Fine-tune your smile

Correction to Hagan et al

Abstract.

Using results derived in Berestycki et al. [1] we correct the celebrated formulae of Hagan et al. [5, 4]. We derive explicitly the correct zero order term in the expansion of the implied volatility in time to maturity. The new term is consistent as . Furthermore, numerical simulations show that it reduces or eliminates known pathologies of the earlier formula.

We discuss here111 The present note originated from a seminar I co-organised at Imperial College London in 2006/2007. I take the opportunity to thank Dr Mijatović and all the participants for fruitful discussions. the celebrated formulae of Hagan and Woodward [5] and Hagan et al. [4], point out some inconsistencies and compare them with the results of Berestycki et al. [1]. This leads to a new corrected version of the original formula derived in [4]. This is a short technical paper and the reader is assumed to be familiar with the SABR model and asymptotic expansions of the implied volatility surface. We refer to Gatheral [3, Chp.7] for background.

Consider the following model for the underlying (we take which should be interpreted as representing the forward value process)

| (1) |

, , which is known as the SABR model. The model (1) is written in the pricing measure under which are correlated Brownian motions. We take and note that putting we obtain a local volatility model. We refer interchangeably to strike or to . The implied volatility is denoted , i.e. a European call with strike and time to maturity has the same price under the SABR model (1) and under the Black-Scholes model with volatility .

Consider now the Taylor expansion of the implied volatility surface in time to maturity

| (2) |

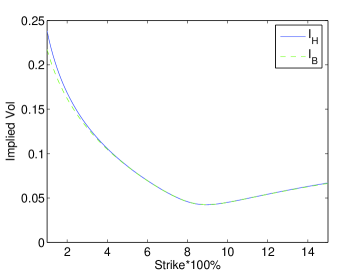

Hagan et al. [4] were first to obtain explicit expressions for and . They used perturbation theory (combined with impressive intuition). More recently, Berestycki et al. [1] treated the subject in a rigorous analytical manner. They proved in particular that is well defined and characterized it via a solution to eikonal equation (or via Varadhan’s signed geodesic distance). Direct, but somewhat tedious, computations allow us to compare their expression for with that of [4] and of [5] (case of ). The findings are summarised in Table 1.

The formula for in the local volatility case agrees in both works and appears to be correct. We note however that it differs from the formula in Hagan and Woodward [5]. Numerically the difference is small but persistent. Unfortunately, it is the formula in [5] which is often used, as in Bourgade and Croissant [2].

The formula for when is the same in [4] and in [1]. However the two papers differ222Note there is a typo in (6.5) in [1] which we corrected here. when and we believe it is the formula of [1] which is correct333Strictly speaking Hagan et al. [4] do not claim to obtain the Taylor expansion in maturity, however their formula (A.65) is of the form (2). and should be used. This is natural as authors in [1] present an analytic treatment of the subject and characterize theoretically. Furthermore, the form of their formula we derived here coincides with the general formula obtained by Labordère [6, Eq. (5.1)] (taken for the case of -SABR). We give now two arguments in favor of the formula of [1]: theoretical and numerical.

From the theoretical point of view, the formula of Hagan et al. [4] has an internal flaw: it is inconsistent as . Indeed, in the formula of [4] does not converge to the known value for as .444However, when one uses the simplified formula (2.17a), which is (A.69c), instead of the general formula (A.65), the convergence issue (magically) disappears. In contrast, as

we have convergence using the formula of [1].

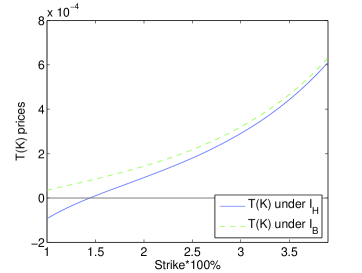

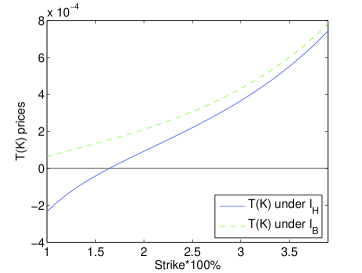

The formula of Hagan et al. [4] is known to produce wrong prices in region of small strikes for large maturities. It assigns a negative price to a structure with a positive payoff, or equivalently it implies a negative probability density for the stock price process in some region. If one uses the formula we derive here the problem either appears in yet lower strikes or disappears completely. To see this, we price the following structure in interest rates: long put and short put at three times the notional, whose payoff is a triangle, zero at zero and at and with a peak at . We denote it . More generally, is the following: long put and short put at times notional. The payoff of is a triangle, zero at zero and at , with a peak at .

Let and be the formulae for from [4] and [1] respectively. The implied volatility in [4, Eq. (A.65)] is given via

| (3) |

and we define the implied volatility , as we did not derive an explicit formulae for from [1]. An explicit formula for , albeit complicated, is derived in Labordère [6], who also argues that is a valid approximation.

, , , ,

, , , ,

Figures compare the prices of the structure derived using and . The anomalies do not occur, or occur at lower strikes, if we price using the implied volatility instead of .

References

- [1] H. Berestycki, J. Busca, and I. Florent. Computing the implied volatility in stochastic volatility models. Comm. Pure Appl. Math., 57(10):1352–1373, 2004.

- [2] P. Bourgade and O. Croissant. Heat kernel expansion for a family of stochastic volatility models: geometry. arXiv:cs/051102, 2006.

- [3] J. Gatheral. The Volatility Surface. Wiley, 2006.

- [4] P. S. Hagan, D. Kumar, A. S. Lesniewski, and D. E. Woodward. Managing smile risk. Wilmott Magazine, pages 84–108, July 2002.

- [5] P. S. Hagan and D. E. Woodward. Equivalent Black volatilities. Applied Math Finance, 6:147–157, 1999.

- [6] P. H. Labordère. A general asymptotic implied volatility for stochastic volatility models. arXiv:cond-mat/0504317, 2005.