We consider

estimation procedures which are recursive in the sense that each successive

estimator is obtained from the previous one by a simple adjustment.

The model considered in the paper is very general as we do not

impose any preliminary restrictions on the probabilistic nature of

the observation process and cover a wide class of nonlinear

recursive procedures. In this paper we study asymptotic behaviour of the

recursive estimators.

The results of the paper can be used to determine

the form of a recursive procedure which is expected to have the same asymptotic

properties as the corresponding non-recursive one defined as a

solution of the corresponding estimating equation.

Department of Mathematics

Royal Holloway, University of London

Egham, Surrey TW20 0EX

e-mail: t.sharia@rhul.ac.uk

Let be independent identically distributed

(i.i.d.) random variables (r.v.’s) with a common distribution

function

with a real unknown parameter . An

-estimator of is defined as a statistic which is a solution

w.r.t. of the estimating equation

(1.1)

where is a suitably chosen function. For example, if

is a location parameter in the normal family of

distribution functions, the choice gives

the MLE (maximum likelihood estimator).

For the same problem, if the

solution of (1.1) reduces to the median of . In general, if is the probability density

function (or probability function) of (w.r.t. a

-finite measure ) then the choice

yields the MLE.

Suppose now that are not

necessarily independent or identically distributed r.v’s, with a

joint distribution depending on a real parameter . Then an

-estimator of is defined as a solution of the

estimating equation

(1.2)

where with . So, the -functions may now depend

on the past observations as well. For instance, if ’s are

observations from a discrete time Markov process, then one can

assume that . In general, if no restrictions are placed on

the dependence structure of the process , one may need to

consider -functions depending on the vector of all past and

present observations of the process (that is, ). If the

conditional probability density function (or probability function)

of the observation given is

, then one

can obtain the MLE on choosing

Besides MLEs, the class of

-estimators includes estimators

with special properties such as robustness.

Under certain regularity and ergodicity conditions, it can be

proved that there exists a consistent sequence of solutions of

(1.2) which has the property of local asymptotic

linearity. (A comprehensive bibliography can be found in, e.g.,

Hampel at al (1986) and Rieder (1994).)

If -functions are

nonlinear, it is rather difficult to

work with the corresponding estimating equations, especially

if for every sample size

(when new data are acquired),

an estimator has to be computed afresh. In this paper we consider

estimation procedures which are recursive in the sense that each successive

estimator is obtained from the previous one by a simple adjustment.

Note that for a linear estimator,

e.g., for the sample mean, we have

, that is

, indicating that the

estimator at each step can be obtained

recursively using the estimator at the previous step

and the new information . Such an exact

recursive relation may not hold for nonlinear estimators (see,

e.g., the case of the median).

In general, the following heuristic argument can be used to

establish a possible form of an approximate recursive relation

(see also Jurekov and Sen (1996),

Khas’minskii and Nevelson (1972),

Lazrieva and Toronjadze (1987)).

Since is defined

as a root of the estimating equation (1.2), denoting

the left hand side of (1.2) by we have

and . Assuming

that the difference is “small”

we can write

Therefore,

where . Now, depending

on the nature of the underlying model, can be replaced by

a simpler expression. For instance, in i.i.d.

models with (the MLE case), by the strong law of large

numbers,

for large ’s,

where is the one-step Fisher information. So, in

this case, one can use the recursion111This procedure should not be confused with the

Newton-Raphson iterative method. See the corresponding discussion in the Introduction of Sharia (2006a).

(1.3)

to construct an estimator which is “asymptotically equivalent”

to the MLE.

Motivated by the above argument, we consider a class of

estimators

(1.4)

where is a suitably chosen vector process, is

a (possibly random) normalizing matrix process and

is some initial value.

If the

conditional probability density function (or the probability

function) of the observation given

is ,

then one can obtain a ML (maximum likelihood) type recursive

estimator on choosing (the dot denotes the

row-vector of partial derivatives w.r.t. and is the transposition).

Note that

while the main goal is to study recursive procedures with

non-linear functions, it is worth mentioning that any

linear estimator can be written in the form (1.4) with

linear, w.r.t. , functions. Indeed, if

where

and are matrix and vector processes of

suitable dimensions, then (see Section 4.2 for details)

Note also

that in the iid case,

(1.3) can be regarded as a stochastic iterative scheme,

i.e., a classical stochastic approximation procedure, to detect

the root of an unknown function when the latter can only be

observed with random errors (see Remark 3.1 in Sharia (2006a)). A theoretical

implication of this is that by studying the procedures

(1.3), or in general (1.4), we study asymptotic

behaviour of the estimator of the unknown parameter. As far as

applications are concerned, there are several advantages in using

(1.4). Firstly, these procedures are easy to use since each

successive

estimator is obtained from the previous one by a simple adjustment

and without storing all the data unnecessarily. This is

especially convenient when the data come sequentially.

Another potential benefit of using (1.4) is that it allows one to

monitor and detect certain changes in probabilistic characteristics of

the underlying process such as change of the value of the unknown parameter. So, there

may be a benefit in using these procedures in linear cases as well.

In i.i.d. models,

estimating procedures similar to (1.4) have been studied by a number of

authors using methods of stochastic approximation theory (see,

e.g., Khas’minskii and Nevelson (1972), Fabian (1978),

Ljung and Soderstrom (1987), Ljung et al (1992), and references therein). Some work

has been done for non i.i.d. models as well. In particular,

Englund et al (1989) give an asymptotic representation results for

certain type of processes. In Sharia (1998), theoretical

results on convergence, rate of convergence and the asymptotic

representation are given under certain regularity and ergodicity

assumptions on the model, in the one-dimensional case with

(see also Campbell (1982), Sharia (1992),

and Lazrieva et al (1997)).

We study multidimensional estimation procedures of type

(1.4) for the general statistical model. In Sharia (2006a),

imposing “global” restrictions on the processes

and , we study “global” convergence of the recursive

estimators, that is the convergence for an arbitrary starting

value . In Sharia (2006b), we present results on

the rate of the convergence. In this paper we are concerned with

asymptotic behaviour of the estimators defined by (1.4).

Since the model considered is very general, the main objective is

to prove that is locally asymptotically linear,

that is, for each there exist a matrix process

such that

where in

probability (see Section 2 for a more general

definition).

Since is typically a martingale-difference,

asymptotic distribution of an asymptotically linear estimator can be studied

using a suitable form of the central limit theorem for

martingales (see e.g., Feigin (1985), Hutton and Nelson (1986),

Jacod and Shiryayev (1987). Detailed discussion of the literature

on this subject can be found in

Barndorff-Nielsen and Sorensen (1994), Heyde (1997) and Prakasa-Rao (1999)).

For example, results in Shiryayev (1984) (see, e.g., Ch.VII,

8, Theorem 4) show that under certain conditions, local

asymptotic linearity implies asymptotic normality. In the

standard case of i.i.d. observations, assuming that

has zero mean and a finite

second moment and for some

non-random invertible , it follows that

where

In particular, in the case of likelihood recursion with

if is the one-step Fisher information, that is,

it follows that is asymptotically normal with

parameters , i.e.

meaning that is

asymptotically efficient.

In general, in the case of one dimensional parameter , an

estimator is said to be asymptotically efficient if it is

asymptotically linear with

where is the conditional Fisher information. This

kind of efficiency is called asymptotic first order efficiency.

The motivation behind this general definition is the same as in

the classical scheme of i.i.d. observations. For a detailed

discussion of this notion see, e.g.,

Hall and Heyde (1980), Section 6.2. Under relatively mild conditions,

asymptotically efficient estimators are asymptotically equivalent to

the MLE , i.e.

in probability (see, e.g., Hall and Heyde (1980), Section 6.2,

Theorem 6.2.). For the generalisation of these concepts see Heyde

(1997).

It is worth mentioning that the global convergence results for

(1.4) were obtained in Sharia (2006a) under conditions that

allow to belong to quite a wide class of processes

which does not directly depend on the choice of ’s (see Remark

3.1 below). In

order to study the rate of convergence, one has to restrict the

class of allowed ’s (see Sharia (2006b)). It turns out

that when dealing with local asymptotic linearity, one has to

restrict this class even further - to an explicit choice of

, depending on the choice of (see Remark

3.2(iv)–(vii) below). In other words, the results of the paper

tell one how to construct a locally asymptotically linear

procedure (1.4) with given ’s. The fact that one is

restricted to this choice of is probably not very

surprising in retrospective, but this issue does not seem to have

been discussed in the existing literature.

An estimator defined by (1.4) is a recursive analogue of

the corresponding -estimator defined as a solution of the

estimating equation (1.2). It should also be noted that

the recursive procedure (1.4) is not a numerical solution

of (1.2). Nevertheless, under quite mild conditions, the

recursive estimator and the corresponding -estimator are

expected to have the same (or equivalent) asymptotic linearity

expansions. It therefore follows that they are asymptotically

equivalent, in the sense that, depending on the regularity and

ergodicity properties of the underlying model, they both have the

same asymptotic distribution.

The paper is organized as follows. Section 2 introduces the main

objects and definitions. The main results are obtained in Section

3 with various comments and explanations of the conditions used

there. In Section 4 we give examples to illustrate the results of

the paper.

2 Basic model

Let

be observations taking values in a measurable space

equipped with a -finite

measure Suppose that the distribution of the process

depends on an unknown parameter where

is an open subset of the -dimensional Euclidean space

. Suppose also that for each , there

exists a regular conditional probability density of given

values of past observations of , which

will be denoted by

where is the

probability density of the random variable Without loss

of generality we assume that all random variables are defined on a

probability space

and denote by the

family of the corresponding distributions on

Let be the -field

generated by the random variables By

we denote

the -dimensional Euclidean space with the Borel

-algebra . Transposition of

matrices and vectors is denoted by . By we denote the

standard scalar product of that is,

and the corresponding norm is denoted by .

Suppose that is a real valued function defined on

. We denote by the row-vector

of partial derivatives

of with respect to the components of , that

is,

The identity matrix is denoted by .

If for each , the derivative

w.r.t.

exists, then we

can define

and the process

(with the convention ). Let us denote

The one step conditional Fisher information matrix for

is defined as

Note that the process is “predictable”,

that is, the random variable is

measurable for each

Note also that by definition,

is a version of the conditional expectation w.r.t.

that is,

Everywhere in the present work conditional expectations are meant

to be

calculated as integrals w.r.t. the conditional probability densities.

The conditional Fisher information at time is

We say that is a sequence of estimating functions and write

, if for each is a Borel function.

Let and denote We write if

is a martingale-difference process for each

i.e., if for

each (we assume that the conditional expectations

above are well-defined and is the trivial

-algebra).

Note that if differentiation of the equation

is allowed under the integral sign, then .

Suppose that and is

a predictable matrix process (i.e. a matrix with predictable components )

with

We say that an estimator is

locally asymptotically linear if

for each

(2.1)

and in probability where

is a sequence of matrices such that

in probability

and weakly w.r.t.

for some random matrix

That is, is

locally asymptotically linear if

(2.2)

in probability , where

(2.3)

is a linear statistic.

ConventionEverywhere in the present work

is an arbitrary but fixed value

of the parameter. Convergence and all relations between random

variables are meant with probability one w.r.t. the measure

unless specified otherwise. A sequence of random

variables has some property eventually if for

every in a set of probability

1,

has this property for all greater than some

.

3 Main results

Suppose that and

, for each , is a

predictable matrix process with , .

Consider the estimator defined by

(3.1)

where is an arbitrary initial

point.

Let be an arbitrary but fixed value of

the parameter and for any define

Let and for denote

where is defined by (2.3).

Then,

It therefore follows that

satisfies the recursive relation given by

(3.4)

where and . By comparing

equations (3.2) and (3.4), one can obtain the following

result on the asymptotic relationship between and

Lemma 3.1

Suppose that and there exists

a sequence of invertible random matrices such

that in probability and

(E)

weakly w.r.t. where is a random matrix

with -a.s.;

(1)

in probability ;

(2)

in probability , where

Then in

probability (i.e., is locally asymptotically linear).

Proof. To simplify notation we drop the fixed argument or

the index in some of the expressions below. Denote

Subtraction (3.4) from (3.2) yields the recursive relation

(3.5)

Denote and Then the

expression

can easily be obtained

by inspecting the difference between ’th

and ’th term of this sequence (exactly in the same way as in (3)), to check that (3.5) holds.

Now, (1) implies that in

probability . Also, by (2),

in probability . So, using (E), it follows that in probability

.

Next result gives sufficient conditions for (1) and

(2).

Proposition 3.1

(a)

Suppose that in Lemma 3.1 are diagonal matrices with non-decreasing (w.r.t. ) elements and

(L1)

in probability ;

Then (1) holds.

(b)

Suppose that in Lemma 3.1 are diagonal non-random matrices,

and

(L2)

in probability , where is the -th diagonal element of the matrix

and is the -th component of

which is defined in (2).

Then (2) holds.

(c)

Suppose that in Lemma 3.1 are diagonal with non-decreasing elements

and

(LL2)

-a.s., where is the -th component of

which is defined in (2).

Then (2) holds.

Proof. See Appendix A.

Remark 3.1

Before analyzing the above results, let us understand how the procedure works.

Consider the maximum likelihood recursive procedure in the

one-dimensional case

where

and is the conditional Fisher information.

Denote

and rewrite the above recursion as

Then,

where

Under usual regularity conditions (see Sharia (2006a) Remark 3.2 for details),

and

implying that

(3.6)

for small values of . Now, assuming that (3.6) holds for all

suppose that at time

that is,

Then, by (3.6),

So, the next step will be in the direction of

.

If at time

by the same reason,

So, on average, at each step the

procedure moves towards . However, the magnitude of the

jumps should decrease, for

otherwise, may oscillate around without

approaching it. On the other hand,

care should be taken to ensure that the jumps do not decrease too rapidly to avoid

failure of to reach

These issues are addressed in Sharia (2006a) and the conditions are introduced to ensure

global convergence of (3.1), that is, convergence for any arbitrary starting value.

These conditions are flexible enough to allow for a quite wide choice of the normalising

sequence for any particular .

Remark 3.2

(i)

As was mentioned above, strong consistency of the recursive estimator , that is

the convergence

(-a.s.) is established in Sharia (2006a).

Here we are interested in the asymptotic behaviour

of the recursive estimator given that it is consistent. Note

that although consistency is not formally required in Lemma 3.1, it is

easy to see that if is not consistent, conditions (1)

and (2) will be satisfied for very special cases only.

Note also that given that ,

conditions (1) and (2) are local in the sense that they are determined

by local (w.r.t. the parameter) behaviour of the functions involved.

(ii) Condition (E) is an ergodicity

type assumption on the statistical model. If

(the conditional Fisher information) and

and are non-random, then the model is called ergodic.

Further discussion of this concept and related work

appears in Basawa and Scott

(1983), Hall and Heyde (1980) 6.2, and

Barndorff-Nielsen and Sorensen (1994).

(iii) Let us examine condition (2) in Lemma 3.1.

Given that , if

the functions and are continuous w.r.t.

(with certain uniformity w.r.t. ), we expect

Parts (b) and (c) in Proposition 3.1

give sufficient conditions for (2). If there exists a non-random sequence

then obviously (L2) is less restrictive then

(LL2). But unfortunately, (L2) can only be used for non-random

. In the case of random

, when (LL2) may be used, just the convergence

may not be enough since in many models the components

of have the rate .

In such cases one may also use the result on the rate of convergence

of presented in Sharia (2006b) (see examples 4.1 and 4.3 in the next section).

(iv)

Condition (1) gives an important clue for an optimal choice

of the normalizing sequence . To see this, let us assume that

so that and have a look at (1) and (L1) in the case of one dimensional parameter

Now we can write

In most applications,

the rate of is and the best one can hope for is

that is stochastically bounded.

Therefore we must at least have the convergence

. Given that

we expect

for large ’s.

Also, since , if is smooth in ,

we can write that

So, denoting

we expect

(3.7)

where

Using the similar arguments, for the multidimensional case,

we expect (3.7) to hold for large ’s, where is

the total differential of in

Therefore,

(3.8)

is an obvious candidate for the normalizing sequence. If

is differentiable in and differentiation

of

is allowed under the integral sign, then

This implies that,

for a given sequence of estimating functions another possible

choice of the normalizing sequence is

(3.9)

or any sequence with the increments

Also, if the differentiation w.r.t. of

is allowed under the integral sign, then by the product rule,

So,

where, as before,

Therefore, denoting

another possible choice of the normalizing sequence is

(v)

Part (iv) above highlights a very important point. Suppose we wish to construct

a recursive estimator with a given sequence of estimating functions.

In order to achieve consistency, we are quite flexible in choice of the normalizing

sequence ;

the recursive procedure will converge even when sequence is not related to

(see Sharia (2006a)). (Of course, the rate of the normalizing sequence still has to be “right”

but is mostly determined by the model.)

If we want to obtain a recursive estimator which is also

asymptotically linear, then the normalizing sequence has to be

(3.8) (or (3.9), (3.11), or a sequence asymptotically equivalent to

(3.8)).

(vi) Let us consider a likelihood case,

that is

Since the process (3.11) in this case is the conditional Fisher

information So, the corresponding recursive procedure is

(3.12)

Also, given that the model possesses certain ergodicity properties,

asymptotic linearity of (3.12) implies asymptotic

efficiency. In particular, in the case

of i.i.d. observations, it follows that the above recursive procedure is

asymptotically

normal with parameters (see Corollary 4.1 in Section 4).

(vii) Normalizing sequences suggested in (iv)

have been derived from the asymptotic considerations. In practice however, behaviour of

sequence for the first several steps might also be important. This can happen when the number of observations

is small or even moderately large.

According to (iv), to achieve asymptotic linearity, one has to choose a normalizing sequence

with the property that

for large ’s. So, we can consider any sequence of the form , where is one of the sequences introduced

above (by (3.8), (3.9), or (3.11)),

is a sequence of non-negative r.v.’s such that eventually

and is a suitably chosen constant.

In practice, and can be treated as tuning constants

to control behaviour

of the procedure for the first several steps (see Sharia (2006a), Remark 4.4).

Under certain assumptions, at each step, the recursive procedure (3.1),

(on average) moves towards the direction of the unknown parameter (see Remark 3.1 or Sharia (2006a), Remark 3.2

for details).

Nevertheless, if the values of the normalizing sequence are too small for the first several steps, then the

procedure will oscillate excessively around the true value of the parameter. On the other hand, too

large values of the normalizing sequence will result in slower convergence of the procedure. A good

balance can be achieved by using the tuning constants.

The detailed discussion of these and related topics will appear elsewhere, but as a rough guide,

the graph of against should ideally have a shape of

those in Figure 1 in Sharia (2006a) (that is, a reasonable oscillation at the beginning of

the procedure before settling down at a particular level).

4 SPECIAL MODELS

AND EXAMPLES

4.1.The i.i.d. scheme. Consider the

classical scheme of

i.i.d. observations with a common probability

density/mass function Suppose that is an estimating

function with

Let us define the recursive estimator by

(4.1)

where is any initial value.

According to Remark 3.2 (iv) and the condition (V) below,

an optimal choice of would be either

or

or any non-random invertible matrix function that satisfies conditions

listed below.

Suppose that

and consider the following conditions.

(I)

For any

(II)

For each

for some constant

(III)

is continuous in

(IV)

(V)

where as for some .

Corollary 4.1

Suppose that for any conditions (I) - (V) are satisfied. Then the estimator is strongly consistent and -a.s.) for any and

any initial value . Furthermore, is

asymptotically normal with parameters , that is,

In particular, in the case of the maximum likelihood type recursive procedure

with and

, the estimator is asymptotically efficient (i.e., asymptotically

normal with parameters ).

Proof See Appendix A.

Similar results (for i.i.d. schemes) were obtained

by Khas’minskii and Nevelson (1972) (when and

,

Ch.8, 4) and Fabian (1978).

4.2.Linear procedures. Consider the

recursive procedure

(4.2)

where the and are predictable matrix processes,

is an adapted process (i.e., is

-measurable for )

and all three are independent of

The following result gives a sets of sufficient

conditions for the asymptotic linearity of the estimator defined by (4.2)

in the case when

the linear is a

martingale-difference, i.e.,

for

Corollary 4.2

Suppose that and

(4.3)

in probability , where

Then the recursive estimator defined by (4.2) is asymptotically

linear with

(4.4)

where in probability

Proof

Let us check the conditions of Lemma 3.1 for

Condition (E) trivially holds. Then, since and

we have

Therefore, (1) is equivalent to (4.3).

Then, it is easy to see that for defined in (2) we have

implying that (2) holds which completes the proof.

Remark 4.1

Condition (4.3) trivially holds if

that is

In this case, the solution of (4.2) is

(4.5)

This can be easily seen by inspecting the difference

for the sequence (4.5) (exactly in the same way as

in (3)), to

check that (4.2) holds. Also, since (4.5) can obviously be rewritten as

it follows that in this case,

is indeed

an obvious necessary and sufficient condition for to be

asymptotically linear (for arbitrary starting value ).

4.3.Exponential family of Markov

processes Consider a conditional exponential family of Markov

processes in the sense of Feigin (1981) (see also Barndorf-Nielson

(1988)). This is a time homogeneous Markov chain

with the one-step transition density

where is a -dimensional vector and

is one dimensional. Then in our notation

and

It follows from standard

exponential family theory (see, e.g., Feigin (1981)) that

is a martingale-difference and

the conditional Fisher information

is

A maximum likelihood type recursive procedure can be defined as

Now suppose that is one dimensional and the process belongs to the

conditionally additive exponential family, that is,

with

(4.6)

where and

(see Feigin (1981)).

Then,

Assuming that

the likelihood recursive procedure is

(4.7)

Remark 4.2

Consistency and rate of convergence of the estimator derived by (4.7) is

studied In Sharia (2006b).

To ensure that (4.7) has the same asymptotic properties as the maximum likelihood

estimator, one has to impose certain restrictions on the and .

In Corollary A1 in Appendix A, the conditions of Section 3 written in terms of this model

are presented. These conditions will be satisfied if there is a certain balance between requirements of

smoothness on , the rate at which , and ergodicity

of the model. For instance, suppose that the model is ergodic, that is, there exists a non-random sequence

such that weakly. Then

will hold if the process

converges to zero (criterion based on the Lenglart-Rebolledo inequality, see (L2) and formula (A5) in Appendix

A). So, assuming that

the estimator is consistent (that is ), by the Toeplits lemma, the above will be guaranteed

by the continuity of . On the other hand, if

the model is non-ergodic, then one may need to impose smoothness of higher order on

function (see condition (iii) below) and restrictions on the growth

of the sequence (see condition (i) below). The following result gives one possible

set of sufficient conditions for the recursive estimator to be consistent and to have the same

asymptotic properties as the maximum likelihood estimator.

Proposition 4.3Suppose that and

(i)

(ii)

there exists a constant such that

for each .

(iii)

The function is locally

Lipschitz , that is, for any there exists

a constant and such that

for small ’s.

Then

defined by (4.7) is strongly consistent (i.e.,

-a.s.) for any initial

value . Furthermore, -a.s. for any ,

and is asymptotically linear with

(4.8)

where in probability

4.4.AR(m) process

Consider an AR(m) process

where

and

is a sequence of i.i.d. random variables.

In Sharia (2006a) we discuss convergence of the recursive estimators of the form

(4.9)

where and () are

respectively suitably chosen vector and matrix processes.

If the probability density function of w.r.t. Lebesgue’s measure is

then the conditional probability density function of given

values of past observations of is

obviously

and so,

It follows from the results of Section 3 (see Remark 3.2 (vi)) that an optimal

choice of the normalizing sequence is the conditional Fisher information ,

(or any sequence with the increments equal to ).

It is easy to see that in this case,

where

Since in this case the conditional Fisher information can also be found recursively,

a likelihood recursive procedure is

(4.10)

for and an arbitrary starting point .

The strong consistency of the estimators (4.9) and, in particular,

that of (4.10) is studied in Sharia (2006a).

The class of estimators (4.9) includes

recursive versions of robust modifications of the

least squares method. These are recursive estimators defined by

(4.11)

where

is a bounded scalar function and is a vector

function of the form for some non-negative function

of

Since (4.11) is of the form (3.1) with

assuming that is differentiable (almost everywhere w.r.t. Lebesgue’s measure)

we obtain

So, according to Lemma 3.1 (see Remark 3.2 (iv) formula (3.9)),

an optimal normalizing sequence for (4.11)

is

(4.12)

where

or a sequence with the increments equal to

Consider for instance a recursive M-estimator

of the parameter of an AR(1) process defined as

(4.13)

where and are scale estimates and is the Huber function,

and is a tuning constant. This is a

recursive version of a robust generalized M-estimator

of the parameter of an AR(1) process proposed by see Denby and Martin (1979).

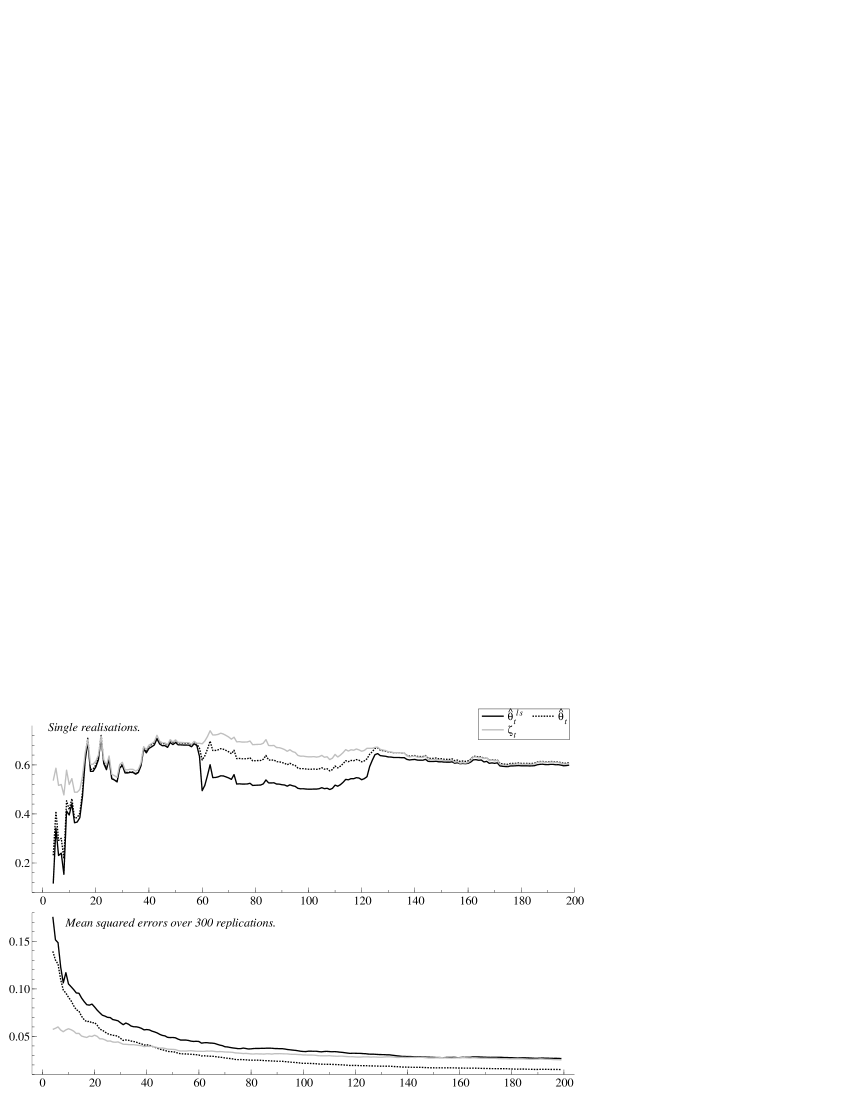

Below we present a brief simulation study.

The time series were generated from the additive effect outliers

(AO) model:

where innovations are i.i.d. Gaussian The

variables are also i.i.d. with distribution where is the distribution

that assigns probability to the origin. Therefore, with

probability the process is observed, and

with probability the observation is the process

plus the error with Gaussian distribution . In

this simulation, , and . The

figures below show the performances of the estimator

defined by (4.13), the estimator

defined by (4.14) and the least squares estimator

(which is equivalent to the recursive

procedure defined by (4.10) with ). The

estimators are computed for the series of length , with the

additional observations

at the beginning on which initial estimates are based; as an

estimates for and we take the median of the absolute

values of the data and residuals respectively, divided by

0.6745. The p.d.f. in (4.13) and (4.14)

is replaced by the p.d.f. of

and the values of the tuning constants are

and .

Figure 1 shows single realizations and the mean squared errors over 300 replications

of the estimators

and for .

Figure 1: Single realizations and the mean squared errors over 300 replications,

for .

Further simulation study is required to study performances of

these procedures. As this brief simulation suggests, both

and outperform

5 Concluding remarks

This is a final part of a series of three papers (see Sharia (2006a) and Sharia (2006b)).

We have introduced

estimation procedures (3.1) which are recursive in the sense that each successive

estimator is obtained from the previous one by a simple adjustment.

To guarantee the convergence one has to impose global restrictions

on the functions in (3.1) (w.r.t. the parameter )

such as a monotonicity type assumption and a restriction on the

growth at infinity (see Sharia (2006a)). This is the price one has to pay for the nice

recursive structure. Once the convergence is ensured, the rate of convergence

(see Sharia (2006b)) and asymptotic

linearity can be deduced from local (in ) conditions.

Also, results presented

give an explicit way of constructing a normalising sequence to ensure

local asymptotic linearity. The

rest relies on the ergodicity of the model. Asymptotic properties

such as asymptotic distribution and efficiency of recursive (as

well as non-recursive) estimators depend on limit theorems

possessed by the model. For example, in the i.i.d. case (see

Corollary 4.1), the central limit theorem and the law of large

numbers imply

that the corresponding recursive procedures are asymptotically

normal and, in addition, the likelihood procedure is

asymptotically efficient. In general, one can obtain asymptotic

distribution and efficiency from asymptotic linearity (Lemma

3.1) and an appropriate central limit theorem.

The model considered in the paper is very general as we do not

impose any preliminary restrictions on probabilistic nature of

the observation process and cover a wide class of nonlinear

recursive procedures for estimation of a multidimensional parameter.

The results are new even for the case of a scalar parameter and provide

a new insight even for the case of i.i.d. observations.

While the advantage of this approach is its

universality, verification of the conditions may be a nontrivial

matter in some models. Examples considered give a flavour of what

is usually involved in this process and show where our

restrictions come from. It is worth mentioning,

that even in the cases where one has difficulties with verifying

our conditions, the results of the paper can be used to determine

the form of a recursive procedure (in fact, an algorithm, see

Remark 3.2 (iv)–(vi)), which is expected to have the same asymptotic

properties as the corresponding non-recursive one defined as a

solution of the equation (1.2).

APPENDIX A

Proof of Proposition 3.1

To simplify notation we drop the fixed argument or the index

in some of the expressions below.

To prove (a),

denote

and

Applying the formula (summation by parts)

with

and

we obtain

Then,

where the last equality follows since is diagonal.

Therefore,

Finally, since ’s are diagonal with non-decreasing elements,

applying the Toeplits Lemma to the components of the right hand side of latter formula we obtain that

To prove (b) and (c)

denote

Since it follows from that is a martingale.

Denote by the -th component of

Then the square characteristic of

the martingale is

and, by (LL2),

It therefore follows that

-a.s. (see e.g., Shiryayev (1984), Ch.VII, §5, Theorem 4).

This proves (c). Now, use of the

Lenglart-Rebolledo inequality (see, e.g., Liptser and Shiryayev

(1989), Ch.1, 9) yields

for each and

Then, by (L2),

in probability .

This implies that

in probability and so,

since is diagonal, (2) follows.

Proof of Corollary 4.1 Using Corollary 4.1 in Sharia (2006a)

it follows that (I) and

(II) imply .

We have and It is easy to see that

(II) implies (B2) from Corollary 4.1 in Sharia (2006b), and

(V) implies that

(B1) of the same Corollary holds with So, for any

Let us check that conditions of Lemma 3.1 are also satisfied

with Condition (EE) trivially holds.

According to Proposition 3.1, condition (1) follows from

(L1). To check (L1), it

is sufficient to show that

where

By (V),

and

where, by (III) and (V),

. Then,

which, by (A1) (since ) converges to zero. Therefore,

(A2) is now a consequence of the Toeplits Lemma.

For the process from (L2) (since

), we have

From (III) and (V) we obtain that and

as . So, using (IV), it is easy to see that Since

(L2) follows from the Toeplitz lemma.

Therefore, the conditions of Lemma 3.1 hold for

This implies that

in probability where

The asymptotic normality now obviously follows

from the central limit theorem for i.i.d. random variables.

Corollary A1Suppose that and is derived by

(4.7). Denote ,

, and

suppose also that

(I)

where

(II)

one of the following two conditions are satisfied;

OR

where

and is a predictable process with

Then (4.8) holds, i.e., the estimator is asymptotically linear.

Proof.

Let us check the conditions of Lemma 3.1 for

and

Since

is a martingale-difference, we have

and so

and

where

Then, since we have

Now, since

it is easy to see that the first condition in (II) implies (1) in Lemma 3.1 and

the second condition in (II) implies (L1) in Proposition 3.1. Therefore, (1) holds.

To verify (2), consider the process defined in

(2). Using (A3) and (A4), it is easy to see that

This shows that (I) implies (2).

Proof of Proposition 4.3

Since, by (iii), is obviously a continuous function,

condition (M2) of Proposition 4.1 in Sharia (2006b) holds. Also, (M1) in the same proposition

obviously follows from (i). So, it follows that all the conditions

of Proposition 4.1 and Corollary 4.2 in Sharia (2006b) are satisfied implying that

-a.s.). Also, by (i),

implying that

So,

To establish asymptotic linearity, let us verify the conditions of Corollary A1 is satisfied.

Since -a.s.) and

, by (iii) we obtain that

eventually.

So,

eventually.

Now,

by (A6) since

So, since we obtain that

Therefore, by the Toeplits Lemma, the second condition of (II) holds.

Now, since is a martingale-difference,

to verify (I), it is sufficient to show that (see e.g., Shiryayev (1984), Ch.VII, §5, Theorem 4)

Since

the above series can be rewritten as

where, by (iii),

Now, using (A6) and continuity of we deduce that

Also,

(see Sharia (2006b),

Appendix A, Proposition A2),

implying that the above series converge which completes the proof.

REFERENCES

Barndorff-Nielsen, O.E. and Sorensen, M. (1994).

A review of some aspects of asymptotic likelihood theory for

stochastic processes. International Statistical Review.62, 1, 133-165.

Basawa, I.V. and Scott, D.J. (1983).

Asymptotic Optimal Inference for Non-ergodic Models.

Springer-Verlag, New York.

Campbell, K.(1982). Recursive computation of

M-estimates for the parameters of a finite autoregressive

process, Ann. Statist., 10, 442-453.

Englund, J.-E., Holst, U., and Ruppert, D.(1989).

Recursive estimators for

stationary, strong mixing processes – a representation

theorem and asymptotic distributions,

Stochastic Processes Appl., 31, 203–222.

Fabian, V. (1978). On asymptotically efficient

recursive estimation.

Ann. Statist.6, 854-867.

Feigin, P.D. (1985). Stable convergence for semimartingales. Stoch. Proc. Appl.19, 125–134.

Hall, P. and Heyde, C.C. (1980). Martingale Limit Theory and Its

Application. Academic Press, New York.

Hampel, F.R., Ronchetti, E.M., Rousseeuw,

P.J., and Stahel, W. (1986).

Robust Statistics - The Approach Based on Influence

Functions, Wiley, New York.

Heyde, C.C. (1997). Quasi-Likelihood and Its Application: A General Approach to

Optimal Parameter estimation. Springer-Verlag, New York.

Hutton, J.E. and Nelson, P.I. (1986). Quasi-likelihood estimation

for semimartingales. Stoch. Proc. Appl.22, 245–257.

Jacod, J. and Shiryayev, A.N. (1987). Limit Theorems

for Stochastic Processes. Heidelberg, Springer.

Jurekov, J. and

Sen, P.K. (1996). Robust Statistical Procedures -

Asymptotics and Interrelations, Wiley, New York.

Khas’minskii, R.Z. and Nevelson, M.B. (1972).

Stochastic Approximation and

Recursive Estimation. Nauka, Moscow.

Lazrieva, N., Sharia, T. and Toronjadze, T.(1997).

The Robbins-Monro type

stochastic differential equations. I. Convergence of solutions,

Stochastics and Stochastic Reports,61, 67–87.

Lazrieva, N., Sharia, T. and Toronjadze, T.(2003).

The Robbins-Monro type

stochastic differential equations. II. Asymptotic behaviour of solutions,

Stochastics and Stochastic Reports,75, 153–180.

Lazrieva, N. and Toronjadze, T. (1987). Ito-Ventzel’s formula for

semimartingales, asymptotic properties of MLE and recursive

estimation, Lect. Notes in Control and Inform. Sciences, 96, Stochast.

diff. systems, H.J, Engelbert, W. Schmidt (Eds.), (pp. 346–355). Springer.

Ljung, L. Pflug, G. and Walk, H. (1992).

Stochastic Approximation and

Optimization of Random Systems, Birkhäuser, Basel.

Ljung, L. and Soderstrom, T. (1987). Theory and

Practice of Recursive Identification, MIT Press.

Prakasa Rao, B.L.S. (1999). Semimartingales and their Statistical Inference.

Chapman Hall, New York.

Rieder, H. (1994). Robust Asymptotic Statistics,

Springer–Verlag, New York.

Sharia, T. (1998). On the recursive parameter estimation for the

general discrete time statistical model. Stochastic Processes Appl.73, 2, 151–172.

Sharia, T. (2006a). Recursive parameter estimation: Convergence.

Statistical Inference for Stochastic Processes (in press).

(see also http://personal.rhul.ac.uk/UkAH/113/ConvA.pdf).

Sharia, T. (2006b).

Rate of convergence in recursive parameter estimation procedures (submitted).

(http://personal.rhul.ac.uk/UkAH/113/GmjA.pdf).

Shiryayev, A.N. (1984). Probability.

Springer-Verlag, New York.