Rational Expectations, psychology and inductive learning via moving thresholds

Abstract

This work suggests modifications to a previously introduced class of heterogeneous agent models that allow for the inclusion of different types of agent motivations and behaviours in a unified way. The agents operate within a highly simplified environment where they are only able to be long or short one unit of the asset. The price of the asset is influenced by both an external information stream and the demand of the agents. The current strategy of each agent is defined by a pair of moving thresholds straddling the current price. When the price crosses either of the thresholds for a particular agent, that agent switches position and a new pair of thresholds is generated.

Different kinds of threshold motion correspond to different sources of motivation, running the gamut from purely rational information-processing, through rational (but often undesirable) behaviour induced by perverse incentives and moral hazards, to purely psychological effects. As with the previous class of models, the fact that the simplest model of this kind precisely conforms to the Efficient Market Hypothesis allows causal relationships to be established between properties at the agent level and violations of EMH price statistics at the global level.

pacs:

89.65.Gh 89.75.DaI Introduction

The Efficient Market Hypothesis (EMH) f70 still has enormous influence in political and economic theory as well as in the day-to-day operations of financial markets. This is in spite of numerous statistical and experimental studies that invalidate both the underlying assumptions (eg. the rationality of economic participants) of the EMH and the output of mathematical models that are derived from them (eg. stock prices that are described by a geometric Brownian motion resulting in a Gaussian distribution of the changes in the log-price returns) ms00 ; c01 . The near-universal statistical properties of real markets, most of which deviate from those predicted by the EMH, are often referred to as the ‘stylized facts’.

The inappropriate use of EMH models and Gaussian statistics by market participants can cause great damage, not just to the participants themselves but to entire economies. For example, a widely-used form of portfolio risk management, called Value-at-Risk, attempts to estimate the maximum loss that can occur with a specified (low) probability. Also many so called ‘quantitative’ hedge-funds use historical correlations between different financial products to identify and exploit perceived market mispricings. This extrapolation from the past into the future becomes less justifiable in an environment where the decreasing probability of large fluctuations follows a power-law rather than an exponential one (i.e. where ‘fat-tails’ are present) and significant coupling between market participants can develop.

To take a very recent example, at the time of writing a sudden rise in the delinquency rates of so-called subprime mortgages in the US has precipitated a credit-crunch in financial markets around the world. The growth of this industry was stimulated by a period of low global interest rates, inadequate accounting and credit-rating standards and the development of novel financial derivatives such as Collateralized Debt Obligations (CDOs) and Credit Default Swaps (CDSs).

However it is the proximal causes that are of more interest us here. The herding phenomenon and the resulting ‘madness of crowds’ that lies at the heart of most, if not all, financial bubbles was present in the general public and their increasingly irrational belief that house prices would continue to rapidly climb. This caused a cycle of additional house-buying and home-equity withdrawal that fuelled prices further. However, on the lending side of the equation, there were significant perverse incentives and moral hazards at play. Realtors, property appraisers and mortgage brokers all receive their commissions at the time of the transaction and have no incentive to question the quality of the transaction or lower its amount. The loan originators were similarly able to distance themselves from the default risk on the loans via the use of CDOs and CDSs. This continued up the financial food chain, helped by the fact that there was no open market for these derivatives and their prices could be easily manipulated via creative accounting practices. Finally, when the housing market burst the liquidity assumption inherent in almost all financial models — that any desired transaction can be carried out at the current price — failed to hold as buyers of these derivatives vanished from the marketplace.

In short, it is hard to see how models based solely upon the notion of efficient markets can begin to adequately predict or quantify situations such as the one described above. The construction of financial models that can incoporate both rational and irrational agent behaviour, as well as the rational-but-perverse consequences of market defects, is an important undertaking. The simple, yet plausible, class of models introduced in this paper provides a possible framework within which the consequences of different EMH violations can be systematically studied.

II Previous Results

In cgls05 ; cgl06 ; ls06 ; cgls07 a class of models using thresholds was introduced. These are briefly described below but the reader is directed to the references for further details. The models consisted of two parts, one defining the price updates and the other determining when agents switch. The price changes were determined by both external factors, namely a Gaussian uncorrelated information stream, and changes in the internal supply/demand due to agents switching positions.

The thresholds are involved in the modeling of the agents themselves. In the simplest case, whenever an agent switches position, a pair of fixed price thresholds is generated (from some predetermined distribution) that straddles the current price. Then, when the price crosses either of the thresholds the agent switches and a new pair of thresholds is generated. If one interprets the price thresholds as representing the agent’s rational future expectations then the model is, both practically and philosophically, an EMH model. Differing expectations cause trading to occur but the lack of any kind of coupling between agents ensures the ‘correct’ pricing outcome.

A propensity towards herding, either due to subconscious psychology or conscious momentum-trading strategies, was then introduced via the introduction of an additional threshold for each agent. While an agent is in the minority their herding pressure increases until they switch to join the majority (unless the majority position changes, or they switch due to the price thresholds being violated, before this occurs). The main conclusion to be deduced from these early models was that, at least within this modeling scenario, herding causes fat-tails and excess kurtosis in the price return data but not volatility clustering. However, long-term correlations in the volatility could be induced by allowing the volatility to depend upon the market sentiment and/or allowing correlations in the information stream. A detailed statistical analysis ls06 showed that all of the important stylized facts could be reproduced and others, such as the asymmetry between large positive and negative moves, could also be introduced using asymmetric herding.

III Moving-threshold Models

The inclusion of additional non-EMH effects, using the above approach, would require more thresholds. However,a much more elegant threshold-based approach is to allow the original pair of price-thresholds to vary with time between switchings. The full mathematical moving-threshold model is now described and more detailed economic justifications for the modeling assumptions can be found in cgls05 ; ls06 ; cgls07 .

The system is incremented in timesteps of length and each of agents can be either short or long the asset over each time interval. The position of the investor over the time interval is represented by ( long, short). The price of the asset at the end of the time interval is and for simplicity the system is drift-free so that corresponds to the return relative to the risk-free interest rate plus equity-risk premium or the expected rate of return. An important variable is the sentiment defined as the average of the states of all of the investors

| (1) |

and .

The pricing formula is given by

| (2) |

where and represents the exogenous information stream. Note that when and the price follows a geometric Brownian motion.

Suppose that at time the investor has just switched and the current price is . Then a pair of numbers are generated from some random distribution and the lower and upper thresholds for that agent are set to be and respectively. Defining the evolution of these thresholds now corresponds to defining a strategy for the investor. Such strategies can be made arbitrarily complicated and may be partly rational (and conscious) and partly irrational (and subconscious). They can also be constructed to include perverse incentives or inductive learning strategies as required.

Three simple examples are of particular note. Firstly, as noted above, the case where the thresholds are fixed (until the agent switches again) completely decouples the agents’ behaviour and gives EMH pricing. Secondly, we can mimic the herding effect by causing the thresholds to move together (increasing and decreasing ) whenever the agent is in the minority. Thus agents in the minority have a higher tendency to switch into the majority than vice versa. Thirdly, we can suppose that a simple, unspecified, perverse incentive is in place, causing agents to prefer one of the states over the other, say over . This can be recreated by moving the thresholds closer together whenever .

The threshold approach should be contrasted with the more common one taken in the literature of Markovian-type switching between investment positions or strategies (lm00 and numerous others). Here the threshold values act as ‘hidden variables’ that are highly-history dependent. Much of human behaviour is, of course, also non-Markovian with decisions being made over a period of time, rather than being spontaneously formulated and acted upon. Finally, we emphasize that the purpose of such simple models is to help gain insights into EMH violations and their causal relationships to the observed statistical properties of real markets.

IV Numerical results

We first select parameters for the model to simulate daily price variations. The time variable is defined in terms of the variance of the external information stream. A daily variance in price returns of 0.6–0.7% suggests a value for of 0.00004. The system properties are independent of the number of agents, for large enough , and appears to be sufficient. The simulations are run for 10000 timesteps which corresponds to approximately 40 years of trading.

The parameter is a measure of the market depth and the relative importance of external noise versus changes in internal supply/demand on the asset price. It is difficult to estimate a priori, but generates price output that is correlated with, but noticably distinct from, the EMH price defined by alone.

The initial thresholds are chosen from the uniform distribution on the interval , corresponding to price moves in the range 10–30%. Simulations have indicated that the models are robust to changes in the exact form of the distribution and so a uniform distribution was chosen. Let us consider first the case where the thresholds are fixed. If and the initial states are sufficiently mixed so that , then as explained in Section III, the model conforms to the EMH and the price is simply

| (3) |

As argued in cgls05 ; ls06 ; b99 , the effect of noise traders (who are not explicitly included) is unlikely to be constant over time. We posit that their number, and therefore also their effect, is greater at times of high sentiment, both positive and negative. This is simulated by increasing the price-changing effect of the external information stream at such times by the use of the function

in (2).

Now let us introduce herding by supposing that for agents in the minority position

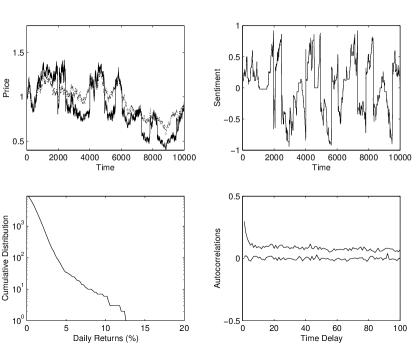

The thresholds are fixed for agents in the majority position. Note that the change in the position of the thresholds is proportional to the length of the timestep and the magnitude of the sentiment. The constant of proportionality is different, but fixed, for each agent and chosen from the uniform distribution on . This range of parameters corresponds to a herding tendency that operates over a timescale of several months or longer. The results of a simulation are shown in Figure 1 and are very similar to those obtained in cgls05 ; ls06 where multiple, fixed thresholds were used.

The top left plot shows both the output price (more volatile) and the EMH pricing obtained from (3) (less volatile). As can be seen there are significant periods of price mismatching. The top right figure plots the sentiment against time. Periods of bullish and bearish sentiments lasting several years can be observed. The bottom left picture shows clear evidence of a fat-tailed distribution in the price returns and this is also confirmed by measures of the excess kurtosis which range from approximately 10–30. Finally, the two curves in the bottom right figure are the autocorrelation decays for both the price returns and their absolute values (the volatility). There is no correlation observable in the price returns, even for lags of a single day, while the volatility autocorelation decays slowly over several months — evidence of volatility clustering. Further numerical testing revealed very similar conclusions to those drawn from the previous fixed-threshold models. These were that, in these models, herding causes fat tails but not volatility clustering since the decay in the volatility autocorrelation vanishes after just a few days when . Also, measurements of power-law exponents similar to those carried out in ls06 provided estimates close to those observed in analyses of price data from real markets.

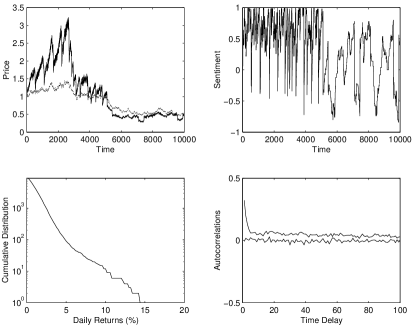

We now suppose that, in addition to the herding and sentiment-dependent volatility, a perverse incentive is in place that makes it advantageous to be in the state . This is achieved by including the following extra rule when an agent is in the state

The value was chosen to make the incentive the same order of magnitude as the herding propensity. The incentive is then switched off after 5000 timesteps. Results for a typical simulation are shown in Figure 2.

The effect of the incentive can be seen in both the price and sentiment variables, where both the average value and the volatility of the variables are increased. This simulation merely serves as a prototype for the kinds of studies that can be performed and more systematic investigations are clearly required in order to draw reliable inferences. These will be reported elsewhere.

V Conclusions

In this paper an agent’s strategy (in the loosest sense of the word) is defined to be a combination of all the rational, inductive learning, psychological and rational-but-perverse factors influencing their decision to switch positions or stay put. We have shown that such strategies can be represented by moving thresholds and can be as simple or as complicated as desired. Indeed the most serious modeling restrictions in the caricature systems simulated above are not in the assumptions behind the moving threshold approach, but in the assumptions made upon the market itself. Giving agents the option to leave the market, a choice of assets, and allowing their strategies to depend upon their current wealth are all obvious first directions in which the models could be extended. However, it seems unlikely that the causal relationships between strategies, as defined above, and global market properties will be understood in complex systems until they are understood in simpler ones.

References

- (1) G.W. Brown. Volatility, sentiment and noise traders. Financial Analysts Journal, pages 82–90, 1999.

- (2) Rama Cont. Empirical properties of asset returns: stylized facts and statistical issues. Quantitive Finance, 1:223–236, 2001.

- (3) Rod Cross, Michael Grinfeld, and Harbir Lamba. A mean-field model of investor behaviour. J. Phys. Conf. Ser., 55:55–62, 2006.

- (4) Rod Cross, Michael Grinfeld, Harbir Lamba, and Tim Seaman. A threshold model of investor psychology. Phys. A, 354:463–478, 2005.

- (5) Rod Cross, Michael Grinfeld, Harbir Lamba, and Tim Seaman. Stylized facts from a threshold-based heterogeneous agent model. Eur. J. Phys. B, 57:213–218, 2007.

- (6) E.F. Fama. Efficient capital markets: A review of theory and empirical work. J. Finance, 25:383–417, 1970.

- (7) H. Lamba and T. Seaman. Market statistics of a psychology-based heterogeneous agent model. Preprint, Econophysics forum.

- (8) T. Lux and M. Marchesi. Volatility clustering in financial markets: A micro-simulation of interacting agents. Int. J. Theor. Appl. Finance, 3:675–702, 2000.

- (9) R. Mantegna and H. Stanley. An Introduction to Econophysics. CUP, 2000.