The fractional volatility model: An agent-based interpretation

Abstract

Based on criteria of mathematical simplicity and consistency with empirical market data, a model with volatility driven by fractional noise has been constructed which provides a fairly accurate mathematical parametrization of the data. Here, some features of the model are discussed and, using agent-based models, one tries to find which agent strategies and (or) properties of the financial institutions might be responsible for the features of the fractional volatility model.

Keywords: Fractional volatility, Statistics of returns, Option pricing, Agent-based models

1 Introduction

Classical Mathematical Finance has, for a long time, been based on the assumption that the price process of market securities may be approximated by geometric Brownian motion

| (1) |

In liquid markets the autocorrelation of price changes decays to negligible values in a few minutes, consistent with the absence of long term statistical arbitrage. Geometric Brownian motion models this lack of memory, although it does not reproduce the empirical leptokurtosis. On the other hand, nonlinear functions of the returns exhibit significant positive autocorrelation. For example, there is volatility clustering, with large returns expected to be followed by large returns and small returns by small returns (of either sign). This, together with the fact that autocorrelations of volatility measures decline very slowly[1] [2] [3], has the clear implication that long memory effects should somehow be represented in the process and this is not included in the geometric Brownian motion hypothesis.

One other hand, as pointed out by Engle[4], when the future is uncertain, investors are less likely to invest. Therefore uncertainty (volatility) would have to be changing over time. The conclusion is that a dynamical model for volatility is needed and in Eq.(1), rather than being a constant, becomes a process by itself. This idea led to many deterministic and stochastic models for the volatility ([5] [6] and references therein).

In a previous paper[7], using both a criteria of mathematical simplicity and consistency with market data, a stochastic volatility model was constructed, with volatility driven by fractional noise. It appears to be the minimal model consistent both with mathematical simplicity and the market data. This data-inspired model is different from the many stochastic volatility models that have been proposed in the literature. The model was used to compute the price return statistics and asymptotic behavior, which were compared with actual data. Deviations from the classical Black-Scholes result and a new option pricing formula were also obtained. The fractional volatility model, its predictions and comparison with data will be reviewed in Section 2.

When this fractional volatility model was first presented, an interesting remark by an economist was ”all right, the model seems to fit reasonably well the data, but where is the economics ? ”. The same remark might be made about the simple geometric Brownian model, which does not even fit the data and is used by most of the of mathematical finance practitioners.. But, of course, our economist was right. The fractional volatility model seems to be a reasonable mathematical parametrization of the market behavior, but it is not sufficient to fit the data. One should also search for the mechanisms in the market that lead to the observed phenomena. No agent-based model can pretend to be the market itself, not even a realistic image of it. Nevertheless it may provide a surrogate model of the basic mechanics at work there. Therefore, the idea in this paper is to use stylized agent-based market models and find out which features of these models correspond to each one of the features of the mathematical parametrization of the data.

2 The fractional volatility model. Induced volatility, statistics of returns, option pricing and leverage

The basic hypothesis for the model construction were:

(H1) The log-price process belongs to a probability product space of which the first one, , is the Wiener space and the second, , is a probability space to be reconstructed from the data. Denote by and the elements (sample paths) in and and by and the algebras in and generated by the processes up to . Then, a particular realization of the log-price process is denoted

This first hypothesis is really not limitative. Even if none of the non-trivial stochastic features of the log-price were to be captured by Brownian motion, that would simply mean that is a trivial function in .

(H2) The second hypothesis is stronger, although natural. One assumes that, for each fixed , is a square integrable random variable in .

A mathematical consequence of hypothesis (H2) is that, for each fixed ,

| (2) |

where and are well-defined processes in . (Theorem 1.1.3 in Ref.[8])

Recall that if is a process such that

| (3) |

with and being adapted processes, then

| (4) |

The process associated to the probability space could then be inferred from the data. According to (4), for each fixed realization in one has

| (5) |

Each set of market data corresponds to a particular realization . Therefore, assuming the realization to be typical, the process may be reconstructed from the data by the use of (5). This data-reconstructed process was called the induced volatility.

For practical purposes we cannot strictly use Eq.(5) to reconstruct the induced volatility process, because when the time interval is very small the empirical evaluation of the variance becomes unreliable. Instead, was estimated from

| (6) |

with a time window sufficiently small to give a reasonably local characterization of the volatility, but also sufficiently large to allow for a reliable estimate of the local variance of .

Once several data sets were analyzed[7], the next step towards obtaining a mathematical characterization of the induced volatility process was to look for scaling properties. It turned out that neither

| (7) |

nor

| (8) |

were good hypothesis for the induced volatility process. It means that the induced volatility process itself is not self-similar.

If instead, one computes the empirical integrated log-volatility, one finds that it is well represented by a relation of the form

| (9) |

the process possessing very accurate self-similar properties.

A nondegenerate process , if it has finite variance, stationary increments and is self-similar

| (10) |

must necessarily [9] have a covariance

| (11) |

with . The simplest process with these properties is a Gaussian process called fractional Brownian motion[10], with

| (12) |

and, for , a long range dependence

| (13) |

Therefore, mathematical simplicity suggested the identification of the process with fractional Brownian motion.

| (14) |

and, from the data, one obtains Hurst coefficients in the range .

Finally one obtains the following fractional volatility model

| (15) |

is a volatility intensity parameter and is the observation time scale. Notice that the volatility is not driven by fractional Brownian motion but by fractional noise, naturally introducing an observation scale dependence.

2.1 The statistics of price returns

At each fixed time is a Gaussian random variable with mean and variance . Then,

| (16) |

therefore

| (17) |

with

| (18) |

Thus, the effective probability distribution of the returns might depend both on the time lag and on the observation time scale used to construct the volatility process. That this latter dependence might actually be very weak, seems to be implied by comparison with the data from several markets.

A closed-form expression for the returns distribution and its asymptotic behavior may be obtained, namely

| (19) |

with asymptotic behavior, for large returns

| (20) |

with

and

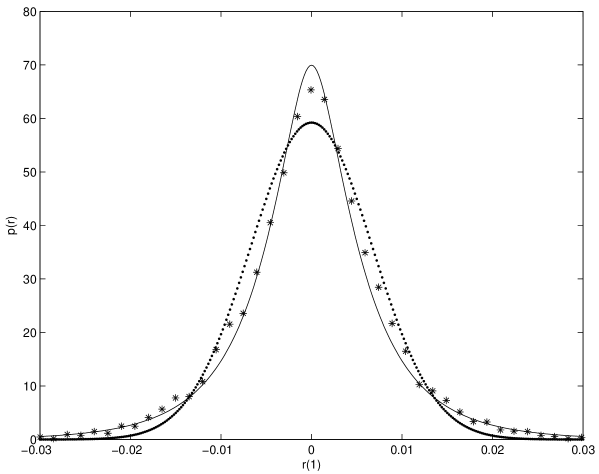

Some illustrative comparisons with market data were performed. In Fig.1 NYSE one-day data was used to fix the parameters of the volatility process. Then, using , the one-day return distribution predicted by the model is compared with the data. The agreement is quite reasonable. For comparison a log-normal with the same mean and variance is also plotted in Fig.1. Then, in Fig. 2, using the same parameters, the same comparison is made for the and data.

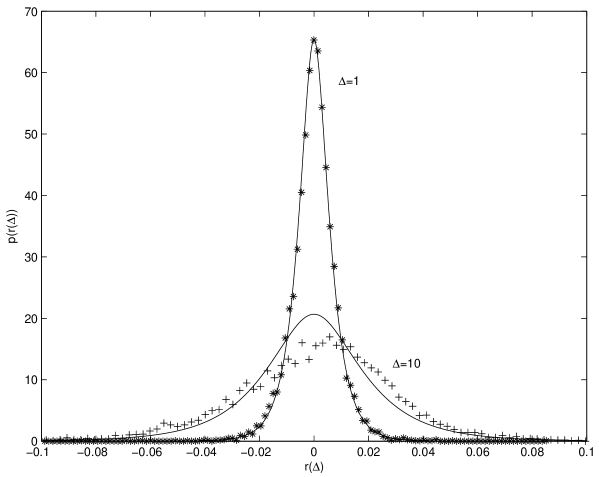

Fig. 3 shows a somewhat surprising result. Using the same parameters and just changing from (one day) to (one minute), the prediction of the model is compared with one-minute data of USDollar-Euro market for a couple of months in 2001. The result is surprising, because one would not expect the volatility parametrization to carry over to such a different time scale and also because one is dealing with different markets.

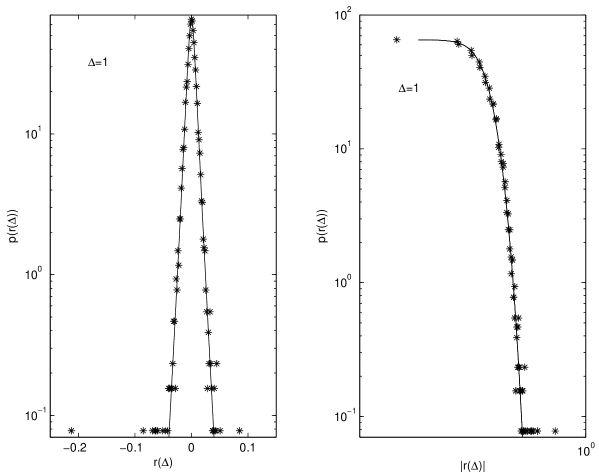

In Fig.4 and Fig.5 one sees the same one-day and one-minute return data discussed before, as well as the predictions of the model, both in semilogarithmic and loglog plots.

As seen from Figs. 4 and 5, the exact result (19) or (20) resembles the double exponential distribution recognized by Silva, Prange and Yakovenko[11] as a new stylized fact in market data. The double exponential distribution has been shown, by Dragulescu and Yakovenko[12], to follow from Heston’s [13] stochastic volatility model. Notice however that our model is different from Heston’s model in that volatility is driven by a process with memory (fractional noise). As a result, despite the qualitative similarity of behavior at intermediate return ranges, the analytic form of the distribution and the asymptotic behavior are different.

2.2 Option pricing

New option pricing pricing formulas may be obtained from the model both in a simplified risk-neutral form or, more accurately, using fractional Malliavin calculus. Assuming risk neutrality [14], the value of an option is the present value of the expected terminal value discounted at the risk-free rate

| (21) |

and the conditional probability for the terminal price depends on and . is the strike price, the maturity time and and the price and volatility of the underlying security.

In stochastic volatility models (with or without fractional noise) risk-neutrality is not an accurate assumption. Nevertheless it provides an approximate estimate of the deviations from Black-Scholes implied by the fractional volatility model. As in Hull and White [15], one uses the relation between conditional probabilities of related variables, namely

| (22) |

being the random variable

| (23) |

that is, is the mean volatility from time to the maturity time conditioned to an average value at time . Finally the result for is[7]

| (24) |

is the complementary error function and and are

| (26) |

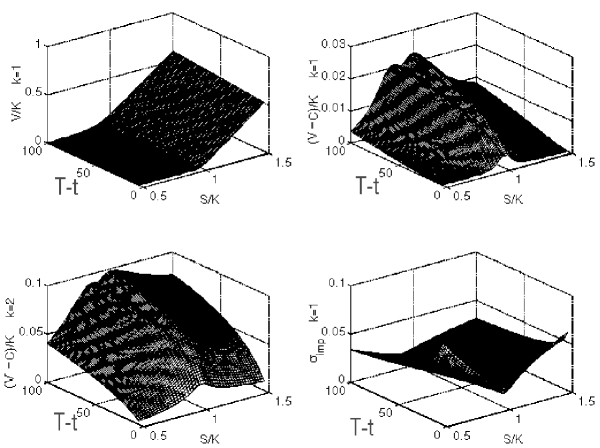

In Fig.6 one plots the option value surface for in the range and as well as the difference for and . The other parameters are fixed at . To compare the predictions of the option pricing formula (24) with the classical Black-Scholes (BS) result[16] [17], the implied volatility required in BS to reproduce the same results was computed. This is plotted in the lower right panel of Fig.6 which shows the implied volatility surface corresponding to for . One sees that, when compared to BS, it predicts a smile effect with the smile increasing as maturity approaches.

2.3 Leverage

The following nonlinear correlation of the returns

| (27) |

is called leverage and the leverage effect is the fact that, for , starts from a negative value and decays to zero whereas for it has almost negligible values. Fig.7 shows computed for the NYSE index one-day data in the period 1966-2000.

The leverage behavior of the fractional volatility model will now be examined. For this purpose it will be convenient to use the following integral representation of fractional Brownian motion [9].

| (28) |

Using this representation the fractional volatility model may be rewritten as

| (29) |

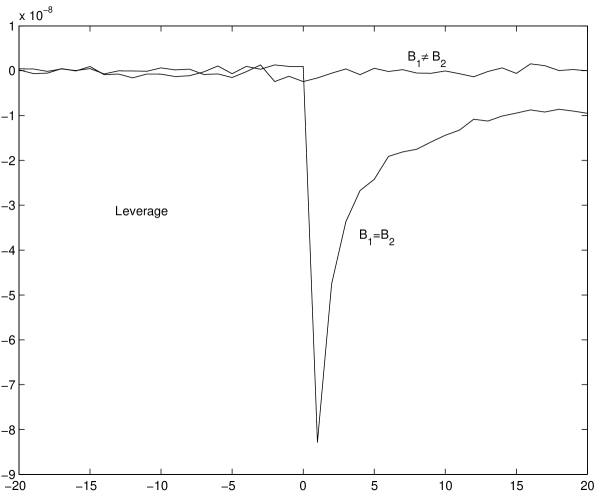

where and different Brownian processes. In Fig.8 one shows the leverage computed for the model (29) with and chosen to match the statistical parameters of the NYSE index. Both the and the cases are considered. One sees that for there is no leverage effect, whereas for an effect is found. Therefore one sees that, identifying the random generator of the log-price process with the stochastic integrator of the volatility, at least a part of the leverage effect is taken into account.

3 Two agent-based studies

Many factors play a role in a real market. To take into account all the factors in a model is neither possible nor, in many cases, illuminating. The objective is to isolate some of the more relevant mechanisms that presumably play a role in the market and, by stripping the model from other (inessential?) complications, to exhibit and understand the purified effect of these factors. As in other branches of science, the splitting apart of the dynamical components of a phenomena, may improve its understanding [18].

Two stylized models will be considered. In the first the traders strategies play a determinant role. In the second the determinant effect is the limit-order book dynamics, the agents having a random nature.

3.1 Agent strategies and market impact

A market model with either random self-adapted strategies or fixed strategies was studied in detail in [19]. There it was found that the dominance of two types of strategies was to a large extent determined by the initial conditions. Different types of return statistics corresponded to the relative importance of either value investors or technical traders. The occurrence of market bubbles also corresponded to situations where technical trader strategies were well represented.

Here, that model will be used for comparison purposes with the fractional volatility parametrization. The basic ingredients of the model are summarized below:

One considers a set of investors playing against the market, that is, they have some effect on an existing market that is influenced by other factors (other investors and general economic effects). This assumption implies that in addition to the impact of this group of investors on the market, the other factors are represented by a stochastic process. Therefore

| (30) |

represents the change in the log price with being the total investment made by the group of traders and the stochastic process that represents all the other factors. No conservation law is assumed for the total amount of stock and cash detained by the group of traders. If is the price of the traded asset at time , the purpose of the investors is to have an increase, as large as possible, of the total wealth at the expense of the rest of the market.

The collective variable is and each investor payoff at time is

| (31) |

Market impact

Let be the price of a representative asset, and the total sum of the buying and selling orders (in money units) for the asset. Buying orders are positive and selling ones negative. The effect of these orders on the price change of the asset is called the market impact function. Let small orders have an impact according to the loglinear law[20] [21]

| (32) |

The constant , is sometimes called the liquidity. Eq.(32) corresponds naturally to a first order expansion and satisfies the condition

| (33) |

which is expected to be valid for small orders. However, as pointed out by Zhang[22] there is experimental evidence that this is not an accurate representation for large orders. Therefore a slightly different market impact function will be used. The reasoning used to motivate it, has some relation to Zhang’s although the result is somewhat different.

When using Eq.(32) in a discrete-time dynamical model we are somehow neglecting the fact that the market takes different times to fulfill (and to react to) small and large orders. Therefore this should be taken into account when reducing the dynamics to a sequence of equal time steps. In particular, the reaction of the market may be parametrized by a change in the coefficient which, being also related to some stochastic process, may vary by a factor proportional to . Taking the time to fill an order to be proportional to its size, one obtains

| (34) |

This price impact function was first proposed in [19] with . For small orders it recovers the loglinear approximation and for very large orders (and ) Zhang’s square root law.

The agent strategies

In first-order, two main types of informations are taken into account by the investors, namely the difference (misprice) between price and perceived value

| (35) |

and the variation in time of the price (the price trend)

| (36) |

Consider now a non-decreasing function such that and . Two useful examples are

| (37) |

The information about misprice and price trend is coded on a four-component vector

| (38) |

The strategy of each investor is also a four-component vector with entries or . means to sell, means to buy and means to do nothing. Hence, at each time, the investment of agent is . A fundamental (value-investing strategy) that buys when the price is smaller than the value and sells otherwise would be and a pure trend-following strategy would be . In this setting the total number of possible strategies is . The strategies will be labelled by numbers

| (39) |

Therefore the fundamental strategy is strategy no. and the pure trend-following one is no. .

An evolution dynamics may be implemented in the model in the following way. After a number of time steps, agents copy the strategy of the best performers and, at the same time, have some probability to mutate that strategy. This evolution aims at attaining the goal of improving gains, while at the same time allowing for some renewal of the strategies. The percentage of each strategy changes in time and one may find whether some of them become dominating or stable and when this may occur.

The model was run with different initial conditions and with or without evolution of the strategies. The following results were obtained in [19]:

- When in the initial condition all traders have the fundamental strategy and evolution is activated, this strategy stays dominant, not being invaded by any other of the strategies that are created by the mutation process. There are however a few other strategies that, after being created, survive the selection process. This is true for example for the strategies , , and . These surviving strategies are however similar to the fundamental one. When there is dominance of the fundamental strategies, the price increments have a Gaussian distribution.

- The fundamental strategy ceases to be stable if it occurs in the initial condition in smaller amounts .

- For a completely random mixture of strategies in the initial condition, although the selection mechanism still favors at each evaluation cycle the best performers, the system never organizes itself to make the total payoff of this group of traders to grow, nor does a clear dominant strategy emerges.

- When the simulation is run without evolution, with a fixed of fundamental strategies (no. 72) and of trend-following ones (no. 60), one sees a large number of bubbles and crashes in the price evolution and the price increments distribution has fat tails.

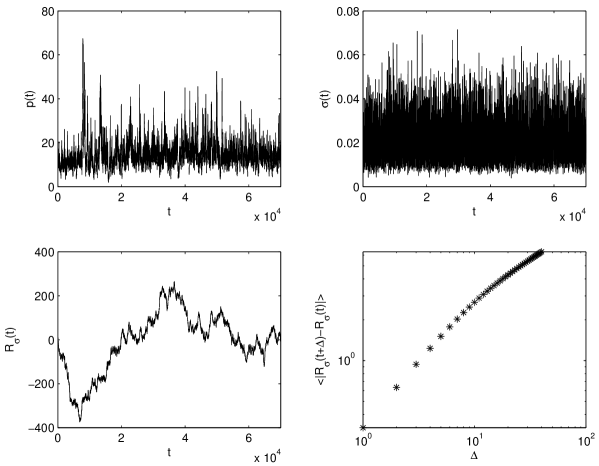

Because this last case is the one where the returns statistics is closer to the actual market data, it is here further analyzed to see whether it also displays the other features of the fractional volatility model. From typical simulation runs one computes

and

Fig.9 shows a typical plot of the price process , the volatility, and obtained from the model with equal amounts of fundamental and trend-following agents and no evolution. One notices the lack of scaling behavior of with an asymptotic exponent , denoting the lack of memory of the volatility process. This might already be evident from the time behavior of in the lower left plot. Also, although the returns have fat tails in this case, they are of different shape from those observed in the market data. Similar conclusions are obtained with other combinations of agent strategies. In conclusion: It seems that the features of the fractional volatility model are not easily captured by a choice of strategies in an agent-based model. Notice however that what the fractional volatility model parametrizes is the bulk of the market data, that is, the behavior of the market in normal days. The agents reactions and strategies are very probably determinant during market crisis and market bubbles.

3.2 A limit-order book dynamics model

Here one considers a limit-order book where asks and bids arrive at random on a window around the current price . Every time a buy order arrives it is fulfilled by the closest non-empty ask slot, the new current price being determined by the value of the ask that fulfills it. If no ask exists when a buy order arrives it goes to a cumulative register to wait to be fulfilled. The symmetric process occurs when a sell order arrives, the new price being the bid that buys it. Because the window around the current price moves up and down, asks and bids that are too far away from the current price are automatically eliminated. Sell and buy orders, asks and bids all arrive at random. The only parameters of the model are the width of the limit-order book and the size of the asks and bids, the sell and buy orders being normalized to one.

The model was run for different widths and liquidities and, for comparison with the fractional volatility model, one computes as before and .

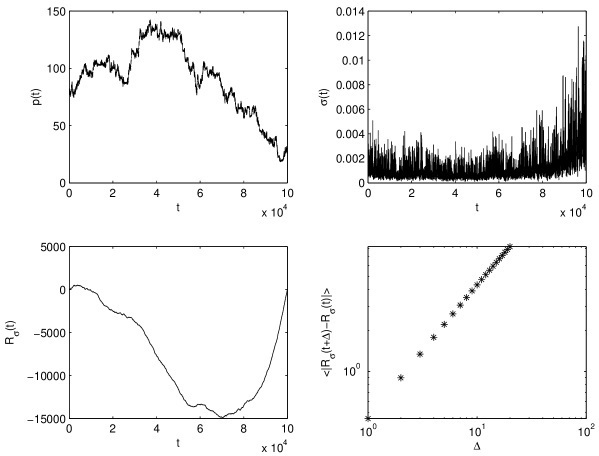

Although the exact values of the statistical parameters depend on and , the statistical nature of the results seems to be essentially the same. Fig.10 shows typical plots of the price process , the volatility, and obtained for and the limit-order book divided into discrete price slots with . The scaling properties of are quite evident from the lower right plot in the figure, the Hurst coefficient being . Fig.11 shows the correlation and the pdf of the one-time returns. From these results one concludes that the main statistical properties of the market data (fast decay of the linear correlation of the returns, non-Gaussianity and volatility memory) are already generated by the dynamics of the limit-order book with random behavior of the agents. This implies, as pointed out by some authors that in the past have considered limit order book models [23] [24] [25] [26], that a large part of the market statistical properties (in normal business-as-usual days) depends more on the nature of the price fixing financial institutions than on particular investor strategies.

4 Conclusions

(a) The fractional volatility model provides a reasonable mathematical parametrization of the bulk market data, that is, it captures the behavior of the market in business-as-usual trading days.

(b) A small modification of the original model, identifying the random generator of the log-price process and the integrator of the volatility process, also describes, at least, a part of the leverage effect.

(c) The market statistical behavior in normal days seems to be more influenced by the nature of the financial institutions (the double auction process) than by the traders strategies. Specific trader strategies and psychology should however play a role on market crisis and bubbles.

References

- [1] Z. Ding, C. W. J. Granger and R. Engle; A long memory property of stock returns and a new model, Journal of Empirical Finance 1 (1993) 83-106.

- [2] A. C. Harvey; Long memory in stochastic volatility, Research report 10, London School of Economics, 1993.

- [3] F. J. Breidt, N. Crato and P. Lima; The detection and estimation of long memory in stochastic volatility models, J. of Econometrics 83 (1998) 325-348.

- [4] R. F. Engle; Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation, Econometrica 50 (1982) 987-1007.

- [5] S. J. Taylor; Modeling stochastic volatility: A review and comparative study, Mathematical Finance 4 (1994) 183-204.

- [6] R. S. Engle and A. J. Patton; What good is a volatility model ?, Quantitative Finance 1 (2001) 237-245.

- [7] R. Vilela Mendes and M. J. Oliveira; A data-reconstructed fractional volatility model, arXiv:math/0602013

- [8] D. Nualart; The Malliavin Calculus and Related Topics, Springer-Verlag, Berlin 1995.

- [9] P. Embrechts and M. Maejima; Selfsimilar processes, Princeton Univ. Press, Princeton NJ 2002.

- [10] B. B. Mandelbrot and J. W. Van Ness; Fractional Brownian motions, fractional noises and applications, SIAM Rev. 10 (1968) 422-437.

- [11] A. C. Silva, R. E. Prange and V. M. Yakovenko; Exponential distribution of financial returns at mesoscopic time lags: A new stylized fact, Physica A344 (2004) 227-235.

- [12] A. A. Dragulescu and V. M. Yakovenko; Probability distribution of returns in the Heston model with stochastic volatility, Quantitative Finance 2 (2002) 443-453.

- [13] S. L. Heston; A closed form solution for options with stochastic volatility with applications to bond and currency options, The Review of Financial Studies 6 (1993) 327-343.

- [14] J. C. Cox and S. A. Ross; The valuation of options for alternative stochastic processes, J. of Financial Economics 3(1976) 145-166.

- [15] J. C. Hull and A. White; The pricing of options on assets with stochastic volatility, J. of Finance 42 (1987) 281-300.

- [16] F. Black and M. Scholes; The pricing of options and corporate liabilities, J. of Political Economy 81 (1973) 637-654.

- [17] R. C. Merton; Theory of rational option pricing, Bell J. Econ. Manag. Sci. 4 (1973) 141-183.

- [18] B. M. Roehner; The taking apart of economic phenomena, an essential step, Econophysics Forum, April - May 1999.

- [19] R. Vilela Mendes; Structure generating mechanisms in agent-based models, Physica A295 (2001) 537-561.

- [20] J. D. Farmer; Market force, Ecology and Evolution; Santa Fe Institute Working Paper 98-12-116.

- [21] J.-P. Bouchaud and R. Cont; A Langevin approach to stock market fluctuations and crashes, European Phys. Journal B6 (1998) 543.

- [22] Yi-Cheng Zhang; Toward a theory of marginally efficient markets, Physica A 269 (1999) 30.

- [23] S. Maslov; Simple model of a limit order-driven market arXiv:cond-mat/9910502

- [24] D. Challet and R. Stinchcombe; Analyzing and modelling 1+1d markets arXiv:cond-mat/0106114

- [25] D. Challet and R. Stinchcombe; Limit order market analysis and modelling: on an universal cause for over-diffusive prices arXiv:cond-mat/0211082

- [26] E. Smith, J. Doyne Farmer, L. Gillemot and S. Krishnamurthy; Statistical theory of the continuous double auction, arXiv:cond-mat/0210475