]Received September 07 2007

Persistence in a Random Bond Ising Model of Socio-Econo Dynamics

Abstract

We study the persistence phenomenon in a socio-econo dynamics model using computer simulations at a finite temperature on hypercubic lattices in dimensions up to 5. The model includes a ‘social’ local field which contains the magnetization at time . The nearest neighbour quenched interactions are drawn from a binary distribution which is a function of the bond concentration, . The decay of the persistence probability in the model depends on both the spatial dimension and . We find no evidence of ‘blocking’ in this model. We also discuss the implications of our results for possible applications in the social and economic fields. It is suggested that the absence, or otherwise, of blocking could be used as a criterion to decide on the validity of a given model in different scenarios.

pacs:

05.20-y, 05.50+q, 75.10.Hk, 75.40.Mg, 89.65.Gh, 89.75.-kI Introduction

The persistence problem is concerned with the fraction of space which persists in its initial state up to some later time . The problem has been extensively studied over the past decade for pure spin systems at both zero [1-4] and non-zero [5] temperatures.

Typically, in the non-equilibrium dynamics of spin systems at zero-temperature, the system is prepared initially in a random state and the fraction of spins, , that persists in the same state as at up to some later time is studied. For the pure ferromagnetic Ising model on a square lattice the persistence probability has been found to decay algebraically [1-4]

where is the non-trivial persistence exponent [1-3]. Derrida et al [4] have shown analytically that for the pure 1d Ising model . The actual value of depends on both the spin [6] and spatial [3] dimensionalities; see Ray [7] for a recent review.

At criticality [5], consideration of the global order parameter leads to a value of for the pure two-dimensional Ising model.

It has been only fairly recently established that systems containing disorder [8-10] exhibit different persistence behaviour to that of pure systems. A key finding [8-9,11] is the appearance of ‘blocking’ regardless of the amount of disorder present in the system. ‘Blocked’ spins are effectively isolated from the behaviour of the rest of the system in the sense that they never flip. As a result, and the key quantity of interest is the residual persistence given by

Note that for the five dimensional pure Ising model without any disorder blocking has also been observed at [3]. At finite temperature there is no evidence of blocking [12].

As well as theoretical models, the persistence phenomenon has also been studied in a wide range of experimental systems and the value of ranges from to [13-15], depending on the system. A considerable amount of the recent theoretical effort has gone into obtaining numerical estimates of for different models [1-11]. Recently, it has been found that the behaviour of the random Ising ferromagnet at zero temperature on a Voronoi-Delaunay lattice [16] is very similar to the behaviour on the diluted ferromagnetic square lattice [8,9].

In this work we add to the knowledge and understanding regarding persistence by presenting the simulation results for the behaviour of a recently proposed spin model which appears to reproduce the intermittency observed in real financial markets [17]. In the next section we discuss the model in detail. In Section III we give an outline of the method used and the values of the various parameters employed. Section IV describes the results and the consequent implications for using the model in a financial or social context. Finally, in Section V there is a brief conclusion.

II The Model

Yamano [16] has proposed a ‘minimalist’ version of the Bornholdt model [18]. We study the persistence phenomenon in the former. In this model one has market traders, denoted by Ising spins , located on the sites of a hypercubic lattice, . The action of the trader of buying or selling a share of a traded stock or commodity at time step corresponds to the spin variable assuming the value or , respectively. Hence, at each time step, a given trader will be either buying or selling. A local field, , determines the dynamics of the spins and, hence, the action of the trader. We follow [16] and assume that

where the first summation runs over the nearest neighbours of only, is a parameter coupling to the absolute magnetization. The nearest neighbour interactions are selected randomly from

where is the concentration of ferromagnetic bonds. The case corresponds to the Edwards-Anderson spin-glass [11]. Each agent is updated according to the following heat bath dynamics:

where is the probability of updating and is temperature. The first term on the right hand side in equation (3) contains the influence of the neighbours and the second term reflects the external environment. The balance between the two terms determines whether an agent buys or sells. If , the agent is equally likely to buy or sell as . If, however, , then and agent is more likely to buy than sell. Similarly, if , then we have and the agent is more likely to sell than buy. and are tunable parameters in our model. The values we select for these are determined by the requirement that the model should be able to reproduce, at least qualitatively, some aspect of actual behaviour observed in a real market. In this model the return is defined in terms of the logarithm of the absolute value of the magnetization, , that is

A key stylised fact observed in real financial markets is the intermittent or ‘bursty’ behaviour in the returns [19]. Simulations [16] in spatial dimensions ranging from to confirm that the above model is able to reproduce the required intermittent behaviour in the returns; see, for example, figure 1 in Yamano [16]. It should be emphasised that intermittency is only observed for certain values of the tunable parameters, and . The temperature, , is defined as the temperature at which intermittency is observed in the returns. Although for all dimensions considered, depending on both and . The values of as determined in [16] were: . A couple of points should be emphasised at this stage. Simulations are performed only on hypercubic lattices where the linear dimension is an odd value. This requirement ensures that the right hand side of equation (6) is well defined. The simulations discussed in the present work were performed in spatial dimensions ranging from to . For each value of , we fine tune the parameters and so that intermittent behaviour is observed in the returns as discussed above. We found that although in all cases, the value of depends on (and also on ) at which intermittency is observed. Our values for and are listed in Table 1. Note that the values of for are consistent with those in [16] but not identical because of finite-size effects.

In our interpretation of the model, a persistent trader is one who doesn’t change his action during the course of the simulation. Hence, we are interested in studying the fraction of traders who have been at time either buying or selling continuously since . Later, we will also suggest a possible interpretation within the context of sociophysics of the model.

III Methodology

| Dimension | ||

|---|---|---|

| 1 | 4000001 | 3.5 |

| 2 | 2001 | 3.0 |

| 3 | 151 | 2.5 |

| 4 | 45 | 1.9 |

| 5 | 21 | 1.4 |

As mentioned in the previous section, for each spatial dimension we first fine tune the temperature to reproduce intermittent behaviour in the returns. As can be seen from Table 1, the temperature decreases with . For a given dimension, all subsequent simulations are performed at that temperature. Averages over at least 100 samples for each run were performed and the error-bars in the following plots are smaller than the data points.

The value of each agent at is noted and the dynamics updated according to equation (3).

At each time step, we count the number of agents that still persist in their initial state by evaluating

Initially, for all . It changes to zero when an agent changes from buying to selling or vice vera for the first time. Note that once , it remains so for all subsequent calculations.

The total number, , of agents who have not changed their action by time is then given by

A fundamental quantity of interest is , the persistence probability. In this problem we can identify with the density of agents continuously buying or selling without interruption since the start [1],

where is the total number of agents present.

IV Results

We now discuss our results. We restrict ourselves to as the problem is symmetric about . It should be noted that we tried various different fits (exponential, power-law, stretched-exponential, etc.) for our data. We will not discuss the fits we discarded as unsatisfactory.

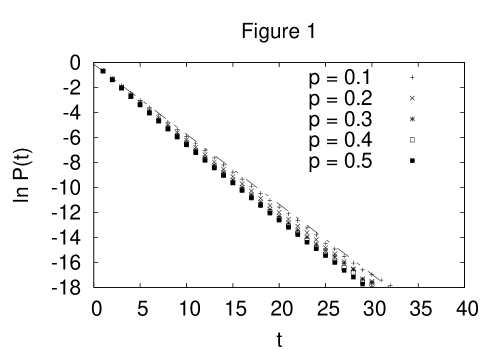

In figure 1 we show a semi-log plot of the persistence probability against time for a range of bond concentrations for . It’s clear from the plot that the data can be fitted to

where we estimate from the linear fit. Note that , independently of .

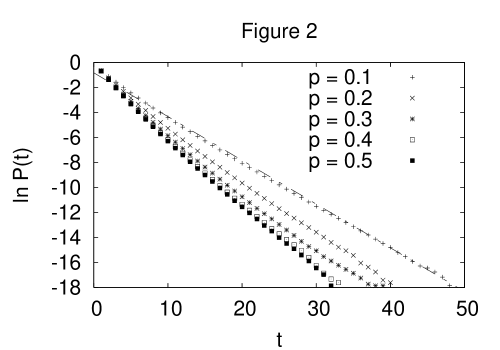

Figure 2 displays the results for . Although, just as for , there is evidence for exponential decay, this time it would appear that the value of the parameter depends on . For we estimate .

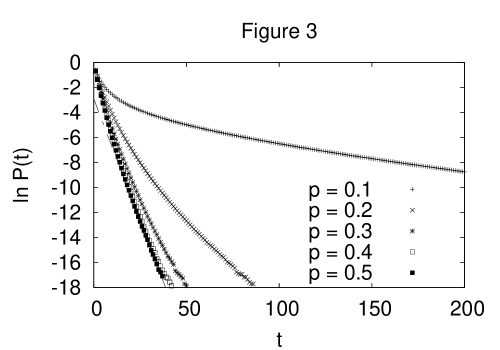

The results for the three-dimensional case are shown in figure 3. Here we see clear evidence that even the qualitative nature of the decay depends on the bond concentration. For we have behaviour very similar to the two cases considered earlier, namely exponential decay. The decay is clearly non-exponential for over the interval considered. A fit to the stretched-exponential is also unsatisfactory even though we have an additional adjustable parameter.

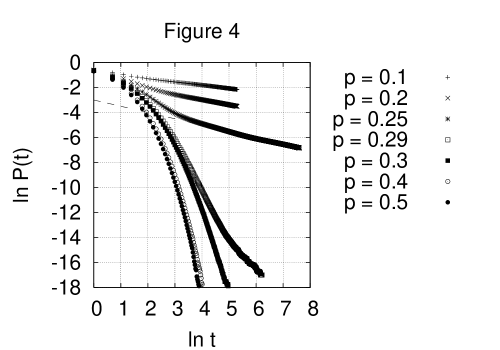

The results in are very similar to those for and we will not present them here. Instead, in figure 4 we show a log-log plot of the persistence against time for . The decay of is seen to be heavily dependent on the concentration of ferromagnetic bonds. For low values of ), we have a power-law decay at long times as given by equation (1) with an estimated value of . For higher value of the decay would appear not to be a power-law but also not exponential in it’s nature. We note that even though we are working with a model containing disorder, no ‘blocking’ is observed in the simulations. This is probably because we are working at a finite temperature and is in agreement with the earlier work on the pure Ising model in high dimensions [3,12].

V Conclusion

To conclude, we have presented the results of extensive simulations for the persistence behaviour of agents in a model capturing some of the features found in real financial markets. Although the model contains bond disorder, we do not find any evidence of ‘blocking’ . This is believed to be because of thermal fluctuations. The persistence behaviour appears to depend on both the spatial dimensionality and the concentration of ferromagnetic bonds. Generally, whereas in low dimensions the decay is exponential, for higher dimensions and low values of we get power-law behaviour.

The initial model was developed in an economic context. Power law persistence in this case means the existence of traders who keep on buying or selling for long durations. Furthermore, the presence of ‘blocking’ would be highly unrealistic for modelling the dynamics because the traders would have access to only a finite amount of capital. Hence, the absence of blocking would suggest that our model is not an unreasonable starting point for further development.

One can also interpret the model in a social context. Here the value or could represent an opinion. Here ‘blocking’ would be realistic and correspond to the proportion of the population that is stubborn and not susceptible to a change. Hence, any model exhibiting exponential decay in the persistence probability would probably be an unrealistic model to use in this scenario.

Hence, we can use the behaviour of the persistence probability as a criterion to decide whether we have a realistic economic or social model.

Acknowledgements.

We thank the referee for his comments on the manuscript and for bringing [12] to our attention. TY thanks L. Pichl for allowing him to use his CPU (mona) at International Christian University, Japan, and acknowledges support by JSPS Grant-in-Aid # 06225. A research grant from Daiwa Foundation Small Grant (Ref: 6124/6356) enabled TY to work as a non-Asian researcher in Birmingham (UK) for six days.References

-

[1] B. Derrida, A. J. Bray and C. Godreche, J. Phys. A: Math Gen 27, L357 (1994).

-

[2] A. J. Bray, B. Derrida and C. Godreche, Europhys. Lett. 27, 177 (1994).

-

[3] D. Stauffer, J. Phys. A: Math Gen 27, 5029 (1994).

-

[4] B. Derrida, V. Hakim and V. Pasquier, Phys. Rev. Lett. 75, 751 (1995); J. Stat. Phys. 85, 763 (1996).

-

[5] S. N. Majumdar, A. J. Bray, S. J. Cornell, C. Sire, Phys. Rev. Lett. 77, 3704 (1996).

-

[6] B. Derrida, P. M. C. de Oliveira and D. Stauffer, Physica 224A, 604 (1996).

-

[7] P. Ray, Phase Transitions 77 (5-7), 563 (2004).

-

[8] S. Jain, Phys. Rev. E59, R2493 (1999).

-

[9] S. Jain, Phys. Rev. E60, R2445 (1999).

-

[10] P. Sen and S. Dasgupta, J. Phys. A: Math Gen 37, 11949 (2004)

-

[11] S. Jain and H. Flynn, Phys. Rev. E73, R025701 (2006)

-

[12] D. Stauffer, Int. J. Mod. Phys. C 8, 361 (1997).

-

[13] B. Yurke, A. N. Pargellis, S. N. Majumdar and C. Sire, Phys. Rev. E56, R40 (1997).

-

[14] W. Y. Tam, R. Zeitak, K. Y. Szeto and J. Stavans, Phys. Rev. Lett. 78, 1588 (1997).

-

[15] M. Marcos-Martin, D. Beysens, J-P Bouchaud, C. Godreche and I. Yekutieli, Physica 214D, 396 (1995).

-

[16] F.W.S. Lima, R.N. Costa Filho and U.M.S. Costa, Journal of Magnetism and Magnetic Materials 270, 182 (2004).

-

[17] T. Yamano, Int. J. Mod. Phys. C 13, 645 (2002).

-

[18] S. Bornholdt, Int. J. Mod. Phys. C 12, 667 (2001)

-

[19] R.N. Mantegna, H.E. Stanley, An Introduction to Econophysics: Correlations and Complexity in Finance, Cambridge University Press, Cambridge (2000).