Cycles in Nonlinear Macroeconomics

’All linear systems are equally happy, whereas each nonlinear system is unhappy in its own way.’

Yu. Bolotin, A. Tur, and V. Yanovskii

”Constructive Chaos”

Preface

Nonlinear dynamics is one of the most important and prospective trends of the development of economic science. Powerful modern techniques of qualitative theory of differential equations and related subjects of mathematical topology provide broad possibilities of obtaining substantial results of qualitative character, in the first place, in solving the problems of economic forecasting. Mathematical economics is characterized by two principally different ways of modeling, i.e., static and dynamic ones. Following N. D. Kondratev [25], we shall dwell on a more detailed and concrete characterization of these two purely theoretical approaches to the study of economic reality.

The static theory considers economic processes in terms of their instant manifestation, without any regard to inertial changes in time. The static approach to the modeling of economic reality is based on the concept of the equilibrium of interrelated elements of an economic system. The concept of equilibrium itself had been sufficiently well familiar to scientists concerned with mechanics before the appearance in 1776 of Adam Smith’s prominent work ”An Inquiry into the Nature and Causes of the Wealth of Nations” wherein, as it seems, the author managed to find an analogy between the economic balance and the resultant force in mechanics. A. Smith put forward the most substantial postulate of the general theory of equilibrium: namely, an ability of the system of competition to achieve such a distribution of resources that, in a sense, proves to be efficient.

On positions analogous to those of A. Smith stand also the constructions of D. Ricardo who put forward the thesis of the freedom of competition and the freedom of movement of labor and capital from one sphere of economic relations to another. D. Ricardo was aware of the fact that the actual price, the actual level of wages and incomes are variables with respect to time, and, at that, he suggested that there exist a tendency towards attaining a certain natural level of equilibrium for the above mentioned characteristics.

An exhaustive formulation of the general concept of equilibrium rightfully belongs to L. Walras, a representative of the school of marginalism (or marginal utility). Works by L. Walras, S. Jevons, and V. Pareto unified the theory of equilibrium with regard to an application to the spheres of exchange, production, capital and money. They were subsequently elaborated by J. Hicks and P. Samuelson. On the whole, these works are of rather broad, comprehensive character: economy is considered as a set of individual consumers and producers, and the number of involved variables is absolutely unlimited. The system of general equilibrium is closed in the sense that the whole set of variables is determined by given conditions. In order to verify the compatibility of the system with the state of equilibrium, one only has to compare the number of equations with the number of unknown variables. However, there exists the problem of the existence of the point of equilibrium and of its uniqueness.

The dynamic analysis in economics formed in parallel with economic theory itself. A confrontation between the dynamic and static approaches can be easily traced throughout the whole history of the economic thought. Apparently, the reason lies in principal differences between the understanding of the balance of the equilibrium of forces and casual dynamics. There is a vast choice of literature references concerned with the theory of economic dynamics. Among a large number of different problems of evolutionary economics, the problems of economic growth and of business cycles are the most important ones. In the treatment of N. D. Kondratev, these distinctions between dynamic processes are interpreted as evolutionary (nonrecurrent, irreversible) and wave-like (recurrent, reversible). By evolutionary (or irreversible) processes one means those changes that in the absence of external perturbative interactions flow in a certain, one and the same, direction. Examples of such processes are given by tendencies of population growth, increase in the total volume of production, etc. N. D. Kondratev terms as wave-like (or reversible) those processes of changes that at each point in time have their specific direction and, consequently, change it permanently. In these processes, the phenomenon, being at a given moment in a given state and changing it afterwards, sooner or later may return to the initial state. The processes of changes in the prices of different consumer goods, interest rates, the level of unemployment, etc. may serve as examples.

In our view, more attention should be paid to the issue of slow (low-frequency) oscillations in economics, i.e., to the so-called long cycles (waves). N. D. Kondratev himself, while singling out long waves of economic activities, related them to the industrial revolution at the end of the XVIIIth - beginning of the XIXth centuries, the construction of railway networks, the dissemination of new communication means (telephone, telegraph) and of electric power, as well as rapid development of automotive industry [2]. Nowadays, the most wide-spread concept is that of five long cycles whose length is approximately equal to 50 years:

-

•

the end of the XVIIIth century - the first third of the XIXth century;

-

•

the second third of the XIXth century - the early 90s of the XIXth century;

-

•

the end of the XIXth century - the 30s of the XXth century;

-

•

the 40s of the XXth century - the 70s of the XXth century;

-

•

from the 80s of the XXth century up to the present time.

Let us try to understand the very nature of the mechanism of the long cycle. To initiate the expansion phase of the cycle, it is necessary to accumulate not only inventions but also capital as well as a desire of entrepreneurs to increase investments. For the industrialist, the dynamics of profit is a factor of primary importance. As a matter of fact, the expansion wave of the long cycle develops as a system of mutually related and mutually stimulating phenomena: an innovation provides a possibility to improve the production conditions, to reduce production costs and to increase profit, which stimulates entrepreneurs to introduce innovations under the condition of availability of necessary resources. Innovations give rise to an increase in profit, which generates additional investments, an increase in the volume of demand and a general positive movement of the growth rate of business factors.

However, at a certain moment the dynamics of the process exhibits a return point. A technological basis for this is provided by substantial weakening of the factors that initiated the expansion phase of the cycle. A cessation of their action slows down the growth of profitability and then decreases it, which reduces the interest of business structures in further innovations and investments. The industry slows down its growth, and negative effects of the economic life, typical of long-wave decline, appear. In the process of this decline, an increase in the number of new inventions takes place, which creates a prerequisite for the completion of the decline and the beginning of a new expansion wave.

N. D. Kondratev’s undoubted merit consists in the fact that he based his conclusions on an analysis of long temporal series of prices of the commodity output, of interest rates, wages, etc. The above-described dynamics is merely a simplified scheme, because the actual changes in the economy are much more complicated and diverse.

The modern status of macroeconomics cannot be understood without an evaluation of the contribution of J. M. Keynes. As a matter of fact , he created macroeconomics as a science in the 1930’s in order to explain the causes of the Great Depression that proved to be the most large-scale recession of the XXth century and, as such, the most important event in the modern history of business cycles [18]. The theory, existing at that time, could not explain why the GDP of the USA had fallen by one third from 1929 to 1933 and the unemployment level had risen to one fourth of the total work force. The classical theories were bases on the assumption that the economy was at competitive equilibrium, with the market regulating everything. In particular, high unemployment had to give rise to the reduction in wage rates down to the level where the employers would agree to employ all those who were willing to work for these wages and unemployment would disappear by itself. However, in practice, this was not the case. Therefore, Keynes put forward radically new ideas whose essence could be reduced to two major postulates.

Firstly, the economy is not at competitive equilibrium at each separate moment; that is, the ”invisible hand” of the market does not fulfil its duties. The basic reason for this equilibrium is the conservation of fixed prices and wage rates for a long time and the absence of adaptation to the current market conditions. Secondly, the level of the development of the economy is determined by the aggregate demand, and the latter, in its turn, depends on some unexplained factors that were vaguely termed by Keynes as ”the brute of investors”. On the basis of these two assumptions, the edifice of the theory of macroeconomics was erected. According to its postulate, the volume of the GDP of the country is influenced by the scale of expenditure of consumers, investors and the government on commodities and services. Therefore, business cycles are stipulated exactly by oscillations of the demand rather than by resources of the country. The first and main formal Keynesian model IS-LM was formulated on the basis of the Keynesian theory by J. Hicks in 1937.

In the course of the next several decades, up to the mid-70s, the discussion went on mostly in the mainstream of the Keynesian theory. The issue was whether the government should at all try to revive the economy in the periods of decline and, if it were so, by what means. According to the above-mentioned position, the government had to react to the decline by increasing government spending. From a point of view of other scientists and specialists, stabilization should be achieved by means of control over money supply: this point of view gave rise to the development of the doctrine of monetarism according to which the main objective of the state is to avoid strong oscillations of the money supply. Nevertheless, the positions of both the antagonistic scientific trends agreed on the point that the basis driving force of the cycle were oscillations of the volume of demand, and, therefore, the main differences between ”Keynesians” and ”monetarists” were almost completely obliterated.

However, in the mid-1970s the word economy faced a new phenomenon, i.e., stagflation, that could not be satisfactorily explained within the framework of the Keynesian concept. At that time, there appeared critical works of R. Lucas, subsequently the 1995 Nobel Prize winner, who criticized not only the economic policy of the authorities but also the whole Keynesian theory of business cycles for the disregard of optimum behavior of business agents including the formation of rational expectations. He suggested that, in contrast to investors and consumers in Keynes’s models that followed certain formal rules of behavior, business agents made, on the average, correct forecasts of the future state of the economy and adhered to the strategy of maximizing their own profits. All this created a demand for some alternative theory of business cycles.

This niche was occupied by the American economists F. Kydland and E. Prescott, who won the 2004 Nobel Prize for Economics. In their seminal paper [45], they proposed a new description of a real business cycle based on the fact that firms maximized the profit and made decisions to invest taking into account the expectation of future demand for their product and of the development of technologies.

Kydland and Prescott presented a series of dynamic models and showed what kind of behavior of basic economic variables (GDP, investment, and savings) was to be expected depending on the effect of technological shocks upon labour productivity and changes in external market conditions. The authors demonstrated that the results of modelling were in satisfactory agreement with the observed regularities. Besides, they drew an important conclusion that a considerable part of oscillations of GDP in many countries corresponded to the predictions of equilibrium models. In other words, there is no need to introduce into these models deviations from market equilibrium in the Keynesian spirit and to realize governmental stabilization policy.

For fairness, it should be noted that the theory of cycles of F. Kydland and E. Prescott by no means explains all the phenomena of actual economic reality: it is permanently subjected to constructive criticism by ”new Keynesianists”. In particular, the most striking example of disagreement between representatives of these two schools is an attempt to explain the technological boom of the 1990s. One is just left with expectations that in not too remote future a consensus will be achieved concerning the actual sources of business cycles.

In our point of view, the achievement of this goal is impossible without accepting the fact that economics, in essence, is a developing system and should be constructed within the framework of the theory of developing systems whose constructiveness is convincingly proved by the example of chemical kinetics, biology and other natural sciences. In this theory, it is shown that in the process of proceeding to the goal in the presence of substantially nonlinear feedback couplings, there emerges a whole hierarchy of instabilities that leads to the appearance of limit cycles, homoclinic structures and to spontaneous formation of chaos. As a result of such transformations (bifurcations), several different states of business equilibrium may appear (the so-called effect of bistability). The methods of nonlinear mechanics allow us to predict the moment of the occurrence of a chaotic regime in the system under investigation, the number of possible states of equilibrium and to determine the character of their stability. All this, in its turn, generates a principal general problem of the construction of alternative scenarios of complex, irreversibly developing system. It would be in order to mention here the statement of G. Malinetskii [28]: ”Indeed, social-technological objects are complex hierarchy systems, with various processes in them developing at different characteristic time scales. The rate of their instability, the limits of their predictability are different as well. In the economic system, the horizon of the forecast has fallen sharply: whereas just 15 years ago 5-year directive or indicative planning was a norm in the world, nowadays this is out of question. In the world, there is more and more supply of ’quick money’ and less and less supply of ’slow money’. However, on the other hand, stable development of the society requires slowly changing strategic goals, scales of social values and norms, culture and ideology. One needs technique, theory and formalism that would allow one to analyze possible dynamics of such ’different-time-scale’ systems and to direct their development on this basis.”

One can hardly question the fact that exactly the mathematical technique of nonlinear dynamics provides the very tools that allow us to approach closely the solution of the problem of ”designing the future”, of finding stable and safe ways of social and economic evolution. The experience of the application of methods and models of nonlinear dynamics has shown that many complex developing systems can be satisfactorily described with the help of a small number of variables, the order parameters. The determination of the order parameters is realized by reduction of the multidimensional system to a subspace of a small dimension owing to methods of the theory of bifurcations and of the theory of central manifolds. However, exactly this fact predetermines the locality of the carried out analysis of dynamic behavior of the studied system. Its applicability is admissible only in small neighborhood of the bifurcation point, to solutions of small amplitude. In what follows, we shall present other periodic solutions of small amplitude generated as a result of the Andronov-Hopf bifurcation of limit cycles and shall determine the character of their stability.

In this book, the choice of the discussed models is made more or less arbitrarily. The authors consider the models that are rooted in basic principles of traditional economics, neoclassical synthesis and Keynesianism.

Chapter 1 Instability and cycles in the Walras-Marshall model

Economics operates such notions as the quantity of goods (productive factors) and their price. In every market, there exist groups of sellers and buyers. In this chapter, a model of the market for one kind of goods will be considered. In the model of a single market the variables, i.e., functions of time, are the volumes of bought and sold goods as well as their prices. The basic principle of modeling of the market interaction is the formation of balance relations between the volumes of the demand and the supply of goods and, accordingly, the prices of the demand and the supply.

The problem of joint action of demand and supply as indicators determining quantitative relations between the volume of a commodity and its price in a given market is very precisely characterized by A. Marshall [29]: ”We could ask on equal grounds whether the price is regulated by utility or production costs, or whether a sheet of paper is cut by the upper or the lower blade of the scissors. Indeed, if one blade is kept motionless and cutting is carried out by the motion of the other blade, we can, without a good deal of thinking, argue that cutting is done by the second blade. However, such an argument is not completely exact, and it may be justified only by a pretension to mere popularity rather than to an exact scientific description of the realized process.”

For more concrete understanding of the modern phenomenological basis of demand and supply, we should present a definition of these notions, using the formulations given, e.g., in [16].

By the commodity demand one means the quantity of this commodity that an individual, a group of individuals or the population on the whole are ready to buy per unit time under certain conditions. A list of these conditions includes the tastes and the preferences of the buyers, the price of this commodity, the income rate, etc. By the demand price one means the maximum price the buyers agree to pay for a fixed quantity of a given commodity. At the same time, the dependence of the volume of the demand on its determining factors is called the demand function.

Analogously, the supply serves as a characteristic of the readiness of the seller to sell a certain quantity of the commodity in a fixed period of time.

By the volume of the supply one means the quantity of a certain commodity that one seller or a group of sellers are willing to sell in the market per unit time under certain conditions.

These conditions, as a rule, include the properties of the applied manufacturing technology, the price of the given commodity, the price rates of the employed resources, tax rates, subventions, etc. The supply price is the minimum price at which the seller agrees to sell a certain quantity of a given commodity. The dependence of the volume of the supply on the structure of its determining factors is called the supply function. Let us point out that the supply function as well as the demand function can be represented in three ways: in the form of numerical tables, graphically, and analytically. In what follows, we shall use only analytical representations for the functions of the demand and the supply.

1.1 Nonlinearity in the Walras model

In classical economic theory, one employs two equally admissible but principally different versions of the description of the mechanism of an interaction between the demand and the supply. The first approach, worked out by L. Walras, postulates that the driving force of changes in the price is the volume of excess demand under a given instant value of the price. In a dynamic aspect, the process of finding the equilibrium in L. Walras’s spirit can be represented in the form of the differential equation

| (1.1) |

where is the price of the commodity;

is the volume of the demand;

is the volume of the supply;

is a constant of the time of the limit process;

is time.

The sign of the quantity , called the volume of excess demand, determines the direction of the changes in the price. It is obvious that for the market price rises, whereas for it falls. The condition of the existence of an equilibrium price is the existence of the solution to the equation

| (1.2) |

There exists also a different approach to the problem under consideration, attributed to A. Marshall. Its essence is that a change of the volume of the mass of commodities in a given market is determined by the influence of the difference between the demand price and the supply price, to which the sellers (or the manufacturers) respond by an increase or a decrease in the volume of the supply of the commodity. In a mathematical form, this statement is expressed by means of the following differential equation:

| (1.3) |

where is the volume of the commodity;

is the demand price;

is the supply price;

is a time constant.

In Eq. (1.3), a surplus of the demand price over the supply price stimulates an increase in ; and if the supply price is higher than the demand price, the value of decreases. An equilibrium value of the volume of the commodity is determined from the equation

| (1.4) |

The algebraic equations (1.2) and (1.3) may have only one or several solutions. It means that both a unique state of equilibrium as well as a set of equilibrium states is possible. It is obvious that the nonuniqueness of equilibrium values of the volume and of the price of the commodity is explained by the presence of nonlinear relations in the basic equations.

An important problem is an analysis of the stability of the available states of equilibrium. It is necessary to ascertain the reasons why an equilibrium volume of the market remains constant under certain, remaining within certain limit values, fluctuations of the price, or on the other hand, why, under a given equilibrium price rate, changes in the volume of the commodity also take place. In what follows, by the stability of equilibrium we understand an ability of the overbalanced market to return again to the initial state owing to the action of endogenous factors. Besides, the problem of the stability of market equilibrium is directly related with the problem of the necessity to employ additional measures to regulate market relations.

First of all, let us consider the problem of stability of the economic model (1.1) described L. Walras’s theory. Let us set the coefficient in Eq. (1.1). In the neighborhood of the equilibrium point determined by the solution of Eq. (1.2), we can approximately represent the functions of the demand and of the supply in the form of polynomials obtained by the truncation of the corresponding Taylor series

| (1.5) |

If we introduce a new variable , which is a deviation of the price from its equilibrium value, equation (1.1) takes the form

| (1.6) |

where , , . Note that from (1.2) it follows , because , which is an equilibrium volume of the market. At the same time, is a stationary point (the state of equilibrium) of Eq. (1.6).

The differential equation (1.6) is called a dynamic system of the first order. The phase space of the considered system is one-dimensional, therefore, the studied process of change in the price can be represented by the motion of an image point on the phase straight [8].

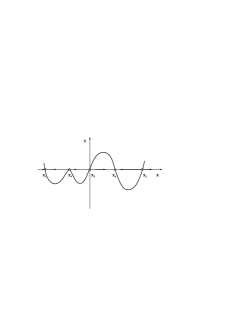

Indeed, in general, the main elements that determine the partition of the phase straight into trajectories are the states of equilibrium of the system. The values that make the function vanish are themselves independent phase trajectories. The rest of the trajectories consist of line segments between the roots of the equation , or of rays forming half-intervals between one of the roots and infinity. The direction of the motion of the image point along these trajectories is determined by the sign of the function : for the image point moves to the right, whereas for it moves to the left. If the form of the curve is known, it is not difficult to establish concrete partition of the phase straight into trajectories.

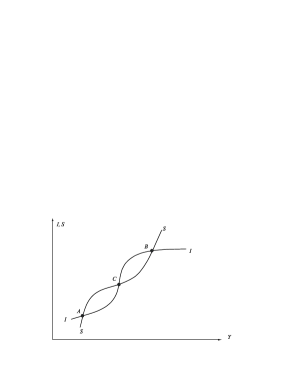

An example of such partition is given in Fig. 1.1, where the arrows show the direction of the motion of the image point. From the structure of the partition of the phase straight into trajectories, it follows directly that the states of equilibrium of the system at the points , are stable, whereas they are unstable at the points , , . It is directly seen in Fig. 1.1 that in the stable states of equilibrium the derivative , whereas in the unstable states . The value may occur at points of both the stable and unstable state of equilibrium. (This situation itself deserves independent consideration, because it requires some additional conditions for the determination of the type of stability of the stationary point.)

As the character of the change of the variable in the first-order system (1.6) is completely determined by the explicit form of the function , it is of interest to consider cases of different values of the order of the polynomial .

Let . Then is a linear function, and there exists the single state of equilibrium . The stability condition in this case is . This inequality reduces to the relation which is the classical condition of stability of L. Walras.

Let us try to interpret the linear stability of L. Walras using the notion of the elasticity of the demand and supply functions to price.

According to the definition of elasticity, in our notation, we have:

or, taking into account that ,

| (1.7) |

where , are coefficients of the demand and supply elasticities to price. They are dimensionless, i.e., relative, quantities.

Therefore, the inequality can be easily reduced to the form

| (1.8) |

Given that , are always positive, the condition of L. Walras is formulated as follows: for the stability of the linear system (1.6) with , it is necessary that the elasticity of the volume of the supply to price should exceed the corresponding demand elasticity, i.e., . In other words, if we introduce the quantity conditionally termed an excess-demand elasticity to price, the stability of (1.6) is determined by the sign of : for , we have stability, and, on the contrary, for , we have instability.

Let us consider the peculiarities of the behavior of the system (1.6) in the case . Here, is a quadratic function of the initial variable.

The equation , or , has two roots: and . To determine the character of stability of each singular point, it is necessary to evaluate .

As a result of differentiation, we have:

| (1.9) |

The substitution of the values of and in expression (1.9) yields

It is thus obvious that the stability of both the states of equilibrium is completely characterized by the sign of the quantity (or ).

In this case, if , i.e., if the demand is more elastic than the supply, the state of equilibrium is unstable, whereas is stable.

On the contrary, for (the demand is less elastic than the supply), is a stable state of equilibrium, and, accordingly, is an unstable one.

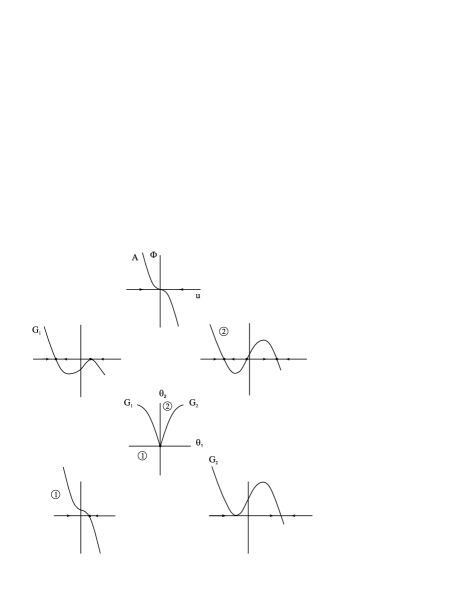

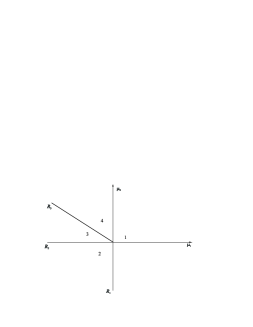

In a noncoarse situation, when is a small quantity changing its sign in the neighborhood of zero, the so-called transcritical bifurcation appears illustrating a change of stability of the states of equilibrium: see Fig. 1.2, where .

As a result of this bifurcation, the singular points and merge for , i.e., when the elasticity of the demand is equal to that of the supply, to form the single two-fold state of equilibrium . At the same time, the condition is important.

Here, we can observe a considerable difference between the behavior of the nonlinear system from that of the linear model, which manifests itself in the present of two equilibrium values that are transformed into one and the same point of equilibrium as a result of a transcritical bifurcation.

It seems to be reasonable to attribute pithy economic meaning to the coefficient of the quadratic term, , in terms of elasticities of the demand and supply functions. To this end, it is necessary to find the derivatives of the corresponding types of elasticity with respect to the price at the point . Skipping over intermediate transformations, we present the following expressions for the quantities and as functions of , , , :

| (1.10) |

It is worth noting that the dependence of the coefficient on the excess-demand elasticity and on its derivative with respect to the price is a linear function.

Let us consider the case when the function of an excess demand in the system (1.6) is cubic. This takes place for , and, accordingly,

The cubic equation may have, depending on the coefficients, one or three real roots, and, accordingly, the system (1.6) may have one or three states of equilibrium.

By analogy with the previous case, the stability of each state of equilibrium is determined by the sign of .

Let the system (1.6) have the representation

| (1.12) |

Assuming the parameters , to be small, sign-alternating quantities, we consider the deformation of the saddle-node bifurcation with an additional degeneracy in the quadratic term [4]. In the saddle-node case, the truncated system with , takes the form

| (1.13) |

After some thinking, we can arrive at the conclusion that there exist small perturbations of the function when the system possesses one or three hyperbolic fixed points (the states of equilibrium) in the neighborhood of , as well as certain ”unusual” perturbations when the system possesses two fixed points, with one of them being nonhyperbolic. All the above-mentioned possibilities can be accounted for by adding low-order terms. It is customary to represent this deformation in the form of the equation

| (1.14) |

where , , .

Here, , are also small quantities. The dynamics of this vector field is formed, with the accuracy of topological equivalence, by its fixed points and the types of their stability. Generally speaking, mathematical theory of singularities provides the means for a systematic study of zeros of families of mappings, with one of the examples being given by the right-hand side of Eq. (1.14).

Let us find the bifurcation set of parameters in the parameter plane , by demanding that the right-hand side of (1.14) and its derivative with respect to the variable vanish:

| (1.15) |

By eliminating the variable from both the equations of the system (1.15), we arrive at the following bifurcation set:

| (1.16) |

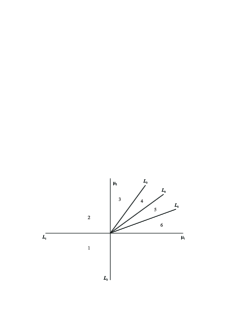

The bifurcation diagram of the system (1.14) is presented in Fig. 1.3 for the case . The system (1.14) may possess one or three coarse states of equilibrium. These states of equilibrium merge in pairs on bifurcation lines and [formula (1.16)] that form Neile’s semicubical parabola with the origin at the point . The point corresponds to merging of all the three states of equilibrium into one state. For the values of the parameters in the plane , that lie inside the parabola (region 2), the system (1.14) possesses three states of equilibrium (two stable states and one unstable state in between), whereas for the ”outside” values of the parameters (region 1) there exists one (stable) state of equilibrium.

It should be noted that, for bifurcation values of the parameters, a projective mapping of the manifold onto the parameter space has fold-type singularities. The dynamic system in the neighborhood of the bifurcation exhibits hysteresis. Let us change the parameters in order to cross the semicubical parabola, while keeping watch on the stable equilibrium regime (Fig. 1.3). In the process of motion from left to right, the ”breakdown of equilibrium” of equilibrium occurs on the right branch , whereas in the case of the reverse motion it occurs on the left branch . This phenomenon is called ”a hysteresis loop”.

From formula (1.16), it is not difficult to obtain an explicit form of the bifurcation set in terms of the initial parameters , . Using (1.14) and (1.16), we derive the relation

| (1.17) |

Furthermore, if we take into account the expressions for and in terms of the demand and supply elasticities to price, using (1.8) and (1.11), we obtain the following expression for the bifurcation line:

| (1.18) |

In the equality (1.18), the value of the excess-demand elasticity and its derivative with respect to the price are small quantities. Therefore, we can argue that the above-mentioned bifurcation can be observed in the initial dynamic system for very close values of the demand and supply elasticities, and of their derivatives, i.e.,

| (1.19) |

Such a type of behavior cannot be explained by means of the methods of comparative statistics traditionally applied in economic analysis. Exactly the analysis of the dynamics of the system in the neighborhood of the state of equilibrium has shown that the behavior of the system is no longer characterized by a unique and smooth reaction to small shifts of the parameters. At the same time, there emerge a variety of states of equilibrium, including multiple and sudden jumps stipulated by the irreversibility of the flowing processes.

Analogously, one can carry out an investigation into the dynamics of the process of establishing the equilibrium value of production according to the concept of A. Marshall, described by the differential equation (1.3.) However, in contrast to the Walras model, in this case an analysis of the stability of the studied dynamic system involves such substantial economic characteristics as the values of elasticities of the prices of the demand and of the supply to the production volume.

It should be noted that the above results ask for more profound understanding of P. Samuelson’s principle of correspondence whose validity relies on the suggestion of predetermined stability of the economic system, with changeability bearing a smooth character.

1.2 A modified Walras-Marshall model

Up to now, we have considered the processes of changes of the market price and of the volume of commodity production as independent, and the mathematical models (1.8) and (1.11) have been studied separately. Therefore, in what follows, in order to study the dynamics of a model of a certain industrial object, we shall make an attempt to unify the equations of Walras and of Marshall into a single economic system, where the processes of production and of formation of the price are mutually related [13].

The issue of price formation in productive economic systems has always been and still remains relevant both for theoretical economic analysis and for the solution of concrete practical problems of the enterprise as well. In our view, it is important to synthesize two major factors of price formation. Thus, on the one hand, classical theory of market price formation argues that the market price corresponds to the equality of the demand and of the supply in the commodity market. On the other hand, according to the theory of the firm, it is known that, in the case of production balance, the price of the products manufactured by the enterprise corresponds to the marginal production costs. Thus, the first approach treats price formation from the point of view of the consumer, whereas the second one does it from the point of view of the producer. However, realities of the economic life witness that the processes of changes in the price and in the volume of production flow simultaneously and are interrelated. Therefore, it seems to be reasonable to consider the market mechanism of balancing the demand with the supply and the production process of accounting for the profit and costs simultaneously, within the framework of a unified dynamic system, according to the methodology presented in the work [5].

As the starting point, we consider a mathematical model describing the dynamics of the interaction between the prices and the volume of production (manufacturing):

| (1.20) |

where is the price of the produced and sold product;

is the volume of the product in natural terms (the market supply of the commodity);

is the market demand for the product in natural terms;

is the supply price, equal to the marginal production costs, i.e., ;

are the production costs (expenses);

, are constant positive parameters describing characteristic times of transient processes.

The first equation of the system of the two ordinary differential equations (1.20) is the classical model of market price formation in the form of L. Walras (or P. Samuelson). They are based on the scheme of price formation searching for the balance between the demand and the supply: for the price rises, whereas for the opposite sign of the inequality it falls. The second equation of (1.20) describes the process of establishing the balance between the price and the marginal production costs with respect to the production (the value of production). Here, it is assumed that the balance is disturbed and it is necessary to regulate the volume of production: if , the profit of the producer rises with an increasing the production volume, whereas in the opposite case one should decrease production activities.

The model is based on substantial simplifications. Firstly, the production is assumed to be single-product. Secondly, a local outlet without competition is considered, when the whole supply is formed by one producer. However, in spite of the above-mentioned assumptions, the model (1.20) admits complicated types of behavior, and their analysis will be the subject of further consideration.

A formal analysis of qualitative properties of system (1.20) should start with the consideration of singular solutions that characterize the states of equilibrium of the economic model.

By making the left-hand sides of (1.20) vanish, we obtain two constraint relations between equilibrium values of the price and of the volume :

| (1.21) |

Let us assume that the system of algebraic equations (1.20) has, at least, one positive solution . concerning the volume of the demand , we point out that the dependence on the price is a substantially nonlinear function and there exists a Taylor expansion up to the third order in the neighborhood of the point :

where , .

The cost (expenses) function is represented by a quadratic function of the volume of production:

where , , are constant parameters.

Accordingly, the marginal costs (the supply price) are described by the formula

Having preliminarily changed the time scale, it is convenient to study the system (1.20) in terms of new variables that represent deviations from the equilibrium values , . In this case, the system (1.20) reduces to the form

| (1.23) |

where .

As is obvious, equations (1.23) possess the trivial state of equilibrium , .

To study the stability of the trivial state of equilibrium, we write down an explicit expression for the characteristic equation of the linear part of the system (1.23):

| (1.24) |

The inequality (1.25) determines restrictions on the parameters of the initial system for stability in the linear approximation.

Let us consider in greater detail the situation in the vicinity of the boundary of the region of stability, taking into account the equality

| (1.26) |

where is small, sign-alternating quantity. It is obvious that, in this case, the divergence of the vector field of the system (1.23) is equal to the small parameter . Therefore, for the type of the singular point (the state of equilibrium) is a stable focus, whereas for it is an unstable focus. In other words, for , in the neighborhood of the equilibrium state, there occurs the formation (annihilation) of a limit cycle as a result of the Hopf bifurcation.

Let us verify the validity of the conditions of Hopf’s theorem as applied to the system (1.23). The eigenvalues are determined (for ) by the equality

| (1.27) |

where , , i.e., they are purely imaginary. Upon the substitution of (1.26) in the quadratic equation (1.24) and subsequent differentiation with respect to the parameter , we obtain for :

| (1.28) |

From (1.28), it follows that the real part of the eigenvalue with respect to the parameter does not vanish, i.e., the eigenvalues in the complex plane cross the imaginary axis with a nonzero velocity. As a result, all the conditions of the Hopf bifurcation theorem are fulfilled.

Let us turn once again to (1.26) in order to give meaningful interpretation of this equality.

The above-mentioned condition can be fulfilled is the parameters and have the same sign. As in the following the value will figure as the bifurcation parameter, its positivity characterizes concavity of the function of expenses , whereas its negativity, accordingly, characterizes convexity. From an economic point of view, determines a positive effect of the volume of production (), whereas means that a rise in the costs outruns the output of the products (), i.e., the production is resource-consuming.

In order to determine essential parameters of the limit cycle that characterize its stability and the structure of periodic solutions, we reduce the system of differential equations (1.23) to the Poincaré normal form by means of a corresponding change of variables , . As a result of the reduction, we obtain for :

| (1.29) |

Using the explicit form of the coefficients of the nonlinear terms of the system (1.29), we derive an expression for the first Lyapunov quantity:

| (1.30) |

For , a stable limit cycle takes place, and a corresponding regime of self-oscillations is called ”soft”. On the contrary, if , the limit cycle is unstable, the self-oscillations break down ”rigidly”, with a manifestation of irreversibility (hysteresis). The case is the most complicated one in the sense of a variety of phase-plane structures of the system (1.29), because there appears a possibility of simultaneous coexistence of two limit cycles (with one being stable and the other one unstable) that subsequently merge into a single multiple limit cycle. This bifurcation has codimension two and will not be studied in detail in this Chapter.

The periodic solution of small amplitude (up to a choice of the initial phase) is itself written down in the form [37]

| (1.31) |

Here, is the amplitude; , is the period of the cycle depending, generally speaking, on the amplitude.

Thus, by the example of the system of two nonlinear differential equations (1.29), it is easy to establish that, in contrast to a linear system, periodic solutions are no longer harmonic, and the period and the amplitude of the oscillations are interrelated.

As an illustration of the obtained results, consider examples of economic-capacity cycles for different groups of commodities with regard to the dependence of the demand functions on the income, following the classification of the Swedish economist L. Tornquest [36].

Example 1. The demand function for essential commodities has a representation

which reflects the fact that an increase in demand for these essential commodities gradually slows down with an increase in the income and has a has a limit . The parameter is called the constant of half-saturation of the income.

Assuming that an equilibrium income is a function of the price,

we express the demand in the form . After corresponding transformations, we get

| (1.32) |

Differentiating (1.32) with respect to the price, we obtain the coefficients of the demand function:

| (1.34) |

From (1.34), it follows that the quantities , are negative numbers, and, therefore, by (1.30), the emerging limit cycle is stable. At the same time, the reason for the emergence of the cycle is the fact of positive influence of the effect of the scale of production of the given group of commodities, i.e., .

Example 2. The demand-for-luxury-goods function is represented in the form

By analogy with Example 1, we express the demand as a function of the price:

| (1.35) |

where , , are positive parameters.

The equation for an equilibrium price has the form

| (1.36) |

Assuming that (1.30) has at least one positive root , we evaluate the coefficients of the powers of :

| (1.37) |

In this case, the coefficients and are positive numbers, and the substitution of their values in (1.30) ensures the condition , which is an indication of a catastrophic loss of stability of the limit cycle. As , the emergence of a limit cycle requires the fulfillment of the condition , which is possible only for resource-consuming production with an outrunning increase in the costs.

Let us consider one more version of the model (1.20), assuming, as a preliminary, that the supply price is a nonlinear function of the volume of production. For simplicity, we consider the quantities and to be deviations from certain equilibrium values and .

Concerning the demand function and the price, we put forward an assumption that they quadratically depend on their arguments, i.e.,

One can argue that a linear analysis of the stability of (1.38) completely corresponds to the previously obtained results for the system (1.23), including a verification of the validity of Hopf’s theorem, up to the substitution of for the parameter . Therefore, assuming the closeness of the bifurcation parameter to the quantity , we transform (1.38) to the normal form of the given bifurcation with the help of the change of variables , (). After some transformations and the introduction of a new time scale , we obtain:

| (1.39) |

Let us represent the system of two ordinary differential equations (1.39) in the form of a differential equation for the complex variable , :

| (1.40) |

where ;

;

.

Now, we possess all the necessary information for the evaluation of the first Lyapunov quantity

Taking into account the explicit form of the coefficients of Eq. (1.40), we get:

| (1.41) |

From (1.41), it is obvious that for the limit cycle is stable, whereas for the instability of the limit cycle takes place.

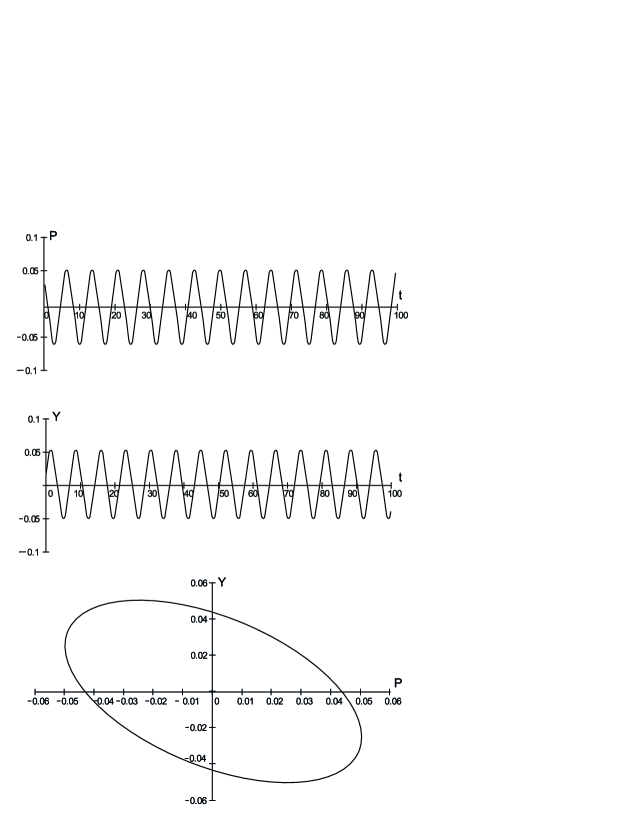

In Fig. 1.4, we present cyclic changes of the price and of the volume of the commodity of the considered state of equilibrium for the following values of the parameters of the system (1.38):

The condition makes the expression for the first Lyapunov quantity vanish. This may mean that the initial system (1.38) possesses two limit cycles that can merge into one two-fold cycle by means of trajectory compaction. This situation is possible, if the second Lyapunov quantity, , does not vanish. Setting for definiteness , as a result of evaluation, we obtain . Moreover, , the next (third) Lyapunov quantity also vanishes under the given conditions. The fact that all the first three Lyapunov quantities vanish means that the state of equilibrium is a center, not a focus. In other words, the initial system (1.38), for

| (1.42) |

turns into a conservative one, with the conservation of the phase volume.

Let us write down the explicit form of (1.38), eliminating the parameters , with the help of Eqs. (1.42):

| (1.43) |

It is important for us to find the first integral of the system (1.43). To this end, we transform the variables and with the help of the linear substitution

| (1.44) |

where , , .

The system (1.45) can be reduced to a total differential equation:

| (1.46) |

By introducing the integrating factor into (1.45), we obtain the following equation:

| (1.47) |

The integration of Eq. (1.45) yields

| (1.48) |

where is an arbitrary constant determined from the initial conditions.

Thus, expressions (1.44) and (1.48) determine a functional interrelation between the price and the volume of the commodity, which is a permanent balance between the income of the producer and his expenses at any moment of time.

Returning to the system (1.38), we should be reminded of the fact that the coefficients , are the demand elasticity and its derivative with respect to the price, whereas , are price demand elasticity and its derivative with respect to the volume of the commodity, i.e.,

(It is understood that the elasticities and their derivatives are evaluated at the trivial state of equilibrium.)

Chapter 2 Periodic regimes in nonlinear models of the multiplier-accelerator

2.1 A multiplier-accelerator model with finite duration of an investment lag

In this Chapter, we consider an example of a certain kind of multiplier-accelerator models that illustrates at a phenomenological level different aspects of the problems of business cycles. As the starting point, we use the investment model of Goodwin [1] that possesses a nonlinear element built in the system of a multiplier-accelerator interaction. The dynamics of this model is characterized by the lag of two types: from the point of view of investment demand, there is a finite-duration lag of the action of the accelerator, whereas there is a continuously distributed lag on the part of supply.

As the main variable, the model involves profit or an output . An excess demand is formalized by the equation

| (2.1) |

where is a cumulative demand comprising a consumer demand , an investment demand , and independent expenses . All the above-mentioned terms are the actual costs. It is assumed that the consumption is directly proportional to the profit and the lag is absent, i.e., , where the quantity characterizes a marginal propensity to consume. We also assume that the actual investments outlay is carried out with a certain fixed lag of the duration of units of time after an investment decision is made, i.e., . Exactly here, the action of the accelerator manifests itself as a functional relation between the volume of investment decisions and an instantaneous velocity of the change in the profit (output volume) . In the most general form, this relation can be represented as follows:

where is a certain nonlinear function possessing the property of saturation.

In other words, for small changes in the profit, the classical linear accelerator comes into play, whereas for a further increase in the profit (output volume), the function reaches its upper bound determined by the resource and capacity limits of the structure of the production.

When the volume of the production output substantially decreases, the quantity tends to its lower bound that depends, generally speaking, on the amortization quota of the fixed capital. For the sake of convenience of further mathematical transformations, within the framework of the model under consideration, we restrict ourselves to a Taylor expansion of the function up to the third order:

where , , are corresponding derivatives of the function .

Given that we have already described the main components of the cumulative demand function, we obtain the following equation:

| (2.2) |

Concerning the independent expenses , it should be noted that they can be considered fixed, i.e., .

Consider next the situation on the part of supply. The main assumption is that value of the output volume lags behind the value of the cumulative demand . The lag is considered to be continuously distributed, and it can be represented by a linear first-order differential equation:

| (2.3) |

where is a constant of the time lag characterizing the dynamics of adjustment between the demand and the supply.

A balance synthesis of the demand and the supply, by (2.2) and (2.3), yields a differential equation with a retarded argument:

| (2.4) |

Equation (2.4) represents the general multiplier-accelerator model of Goodwin with nonlinear interactions.

With regard to the form of (2.4), it is nothing but a mixed differential-difference equation.

As is obvious, equation (2.4) has a singular solution that represents an equilibrium level of profit (output volume) resulting from the action of the static multiplier. In what follows, it is reasonable to introduce the variable that represents a deviation of the profit from its equilibrium value.

In terms of the new variable , equation (2.4) takes the form

| (2.5) |

where is a marginal propensity to save.

The given model, represented by Eq. (2.5), determines the dynamics of profit (output volume) in terms of deviations from the above-mentioned equilibrium level .

For the sake of a further analysis of dynamic properties of the considered process of changes in profit, it is necessary to carry out a sequence of mathematical transformations and simplifications that will allow us to reduced the mixed first-order differential-difference equation to an ordinary differential equation of higher order [35].

Let us introduce new time instead of . Then, equation (2.5) can be represented as

| (2.6) |

Our next step consists in expanding the left-hand side of Eq. (2.6) into a power series in , while retaining terms containing the first power of . We obtain:

or

| (2.7) |

In Eq. (2.7), we substitute the explicit form of the function as a cubic polynomial. As a result of transformations, we obtain an ordinary second-order differential equation:

| (2.8) |

Making the change of variables , , we represent (2.8) in the form of a system of two differential equations:

| (2.9) |

It is natural to begin the qualitative study of the dynamic system (2.9) from an investigation into the states of equilibrium. As is obvious, equations (2.9) possess only the trivial state of equilibrium , . To classify the type of this singular point, it is necessary to find characteristic numbers of the linear part of (2.9) determined by the quadratic equation

| (2.10) |

From the explicit form of (2.10), one can infer that the singular point of the system (2.9) may be either a stable (unstable) node or a stable (unstable) focus. Of primary interest for us is the situation when a complex focus changes its stability, which may be accompanied by the formation of a limit cycle giving rise to a corresponding self-oscillation regime. In this case, we represent the solution of (2.10) in the form

| (2.11) |

where , , and is a small quantity. In other words, for , accordingly, the eigenvalues are purely imaginary: .

By differentiation expression (2.10) with respect to the parameter , we obtain: . This means that the eigenvalues cross the imaginary axis with a nonzero velocity. Therefore, we can argue that the conditions of Hopf’s bifurcation theorem are fulfilled, and the system (2.9) allows for the formation of a limit cycle from the complex focus.

It would be in order here to draw attention to the reason for the occurrence of instability in the multiplier-accelerator model. As it seems, exactly the accelerator ”blows up” the damped oscillations induced by the multiplier and generates a structural self-sustained oscillation motion (self-oscillations). We have already seen that instability occurs in a given economic system when one of its parameters changes. It is most natural to consider as a variable parameter the coefficient of the linear accelerator whose critical value changes the direction of damping in the system (2.9). Thus, the coefficient plays the role of a bifurcation parameter. The criterion of stability can now be written down in the form . A linear analysis shows that when , while increasing, passes through the value , a loss of stability of the focus is caused by a pair of complex conjugate eigenvalues of the matrix of the coefficients of the linear part of the system (2.9).

The loss of stability at occurs under the conditions of Hopf’s theorem that states that, in addition to a stationary solution, there appear periodic solutions.

However, Hopf’s theorem itself does not provide information on whether these periodic solutions describe regimes that can be actually observed as steady ones. Periodic solutions may prove to be unstable and, accordingly, unobservable without the use of special procedures. Therefore, the next goal of our study of emerging periodic solutions in the system (2.9) is to derive explicit formulas describing their stability, amplitude, and period.

To achieve the above-mentioned goal, we shall use the techniques presented in [37]. For the sake of convenience of the application of the proposed methods, we shall retain original notation.

In order to reduce the system (2.9) to the normal Poincaré form, we make the change of variables , . As a result, for , we obtain

| (2.12) |

Let us represent the system of the two ordinary differential equations (2.12) in the form of a complex differential equation with respect to the variable :

| (2.13) |

where is the complex conjugate of , and the inverse change of variables yields , .

For further evaluation, we need only the coefficients , , , and . Their explicit forms are

| (2.14) |

Given expressions (2.14), we obtain the following:

1) the value of the first Lyapunov quantity

| (2.15) |

2) the amplitude of small oscillations

| (2.16) |

3) an approximate value of the period of oscillations

| (2.17) |

The periodic solution itself, up to the choice of the initial phase, in terms of the original variable, is written down in the form

| (2.18) |

It is important for us to know the sign of the coefficients that determines the sign of the first Lyapunov quantity in (2.15). For , , and, accordingly, the limit cycle is unstable; that is, rigid excitation of self-oscillations takes place, accompanied by the phenomenon of hysteresis. However, the assumption of the positivity of is unrealistic, because the condition of achieving the limit saturation () under an increase (decrease) in the velocity of changes of profit will not be satisfied. Therefore, we should set (). In this case, a stable limit cycle is generated with a soft excitation regime of self-oscillations.

While analyzing the explicit form of the approximate solution for in expression (2.18), we should note the contribution of the coefficient . A nonzero value of introduces certain asymmetry into the structure of the resulting oscillations. Obviously, they are nonharmonic even for small values of the amplitude. Besides, the coefficient induces an increase in the period of oscillations with a growth in their amplitude.

An economic meaning of the asymmetry of the cycle consists in a difference between the duration of periods of expansion and that of periods of decline, which, on the whole, is a characteristic feature of nonlinear models of economic dynamics.

Somewhat earlier, we considered in detail the influence of the accelerator parameter on the degeneracy of the linear part of the system (2.9) that directly induced a bifurcation of limit-cycle generation from an equilibrium state of the complex-focus type and the establishment of the regime of self-sustaining oscillations [12].

Summarizing, we want to emphasize that, in the present study of behavioral properties of the nonlinear multiplier-accelerator model of Goodwin, we have ascertained the mechanism of the occurrence of a cycle; we have determined the type of its stability, and we have given meaningful interpretation of the influence of all the parameters of the nonlinear accelerator on peculiarities of the self-oscillation regime.

2.2 A model of the multiplier-accelerator with a continuously distributed lag

In the previous Section, we have studied in detail an example of one nonlinear model of the multiplier-accelerator characterized by the occurrence of a stable limit cycle in the neighborhood of an equilibrium state. In that case, an essential element in the construction of the accelerator has been a finite-dimension lag in the functional relation between the measure of the volume of investment decisions and the instantaneous velocity of the change in profit (output volume). As basic assumptions in the synthesis of the initial model, we have employed nonlinear dependence of the accelerator on the derivative of profit, as well as linear dependence of the consumption function on the value of profit.

In the present consideration, the multiplier-accelerator model will be represented in a different form. First of all, we assume that the action of the accelerator is now expressed in terms of a continuously distributed lag [14].

According to R. Allen [1], if the investment function represents the actually induced investment at the moment of time , caused by changes in the output volume , the lag is described by the differential equation

| (2.19) |

where is a nonlinear accelerator function, and the parameter characterizes the rate of changes in the investment function . Concerning , it should be noted that its behavior for small changes in the profit is close to linear one, whereas with a further increase in the accelerator function grows slower and may even become non-monotonic. We shall assume that the mechanism of the action of the accelerator is satisfactorily described by the cubic parabola

where , , are corresponding derivatives of .

The next step consists in the introduction of a lag into the model of the multiplier. In an analysis that follows, we shall also employ a continuous representation for the description of the action of the multiplier effect by means of a corresponding differential equation.

Let us assume that on the part of cumulative demand, a lag is absent. The planned consumption is given by , and independent expenses are determined by the quantity

Then, the cumulative demand can be represented in the form of the equation

| (2.20) |

Here, we give up the hypothesis that the consumption function is linear and assume that is a substantially nonlinear function of the output volume .

In the most general case, we restrict ourselves to representing in the form of a third-order polynomial, i.e.,

The coefficients , have the same meaning as in the case of the accelerator function. Moreover, , whereas and may have opposite signs.

The parameter of independent expenses is considered to be constant.

Consider the situation on the part of supply. Here, a response of the output volume to the cumulative demand is considered to be non-instantaneous, inertial, i.e., there exists a continuously distributed lag in the form of a corresponding differential equation:

| (2.21) |

where is a time constant of the multiplier

Equations (2.19)-(2.21) completely determine the system of two nonlinear differential equations that describe an interaction between the multiplier and the accelerator. This system is represented as follows:

| (2.22) |

Given that , the system (2.22) has singular solutions determined by the system of algebraic equations

| (2.23) |

The first equation of (2.23), by the explicit form of , may have up to three roots that represent the coordinates of an equilibrium state of the system (2.22).

We represent the system of two differential equations (2.22) in the form of a single second-order differential equation:

| (2.24) |

where .

With the help of (2.24), we have succeeded in eliminating dependence on the variable . In what follows, we shall operate a vector field composed of the variables and . Introducing the coordinates and , it is reasonable to transform Eq. (2.24) into a system of two first-order differential equations:

| (2.25) |

As is obvious, the system (2.25) possesses the same states of equilibrium as the system (2.24) does.

Let the coordinates of a single point be given as , where is the solution of the equation . In order to analyze behavioral properties of the system (2.25) in the neighborhood of the given state of equilibrium, we introduce new variables and .

Given the explicit form of the nonlinear consumption function , as a result of some transformations, we arrive at the system of differential equations

| (2.26) |

where .

Let us consider a particular case of the system (2.26) under the conditions , . Under the above-mentioned restrictions, the quadratic terms in (2.26) vanish; that is, there is symmetry with respect to the change , . Furthermore, under the assumption that

the equation for singular points is factorized as follows:

| (2.27) |

Accordingly, is the coordinate of the state of equilibrium in whose neighborhood the behavior of the system (2.26) is being studied. To ensure the positivity of , we assume that , , and the parameter.

We shall be concerned with qualitative properties of the system (2.28) in the neighborhood of the trivial state of equilibrium , . To determine the type of equilibrium, it is necessary to ascertain spectral properties of the linear part of (2.28) with the characteristic equation

| (2.29) |

where .

The explicit form of the quadratic equation (2.29) is analogous to that of the characteristic polynomial in [12]. Therefore, when analyzing the situation with the occurrence of a periodic regime in the system (2.29) resulting from the change of stability of the singular point of the type of a complex focus

we can arrive at the conclusion that the reason for this effect is transition of the linear parameter of the accelerator through a certain critical value .

Note that the derivative of the eigenvalue with respect to the parameter is nonzero:

In this case, we may argue that the conditions of Hopf’s theorem are satisfied, and a limit cycle around the trivial state of equilibrium is generated in the system (2.28) from a complex focus.

The fact that a self-oscillation regime is present is rather remarkable in itself; however, it does not provide much information. Hopf’s bifurcation theorem does not give any answer to the question about the uniqueness of the limit cycle and the character of its stability.

To resolve the posed problems, we reduce (2.28) to the normal Poincaré form for , using the change of variables , :

| (2.30) |

Making use of the explicit expressions for the coefficients , it is not difficult to determine the first Lyapunov quantity:

| (2.32) |

As before [5], we assume that, as a result of the effect of investment saturation, , whereas the coefficient . Therefore, a sign change in expression (2.32) is possible, which is a manifestation of different types of stability of the limit cycles. From (2.32), the stability of the limit cycle for () follows directly, whereas for the opposite sign of the inequalities an unstable self-oscillation regime with a catastrophic loss of stability takes place.

The case when the first Lyapunov quantity is small and alternates the sign, i.e.,

| (2.33) |

is of much greater interest.

As is well-known [6], the behavior of dynamic systems in the vicinity of the parameter values satisfying the equality , such that the first Lyapunov quantity vanishes, substantially depend on the sign of the second Lyapunov quantity . Depending on the first and the second Lyapunov quantities, as well as on the sign of the real part of the roots of the characteristic equation , in small neighborhood of the state of equilibrium on the phase plane, one or two limit cycles may exist with all possible combinations of stability and instability: namely, one stable or unstable limit cycle, or two limit cycles (a stable one inside an unstable one or vice versa).

The second Lyapunov quantity is determined by the expression

| (2.34) |

After substitution in (2.34) of the actual values of the parameters, we obtain:

or, by the validity of ,

| (2.35) |

As is obvious, the quantity does not vanish for any values of the parameters and is strictly positive, i.e., .

If we make a conversion from the complex-valued variables to polar coordinates, we get two independent equations for the amplitude and the phase of the cycles:

| (2.36) |

The states of equilibrium for the first equation of (2.36) satisfy the biquadratic equation

| (2.37) |

Equation (2.37) may have either none or one, or two positive solutions (cycles).

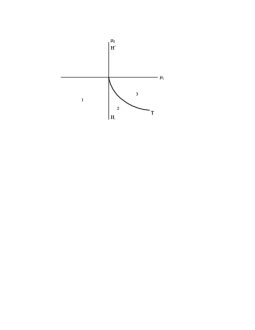

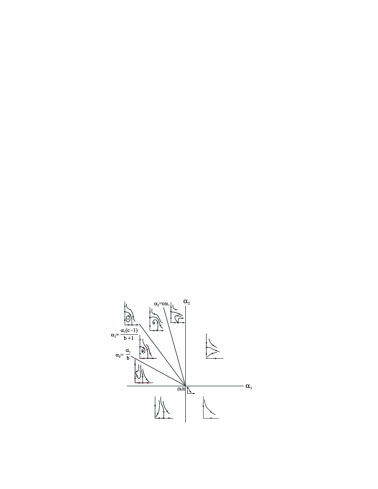

In Fig. 2.1, we present the corresponding bifurcation diagram. The line relates to the usual Hopf’s bifurcation. The state of equilibrium is stable for , and it is unstable for . If we move along the line to the points where , the complex second-order focus on the phase plane will generate an unstable (coarse) limit cycle, whereas the focus itself becomes non-coarse and stable. Should we enter, while crossing , region 2, the stable complex focus generates a stable limit cycle. In region 2, both the cycle, the stable one and the unstable one, coexist simultaneously; the merge and disappear on the line .

The line characterizes the bifurcation of the double cycle. Further in region 3, limit cycles are absent.

In Fig. 2.2, the region of the coexistence of the two limit cycles is shown.

In conclusion of this investigation, we would like to point out the following: the presence of two limit cycles in the initial dynamic system of the multiplier-accelerator is stipulated not only by the nonlinearity of the accelerator function, but also by substantial nonlinearity of the consumption function, because exactly a relation between nonlinear coefficients of these functions ensures the bifurcation of the double cycle.

2.3 Cyclic regimes in a nonlinear model of the multiplier-accelerator with two degrees of freedom

Consider a model of the multiplier-accelerator with spatial inhomogeneity. Such a model reflects peculiarities of interregional trade in the presence of an import-export multiplier, which agrees with the already studied multiplier of local expenses, as well as with the general concept of Keynes and Samuelson [30, 31]. Let the quantity of an imported commodity depend on the local profit , which is now a function of time and of a generalized spatial coordinate . Assuming, as the first approximation, that the action is local, we suppose that the commodity is imported from the nearest neighborhood of a considered point, whereas the exported product is produced under the influence of the same propensity to import in the neighborhood of this point. Then, the net trade surplus is determined by the product of a constant propensity to import and a profit margin in export-import operations. In other words, the above-said can be represented in the form of the following expression:

where is an export volume;

is an import volume;

is a constant propensity to import.

The spatial model of the multiplier-accelerator is represented in the form of a single second-order differential equation with a nonlinear investment function:

| (2.38) |

where is a marginal propensity to save;

is the coefficient of the accelerator.

In our consideration, we assume that all the parameters of the model, i.e., , , and , are constant positive quantities that do not depend either on time or on the spatial coordinate.

The model described by Eq. (2.38) is a rather complicated mathematical object that exhibits a variety of forms of spatial-temporal organization. Therefore, in what follows we shall focus on dynamic processes, having preliminarily subdivided the space into two parts interrelated by the regional trade. This will allow us to study such phenomena as frequency matching and quasi-periodic motion. In other words, we may encounter a new form of the attractor, namely, an invariant torus.

The partial differential equation (2.38) is represented in the form of two coupled ordinary differential equations of the second order:

| (2.39) |

Here, we have assumed that the parameters of the accelerator, the rates of accumulation and of import are different for each region of the subdivision.

Previously, for the model of the multiplier-accelerator in one region, we have found periodic regimes with the emergence of corresponding self-oscillations, and we have studied the character of their stability. As it seems, for the model with two regions, cyclic motion is also possible. Moreover, quasi-periodic motion with two matched frequencies is possible as well.

Let us represent the system (2.39) in the traditional form of a system of first-order differential equations. This new system is four-dimensional.

Obviously, the system (2.40) has trivial equilibrium , . The matrix of the linear part of (2.40), corresponding to this singular point, has the form

| (2.41) |

The matrix (2.41) has the characteristic polynomial

| (2.42) |

Equation (2.42) is a fourth-order equation; hence, it has four roots. Of primary interest for us is the situation when (2.42) has two pairs of complex conjugate roots with small parameters in their real parts, i.e.,

| (2.43) |

Under the assumption that , , there exist, for , critical values of the parameters of the accelerator that are responsible for a possible formation of limit cycles.

For , equation (2.42) reduces to to the biquadratic equation

which, for , yields an equation for the frequencies:

| (2.44) |

As the free term in (2.44) is positive, equation (2.44) has two positive roots that determine the squared frequencies:

For definiteness, we assume that . If we compare the values of the so-called eigenfrequencies , , it is not difficult to prove that , whereas . It means that the common frequency of the matched oscillations is either higher than the maximum natural frequency or lower than the minimum natural frequency. On the other hand, in the case of free oscillations, the matched system will never be able to oscillate with an intermediate, compared to natural frequencies, frequency. From an economic point of view, this fact means that a connection between two regions by means of trade relations either speeds up or slows down a cycle of business activity in both the regions.

For further consideration of the properties of the four-dimensional flux that possesses a state of equilibrium with two pairs of purely imaginary eigenvalues, it is necessary to construct the normal form for the system of ordinary differential equations (2.40). This can be done by means of a sequence of linear transformations of the initial variables as follows:

| (2.45) |

The transformation (2.45) converts the system of four ordinary differential equations in real variables into a system of two complex differential equations that takes the following form in terms of the polar coordinates :

| (2.46) |

Here, ; , are small sign-alternating parameters; the coefficients , , are functions of the initial parameters of the system.

We can learn a lot about the dynamics of the system (2.45) from the consideration of a plane vector field obtained by discarding the angular coordinates, following the methods proposed in [42].

In order to reduce the number of parameters, we scale the variables and . Setting and , dropping for notation convenience in what follows the bar over and , and, if necessary, scaling the time variable, we obtain:

| (2.47) |

The system (2.47) is characterized by twelve topologically different situations, presented in the following table:

| Case | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| + | + | + | + | + | + | - | - | - | - | - | - | |

| + | + | + | - | - | - | + | + | + | - | - | - | |

| + | + | - | + | - | - | + | - | - | + | + | - | |

| + | - | + | + | + | - | - | + | - | + | - | - |

This classification is based on an analysis of secondary ”pitchfork” bifurcations from nontrivial states of equilibrium of the plane vector field. Note that the singular point is always a state of equilibrium; besides, up to three states of equilibrium may exist in the positive quadrant:

| (2.48) |

where , .

In general, the behavior of the system remains comparatively simple until the occurrence of secondary Hopf bifurcations from the fixed point . In order to detect such bifurcations, we linearize the dynamic equations in a small neighborhood of this singular point. As a result, we obtain the following matrix:

whose trace is

and the determinant is

Taking into account the conditions of the existence of the singular point (2.48), we infer that the secondary Hopf bifurcation may occur only on the straight line

| (2.49) |

and, at that, .

From this fact, it follows immediately that the secondary bifurcation does not occur in cases 2, 6, 7, 9, 11, 12. It is also possible to show that this bifurcation does not occur in cases 1, 3, 4, 5, because, for its realization, it is important that the angular coefficient of the straight line (2.49) should lie in between the angular coefficients of the straight lines that correspond to the ”pitchforks”, i.e.,

| (2.50) |

which is equivalent to

in a corresponding sector of the plane .

As can be shown by means of simple evaluation, in each case, this requirement does not ensure the condition .

Consider case 8, in which a Hopf bifurcation may occur. Some bifurcation sets and phase portraits for this case are represented in Fig. 2.3.

On the Hopf-bifurcation line (2.49), the system

| (2.51) |

is integrable, whereas the function

| (2.52) |

with , , and , is constant along the solutions. In case 8, we have: , , and ; therefore, level lines of this function have the form shown in Fig. 2.4.

As the system (2.51) is integrable, the secondary Hopf bifurcation is degenerate. Therefore, to study the topology of this bifurcation in full detail, it is necessary to consider in (2.49) terms containing higher powers of the initial variables.