

functionals is sufficient for applications, they are not strictly

needed and can be relaxed by taking limits.

4. n-point Functions

Definition 14.

(Filtered Probability Spaces.)

Consider the algebra generated by the functionals of form

(3.4) and (3.5) by taking linear combinations

of finite products and completing the resulting normed space. A filtered probability space upon the lattice is defined as

a bounded linear functional on the algebra .

A constructive definition of a stochastic process can be given with

various degrees of generality. We don’t aim here at the utmost

generality but instead at pedagogical simplicity and at ultimately

explaining how to frame the theory of Markov processes. As a step

toward this goal, we introduce here a family of time ordered

point functions

(4.1)

defined for and

which is assumed to be piecewise differentiable in the time

coordinates. In addition, we assume that the following properties

hold for all :

Notice that for each fixed starting point and fixed sequence

, the function is a probability distribution function in

the arguments . This is interpreted as the probability

distribution density for paths starting from the site at time

and achieving the values at times .

Definition 15.

(Stochastic Processes.)

An adapted (stochastic) process is given by a non-anticipatory path

functional and a measure on defined by a family of

point functions .

Given an adapted process of the form and

given a , the expectation subject to the initial condition of the value attained by the process at time is

given by

(4.2)

For an adapted process of the form (3.5) instead, the

conditional expectation is given by

(4.3)

Also higher moments can be computed. To keep expressions simple,

consider a path functional of the form

(4.4)

The variance of this process at a future point in time conditional

to the starting point at time is given by

(4.5)

Notice that the factor 2 compensates for the time-ordering needed to

recast the expression in such a way that we can apply to it a

2-point function. This expression and its generalizations are used

extensively in the applications to path-dependent options discussed

below.

More generally, consider two path functionals and , where is defined as in (3.5)

and

(4.6)

Then we can compute a mixed moment as follows:

where the sum ranges over all the permutations of the time

ordered sequence such that

and . Higher conditional moments of any path functional of

the form above can be evaluated in a similar way.

-point functions are

conditioned to the starting point . It is straightforward to

define variations of these -point functions which reflect

conditioning on an initial stretch of a path for ,

where . Conditioning to a past history is equivalent to

restricting the integral over each manifold to a

sub-manifold which is part of its boundary. In general, this results

in rather clumsy expressions which are difficult to compute. In the

next section we specialize to the Markovian case for the underlying

lattice process and in this case there are no memory effects and

conditioning is more straightforward.

Definition 16.

(Radon-Nykodim Derivative.)

Consider two sequences of -point functions on the simplicial

sequence and

, where .

The Radon-Nykodim derivative of with respect to is

given by the path functional defined as follows:

(4.7)

where . Notice that the Radon-Nykodim

derivative might possibly be infinite on some paths.

The measure in path space given by is said to be

absolutely continuous with respect to if the

Radon-Nykodim derivative is finite and summable.

Finally, a word on stopping times.

Definition 17.

(Stopping Times.)

A stopping time is an adapted process

which can take only two values, by convention 0 and 1.

Stopping times are often used in conjunction with other adapted

processes to construct stopped versions of it. If is an adapted process and is a

second process, then a stopped version of corresponds to the

adapted process of function , where if and if .

5. Markov Processes

Definition 18.

(Markov Propagator.)

A Markov propagator on the simplicial sequence is

defined as a sequence of functions where

and satisfying the

following Chapman-Kolmogorov axioms:

Given a Markov propagator , one can define

a sequence of point function having all the necessary properties

by setting

(5.1)

where .

Definition 19.

(Markov Process.)

A filtered probability space generated by a Markov propagator is

called Markovian and the corresponding stochastic process is called

Markov process.

Definition 20.

(Markov Generator.)

If the matrix elements are differentiable

functions of the time parameter in a right neighborhood of

, then one defines the Markov generator at time as the

following right derivative:

(5.2)

Proposition 1.

If is a Markov generator, then for all pairs

the following two properties hold:

(5.3)

(5.4)

Viceversa, if is a differentiable

one-parameter family of matrices satisfying conditions and

above, then the differential equation (5.2) admits

one and only one solution satisfying the initial condition .

The propagator defined by the differential

equation in (5.2) can be represented by means of a

so-called path-exponential defined as follows. Let be an

integer and let us consider the product

(5.5)

where . If is so large that

(5.6)

then the operator product in equation

(5.5) is a probability kernel. Passing to the limit

, we find

(5.7)

By expanding the product in (5.5) and passing to the

limit, we arrive at the following:

Theorem 3.

(Dyson expansion.) The probability kernel can

be represented as the following convergent series:

(5.8)

By differentiating with respect to the two time coordinates in the

Dyson expansion, we also find the following two equations:

Theorem 4.

(Forward and backward equations.) The probability kernel

satisfies the backward equation

(5.9)

as well as the forward equation

(5.10)

A handy notation for this expansion is given by the following:

Definition 21.

(Path-ordered Exponential.)

The equation (5.8) is written as a

path ordered exponential

(5.11)

where the operator formally acts as follows:

(5.12)

Using the Dyson expansion for the path-ordered exponential, one

finds a path-integral representation of the probability kernel. Let

us set the following definition:

Definition 22.

(Symbolic Path.)

A symbolic path

is an infinite sequence of sites in such that for all . Let be the set of

all symbolic paths in .

Theorem 5.

(Path-Integral Representation.)

The propagator admits the following representation:

(5.13)

(5.14)

where .

Notice that the total mass of the sector of path space

consisting of lattice paths originating from

at time and attaining at most different

values by time is given by

where . If and is the operator norm of the matrix

, then we have that

(5.15)

This expression reaches a maximum as a function of at and then declines at super-exponential rate. Hence, by

discretizing the space coordinate, we ensure that the probability

mass of the set of paths with changes decreases faster than any

exponential in the limit as . This convergence is

however not uniform as and .

Definition 23.

(Inverse lattice.)

Let us consider the following lattice:

(5.16)

also called Brillouin zone or inverse lattice with

respect to .

Definition 24.

(Pseudo-differential Symbols.)

The symbol of a Markov generator is defined as follows:

(5.17)

where .

Two particularly important special examples of Markov processes are

given by monotonic processes and diffusions.

Definition 25.

(Monotonic process.) A Markov process of generator on the simplicial sequence is said monotonic

non-decreasing if

(5.18)

and monotonic non-increasing if

(5.19)

Definition 26.

(Diffusion Process.) A diffusion process is

a Markov process with generator of the form

(5.20)

where

(5.21)

and and

are two simplicial functions which, for simplicity, we assume smooth

in both arguments.

Proposition 2.

(i)

The symbol of a diffusion process is given by

(5.22)

(ii)

The path integral representation for a diffusion process has the

form

(5.23)

where

(5.24)

and .

6. Martingales and Monotonic Processes

In this section we introduce the notion of piecewise smooth Markov

process which covers a large family of models useful for

applications. In this context, we define martingales and monotonic

Markov processes.

Definition 27.

(Piecewise Smooth Markov Processes.)

Consider the time interval , the simplicial sequence ,

and a finite number of time points .

A piecewise smooth Markov process is given by

a family of Markov generators defined

on each half open time interval , where .

In correspondence to each time point , one also defines

a mapping operator such that

(6.1)

(6.2)

The Markov propagator for any pair of time points is defined as follows:

(6.3)

Moreover, if , then

(6.4)

More general Markov propagators are obtained by taking products of the ones above.

Definition 28.

(Attainable Sets.)

Let be a piecewise smooth Markov process, , and . The attainable set is defined as follows: if for

some , then is the set of such that . If instead for some , then is defined as

the set of the such that .

Definition 29.

(Equivalent Markov Processes.)

Two piecewise smooth Markov propagators and are called

equivalent if their attainable sets and are

equal for all and all . If is a

subset of for all and all

, then one says that is absolutely continuous with

respect to .

Definition 30.

(Measure Changes.)

Let

be a family of piecewise smooth Markov propagators. A measure change

is characterized by a family of positive, non-zero functions

indexed by and ,

which is strictly positive for all and zero otherwise. A measure

change function defines a transformation of a Markov generator into

an equivalent one according to the following formula:

(6.5)

Notice that the specification of the function at the

point is immaterial in the sense that it does not affect

the measure change transformation.

Definition 31.

(Time Changes.)

A measure change is called time change if there is a function

such that

for all , and .

The time change is called state

independent if is a function of the

time coordinate only.

Theorem 6.

(Deterministic Time Changes.) If defines a state independent time change

corresponding to the measure change function , then

(6.6)

where

(6.7)

The following is a particularly interesting special case of measure change:

Definition 32.

(Numeraire Changes.)

Consider a smooth (as opposed to just piece-wise smooth) Markov process

of generator . Let be a function satisfying the equation

(6.8)

The measure change given by the function

is called numeraire change and the Markov generator transforms

as follows:

(6.9)

Notice that if denotes the multiplication operator of

kernel , then equation (13.4)

can be written more compactly as follows:

(6.10)

Theorem 7.

(Numeraire Changes.) If satisfies equation (13.3) and

defines a numeraire change, then

(6.11)

Let be an adapted process in the time interval

Let us consider a fixed time . Recall that, since is

non-anticipatory, we have that for

all pairs of paths such that for all . If

, let

be the constant extension path such that for all and

for all . With probability one, we have

that

(6.12)

for some .

Definition 33.

(Monotonic Processes.)

Let be a piecewise smooth Markov

propagator and let be an adapted process given by the

non-anticipatory path functional . is said to

be increasing at time if

(i)

For all we have that

(6.13)

(ii)

We have that

(6.14)

where .

(iii)

For all and all , either

the inequality in (i) holds in a strict sense for at least one

or the inequality in (ii) holds in a

strict sense.

In case the property (iii) fails but the other two still hold, the

process is called non decreasing.

Theorem 8.

(Monotonic Processes.)

Let and be two piecewise smooth Markov propagators and

let be a non-anticipatory path functional. If

and are equivalent and if regarded as an

adapted process under the path measure generated by is

increasing (non-decreasing), then also regarded as

an adapted process under is increasing (non-decreasing).

Proof.

This theorem descends from the fact that the definition

of monotonicity depends only on the attainable sets.

∎

Definition 34.

(Martingale Processes.)

A process is a martingale if for all times we have that

(6.15)

The process is called an equivalent martingale if there

is a second piecewise smooth Markov propagator for which the

non-anticipatory path functional is a martingale

process.

Theorem 9.

(Equivalent Martingales.)

(i)

If is an increasing adapted process then it

is not an equivalent martingale. Otherwise stated, if is an

equivalent martingale then it is not increasing.

(ii)

If is a non-decreasing adapted process and it

is also an equivalent martingale, then it is a constant process with

for all .

Proof.

This theorem descends from the fact that

monotonicity properties are preserved by measure changes.

∎

Martingales are particularly useful as they can be constructed by

taking expectations.

Let be a continuous path-functional. From the

modeling viewpoint, such a functional can represent future cash flow

streams. For instance, one choice could be

(6.16)

where is a continuous univariate function and is fixed.

In a more general example, one may consider a path functional of the form

(6.17)

with for . The path conditioned

expectation of is the non-anticipatory path

functional such that

(6.18)

where the integral is restricted to the set . The intersection of

the set with each of the spaces is a

compact, finite dimensional submanifold with boundaries. To denote

path conditioning, we also use the following notation:

Equation (6.15) descends from the backward equation

in (5.9).

∎

7. The Fundamental Theorem of Finance

In this section, we derive the Fundamental Theorem of Finance

in a context general enough to encompass most cases of practical relevance.

Definition 35.

(Financial Model.)

Let be a simplicial sequence. A financial model is

given by a family of adapted

processes modeling asset prices and a non-decreasing adapted process

modeling the money-market account. For notational

convenience, we set . Let us

introduce also the discounted asset price process defined as

follows:

(7.1)

Definition 36.

(Trading Strategies.) Given

a financial model with assets, a trading

strategy is given by a family of adapted processes

. The value

process of a strategy is the adapted process

(7.2)

The discounted value process instead is given by

(7.3)

Definition 37.

(Self-Financing Condition.)

An adapted trading strategy is called self-financing if the following

two conditions hold:

(7.4)

and if, for all , we have

that

(7.5)

Proposition 4.

If is a self-financing trading strategy, then

the corresponding discounted value process satisfies

(7.6)

and for all , we have that

(7.7)

(7.8)

Definition 38.

(Arbitrage Strategies.)

A self-financing strategy is called arbitrage at time if the

corresponding discounted value process

is increasing at time .

Theorem 10.

(Fundamental Theorem of Finance.)

If there is an equivalent measure with respect to which all discounted base asset

price processes are martingales, then

(i)

The discounted value process of any self-financing trading

strategy under the same equivalent measure is a martingale.

(ii)

There is no arbitrage.

Conversely, if there is no arbitrage than there exists a measure change

under which all discounted asset price processes become martingales.

Proof.

The first part of the theorem is a simple consequence of the definitions

put forward. The converse instead requires a proof.

Let be the vector space spanned by

functions of the form where . Let be the cone in made up by

all the vectors with non-negative components. Also, let us introduce

the following vector :

(7.9)

Notice that, in case and the asset is the money market account, then

for all .

Suppose there is no arbitrage and fix a time . Assuming

there does not exist a trading strategy with a strictly increasing

value process, for all vectors there are

two elements such that

(7.10)

If in equation (7.10) we set , we

conclude that the vector has both positive and negative components.

Hence, the the hyperplane

orthogonal to the vector intersects .

Let be the orthogonal projection operator onto the hyperplane

and let us consider the vector

(7.11)

for . Due to absence of arbitrage, there are

two elements such that

(7.12)

Hence, the vector is transversal to the octant of positive vectors.

As a consequence, the hyperplane is orthogonal to both vectors and

, also intersects .

The argument above can be iterated times, leading to the

conclusion that there exists a strictly positive function

, such that

(7.13)

for all . In particular, this implies that there exists

a measure change function such that

(7.14)

∎

8. Weak Convergence of Markov Generators

Consider a one dimensional Markov process defined on the simplicial

sequence and the time interval . Many

different specifications of Markov generators on may

correspond to the same limit. In this section we identify a

canonical sequence of generators under a few regularity hypotheses

which imply the existence of a weak limit in distribution sense for

the generator. This is a necessary first step to single out the

general form of an admissible Markov generator. In the following

sections, we then investigate convergence under the much finer

criteria of pointwise convergence for probability kernels and their

derivatives.

First consider the case when the limiting domain is bounded. Without

restricting generality, let us suppose that .

Let be a sequence of Markov generators.

The first assumption we make is that the first two moments are finite, or more specifically

Hypothesis MG1. The sequences

(8.1)

are uniformly bounded in absolute value as and converge to

limits for all and all , i.e. the following limits exist:

(8.2)

Notice that, due to the dominated convergence theorem, the functions

and regarded as piecewise constant functions on

converge weakly to the corresponding limits.

Hypothesis MG2. The following limits exist and are finite for all and

all pairs such that :

(8.3)

The family of functions can be represented in terms of the

so called Levy measures specified as follows:

Theorem 11.

(Levy measures.)

For all there exists a measure in (called Levy measure)

with the following two properties:

(i)

(8.4)

(ii)

For all with the

following representation is valid:

(8.5)

Definition 39.

(Finite activity jumps.)

A Markov process is said to have finite activity jumps if

for all and all we have that

(8.6)

Notice that given and we have

(8.7)

More generally, if is a test function

such that and , then we have that

(8.8)

Although the above sequence is bounded, the limit may not exist in general.

We thus need to stipulate this as a separate assumption:

Hypothesis MG3. For all test

functions such that and all , the sequence admits a limit as .

Let us introduce the following notations:

(8.9)

Notice that the sequence is non-negative and

is uniformly bounded as a function of . More precisely

(8.10)

On the other hand, we cannot conclude in general that is necessarily uniformly bounded. In fact, the difference

could diverge as while

being compensated by terms concentrated at which in

turn also diverge in the limit as while keeping the

total drift uniformly bounded. An exception to this

general situation is found in case the following condition is

satisfied:

Hypothesis MG4. For all

and all we have that

(8.11)

Two particularly important situations in which this condition

holds are given in the following:

Theorem 12.

(MG4.) Assuming , if the Markov process

is either monotonic or has finite activity jumps, then holds.

Under the three assumptions ,

the sequence of Markov generators

can be mapped into an equivalent canonical sequence of Markov generators .

More precisely, we set

(8.12)

in case . Furthermore,

we set

(8.13)

where

(8.14)

and the operators and are defined as in

equation (5.21). Finally,

(8.15)

Theorem 13.

(Canonical Representations of Markov Generators.)

For all smooth functions of compact support and all we have that

(8.16)

A compact representation for a canonical generator summarizing these

definition is obtained by considering the symbol as specified in

Definition (24).

Theorem 14.

(Levy-Khintchine representation.) Under the hypothesis above and in case is bounded, the

symbol of a generator in canonical form can be expressed as follows:

(8.17)

The following limit converges in the weak topology:

(8.18)

where is the Levy measure. Moreover, if also

is satisfied, then

the symbol of a generator in canonical form can be expressed as follows:

(8.19)

The following limit converges in the weak topology:

(8.20)

9. Fast Exponentiation and Spectral Methods

Numerical analysis of pricing models in the operator formalism

depend on the ability to compute the propagator for a given

generator . Time homogenous Markov generators represent a privileged special case of particular importance.

In this case, the associated propagator solving the differential

equation in (5.2) is given by the matrix exponential

(9.1)

Matrix exponentiation can be defined in several equivalent ways,

such as by Taylor expansion

(9.2)

or by means of Neper’s formula

(9.3)

We find that the most efficient and robust method for exponentiating

Markov generators is the so called fast exponentiation

algorithm.

Let us fix a

Markov generator and a time horizon . Let be the largest time

interval for which both of the following properties are satisfied:

To compute , we first define the elementary

propagator

(9.4)

and then evaluate in sequence , ,

… .

As we show in the next few sections, this algorithm approximates

probability kernels with errors with respect to the continuous time

kernel density which, in fairly general cases, are of order

. This is the same order by which

the continuous time kernel density differs from its continuous limit

also according to estimates below. In the case of Brownian motion, a

sharp convergence estimates of ordered can also be

proven.

Matrix multiplication is accomplished numerically by invoking the

routine in Level-3 BLAS. Very efficient, processor

specific version of are now available along with

implementations on massively parallel GPU chipsets. It turns out

that the standard measure of algorithmic complexity as the number of

floating point operations required to accomplish a certain task, is

not simply proportional and scales non-linearly with respect to

execution time. Using blocking and cache optimizations and

distributing the load across many cores, execution time for medium

to large matrices appears to scales much better than the naive

scaling one would obtain by triple looping [GotoGeijn].

A more general method that allows to compute not only exponentials

but also other functions of a Markov generator is full

diagonalization. Unfortunately, unless the Markov generator is

symmetrizable, diagonalization algorithms can possibly run into

serious instabilities within double precision arithmetics because of

the phenomenon of pseudo-spectrum [TE2006]. This makes it

impossible to diagonalize exactly within the limits of

double-precision arithmetics and forces one to resort to expedients

such as for instance spectral truncations. Since the fast

exponentiation method has much better scaling properties than full

diagonalization and is entirely stable, we recommend that it be used

in all situations where a matrix exponentiation is required.

However, it often arises the necessity to define and compute also

other functions of a given time independent Markov generator and for

this purpose diagonalization can be usefully employed, especially

when the target matrix is symmetrizable.

Not all Markov generators are diagonalizable but most are and it is

safe to take diagonalizability for granted in numerical

applications. To make this statement more precise, one sets out the

following definitions:

Definition 40.

(Generic Properties.)

A dense of a topological space is

a countable intersection of dense open subsets. If a property is

valid on a dense one says that it is valid generically, or that it is generic. Instead, if the same

topological set is endowed of a measure and a property is valid on a

full measure set of parameters, one says that it is valid almost

surely with respect to that particular measure.

We have that

Proposition 5.

Markov generators are

diagonalizable both generically and almost surely.

Let and , , be eigenfunctions and

eigenvalues of the Markov generator , i.e.

(9.5)

Let be the matrix whose columns are given by the vectors

and let be the diagonal matrix with the

eigenvalues on the diagonal. Hence

(9.6)

We have that and . This equation expressed in components reads as

follows:

(9.7)

where is the th row vector of the inverse matrix .

One may extend the above definition to other functions of a Markov

generator. If is a function, one may define

as the operator whose matrix is given by

(9.8)

An important example of functional calculus is found to express the

Markov generator of processes obtained by stochastic time change,

whereby the time-change process has independent, uniformly

distributed increments. Processes in this class are called Bochner subordinators. Because of time and space homogeneity,

Bochner subordinators can be constructed starting from a process on

simplicial sequence and are characterized by a Markov

generator of the form .

Theorem 15.

(Bochner Subordinators.)

If the limit exists in weak sense on

then the limit kernel has the following form

(9.9)

where is a positive measure supported on and is

such that

(9.10)

The characteristic function of the process defined as the

Fourier transform of the Markov generator is thus

(9.11)

The Laplace transform instead is given by

(9.12)

A function of this form is called Bernstein function.

Bernstein functions may be used to express Laplace transform of the

transition probability kernel of time-homogeneous monotonic

processes as follows:

(9.13)

In turn, we may also express the transition probability kernel in

terms of the characteristic function, i.e.

(9.14)

Notice that since , the last formula may

also be interpreted as the Fourier-Mellin inversion of the previous

one.

Example 1.

(Poisson Process)The Poisson process corresponds to

(9.15)

Example 2.

(Stable Process)The stable subordinator with index

is given by

(9.16)

Example 3.

(Gamma Process)The Gamma subordinator with variance rate

is given by

(9.17)

To add jumps to a diffusion process one can use the method of

independent stochastic subordination. Namely let be the

diffusion process with drift function and volatility

function and let be the

corresponding Markov generator. Consider the generator

(9.18)

The propagator for satisfies the following

equation:

(9.19)

where are the paths of the monotonic process in Example 3,

the are the eigenfunctions of the diffusion generator

, are the corresponding eigenvalues

and the functions are defined as in (9.7).

Hence, the generator identifies the

time-changed process with paths .

To model asymmetric jumps one can follow several strategies. A

simple one is to specify the two different variance rates

and for the up and down jumps and compute separately two

Markov generators

(9.20)

The new generator for our process with asymmetric jumps is obtained

by combining the two generators above

(9.21)

The construction can also be localized. If is a

family of Bernstein functions indexed by the state variable

, then one can consider the Markov generator of

matrix

(9.22)

This construction allows one to model state dependent jumps.

10. Construction of Brownian Motion

This section is based on work in collaboration with Alex Mijatovic,

see [AlbaneseMijatovicBM].

Let be a simplicial sequence

converging to an interval , where . Let and be two constants.

The generator of a Brownian motion on has the form

(10.1)

for all interior points . We assume that is

large enough so that

(10.2)

for all .

If is a boundary point, i.e. , then several

definitions of the operator are possible depending on the

choice of boundary conditions. Absorbing boundary conditions

correspond to the choice

(10.3)

Reflecting boundary conditions correspond to

(10.4)

(10.5)

where is the closest point to in the interior of

, while for all other points . Periodic boundary conditions are implemented by setting

(10.6)

if or is the closest point to in the

interior of , and also

(10.7)

where is the boundary point at the opposite

extreme of the simplex . Finally, mixed boundary

conditions can also be defined by taking a convex linear combination

of the generators satisfying one of the three boundary conditions

above.

Theorem 16.

(Convergence Estimates for Brownian Motion.) Consider a Brownian motion

defined as the process with generator in (10.1) where

and are constants satisfying the bounds in

(10.2) for all and we assume

periodic boundary conditions. Let us consider the kernels

(10.8)

and

(10.9)

If is such that and is large enough, then

there is a constant such that for all we

have the following inequalities:

(i)

(10.10)

(ii)

(10.11)

(iii)

(10.12)

(iv)

(10.13)

Proof.

It suffices to show this inequality for . Let us assume

for simplicity that and for all . The argument extends to more

general lattice geometry but the consideration of these more general

cases would obscure the simplicity of the proof with needless detail

and will thus be omitted.

Let be the Brillouin zone as defined in equation

(5.16). Let

be the Fourier transform operator defined so that:

(10.14)

for all . The inverse Fourier transform is given by

(10.15)

The Fourier transformed generator is diagonal and is given by the

operator of multiplication by

(10.16)

We have

(10.17)

Using this Fourier series representation, we find

Let

(10.19)

If is small enough, i.e. if is sufficiently large, we

have that

where denotes the real part of and

denotes a generic constant. Similarly

Since

(10.22)

and

(10.23)

we find that if then

(10.24)

Moreover, since

(10.25)

we conclude that in case , the following inequality holds:

(10.26)

Hence, if is large enough, we find

(10.27)

for some constant independent of . This concludes the proof

of the bound in (10.10).

To estimate the sensitivity in (10.11) notice that

(10.28)

and

Let

(10.30)

If is small enough, we have that

where denotes a generic constant. Similarly

(10.32)

If is large enough, we also find

for some constant independent of . This concludes the proof

of the bound in (10.11). The bound in (10.12) can

be derived in a similar way.

Finally, consider the following Fourier representation for the

discretized kernel

(10.34)

Consider the formula

(10.35)

and let’s represent the difference between kernels in

(10.13) as follows:

where is chosen as in (10.19). The very same bounds

above lead to the conclusion that this difference is .

∎

11. Kernel Convergence Estimates for Diffusion Processes

Diffusions are a particularly important class of Markov processes

which generalize Brownian motions to allow for space dependent

drifts and volatility. In this section we find kernel convergence

estimates for the one-dimensional case following

[AlbaneseKernelEsimtatesA].

Let be a simplicial sequence

converging to an interval , where . Let and be smooth

functions defined in a neighborhood of . The generator of a

diffusion on has the form

(11.1)

We assume that is large enough so that

(11.2)

for all and all . The definition of the

generators at boundary points can be extended by imposing one of the

boundary conditions in the previous section, i.e. reflecting,

absorbing, periodic or mixed.

Theorem 17.

(Convergence Estimates for Diffusions.)

Consider a diffusion process

defined as in (11.1) where and

are smooth functions satisfying the bounds in

(11.2) for all . Assume that

boundary conditions are either periodic or absorbing. Then there is

a constant such that

(11.3)

for all and all .

It suffices to establish the above inequality in the case . In fact, given this particular case, the general statement can

be derived with an iterative argument. Let so that

.

Recall that the path integral representation for a diffusion process

has the form in equation (11.4). In the special case of a

time-homogeneous process, this expansion reads as follows:

(11.4)

where

(11.5)

where .

Let us introduce the following two constants characterizing the

volatility function:

(11.6)

and let

(11.7)

Since our interval is bounded, we have that and

.

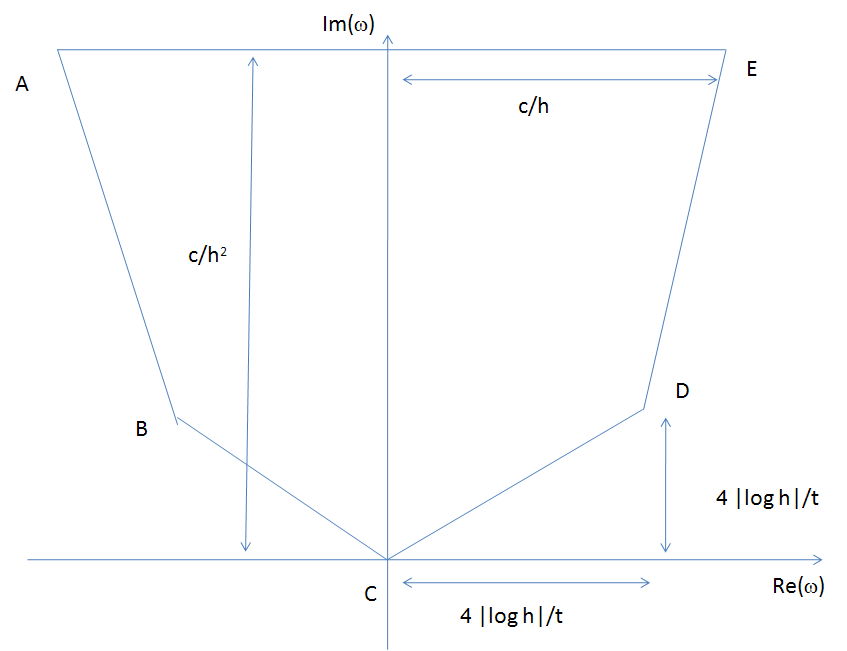

Figure 1. Contour of integration for the integral in (11.9).

is the countour joining the point to the

points . is

the countour joining the point to to .

Let us introduce the following Green’s function:

(11.8)

The propagator can be expressed as the following contour integral

(11.9)

Here, is the contour joining the point to the

points in Fig. 1, while

is the contour joining the point to to . By design, each

point on the upper path is separated from

the spectrum of .

Lemma 1.

For sufficiently large,

there is a constant such that

(11.10)

Proof.

The proof is based on the geometric series expansion

(11.11)

whose convergence for can be established

by means of a Kato-Rellich relative bound, see [Ka1976]. More

precisely, for any , one can find a such that

the operators and satisfy the following

relative bound estimate:

(11.12)

for all periodic functions and all . This bound can be

derived by observing that and can be

diagonalized simultaneously by a Fourier transform, as done in the

previous section, and by observing that for any , one can

find a such that

(11.13)

for all and all .

Under the same conditions, we also have that

(11.14)

Hence

(11.15)

where the last inequality holds if , if

is chosen sufficiently small and if is large enough. In

this case, the geometric series expansion converges in

(11.11) converges in operator norm. The uniform norm

of the kernel is pointwise

bounded from above by .

Since the points and have imaginary part equal at height , the integral over the contour

converges also and is bounded from above by in uniform norm.

∎

Lemma 2.

If we have that

(11.16)

Proof.

Let us define the function

(11.17)

where is the characteristic function of . We have

that

(11.18)

where is the th convolution power, i.e. the

fold convolution product of the function by itself. The

Fourier transform of is given by

(11.19)

The convolution power is given by the following inverse Fourier

transform:

(11.20)

Introducing the new variable , the integral can be recast as follows

(11.21)

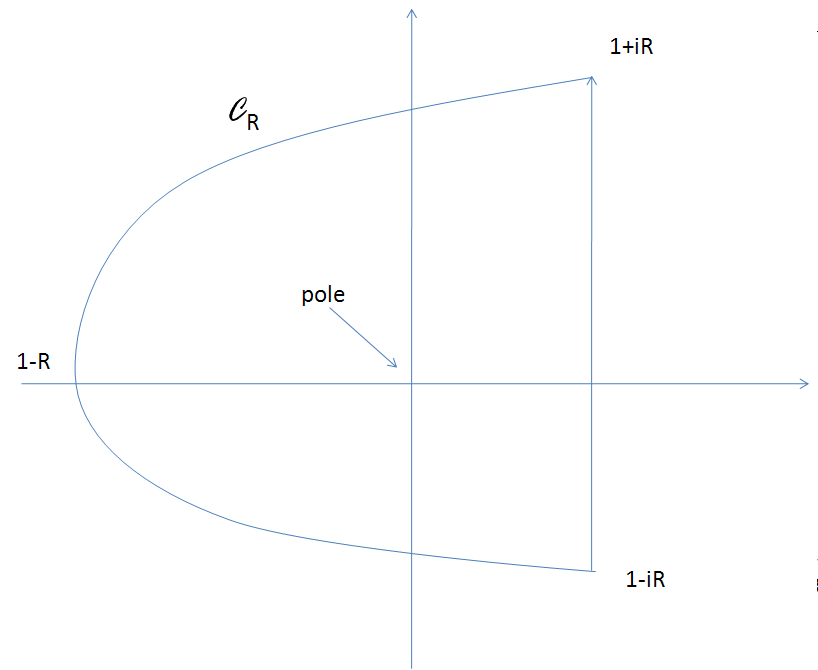

where is the contour in Fig. 2.

Using the residue theorem and noticing that the only pole of the

integrand is at , we find

Figure 2. Contour of integration for the integral in (11.21).

∎

Definition 41.

(Decorating Paths.)

Let and let be a symbolic sequence in . A decorating

path around is defined as a symbolic sequence with containing

the sequence as a subset and such that if and

, then all elements with are such

that . Let be the set of all decorating sequences around

. The decorated weights are defined as follows:

(11.24)

Finally, let us introduce also the following Fourier transform:

(11.25)

Definition 42.

(Notations.)

In the following, we set so that . We also

use the Landau notation to indicate a function such

that is bounded in a neighborhood of .

Lemma 3.

Let and let be an

integration contour as in Fig. 1. Then

(11.26)

Proof.

We have that

(11.27)

The number of paths over which the summation is extended is

(11.28)

where Applying Stirling’s

formula we find

(11.29)

Hence

for some constant . It suffices to

extend the summation over only up to

(11.31)

To resum beyond this threshold, one can use the previous lemma. More

precisely, we have that

Let . To evaluate the resummed weight function,

let us form the matrix

(11.33)

and decompose it as follows:

(11.34)

where

(11.35)

(11.36)

(11.37)

and

(11.38)

Let us introduce the sign variable , the functions

(11.39)

(11.40)

and their Fourier transforms

(11.41)

where

(11.42)

We also require the functions

(11.43)

and the corresponding Fourier transforms

(11.44)

If is a symbolic sequence, then

(11.45)

(11.46)

Let us estimate the difference between the functions

and

assuming that is in the contour in Fig.

2. Retaining only terms up to order up to ,

we find

A lengthy but straightforward calculation which is best carried out

using a symbolic manipulation program, gives

where

We have that

where is a primitive of , i.e.

(11.51)

We conclude that there is a constant such that

(11.52)

for all . Here we use the decay of

in the upper half of the complex plane to offset the

dependencies in the integrand. Similar calculations lead to

the following expansions:

(11.53)

Since and , we find

(11.54)

This completes the proof of the Lemma and of the Theorem.

∎

12. Convergence of Time Discretization Schemes

In this section we analyze the convergence of the time discretized kernel

that is obtained by means of fast exponentiation.

Let be a simplicial sequence

converging to an interval , where . Let and be

functions on satisfying all the conditions in the previous

section and consider the generator of a diffusion on of the form

(12.1)

Theorem 18.

(Convergence Estimates for Fast Exponentiation.)

Let and consider the discretized kernel

(12.2)

where is the operator in (12.1) and

is so small that

(12.3)

Assume that boundary conditions are either periodic or absorbing

and that the ratio is an integer.

Then there is a constant such that

(12.4)

for all and all .

Proof.

A Dyson expansion can also be obtained for the time-discretized kernel and

has the form

(12.5)

where and . In this case, the propagator can be expressed

through a Fourier integral as follows:

(12.6)

where

(12.7)

The propagator can also be represented as the limit

(12.8)

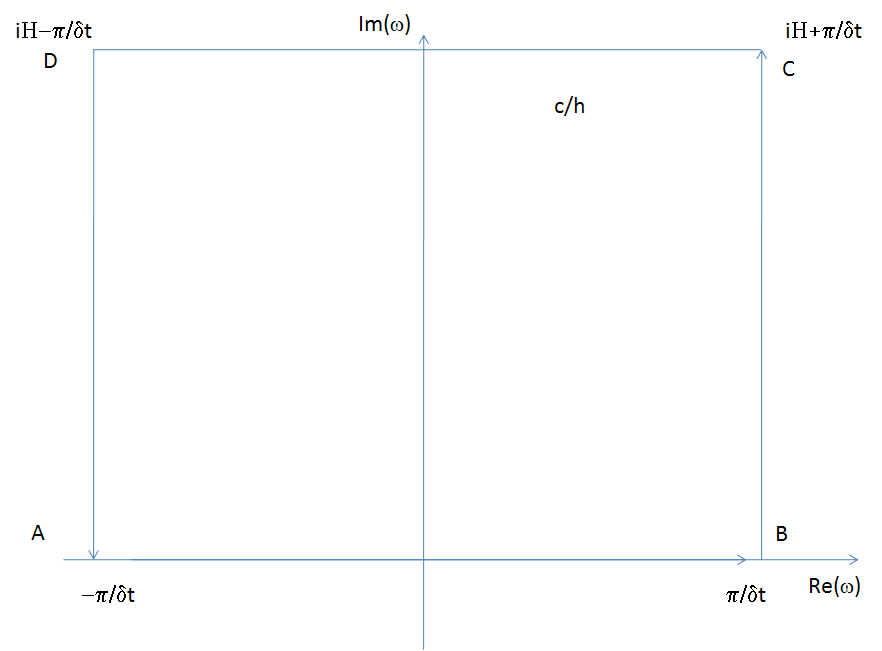

where is the contour in Fig. 3.

This is due to the fact that the integral along the segments

and are the negative of each other, while the integral over

tends to zero exponentially fast as ,

where is the imaginary part of . Using

Cauchy’s theorem, the contour in Fig. 3 can be

deformed into the contour in Fig. 1. To estimate

the discrepancy between the time-discretized kernel and the

continuous time one, one can thus compare the Green’s function along

such contour. Again, the only arc that requires detailed attention

is the arc , as the integral over rest of the contour of

integration can be bounded from above as in the previous section.

Figure 3. Contour of integration for the integral in (12.8).

Let and let us introduce the two functions

(12.9)

(12.10)

and the corresponding Fourier transforms

(12.11)

(12.12)

We have that

(12.13)

where the last step uses the fact that .

Let us also introduce the functions

(12.14)

and the corresponding Fourier transforms

(12.15)

Again we find that

(12.16)

If is a symbolic sequence, then let us set

(12.17)

(12.18)

We have that

(12.19)

The integration over the contour in Fig. 1 can

again be split into an integration over the countour and an integration over . The integral over

can be bounded from above thanks to Lemma

3. Furthermore, we have that

(12.20)

∎

13. Hypergeometric Brownian Motion

This section is based on work in collaboration with Joe Campolieti,

Peter Carr and Alex Lipton, see [ACCL2002].

In this section we pose the problem of constructing driftless

diffusion models which reduce to a given diffusion by means of a

combination of a measure change and a coordinate transformation.

Consider a Markov process on the simplicial sequence with generator . Let be a

real valued parameter and suppose and are

two linearly independent solutions of the equation

(13.1)

for all . Notice that on the boundary these equations may fail and, in actual applications, they

will indeed as a rule fail. Consider the function

(13.2)

for some choice of constants such that this function is

strictly positive. This function satisfies the equation

(13.3)

Hence defines a measure change and one can construct a

new Markov generator by setting

(13.4)

Consider the linear fractional transformation

(13.5)

for some choice of constants .

Theorem 19.

(Linear Fractional Transformations.)

The process satisfies the martingale condition

(13.6)

for all .

Proof.

We have that

∎

This Theorem provides a general methodology for constructing a

process which is nearly a martingale out of a Markov process. In the

particular case of one-dimensional diffusion processes, the

construction gives rise to families with up to 7 adjustable

parameters of analytically solvable diffusions with drift equal to

zero within the interior of the domain of definition. What makes the

case of one-dimensional diffusions special is the fact that the

function is invertible in the limit as , i.e.

either monotone increasing or monotone decreasing in this limit.

More specifically, consider the diffusion with Markov generator:

(13.8)

where . Two important cases are the CIR process (reducing

to the Bessel equation in the continuous limit) for which

(13.9)

with and the Jacobi process (reducing to a gaussian

hypergeometric polynamials of type ) for which

(13.10)

and .

The construction above admits a continuous limit if the simplicial

functions converge to twice differentiable

functions and satisfy the equation

(13.11)

within the interior of the domain . Here

(13.12)

Theorem 20.

(Invertibility.) Let be functions satisfying

equation 13.12 in the interior of the corresponding domain

of definition and let

(13.13)

for some choice of constants such that the

denominator in this equation has no zeros. Then we have that

(13.14)

where

(13.15)

where either sign would be allowed and is a positive

constant. In particular, the function is invertible.

Proof.

Let us introduce the Wronskian

(13.16)

such that

(13.17)

A direct calculation shows that

(13.18)

and

(13.19)

Hence, (13.15) gives the solution to the

equation in (13.19).

∎

Let be the inverse of the function , we have that

(13.20)

where

(13.21)

Theorem 21.

(Kernel mapping.)

In the limit , the propagator density for the process

with zero drift and volatility as in (13.21) is

given by

(13.22)

where is the propagator density for the process of

generator (13.12).

Let us consider in detail the case of the CIR model in

(13.9). If , then the pricing kernel for the

state variable is expressed in terms of modified Bessel functions as

follows:

(13.23)

The generating function is

(13.24)

with arbitrary constants ,. Here is the

modified Bessel function of order and is the

associated McDonalds function. In this case we obtain a dual family

with 6 adjustable parameters.

In case . the propagator density for the state variable

can still be expressed in terms of modified Bessel functions as

follows:

(13.25)

where . For a

derivation see [Giorno88]. The general solution of equation

(13.1) reduces to Whittaker’s equation and generating

functions have the general form

(13.26)

for arbitrary constants ,. Here and

are Whittaker functions which can also be expressed

in terms of confluent hypergeometric functions or in terms of Kummer

functions.[Abramowitz] This construction gives rise to a dual

family with 7 free parameters where

(13.27)

The 7 parameter family which reduces to the CIR model has a local

volatility function defined on either an interval or on a half line

and behaves asymptotically as the CEV volatility on one hand and as

a quadratic model on the other. This hybrid shape allows for greater

flexibility.

Next, we show that classic exact solutions in the literature, namely

quadratic and CEV models, can all be rediscovered as particular

cases of our general formula for the Bessel family where we make use

of the above solutions to the underlying space process with

, and .

Without loss of generality, we can fix . Let’s specialize

further to the case where

(13.28)

which leads to a transformed process with volatility

(13.29)

where is the inverse of the function in equation

(13.28). In this family, and are positive,

is arbitrary and . The function maps

the half line into ,

where is a strictly monotonically increasing function with

. This solution region can be

inverted so that . This is accomplished by

either replacing by in equation (13.28) or by

applying a linear change of variables that maps into . In this special case, we make use of the generating function in

equation (13.24), with the choice , and formula

(13.22) reduces to

(13.30)

We note that this density integrates exactly to unity in space

(i.e. no absorption).

Example 4.

(Quadratic volatility models)Pricing kernels for quadratic

volatility models are readily obtained as a subset of the above

general family with the special choice of parameter .

After making the substitution and setting

the transformation function

becomes

(13.31)

where . Here, we assume that .

The inverse transformation is given by

(13.32)

and the volatility function is obtained by insertion

into equation (13.29) while using the Bessel function of

order ,

(13.33)

Inserting the expression (13.32) into equation

(13.30), one obtains the pricing kernel

(13.34)

where . In

the special case of a volatility function with a double root, i.e.

(13.35)

the pricing kernel is computed by taking the limit as

, and one finds

(13.36)

Example 5.

(Lognormal models)The pricing kernel for the log-normal Black-Scholes model with

is a particular case of the above formula

for the quadratic model. The derivative with respect to of the

quadratic volatility function in (13.33), evaluated at

, is . Taking the limit (or ), while holding the other

parameters fixed, one obtains .

The pricing kernel in (13.34) gives the kernel for the

log-normal model in the limit , i.e.

(13.37)

Example 6.

(CEV model)The constant-elasticity-of-variance (CEV) model is recovered in the

limiting case as . Assume and let

be defined so that . The transformation

(13.38)

has inverse given by

(13.39)

for any constant . The volatility function for this model

is

(13.40)

In the limit , the Laplace transform , which implies that the numeraire change is trivial in this case.

The pricing kernel can be evaluated by substitution into the general

formula (13.22), and after collecting terms, it turns

out to be

(13.41)

This formula was derived in the case , for which the

limiting value is not attained and the density is easily

shown to integrate to unity (i.e. no absorption occurs and the

density also vanishes at the endpoint ). We note that the

same formula solves the propagator equation for ,

leading to the same Bessel equation of order . In

the range , however, the properties of the above pricing

kernel are generally more subtle. In particular, one can show that

the density integrates to unity for all values ,

hence no absorption occurs for . The

boundary conditions for the density can be shown to be vanishing at

(i.e. paths do not attain the lower endpoint) for all

. In contrast, for the density

becomes singular at the lower endpoint (hence this

corresponds to the case that the density has an integrable

singularity for which paths can also attain the lower endpoint, but

are not absorbed). For the special case of the formula

gives rise to absorption. [Note that only for the range the above pricing kernel is not useful since it gives rise

to a density that has a non-integrable singularity at .

In this case, however, another solution that is integrable is

obtained by only replacing the order by

in the Bessel function. The latter solution for

the density does not integrate to unity and hence gives rise to

absorption which can be of use to price options in a credit

setting.] The special case of gives a nonzero constant

value at the lower endpoint, and recovers the Wiener process with

reflection and no absorption on the interval with

(13.42)

14. Stochastic Integrals for Diffusion Processes

This section provides a new derivation of a theorem by Cameron,

Feynman, Girsanov, Ito, Kac and Martin, see [CameronMartin],

[Ito1951], [Feynman1948] and [Kac1950]. This result

is at the center of stochastic calculus and in the following

sections, we derive far reaching extensions and applications.

Theorem 22.

(Cameron-Feynman-Girsanov-Ito-Kac-Martin.)

Consider a diffusion process on the simplicial sequence

and of generator

(14.1)

Consider also the process given by the integral

(14.2)

where and are smooth functions in both