The Local Fractal Properties of the Financial Time Series on the Polish Stock Exchange Market

Abstract

We investigate the local fractal properties of the financial time series based on the evolution of the Warsaw Stock Exchange Index (WIG) connected with the largest developing financial market in Europe. Calculating the local Hurst exponent for the WIG time series we find an interesting dependence between the behavior of the local fractal properties of the WIG time series and the crashes appearance on the financial market.

The models and mechanisms enabling to predict the future behavior of

the financial market on a long or short term period are a big

challenge in the financial engineering and very recently also in

econophysics. In the latter case one believes that the approach

based on the analogy of the financial market with the complex

dynamical system could be very fruitful [1]–[8]. In

particular, the scale invariance of the complex systems is used to

reveal the log-periodic oscillations characteristic for these

systems before the phase transition point is reached. The

log-periodic oscillations preceding the crashes or ruptures points,

i.e. the moments when the increasing long-term trend is being

broken and starts to reverse, have really been observed for the

market indices or share prices (see

e.g. [1, 2], [9]–[13]). A number of crash

moments has been predicted in the literature so far, some of

them being in a very good agreement with the actual moment the crash

took place [11]–[13].

However one has to remember that any financial system should be

considered as an open system, while the scaleless behavior and the

quantitative description following from this assumption are

completely true only in a case of the closed statistical systems.

Therefore one should be aware that the methods based on the closed

system assumption are very sensitive to the number of data points

(information) one takes into account to make the fit of log-periodic

oscillation parameters. As a result the predictive power of such

models can be in general very limited [14].

Few years ago another approach based on the local properties of the time series was proposed [15]. The method uses the local Hurst exponent [16, 17] or the local fractal dimension of the time series built on the index values or share prices. These quantities are linked together by the well known relation

| (1) |

in an analogy with the similar equation satisfied for the global

and

values usually used to describe the monofractal signals.

In Ref. [15] it was shown that the local Hurst exponent calculated

for the main Dow Jones (DJIA) index forms the characteristic pattern

before any of the crashes on American stock market.

The values drop significantly down before any rupture

point. The moving average of the local

Hurst exponent calculated on the one week period (5 sessions) drops

down to or even less for sessions immediately preceding the

rupture point, thus revealing the presence of the growing

antipersistence in the financial time series signal before

the crash occurs. The similar qualitative behavior of the local

values for other financial time series (shares) has also been

confirmed [18].

The advantage in the use of over other methods is that it

actually measures ’the local state’ of the market and therefore it

seems to be more resistable to the long-term

inaccuracies or distortions coming e.g. from the rapid change

of the boundary conditions around the financial system.

Therefore the method might be also applied to an open complex system

and the financial

market is a good candidate of such system.

In this report we intend to apply the technique used in Ref. [15] to

investigate the market index of the largest emerging market in

Europe - the Warsaw Stock Exchange Index (WIG)

incorporating more than companies. It has already -years

old history up to now with more than closure day values at

the moment.

The WIG time series has been analyzed by us with the

Detrended Fluctuation Analysis (DFA) technique [16] to extract the

scaling Hurst exponent . This technique is well described in the

literature [16, 17, 19] so we will not quote it here. Let us remind however

its local version applied in our calculations.

We first form for a given trading day a time subseries of

length with points in the period . We call this subseries

the observation box or the observation time-window. Then the

standard DFA procedure is applied to this time-window, i.e. we

cover the subseries with smaller non-overlapping boxes of size

starting from the given trading point and going backwards in

time up to . In order to cover the whole time-window with -size boxes

we put the last box in the period ,

where means the integer part. This box partly overlaps the

preceding one but this does not modify the obtained results. In

each box the detrended signal is found according to DFA method for

the simplest linear trend assumed in every box of size . The

detrended signal fluctuates and its variance is related to the box

width by the power law relation known for DFA:

| (2) |

Thus moving the observation box of length session after session

we are able to reproduce the whole history of changes

in

time.

It is well known that the exponent measures the level of

persistence or anti persistence in the signal.

For one obtains the Brownian (integer) signal with null

autocorrelations. Hence, only the case is meaningful for

practical applications. The observation of the

evolution may suggest in what state the financial market is at the

given moment. Indeed, big investors usually called speculators cash

their profits more frequently if they ’feel’ the rupture point in

the increasing trend is coming. The more nervous behavior of

speculators gives a signal to all other players on the market

(spectators) who also start to cash their investments at lower

prices. It actually leads after some time to the change of trend and

if the market is particularly nervous - to the crash appearance.

Thus we put a hypothesis that the nervous situation on the market

can (should) be observed as the appearance of the anti correlations

in price returns of various assets and finally we may expect the

growing local fractal dimension of the financial time series (or

decreasing

) before a crash.

To check if this hypothesis works well for the polish financial

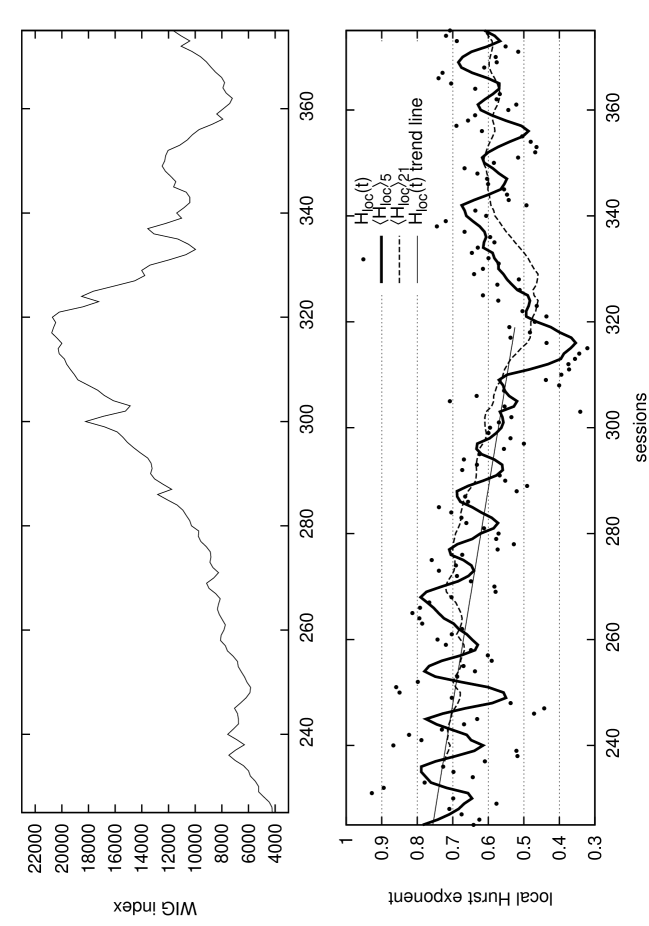

market we studied three main crashes (or rupture points) that have

already taken place during the whole WIG history 1992-2007. First we

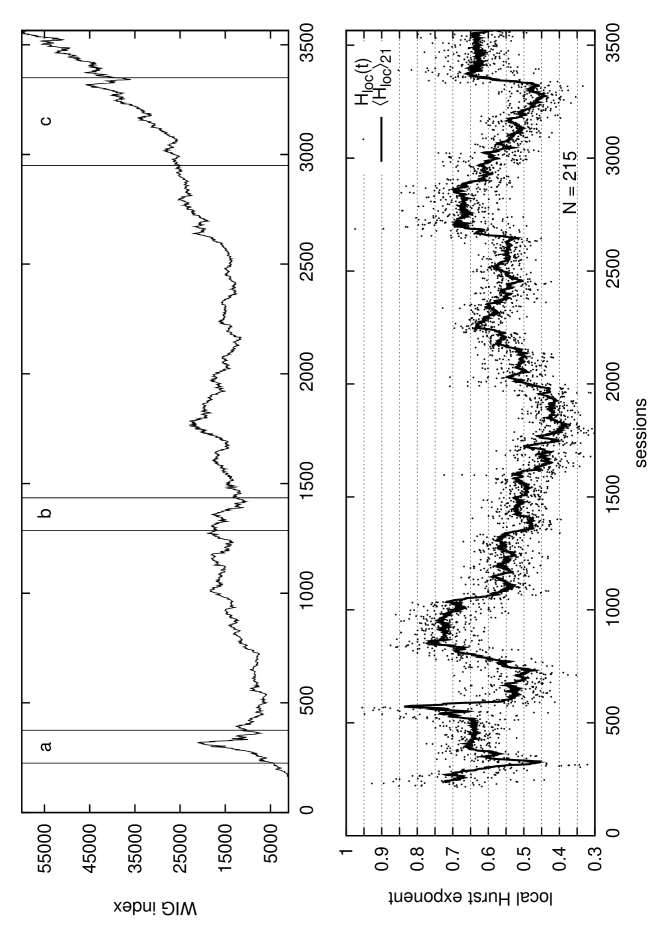

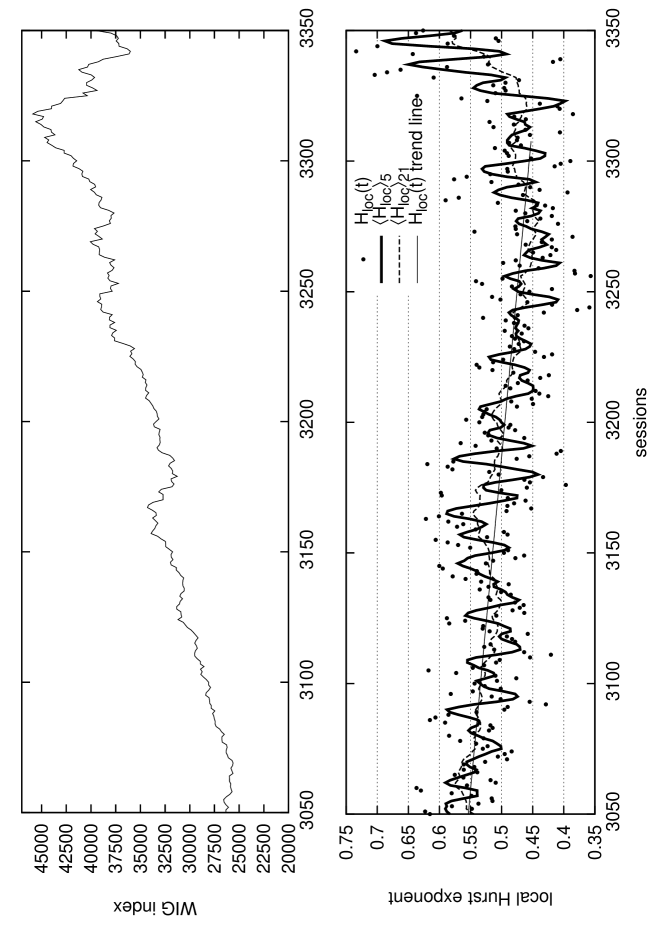

calculated the for any point of the closure day WIG time

series. The are usually widely spread out due to the

statistical noise. Therefore the moving average of last five sessions (one trading week) or the

moving average of last 21 sessions

(one trading month) have been calculated for the local Hurst

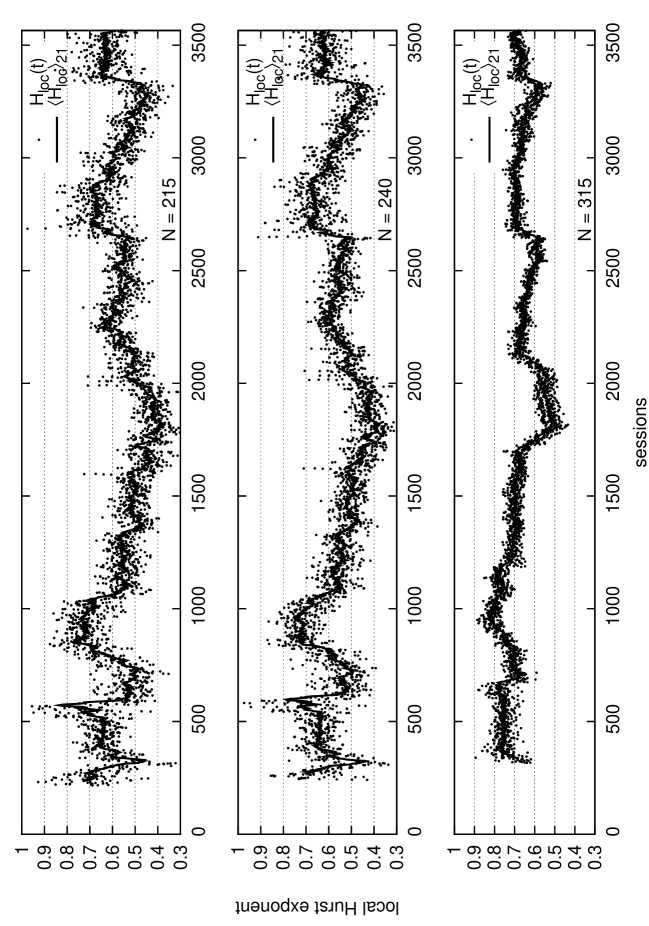

exponent for the whole WIG history. The results of are shown in Fig. 1 and Fig. 2. All plots were

done for the observation boxes of length from till

sessions. It corresponds to the depth of looking back in time from

10 months till 15 months.

Let us notice that the main trend pattern of is

independent on the observation box length but the depth of

fluctuations does depend on (see Fig. 2). It is

because of the different noise cut level changing with the

time-window length. To examine the structure of a local behavior

more rigorously we have chosen the 10 months observation box to

perform further analysis (the similar size was used in Ref. [15]). The

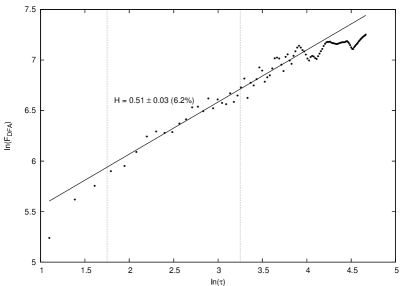

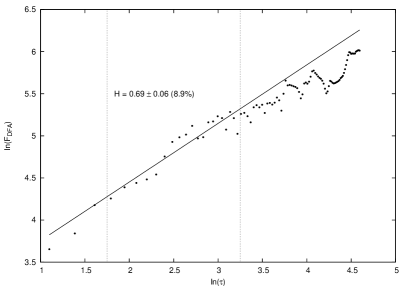

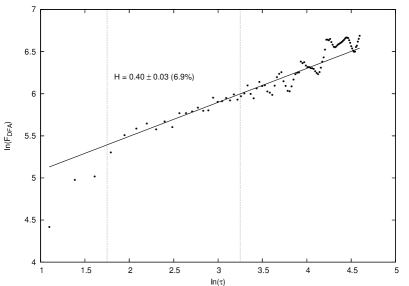

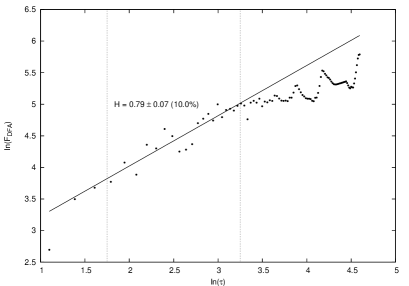

examples of plots vs in log-log scale, from which

the values have been extracted

according to Eq. (2), are shown in Fig. 3.

| Date | Initial 3 sessions drop | Total relative drop(duration time) |

|---|---|---|

| 17.03.94 | 11 % | 65 % (41 sessions) |

| 22.07.98 | 4 % | 39 % (30 sessions) |

| 12.05.06 | 5 % | 21% (24 sessions) |

Then the most spectacular crashes on the Polish stock exchange market were examined within this technique in some surrounding of the crash (rupture) points. The investigated cases are found between the vertical lines in Fig. 1. and correspond to crashes described in Table 1. The zoomed evolution of the for these crashes is shown in Fig. 4a-c. The decreasing trend in is the most evident from these plots and lasts for many sessions before the rupture point occurs. Looking at the common characteristic pattern of plots before the crash moment, we may formulate the following necessary conditions to be simultaneously satisfied (signal to sell) if the rupture point is expected soon:

-

1.

is in decreasing trend and except for small fluctuations

-

2.

-

3.

-

4.

minima of for not necessary consecutive sessions satisfy

Contrary, if all the above conditions are not satisfied we expect

the strong signal to buy on the market.

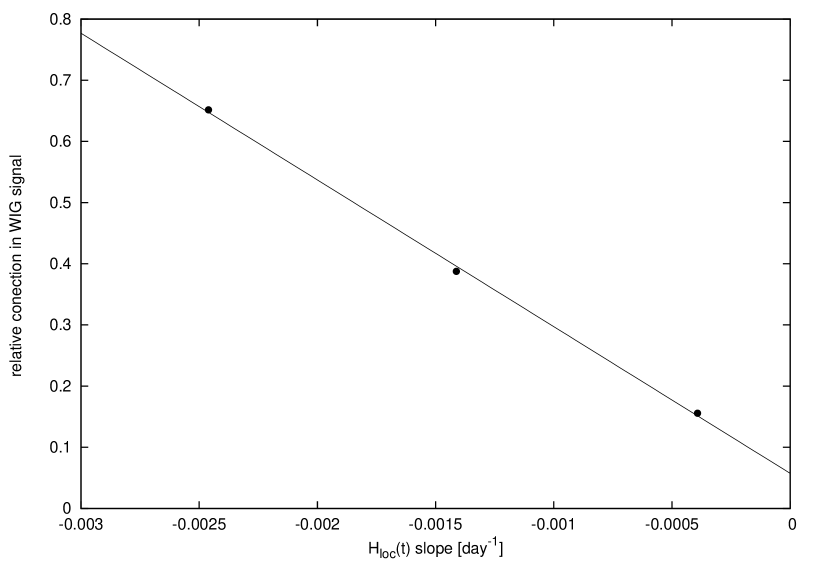

Moreover we are able to find a relation between the rate of the

drop and the total correction the WIG

index gains after the crash. Generally, the deeper the bottom of signal

the bigger crash or major correction can be expected. The latter correction can be calculated

as the difference in the index signal magnitude between the rupture point

and the minimum in the signal value after the crash from which the

next long-lasting trend is being formed. We observe this correction

is proportional to the absolute slope of the trend assumed

as a straight line. Such straight line-fits to the local Hurst

exponents have been drawn in Fig. 4a-c for periods immediately

preceding the crashes on the Polish stock exchange market. We have

also drawn in Fig. 5 a relation between the magnitude of the relative

WIG index correction and the slope of the linear trend

fit before the crash. Amazingly, this relation is linear! The fit done with just three points

may not of course entitle to draw a strong conclusion,

nevertheless the relation is striking and worth further

investigation.

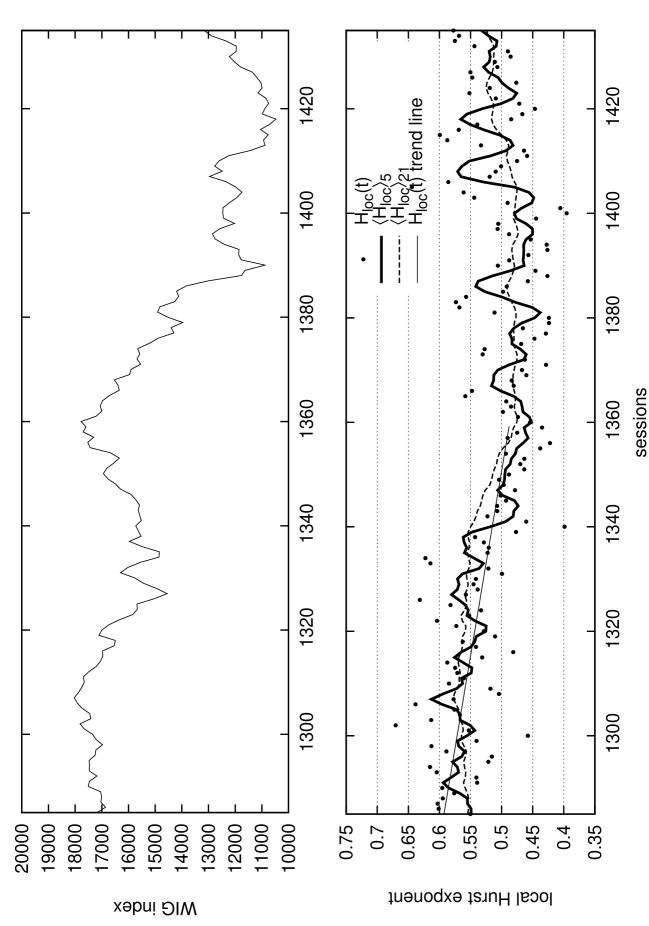

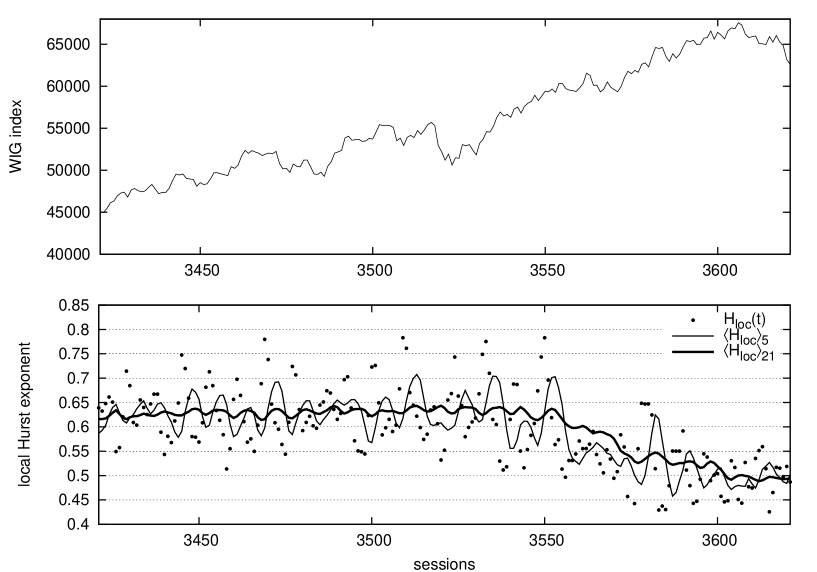

Finally we checked also the current situation on the market. The

plot of the recent WIG signal with the corresponding local fractal

properties is illustrated in Fig. 6. The started to fall

down almost three trading months ago (from the session ), despite the WIG signal has still been increasing. The

average reached its critical value

in the end of June (June 28 ’07 – session ), however the

crash pattern (conditions (1)-(4)) is not so clear as in previous cases (a)–(c).

We still have remaining only slightly below the critical value . Also minima

are higher then previously. As a result a crash has not been

formed so far but the correction in WIG signal

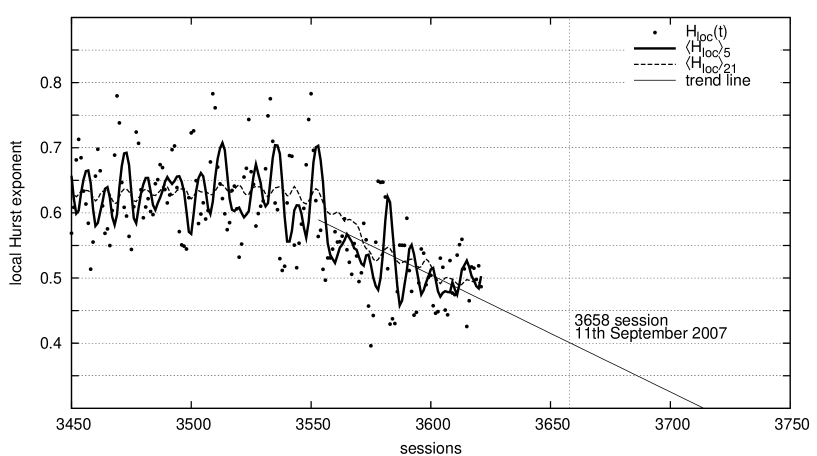

actually took place. The future situation on the market will, in our

opinion, be driven by the forthcoming behavior of as

indicated in Fig.7. One may think about two possible scenarios. In

the first one the local Hurst exponent will remain in the decreasing

trend. If the dropping rate of remains the same as it

is now we may expect around the

beginning of September ’07 (see Fig.7). This means that a major

crash should take place no later than mid-September. If however, we

would observe that began to increase and the other

conditions (1)–(4) were not fulfilled, the

crash should not take place and the current drop of WIG index will

be just a minor correction in the long-lasting increasing trend of

WIG signal. We believe the further evolution will choose very soon

one of these scenarios.

References

- [1] D. Sornette, A. Johansen, J.-P. Bouchaud, J. Phys. I France 6 (1996)

- [2] J. A. Feigenbaum, P.G.O. Freund, Int. J. Mod. Phys. B 10, 3737 (1996)

- [3] B.B. Mandelbrot, J. Business 36, 349 (1963)

- [4] R. N. Mamtegna, H.E. Stamley, Nature 376, 46 (1995)

- [5] J.-P. Bouchaud, D. Sornette, J. Phys. I France 4, 863 (1994)

- [6] Y. Liu, P. Cizeau, M. Meyer, C.-K. Peng, H.E. Stanley, Physica A 245, 437 (1997)

- [7] H. Takayasu, H. Miura, T. Hirabayashi, K. Hamada, Physica A 184, 127 (1992)

- [8] P. Bak, M. Paczuski, M. Shubik, Physica A 246, 430 (1997)

- [9] D. Sornette, A. Johansen, Physica A 245, 411 (1997)

- [10] N. Vandewalle, Ph. Boveroux, A. Minguet, M. Ausloos, Physica A 255, 201 (1998)

- [11] N. Vandewalle, M. Ausloos, Ph. Boveraux, A. Minguet, Eur. Phys. J. B 4, 139 (1998)

- [12] N. Vandewalle, M. Ausloos, Ph. Boveraux, A. Minguet, Eur. Phys. J. 9, 355 (1999)

- [13] S. Drozdz, F. Grummer, F. Ruf, J. Speth, Physica A 324, 174 (2003)

- [14] Ł. Czarnecki, D. Grech, in preparation

- [15] D. Grech, Z. Mazur, Physica A 336, 133 (2004)

- [16] C.-K. Peng, S.V. Buldyrev, S. Havlin, M. Simons, H.E. Stanley, A.L. Golberger, Phys. Rev. E 49, 1691 (1994)

- [17] N. Vandewalle, M. Ausloos, Physica A 246, 454 (1997)

- [18] P. Oświȩcimka, J. Kwapień, S. Drozdz, R. Rak, Acta Phys. Pol. B36, 2447 (2005)

- [19] M. Ausloos, N. Vandewalle, Ph. Boveroux, A. Minguet, K. Ivanova, Physica A 274, 229 (1999)