Nonlinear option pricing models for illiquid markets: scaling properties and explicit solutions

Abstract

Several models for the pricing of derivative securities in illiquid markets are discussed. A typical type of nonlinear partial differential equations arising from these investigation is studied. The scaling properties of these equations are discussed. Explicit solutions for one of the models are obtained and studied.

keywords:

Nonlinear Black-Scholes model , lliquid markets , exact invariant solutionsurl]http://www2.hh.se/staff/ljbo/

url]www.math.uni-leipzig.de/ frey

AMS subject classification.

35K55, 22E60, 34A05

1 Introduction

Standard derivative pricing theory is based on the assumption of frictionless and perfectly liquid markets. In particular, it is assumed that all investors are small relative to the market so that they can buy arbitrarily large quantities of the underlying assets without affecting its price (perfectly liquid markets). Given the scale of hedging activities on many financial markets this is clearly unrealistic. Hence in recent years a number of approaches for dealing with market illiquidity in the pricing and the hedging of derivative securities have been developed. The financial framework that is being used differs substantially between model classes. However, as shown in Section 2 below, in all models derivative prices can be characterized by fully nonlinear versions of the standard parabolic Black-Scholes PDE. Moreover, these nonlinear Black-Scholes equations have a very similar structure. This makes these nonlinear Black-Scholes equations a useful reference point for studying derivative asset analysis under market illiquidity. In Sections 3 we therefore study scaling properties and compute explicit solutions for a typical fully nonlinear Black-Scholes equation; Section 4 is devoted to studying properties of solutions and sensitivities with respect to model parameters. The relevant literature is discussed in the body of the paper.

2 Illiquid markets and nonlinear Black-Scholes equations

In order to motivate the subsequent analysis we present a brief synopsis of three different frameworks for modeling illiquid markets. We group them under the labels a)transaction-cost models; b) reduced-form SDE-models; c) reaction-function or equilibrium models. In particular, we show that the value function of a certain type of selffinancing strategies (so called Markovian strategies) must be a solution of a fully nonlinear version of the standard Black-Scholes equation. In all models there will be two assets, a risk-free money-market account which is perfectly liquid and a risky and illiquid asset (the stock). Without loss of generality, we use the money market account as numeraire; hence , and interest rates can be taken equal to zero.

(Quadratic) transaction-cost models. The predominant model in this class has been put forward by Cetin, Jarrow and Protter [7]. In this model there is a fundamental stock price process following geometric Brownian motion,

| (2.1) |

for constants , and a standard Brownian motion . The transaction price to be paid at time for trading shares is

| (2.2) |

where is a liquidity parameter.

Intuitively, in the model (2.2) a trader has to pay a spread whose size relative to the fundamental price, , depends on the amount which is traded. As shown by [7], this leads to transaction costs which are proportional to the quadratic variation of the stock trading strategy. In order to formulate this statement more precisely we consider a selffinancing trading strategy giving the number of stocks and the position in the money market for predictable stochastic processes and . The value of this strategy at time equals .

Consider now a Markovian strategy, i.e. a trading strategy of the form for a smooth function . In this case is a semimartingale with quadratic variation given by

see for instance Chapter 2 of [22]. Then Theorem A3 of [7] yields the following dynamics of

| (2.3) |

Note that according to (2.3), the market impact of the large trader leads to an extra transaction-cost term of size in the wealth dynamics.

Suppose now that and are smooth functions such that gives the value of a selffinancing trading strategy with stock position . According to the Itô formula, the process has dynamics

Comparing this with (2.3), using the uniqueness of semimartingale decompositions it is immediate that must satisfy the PDE and that moreover . The last relation gives , so that we obtain the following nonlinear PDE for

| (2.4) |

When pricing a derivative security with maturity date and payoff for some function we have to add the terminal condition , . For instance, in case of a European call option with strike price we have .

Note that the original paper [7] goes further in the analysis of quadratic transaction cost models. To begin with, a general framework is proposed that contains (2.2) as special (but typical) case. Moreover, conditions for absence of arbitrage for a general class of trading strategies - containing Markovian trading strategies as special case - are given, and a notion of approximative market completeness is studied.

Reduced-form SDE models. Under this modeling approach it is assumed that investors are large traders in the sense that their trading activity affects equilibrium stock prices. More precisely, given a liquidity parameter and a semimartingale representing the stock trading strategy of a given trader, it is assumed that the stock price satisfies the SDE

| (2.5) |

The intuitive interpretation is as follows given that the investor buys (sells) stock () the stock price is pushed (downward) upward by ; the strength of this price impact depends on the parameter . Note that for the asset price simply follows a Black-Scholes model with reference volatility . The model (2.5) is studied among others in [10], [11], [14] or [18].

In the sequel we denote the asset price process which results if a large uses a particular trading strategy by . Suppose as before that the trading strategy is Markovian, i.e. of the form for a smooth function . Applying the Itô formula to (2.5) shows that is an Itô process with dynamics

with adjusted volatility given by

| (2.6) |

see for instance [10] for details. In the model (2.5), a portfolio with stock trading strategy and value is termed selffinancing, if satisfies the equation . Note that the form of the strategy affects the dynamics of ; this feedback effect will give rise to nonlinearities in the wealth dynamics as we now show. Suppose that and for smooth functions and . As before, applying the Itô formula to the process yields . Moreover, must satisfy the relation . Using (2.6) and the relation we thus obtain the following fully nonlinear PDE for

| (2.7) |

Again, for pricing derivative securities a terminal condition corresponding to the particular payoff at hand needs to be added.

Equilibrium or reaction-function models. Here the model primitive is a smooth reaction function that gives the equilibrium stock price at time as function of some fundamental value and the stock position of a large trader. A reaction function can be seen as reduced-form representation of an economic equilibrium model, such as the models proposed in [12], [21] or [23]. In these models there are two types of traders in the market: ordinary investors and a large investor. The overall supply of the stock is normalized to one. The normalized stock demand of the ordinary investors at time is modelled as a function where is the proposed price of the stock. The normalized stock demand of the large investor is written the form ; is a parameter that measures the size of the trader’s position relative to the total supply of the stock. The equilibrium price is then determined by the market clearing condition

| (2.8) |

Under suitable assumptions on equation (2.8) admits a unique solution, hence can be expressed as a function of and , i.e. . For instance we have in [21] ; the model used in [12] and [25] leads to the reaction function The reaction-function approach is also used in [15] and in [9].

Now we turn to the characterization of selffinancing hedging strategies in reaction-function models. Throughout we assume that the fundamental-value process follows a geometric Brownian motion with volatility (see (2.1)). Moreover, we assume that the reaction function is of the form for some increasing function . This holds for the specific examples introduced above and, more generally, for any model where for a strictly increasing function with suitable range.

Assuming as before that the normalized trading strategy of the large trader is of the form for a smooth function we get from Itô’s formula, since ,

the precise form of is irrelevant for our purposes. Rearranging and integrating the expression over both sides of this equation gives the following dynamics of :

| (2.9) |

Remark 2.1

A very general analysis of the dynamics of selffinancing strategies in reaction-function models (and generalizations thereof) using the Itô-Wentzell formula can be found in [1].

A similar reasoning as in the case of the reduced-form SDE models now gives the following PDE for the value function of a selffinancing strategy

| (2.10) |

In particular, for we have and (2.10) reduces to equation (2.7); for as in [12], [25], we get the PDE

| (2.11) |

Nonlinear Black-Scholes equations. The nonlinear PDEs (2.4), (2.7) , (2.10) and (2.11) are all of the form

| (2.12) |

where . Since is often considered to be small, it is of interest to replace with its first order Taylor approximation around . It is immediately seen that for the equations (2.7) and (2.11) this linearization is given by replacing with this first order Taylor approximation in (2.7) and (2.11) thus immediately leads to the PDE (2.4).

Note that (2.12) is a fully nonlinear equation in the sense that the coefficient of the highest derivative is a nonlinear function of this derivative. A similar feature can be observed for the limiting price in certain transaction cost models under a proper rescaling of transaction cost and trading frequency; see for instance [2]. Nonlinear PDEs for incomplete markets obtained via exponential utility indifference hedging such as [3] or [19] on the other hand are quasi-linear equations in the sense that the highest derivative enters the equation in a linear way, similar to the well-known reaction-diffusion equations arising in physics or chemistry. From an analytical point of view the nonlinearities arising in both cases are quite different. In the latter quasi-linear case we have to do with a regular perturbation of the classical Black-Scholes (BS) equation but in the case (2.10) we have to do with singular perturbation, meaning that the highest derivative is included in the perturbation [16]. In case of a regular perturbation it is typical to look for a representation of a solutions to a quasi-linear equation in the form

| (2.13) |

For many forms of nonlinearities the uniform convergence as of the expansions of type (2.13) can be established. If the perturbation is of the singular type, the asymptotic expansion of type (2.13) typically breaks down for some and some . It can as well happens that the definition domain for the solutions of type (2.13) include just one point or that it is empty. It is very important to obtain explicit solutions for such models because in these case we can not hope to get good approximations for solutions by expansions of the type (2.13) in the whole region.

3 Invariant Solutions for a Nonlinear Black-Scholes Equation

Our goal in this section is to investigate the nonlinear Black-Scholes equation (2.7) using analytical methods. As we have just seen, this equation is typical for the nonlinearities arising in pricing equations for derivatives in illiquid markets in general.111Our approach can be applied to equations (2.4) and (2.11) as well; see [4, 24] for details. Using the symmetry group and its invariants the partial differential equation (2.7) can be reduced in special cases to ordinary differential equations. In [6] a special family of invariant solutions to the equation (2.7) was studied; in particular, the explicit solutions were used as test case for various numerical methods. In the present paper we study all invariant solutions to equation (2.7).

3.1 General Results

In order to describe the symmetry group of (2.7) we use results from Bordag [5]. In that paper the slightly more general equation

| (3.14) |

with a continuous function is studied (note that for this equation reduces to (2.7)) and the following theorem was proved.

Theorem 3.1

The proof is based on methods of Lie point symmetries, i.e. the Lie symmetry algebras and groups to the corresponding equations were found; see [5] for details and [17, 20, 13] for a general introduction to the methodology. As we will see later, the solutions found in [5] for the case can be used to obtain the complete set of invariant solutions to equation (2.7).

For with we can use (3.19) to obtain a new independent invariant variable and (3.21) to obtain a new dependent variable ; these variables are given by

| (3.22) |

Using these variables we can reduce the partial differential equation (3.18) to the ordinary differential equation

| (3.23) |

where It is a straightforward consequence of Theorem 3.1 that these are the only nontrivial invariant variables. In the sequel we will determine explicit solutions for (3.23) for the case which corresponds to the original equation (2.7).

Remark 3.1

Equation (3.23) with and are related to each other. Note however, that the relation between the corresponding solutions is not so straightforward, because (3.23) is nonlinear and we need real valued solutions. Hence the results from [5] - where (3.23) was studied for the case - do not carry over directly to the present case , so that a detailed analysis of the case is necessary.

To find families of invariant solution we introduce a new dependent variable

| (3.24) |

If we assume that the denominator of the equation (3.23) is different from zero, we can multiply both terms of equation (3.23) by the denominator of the second term and obtain

| (3.25) |

We denote the left hand side of this equation by . The equation (3.25) can possess exceptional solutions which are the solutions of a system

| (3.26) |

The first equation in this system defines a discriminant curve which has the form

| (3.27) |

If this curve is also a solution of the original equation (3.25) then we obtain an exceptional solution to equation (3.25). We obtain an exceptional solution if , i.e. . It has the form

| (3.28) |

This solution belongs to the family of solutions (3.30) by the specified value of the parameter . In all other cases the equation (3.25) does not possess any exceptional solutions.

Hence the set of solutions of equation (3.25) is the union of the solution sets of following equations

| (3.29) | |||||

| (3.30) | |||||

| (3.31) | |||||

| (3.32) |

where one of the solutions (3.30) is an exceptional solution (3.28) by for . In case we have so that solutions of (3.30) are complex valued functions. We denote the right hand side of equations (3.31), (3.32) by . The Lipschitz condition for equations of the type is satisfied in all points where the derivative exists and is bounded. It is easy to see that this condition will not be satisfied by

| (3.33) |

Hence on the lines (3.33) the uniqueness of solutions of equations (3.31), (3.32) can be lost. We will study in detail the behavior of solutions in the neighborhood of the lines (3.33). For this purpose we look at the equation (3.25) from another point of view. If we assume now that are complex variables and denote

| (3.34) |

then the equation (3.25) takes the form

| (3.35) |

where The equation (3.35) is an algebraic relation in and defines a plane curve in this space. The polynomial is an irreducible polynomial if at all roots of either the partial derivative or are non equal to zero. It is easy to prove that the polynomial (3.35) is irreducible.

We can treat equation (3.35) as an algebraic relation which defines a Riemannian surface of as a compact manifold over the -sphere. The function is uniquely analytically extended over the Riemann surface of two sheets over the sphere. We find all singular or branch points of if we study the roots of the first coefficient of the polynomial , the common roots of equations

| (3.36) |

and the point The set of singular or branch points consists of the points

| (3.37) |

As expected we got the same set of points as in real case (3.33) by the

study of the Lipschitz condition but now the behavior of solutions at the

points is more visible.

The points are the branch points at which two sheets of are glued on. We remark that

| (3.38) |

where is a local parameter in the neighborhood of For the special value of , i.e. k=0, the value is equal to zero.

At the point we have

where is a local parameter in the neighborhood of At the point the function has the following behavior

| (3.39) | |||||

| (3.40) | |||||

| (3.41) |

Any solution of an irreducible algebraic equation (3.35) is meromorphic on this compact Riemann surface of the genus 0 and has a pole of the order one correspondingly (3.39) over the point and the pole of the second order over . It means also that the meromorphic function cannot be defined on a manifold of less than 2 sheets over the sphere.

To solve differential equations (3.31) and (3.32) from this point of view it is equivalent to integrate on a differential of the type and then to solve an Abel’s inverse problem of degenerated type

| (3.42) |

The integration can be done very easily because we can introduce a uniformizing parameter on the Riemann surface and represent the integral (3.42) in terms of rational functions merged possibly with logarithmic terms.

To realize this program we introduce a new variable (our uniformizing parameter ) in the way

| (3.43) | |||||

| (3.44) |

Then the equations (3.31) and (3.32) will take the form

| (3.45) | |||

| (3.46) |

The integration procedure of equations (3.45), (3.46) gives rise to relations defining a complete set of first order differential equations. In order to see that these are first order ordinary differential equations recall that from the substitutions (3.34) and (3.24) we have

| (3.47) |

We summarize all these results in the following theorem.

Theorem 3.2

The equation (3.23) for arbitrary values of the parameters can be reduced to the set of first order differential equations which consists of the equations

| (3.48) |

and equations (3.31), (3.32) where is defined by the substitution (3.24). The complete set of solutions of the equation (3.23) coincides with the union of solutions of these equations.

To solve equations (3.45), (3.46) exactly we have first to integrate and then invert these formulas in order to obtain an exact representation of as a function of . If an exact formula for the function is found we can use the substitution (3.47) to obtain an explicit ordinary differential equation of the type or another suitable type; in that case it is possible to solve the problem completely. However, for an arbitrary value of the parameter inversion is impossible, and we have just an implicit representation for the solutions of the equation (3.23) as solutions of the implicit first order differential equations.

3.2 Exact invariant solutions for a fixed relation between and

For a special value of the parameter , namely for , we can integrate and invert the equations (3.45) and (3.46). For the relation between the variables and is fixed in the form

| (3.49) |

equation (3.45) takes the form

| (3.50) |

and correspondingly the equation (3.46) becomes

| (3.51) |

where an arbitrary constant. It is easy to see that the equations (3.50) and (3.51) are connected by a transformation

| (3.52) |

This symmetry arises from the symmetry of the underlining Riemann surface (3.35) and corresponds to a change of the sheets on . Using these symmetry properties we can prove following theorem.

Theorem 3.3

The second order differential equation

| (3.53) |

is exactly integrable for any value of the parameter . The complete set of solutions for is given by the union of solutions (3.2), (3.2) -(3.2) and solutions

| (3.54) |

where is an arbitrary constant. The last solution in (3.54) corresponds to the exceptional solution of equation (3.25).

For equation (3.53) is linear and its solutions are given by , where are arbitrary constants.

Proof. Because of the symmetry (3.52) it is sufficient to study either the equations (3.50) or (3.51) for or both these equations for . The value can be excluded because it complies with the constant value of and correspondingly constant value of , but all such cases are studied before and the solutions are given by (3.54).

We will study equation (3.51) in case and obtain on this way the complete class of exact solutions for equations (3.50)-(3.51) and on this way for the equation (3.53).

Equation (3.51) for has a one real root only. It leads to an ordinary differential equation of the form

| (3.55) | |||||

Equation (3.55) can be exactly integrated if we use an Euler substitution and introduce a new independent variable

| (3.56) |

The corresponding solution is given by

where is an arbitrary constant. If in the right hand side of equation (3.51) the parameter satisfies the inequality and the variable chosen in the region

| (3.58) |

then the equation on possesses maximal three real roots. These three roots of cubic equation (3.51) give rise to three differential equations of the type . The equations can be exactly solved and we find correspondingly three solutions .

The first solution is given by the expression

where is an arbitrary constant. The second solution is given by the formula

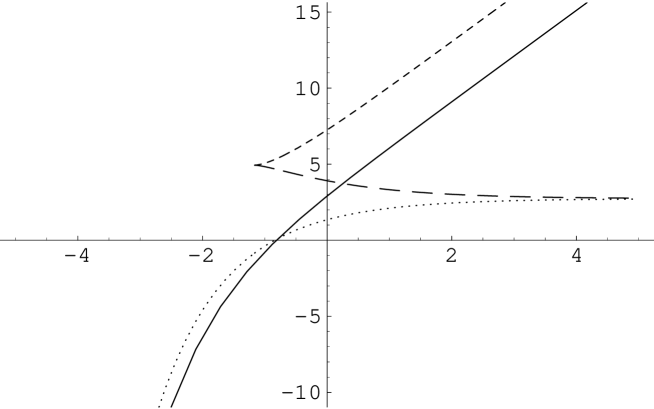

where is an arbitrary constant. The first and second solutions are defined up to the point where they coincide (see Fig. 1).

The third solution for is given by the formula

where is an arbitrary constant. In case the polynomial (3.51) has a one real root and the corresponding solution can be represented by the formula

The third solution is represented by formulas and for different values of the variable .

One of the sets of solutions (3.2), (3.2) -(3.2) for fixed parameters is represented in Fig. 1. The first solution (3.55) and the third solution given by both (3.2) and (3.2) are defined for any values of . The solutions and cannot be continued to the left after the point where they coincide.

If we keep in mind that and we can represent the complete set of exact invariant solution of equation (2.7). The solution (3.2) gives rise to an invariant solution in the form

where , . This solution was obtained and studied in [6]. We describe now other invariant solutions from the complete set of invariant solutions.

In case we can obtain correspondingly three real solutions if

| (3.64) |

The first solution is represented by

| (3.65) | |||

where , . The second solution is given by the formula

where , . The first and second solutions are defined for the variables under conditions (3.64). They coincide along the curve

and cannot be continued further. The third solution is defined by

where and satisfied the condition (3.64).

In case the third solution can be represented by the formula

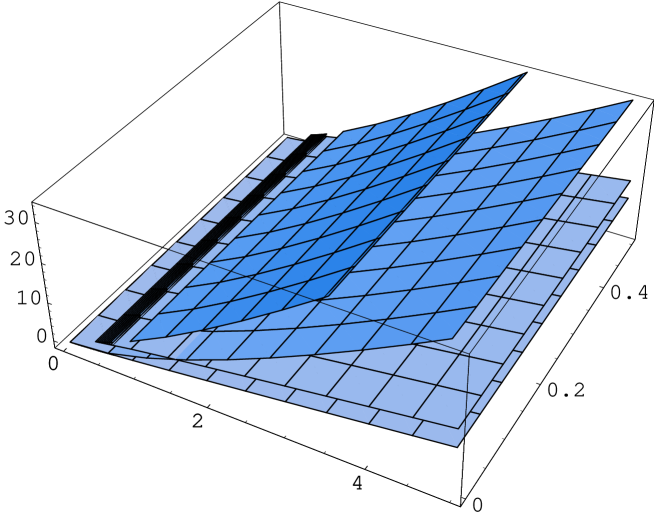

where The solution (3.2) and the third solution given by , (3.2),(3.2) are defined for all values of variables and . They have a common intersection curve of the type . The typical behavior of all these invariant solutions is represented in Fig. 2.

The previous results we summarize in the following theorem which describes the set of invariant solutions of equation (2.7).

Theorem 3.4

The invariant solutions of equation (2.7) can be defined

by the set of first order ordinary differential equations

listed in Theorem 3.2.

If moreover the

parameter , or equivalent in the substitution (3.22) we chose

then the complete set of invariant solutions of

(2.7) can be found exactly. This set of invariant

solutions is given by formulas (3.2)–(3.2) and by

solutions

where is an arbitrary constant. This set of invariant solutions is unique up to the transformations of the symmetry group given by Theorem 3.1.

The solutions , (3.2), , (3.65), , (3.2), ,(3.2), (3.2), have no one counterpart in a linear case. If in the equation (2.7) the parameter equation becomes linear. If the parameter then equation (2.7) and correspondingly equation (3.18) will be reduced to the linear Black-Scholes equation but solutions (3.2)-(3.2) which we obtained here will be completely blown up by because of the factor in the formulas (3.2)-(3.2). This phenomena was described as well in [6], [8] where the solution was studied and for the complete set of invariant solutions of equation (3.18) with in [5].

4 Properties of solutions and parameter-sensitivity

We study the properties of solutions, keeping in mind that because of the symmetry properties (see Theorem 3.1) of the equation (2.7) we can add to each solution a linear function of .

4.1 Dependence on the constant and terminal payoff

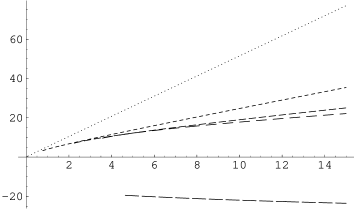

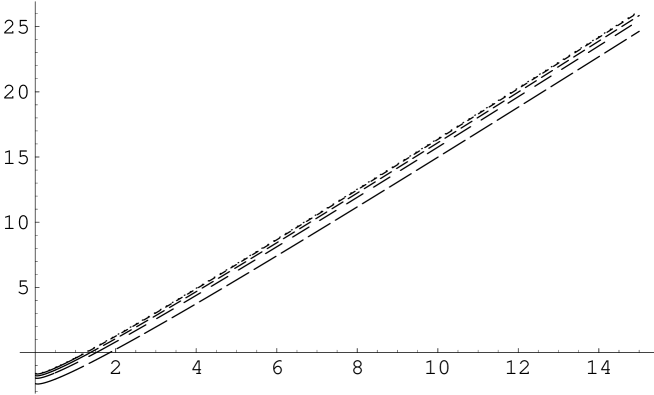

First we study the dependence of the solution on the arbitrary constant . The constant is the first constant of integration of the ordinary differential equations (3.31), (3.32). This dependence is illustrated in Figure 4.

The curves going from up to down with the growing value of the parameter .

The curves going from up to down with the growing value of the parameter .

We see on Fig. 4 that for different values of the constant the domains of the solutions are different. The dependence of the solutions on the constant is exemplified in Figure 4.

We obtain a typical terminal payoff function for the solutions (3.2)-(3.2) if we just fix . By changing the value of the constant and by adding a linear function of we are able to modify terminal payoff function for the solutions. Hence we can approximate typical payoff profiles of financial derivatives quite well.

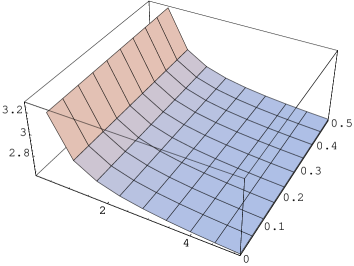

4.2 Dependence on time

All solutions depend weakly on time because of the substitution (3.49) all invariant solutions depends on the combination . As long as we take the volatility to be small we obtain a dampened dependence of the solutions on time.

In Fig. 5 we can see this dependence for examples of the solution .

The highest level corresponds to and the lowest to .

4.3 Dependence on the parameter

All solutions found in this paper have the form

| (4.69) |

where is a smooth function of . Hence the function solves the equation (2.7) with ,

| (4.70) |

Because of this relation any -dependence of invariant solutions of (2.7) trivial. In particular, if the terminal conditions are fixed, , then the value will increase if the value of the parameter increases. This dependence of hedge costs on the position of the large trader on the market is very natural.

4.4 Dependence on the asset price

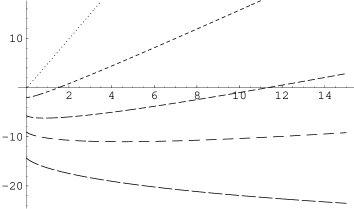

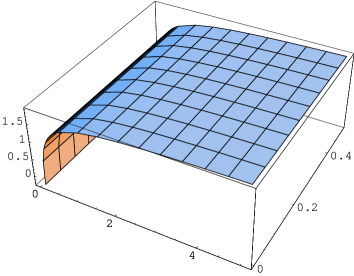

In practice one use often delta-hedging to reduce the sensitivity of a portfolio to the movements of an underlying asset. Hence it is important to know the value defined by where denotes the value of the derivative product or of a portfolio. Using the exact formulas for the invariant solutions we can easily calculate as a function of and . The corresponding to the solution is presented in Fig. 7

The of the solution is represented on the

Fig. 7.

We see in both cases the strong dependence on for small value

of . If , in both cases the tends to a constant which is

independent of time and the constant .

4.5 Asymptotic behavior of invariant solutions

If is large enough we have four well defined solutions , , , . The asymptotic behavior solutions from (3.2) and from (3.65) coincides in the main terms as and is given by the formula

| (4.71) |

The exact formula for the asymptotic behavior of the function for is given by

| (4.72) | |||||

We see that for , the main term does not depend on time or on the value of the constant . Moreover, this term cannot be changed by adding a linear function of to the solution.

The main terms of the solutions from (3.2) and from (3.2) behave similar to each other as ; this behavior is given by the formulas

and

| (4.74) | |||||

| (4.75) |

Note that the main term in formulas (4.5) and (4.74) depends on linearly and has a coefficient which depends on the constant only. Hence we can change the asymptotic behavior of the solutions and , by simply adding a linear function of to the solutions.

For in a neighborhood of there exist just two non trivial real invariant solutions of equation (2.7), i.e. the known solution and the new solution . Using the exact formulas for the last solution we retain the first term and obtain as for the solution

| (4.76) |

The main term in this formula do not depend on or constant and can be changed by adding a linear function of to the solution.

5 Conclusion

In this paper we have obtained explicit solutions for the equation (2.7) and studied their analytical properties. These solutions are useful for a number of reasons. To begin with, while the payoffs of these similarity solutions cannot be chosen arbitrary, the payoffs can be modified using embedded constants to tailor a given portfolio reasonably well. For some values of the parameters we obtain a payoff typical for futures, for other values the payoff is very similar to the form of calls (see Figure 4 and Figure 4). Moreover, the explicit solutions can be used as benchmark for different numerical methods.

An important difference between the case of the linear Black-Scholes equation and these nonlinear cases can be noticed if we consider the asymptotic for . In the linear case the price of a Call option satisfies . In the nonlinear case the families of similarity solutions and which approximate the payoff of a Call option well on a finite interval , grow faster than linear as ; see the formulas (4.5) and (4.74) for details. This reflects the fact that in illiquid markets option hedging is more expensive than in the standard case of perfectly liquid markets.

6 Acknowledgements

The authors are grateful to Albert N. Shiryaev for the interesting and fruitful discussions.

References

- [1] P. Bank and D. Baum. Hedging and portfolio optimization in financial markets with a large trader. Math. Finance, 14:1–18, 2004.

- [2] G. Barles and M. Soner. Option pricing with transaction costs and a nonlinear Black-Scholes equation. Finance Stoch., 2:369–397, 1998.

- [3] D. Becherer. Utility indifference hedging and valuation via reaction-diffusion systems. R. Soc. Lond. Proc. Ser. A Math. Phys. Eng. Sci., 460:27–51, 2004.

- [4] M. V. Bobrov. The fair price valuation in illiquid markets. Master’s Thesis in Financial Mathematics, Technical report IDE0738, Halmstad University, Sweden, 2007.

- [5] L. A. Bordag. On the valuation of a fair price in case of an non perfectly liquid market. Proceedings of the Workshop on Mathematical Control Theory and Finance, Lisbon, 10-14 April, 2007. (working paper version entitled ‘Symmetry reductions of a nonlinear model of financial derivatives’, arXiv:math.AP/0604207, 09.04.2006).

- [6] L. A. Bordag and A. Y. Chmakova. Explicit solutions for a nonlinear model of financial derivatives. International Journal of Theoretical and Applied Finance, 10:1–21, 2007. No. 1.

- [7] U. Cetin, R. Jarrow, and P. Protter. Liquidity risk and arbitrage pricing theory. Finance Stoch., 8:311–341, 2004.

- [8] A. Y. Chmakova. Symmetriereduktionen und explizite Lösungen für ein nichtlineares Modell eines Preisbildungsprozesses in illiquiden Märkten. PhD thesis, BTU Cottbus, Germany, 2005.

- [9] R. Frey. Perfect option replication for a large trader. Finance Stoch., 2:115–148, 1998.

- [10] R. Frey. Market illiquidity as a source of model risk in dynamic hedging. In R. Gibson, editor, Model Risk, pages 125–136. Risk Publications, London, 2000.

- [11] R. Frey and P. Patie. Risk management for derivatives in illiquid markets: a simulation study. In K. Sandmann and P. Schönbucher, editors, Advances in Finance and Stochastics. Springer, Berlin, 2002.

- [12] R. Frey and A. Stremme. Market volatility and feedback effects from dynamic hedging. Math. Finance, 7(4):351–374, 1997.

- [13] Nail H. Ibragimov. Elementary Lie Group Analysis and Ordinary Differential Equations. John Wiley & Sons, Chichester, USA, 1999.

- [14] M. Jandačka and D. Ševčovi ̌c. On the risk-adjusted pricing-methodology-based valuation of vanilla options and explanation of the volatility smile. Journal of Applied Mathematics, 3:253–258, 2005.

- [15] R.A. Jarrow. Derivative securities markets, market manipulation and option pricing theory. J. Finan. Quant. Anal., 29:241–261, 1994.

- [16] Robin Stanley Johnson. Singular perturbation theory:. Mathematical and analytical techniques with applications to engineering. Springer, New York, 2004.

- [17] Sophus Lie. Vorlesungen über Differentialgleichungen mit bekannten infinitesimalen Transformationen. Teubner, Leipzig, 1912.

- [18] H. Liu and J. Yong. Option pricing with an illiquid underlying asset market. Journal of Economic Dynamics and Control, 29(12):2125–2156, 2005.

- [19] M. Musiela and T. Zariphopoulou. An example of indifference prices under exponential preferences. Finance and Stochastics, 8:229–239, 2004.

- [20] P. J. Olver. Application of Lie groups to differential equations. Springer-Verlag, New York, USA, 1986.

- [21] E. Platen and M. Schweizer. On feedback effects from hedging derivatives. Math. Finance, 8:67–84, 1998.

- [22] P. Protter. Stochastic Integration and Differential Equations: A New Approach. Applications of Mathematics. Springer, Berlin, 1992.

- [23] P. Schönbucher and P. Wilmott. The feedback-effect of hedging in illiquid markets. SIAM J. Appl. Math., 61:232–272, 2000.

- [24] N. Sergeeva. The feedback effects in illiquid markets, hedging strategies of large traders. Master’s Thesis in Financial Mathematics, Technical report IDE0741, Halmstad University, Sweden, 2007.

- [25] R. Sircar and G. Papanicolaou. General Black-Scholes models accounting for increased market volatility from hedging strategies. Appl. Math. Finance, 5:45–82, 1998.