Universality results for largest eigenvalues of some sample covariance matrix ensembles

Abstract

For sample covariance matrices with iid entries with sub-Gaussian tails, when both the number of samples and the number of variables become large and the ratio approaches to one, it is a well-known result of A. Soshnikov that the limiting distribution of the largest eigenvalue is same as the of Gaussian samples. In this paper, we extend this result to two cases. The first case is when the ratio approaches to an arbitrary finite value. The second case is when the ratio becomes infinity or arbitrarily small.

1 Introduction

The scope of this paper is to study the limiting behavior of the largest eigenvalues of real and complex sample covariance matrices with independent identically distributed (i.i.d.), but non necessarily Gaussian, entries. Consider a sample of size of i.i.d. random vectors . We further assume that the sample vectors have mean zero and covariance . We use to denote the data matrix and to denote the sample covariance matrix. Random sample covariance matrices have been first studied in mathematical statistics ([4], [13], [11]). A huge literature deals with the case where , being fixed, which is now quite well understood. Contrary to the traditional assumptions, it is now of current interest to study the case where is of the same order as , due to the large amount of data available. In particular, the limiting behavior of the largest eigenvalues is important for testing hypotheses on the covariance matrix Here we focus on the simple case, versus and study the asymptotic distribution of extreme eigenvalues under the . The study of extreme eigenvalues is also of interest in principal component analysis. We refer the reader to [15] and [7] for a review of statistical applications. Other examples of applications include genetics [21], mathematical finance [24], [18], [19], wireless communication [34], physics of mixture [25], and statistical learning [12]. We point out that the spectral properties of readily translate to the companion matrix Indeed, is a matrix, of rank , with the same non-zero eigenvalues as Thus, it is enough to study the spectral properties of to give a complete picture of the spectrum of such sample covariance matrices.

1.1 Model and results

We consider both real and complex random sample covariance matrices

where is a , random matrix satisfying certain “moment conditions”. In the whole paper, we set

We assume that the entries of the sequence of random matrices are non-necessarily Gaussian random variables satisfying the following conditions. First, in the complex case,

(i) are real independent random

variables,

(ii) all these real variables have symmetric laws (thus,

for all ),

(iii) ,

(iv) all their other moments are assumed to be sub-Gaussian i.e. there exists a

constant such that uniformly in and ,

In the real setting, is a random matrix

such that

(i’) the are independent random variables,

(ii’) the laws of the are symmetric (in particular,

),

(iii’) for all , ,

(iv’) all the other moments of the grow not faster than the Gaussian ones. This

means that there is a constant such that, uniformly in

and , .

When the

entries of are further assumed to be Gaussian, we will denote by the

corresponding model. In this case and in the complex setting, is of the

so-called Laguerre Unitary Ensemble (LUE), which is also called the complex Wishart ensemble. In the real setting, is of the so-called Laguerre Orthogonal Ensemble (LOE) or real Wishart ensemble.

The scope of this paper is to describe the large--limiting distribution of the largest eigenvalues induced by any such ensemble, for any fixed integer independent of Two regimes are investigated in this paper. In the first part, we assume that there exists some constant such that

In the second part, we consider the case where as

Before stating our results, we recall some known results about sample covariance matrices. We first focus on the case where

Let be the ordered eigenvalues induced

by any ensemble of the above type. The first fundamental result for the limiting spectral behavior

of such random matrix ensembles has been obtained by Marchenko and Pastur in [20] (in a much more general context than here).

It is in particular proved therein that the spectral measure a.s. converges as goes to infinity. Set Then one has that

| (1) |

The limiting probability distribution is the so-called Marchenko-Pastur distribution.

The above result gives no insight

about the behavior of the largest eigenvalues. The first study of the asymptotic behavior of the

largest eigenvalue goes back to S. Geman [10]. It was later refined in [2] and

[26]. In particular, it is well known that

a.s. if the entries of the random matrix admit moments up to order .

Significant results about fluctuations of the largest eigenvalues around are much more

recent and are essentially established for Wishart ensembles only. In particular, the limiting distribution of the largest eigenvalue has been obtained by K. Johansson [14] for complex Wishart matrices and I. Johnstone [15] for real Wishart matrices. A. Soshnikov [30] has derived for both ensembles the limiting distribution of the largest eigenvalues, for any fixed integer .

Before recalling their results, we need a few definitions.

We denote by the

eigenvalues induced by the Wishart ensembles, with (resp. ) for the LUE (resp.

the LOE). We also define the limiting Tracy-Widom distribution for the largest eigenvalue.

Let denote the standard Airy function and denote the solution of the Painlevé II differential equation with boundary condition

Definition 1.1.

The GUE (resp. GOE) Tracy-Widom distribution for the largest eigenvalue is defined by the cumulative distribution function (resp.

The GUE (resp. GOE) Tracy-Widom distribution for the joint distribution of the largest eigenvalues (for any fixed integer ) has been similarly defined. We refer the reader to [35] and [36] for a precise definition.

We then rescale the eigenvalues as follows: for we set

| (2) |

Theorem 1.1.

The proof of Theorem 1.1 relies on the crucial fact that the joint eigenvalue density of the

Wishart ensembles can be exactly computed.

Starting from numerical simulations, it was then conjectured, in [15] e.g., that

Theorem 1.1 actually holds for a class of random sample covariance matrices much wider than the Wishart ensembles.

Such a universality result was later proved for some quite general ensembles by A. Soshnikov [30], yet

under some restriction on the sample size, as we now recall.

For any ensemble satisfying to (resp. to ), we set:

| (3) |

Theorem 1.2.

[30] Assume that . The joint distribution of the rescaled largest eigenvalues , induced by any ensemble satisfying to (resp. to ) converges, as goes to infinity, to the joint distribution defined by the GUE (resp. GOE) Tracy-Widom law.

In this paper, we prove that such a universality result holds for any value of the parameter This is the main result of this note.

Theorem 1.3.

The joint distribution of the rescaled largest eigenvalues , induced by any ensemble satisfying to (resp. to ) converges, as goes to infinity, to the joint distribution defined by the GUE (resp. GOE) Tracy-Widom law. The results holds for any value of the parameter

Remark 1.1.

Assumptions and can actually be relaxed. This relaxation is discussed in the second paragraph of Subsection 1.2.

Before giving secondary results, we give a few comments on the way we proceed to prove Theorem 1.3. In Theorem 1.2, the reason for the restriction on follows from the idea of the proof used therein. Basically,

when , the eigenvalues of a random sample covariance matrix roughly behave as the squares of those of a typical Wigner random matrix. This adequacy still works for the largest eigenvalues,

but fails if is not close enough to one. Theorem 1.2 has been proved using universality

results established for classical Wigner random matrices.

Here, we revisit the problem of computing the asymptotics of for some powers that may go to infinity, using combinatorial tools specifically well suited for the study of spectral functions of sample covariance matrices. It is well known that Dyck paths and Catalan numbers are associated to standard Wigner matrices (see [1]). Suitable combinatorial tools in the case of sample covariance matrices are the so-called Narayana numbers and some particular Dyck paths. Using those, we can extend the universality result of [30] to any value of the ratio

The case where can also be considered thanks to the companion matrix .

Let be the eigenvalues of , ordered in decreasing order and let so that as We set:

Corollary 1.1.

Under the assumptions to (resp. to ), the joint distribution of converges as to the GUE (resp. GOE) Tracy-Widom joint distribution of the largest eigenvalues.

The machinery we develop to prove Theorem 1.3 can also be used to consider the case where the size of the sample data increases in such a way that go to infinity and . The large--limiting behavior of extreme eigenvalues of Wishart matrices for such a regime has been obtained by N. El Karoui [6]. The particular interest of such a study for statistical applications (e.g. microarrays) is also explained in great detail therein.

Under the same assumptions to (resp. to ), we prove that universality still holds in the regime

Theorem 1.5.

Theorem 1.3 also holds if .

1.2 Statistical implications of the result

Testing homogeneity of a population has long been of interest in mathematical statistics, and it is often a preliminary step in discriminant analysis and cluster analysis. Assuming high dimensionality, we consider the test of the null hypothesis vs. the alternative hypothesis The result stated here for the largest eigenvalue can be formulated as

| (4) |

The above theoretical result was essentially established for Gaussian samples only so far (cf. [16] for a review). Removing the Gaussianity assumption is actually fundamental for various statistical problems. Our result may be of use for instance in genetics (see [21] e.g.). Samples in genetic data are usually drawn from a distribution with compact support and the size of matrices encountered therein is typically large enough so that (4) should be observed for some appropriate models. Some Gaussian (or other kinds) mixtures also fall into the class of distributions studied here. Such distributions occur for instance in finance in modeling some fat-tailed returns.

Regarding especially the assumptions we make on the distribution of the entries, they may appear strong for other statistical purposes. The moment assumptions and can actually be relaxed, using truncation techniques. We can show that Theorem 1.3 holds under the assumption that

for some (see Remarks 2.3 and 2.5).

We do not consider this case here, which would increase the technicalities of the paper. To illustrate this, a simulation is given below where the entries of have a Student’s distribution with degrees of freedom. These distributions may be interesting in statistical models due to their (relative) robustness with respect to outliers.

The symmetry assumption is probably more problematic and is again a technical assumption for the proof.

Indeed, it is expected that the lack of symmetry has no impact on the limiting distribution of largest eigenvalues (provided the distribution is centered). Yet, analytical tools to prove such a result are not established (see e.g. [22] for recent progress).

The method we develop is also a first step towards considering samples with non-Identity covariance. Such results are of practical importance for understanding the behavior of Principal Component Analysis and dimension reduction in high dimensional setting. It is therefore important to consider covariance matrices with more complex structure. In particular (in progress), the moment approach developed here seems to be well suited in the case where the population covariance is a so-called “spiked” diagonal matrix. That is, , where the deformation is a finite rank diagonal matrix. This is important, since the test based on (4) may not reject if the largest eigenvalue of is not large enough, because of a phase transition phenomenon described e.g. in [3].

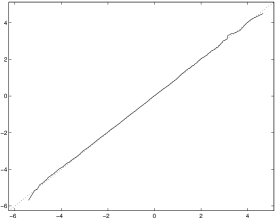

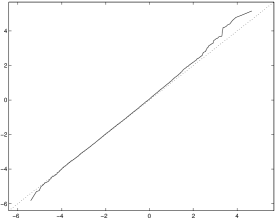

A few simulations have been done to give, from a practical point of view, an idea of the rate of convergence of the distribution of the largest eigenvalue. We have generated real random matrices with i.i.d. entries with a distribution or a Gaussian mixture distribution. To fit the limiting Tracy-Widom distribution, we have rescaled the largest eigenvalue as follows:

| (5) |

for some adjustment parameters and . We indeed have some freedom in the choice of these parameters, which can be any fixed real numbers. In the real Wishart case, the best parameters are known to be Determining the optimal parameters is important to improve convergence rates for (4). They have been established in [8] for complex Gaussian samples. Providing a general formula for these parameters is an issue that we cannot handle so far. Nevertheless, in view of our simulations, the optimal parameters may depend on the distribution of the entries and maybe also on the dimensions and For instance, for the Gaussian mixture distribution, we found empirically that the best parameters are (choosing gives results which are similar but not so satisfying). We also tested various distributions. For the distribution with (resp. ) degrees of freedom, we found that (resp. ) were the optimal parameters.

Such a change can be understood, as the similarity between the distribution and the Gaussian distribution increases with the number of degrees of freedom.

For the simulations given below, we have considered two distributions:

- the Gaussian mixture

- the Student’s distribution with degrees of freedom.

We also considered various dimensions , , and , as well as different sample size to dimension ratios, and .

For each size and each distribution, we have generated random matrices with i.i.d. entries. For each replication, we have rescaled the largest eigenvalue of as in (5) with (resp. ) for the Student’s (resp. Gaussian mixture) distribution.

We then derived the estimated cumulative probabilities for obtained from the replications.

For small sizes, and e.g, the proximity between the observed cumulative distribution of the rescaled largest eigenvalue and the Tracy-Widom distribution is reasonable essentially for upper quantiles for the distribution(95 ). For the Gaussian mixture, it is reasonable for smaller quantiles.

As the size of the matrix increases, the proximity becomes acceptable for almost the whole range. We also note that the convergence is almost as good as for the Wishart ensemble (compare with Table 1 in [15]) in both cases.

| . | |||||||

|---|---|---|---|---|---|---|---|

| -3.896 | .01 | .0079 | .0103 | .0097 | .0107 | .0114 | .0092 |

| -3.516 | .025 | .0256 | .0246 | .0270 | .0257 | .0267 | .0236 |

| -3.180 | .05 | .0554 | .0487 | .0512 | .0568 | .0516 | .0489 |

| -2.782 | .10 | .1172 | .0973 | .0971 | .1099 | .1004 | .0994 |

| -2.088 | .25 | .2912 | .2502 | .2478 | .2724 | .2453 | .2436 |

| -1.269 | .50 | .5354 | .4935 | .4894 | .5154 | .4960 | .4922 |

| -0.392 | .75 | .7550 | .7401 | .7336 | .7465 | .7440 | .7389 |

| 0.450 | .90 | .8951 | .8897 | .8879 | .8870 | .8892 | .8894 |

| 0.979 | .95 | .9417 | .9396 | .9436 | .9368 | .9422 | .9425 |

| 1.454 | .975 | .9676 | .9662 | .9718 | .9644 | .9718 | .9691 |

| 2.024 | .99 | .9855 | .9857 | .9875 | .9824 | .9875 | .9858 |

The first column shows the percentiles of the Tracy-Widom distribution corresponding to the values in the second column. The next columns give the estimated cumulative probabilities for obtained from replications. The entries of the random matrices are i.i.d. with the Gaussian mixture distribution and . The Matlab functions normrnd and unifrnd were used to generate the Gaussian mixtures. The Tracy-Widom quantiles were computed thanks to the p2Num package, provided by C. Tracy.

| . | |||||||

|---|---|---|---|---|---|---|---|

| -3.896 | .01 | .0024 | .0047 | .0069 | .0041 | .0052 | .0078 |

| -3.516 | .025 | .0097 | .0144 | .0188 | .0129 | .0162 | .0220 |

| -3.180 | .05 | .0262 | .0346 | .0392 | .0336 | .0350 | .0469 |

| -2.782 | .10 | .0674 | .0838 | .0857 | .0755 | .0842 | .0924 |

| -2.088 | .25 | .2203 | .2266 | .2375 | .2220 | .2317 | .2399 |

| -1.269 | .50 | .4863 | .4784 | .4950 | .4835 | .4890 | .4922 |

| -0.392 | .75 | .7457 | .7421 | .7487 | .7415 | .7433 | .7493 |

| 0.450 | .90 | .8908 | .8950 | .9028 | .8951 | .8888 | .9003 |

| 0.979 | .95 | .9440 | .9463 | .9501 | .9490 | .9421 | .9507 |

| 1.454 | .975 | .9694 | .9730 | .9730 | .9727 | .9697 | .9735 |

| 2.024 | .99 | .9872 | .9887 | .9896 | .9878 | .9880 | .9895 |

The entries of the random matrices are i.i.d. with a distribution with degrees of freedom and . We have used the Matlab function trnd to generate the Student random variables.

|

|

| . | |||||||

|---|---|---|---|---|---|---|---|

| -3.896 | .01 | .0147 | .0114 | .0099 | .0180 | .0159 | .0113 |

| -3.516 | .025 | .0342 | .0276 | .0248 | .0377 | .0322 | .0260 |

| -3.180 | .05 | .0615 | .0553 | .0488 | .0643 | .0590 | .0501 |

| -2.782 | .10 | .1156 | .1051 | .1009 | .1148 | .1069 | .0977 |

| -2.088 | .25 | .2706 | .2473 | .2418 | .2663 | .2552 | .2420 |

| -1.269 | .50 | .5024 | .4906 | .4839 | .5049 | .4971 | .4792 |

| -0.392 | .75 | .7432 | .7375 | .7354 | .7450 | .7411 | .7284 |

| 0.450 | .90 | .8899 | .8887 | .8906 | .8882 | .8884 | .8893 |

| 0.979 | .95 | .9435 | .9434 | .9448 | .9393 | .9432 | .9425 |

| 1.454 | .975 | .9694 | .9716 | .9706 | .9698 | .9698 | .9712 |

| 2.024 | .99 | .9867 | .9876 | .9875 | .9875 | .9878 | .9883 |

The entries are i.i.d. with a Gaussian mixture distribution and .

| . | |||||||

|---|---|---|---|---|---|---|---|

| -3.896 | .01 | .0094 | .0093 | .0096 | .0100 | .0099 | .0096 |

| -3.516 | .025 | .0224 | .0246 | .0221 | .0252 | .0221 | .0229 |

| -3.180 | .05 | .0470 | .0467 | .0479 | .0503 | .0466 | .0468 |

| -2.782 | .10 | .1006 | .0898 | .0961 | .0965 | .0936 | .0962 |

| -2.088 | .25 | .2415 | .2356 | .2422 | .2466 | .2412 | .2419 |

| -1.269 | .50 | .4938 | .4819 | .4901 | .4882 | .4893 | .4883 |

| -0.392 | .75 | .7418 | .7409 | .7456 | .7418 | .7400 | .7452 |

| 0.450 | .90 | .8970 | .8928 | .8984 | .8953 | .8917 | .8979 |

| 0.979 | .95 | .9468 | .9462 | .9469 | .9495 | .9480 | .9466 |

| 1.454 | .975 | .9717 | .9747 | .9727 | .9743 | .9733 | .9715 |

| 2.024 | .99 | .9889 | .9889 | .9885 | .9895 | .9902 | .9887 |

The entries are i.i.d. with a distribution and .

1.3 Sketch of the proof

We here give the main ideas of the proof of both Theorems 1.3 and 1.5. The proof follows essentially the strategy introduced in [30] and we refer to this paper for most of the detail. We focus on the case where Basically we compute the leading term in the asymptotic expansion of expectations of traces of high powers of :

| (6) |

Here is a sequence such that there exists some constant with It is indeed expected that the largest eigenvalues exhibit fluctuations in the scale around The core of the proof is to show that for large powers , for any integer and any real numbers chosen in a compact interval of , there exists such that and

| (7) |

Formula (7) claims universality of moments of traces of powers of in the scale . Using the machinery developed in [29] (Sections 2 and 5) and [30] (Section 2), we can then deduce that the limiting joint distribution of any fixed number of largest eigenvalues for sample covariance matrices of type to (resp. to ()) is the same as for complex (resp. real) Wishart ensembles. Here we roughly give the main idea. On one hand, the Laplace transform of the joint distribution of a finite number of the rescaled eigenvalues can be conveniently expressed in terms of joint moments of traces as in (6). On the other hand, the asymptotic distribution of these rescaled largest eigenvalues (and also the corresponding Laplace transform) is well-known in the Wishart setting. One can then deduce from universality of moments of traces that the asymptotic joint distribution of the largest eigenvalues for any ensemble considered here is the same as for the corresponding Wishart ensemble. The detail of the derivation of such a result from formula (7), including the required asymptotics of correlation functions for Wishart ensembles, can be found in [29], [30] and [6]. The improvement we obtain with respect to [30] is actually that Formula (7) holds for any value . Our result is due to a refinement in the counting procedure of [30].

The paper is organized as follows. In Section 2, we introduce the so-called Narayana numbers. These numbers are the major combinatorial tools needed to adapt the computations of [30] to sample covariance matrices of any sample size to dimension ratio We also establish a central limit theorem for traces of high powers of . Section 3 is simply a mimicking of the computations made in [30] and essentially yields formula (7). Finally, in Section 4, we consider the case where , which requires some minor modifications.

Acknowledgments

I thank C. Tracy for the Mathematica code of the Tracy-Widom distribution, A. Soshnikov, D. Paul, N. Patterson, R. Cont, L. Choup and C. Semadeni for their great help in the improvement which lead to the final version of this paper. This work was done while visiting UC Davis.

2 Combinatorics

In this section, we define the combinatorial objects suitable for the computation of moments of the spectral measure of random sample covariance matrices. These combinatorial objects are the Narayana paths and are directly related to the so-called Marchenko-Pastur distribution. Then, we give the basic technical estimates needed to compute the moments of traces of powers of sample covariance matrices. We illustrate our counting strategy by giving a refinement of the Marchenko-Pastur theorem and also obtain a Central Limit Theorem.

2.1 Dyck paths and Narayana numbers

Let be some integer that may depend on . Developing (6), we obtain

| (8) | |||

| (9) | |||

| (10) |

In the whole paper, we denote by the rule (10) for the choice of indices in (9). We shall later prove that such a rule plays a fundamental role in the asymptotics of (6). To each term in the expectation (9), we associate three combinatorial objects that will be needed in the following.

First, to each term occuring in (9), we associate the following “ edge path” , formed with oriented edges (read from bottom to top)

| (11) |

Due to the symmetry assumption on the entries of , the sole paths leading to a non zero contribution in (9) are such that each oriented edge appears an even number of times. From now on, we consider only such even edge paths.

To such an even edge path, we also associate a so-called Dyck path, which is a trajectory of a simple random walk on the positive half-lattice such that

We start the path at the origin and draw up steps and down steps as follows.

We read successively the edges of (11), reading each edge from bottom to top.

Then if the edge (oriented) is read for an odd number of times, we draw an up step. Otherwise we

draw a down step. We obtain in this way a trajectory with up and down steps, which is clearly a Dyck path.

We shall now estimate the number of possible trajectories associated to the edge path. Due to the

constraint on the choices for vertices, we shall distinguish trajectories with respect to the number

of up steps performed at an odd instant. Indeed, they are the moments of time where the vertices can be chosen in the set .

In the whole paper, we denote by the number of up steps performed at an odd instant in a Dyck path.

In particular, we denote by the trajectory associated to , where is the number of its odd up steps. We also call the set of Dyck paths of length with odd up steps.

Proposition 2.1.

Remark 2.1.

Narayana numbers are intimately linked with Dyck paths. Let be the Catalan number counting the number of Dyck paths of length It is obvious that Narayana numbers are also linked to the moments of the Marchenko-Pastur distribution defined in (1), since the following was proved by Jonsson [17] (see also [23] and [1]).

Proposition 2.2.

For any integer , one has that

| (13) |

Remark 2.2.

Proposition 2.2 was actually proved for a broader class of sample covariance matrices than that considered in this paper.

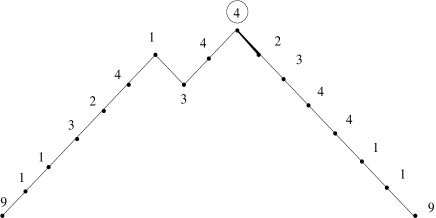

Last, we associate to the edge path a “usual” path, which we denote by as

follows. We mark on the underlying trajectory the successive vertices met in the edge path.

The path associated to (11) is then

For instance, the path associated to

the path

is

given on Fig. 2 below.

|

The three structures and we have here introduced will now be used to compute the moments of traces of (high) powers of Our counting strategy is as follows. Given the sublying Dyck path , we shall estimate the number of edge paths that can be associated to this Dyck path. We shall also estimate their contribution to the expectation (9). This is the object of the two next subsections.

2.2 Marked vertices

In this subsection, we bring out the connection between Narayana paths and the restriction for the choices of vertices occuring in the path imposed by the rule Given a trajectory , we shall now count the number of ways to mark the vertices using the rule In this way, we count the number of paths associated to a given trajectory. The terminology we use is close to the one used in [29], [27], [28] and [30]. We recall the main definitions that will be needed here and also assume that the reader is acquainted with most of the techniques used in the above papers.

The first task is to choose the pairwise distinct vertices occuring in the path. There are at most such vertices. We shall now define “marked vertices”, separating the cases where they are marked at an odd or even instant.

Definition 2.1.

An instant is said to be marked if it is the right endpoint of an up edge of the trajectory .

Marked instants correspond to the moments of time where, considering the top and bottom lines separately, one can possibly “discover” some vertex not already encountered. Consider first the vertices on the top line of the edge path , that is, vertices occuring at odd instants in the path . For , call the class of vertices of occuring times as a marked vertex at an odd instant. Then if we set one has

Note that each time we “discover” on the top line some new vertex, the corresponding instant is necessarily marked. Consider also the vertices on the bottom line. For , denote by the class of vertices of occuring times as a marked vertex at an even instant. Then one has, if

Note that a vertex from the set can occur as a marked vertex on both lines. Yet it is the type of the vertex on each line which is here taken into account. Thanks to the above definition, we characterize a path by its type

For short, we denote by the type of such a path. We also use the following notations. Any vertex (resp. ) is said to be a vertex of self-intersection on the top (resp. bottom) line. A vertex (resp. ) is said to be of type on the top (resp. bottom) line.

The choice of marked vertices is enough to determine the distinct vertices of the path , if the origin of the path also occurs as a marked vertex. We will see that for typical paths, this is not the case and Thus, given the type of the path, the number of ways to assign vertices at the marked instants and choose the origin is then at most:

| (14) |

Indeed, one distributes the vertices of and into the possible classes choose the corresponding marked occurrences of each vertex and fix the origin. Once the marked vertices and the origin of the path are chosen, there remains to fill in the blanks of the path . Due to self-intersections, there are multiple ways to do so. We investigate this numbering in the sequel and consider at the same time the expectation of the filled path.

2.3 Filling in the blanks of the path

Consider now a path with odd marked instants and of type . Call the maximum number of ways to fill in the blanks of at the unmarked instants, once the marked instants and the origin are given.

Proposition 2.3.

Set .

There exists

independent of and such that

| (15) |

Proof of Proposition 2.3

We only sketch the proof which follows essentially the same steps as that of Lemma 1 in [28]. Assume that in , at the unmarked instant , one makes a down step with left vertex . If is of type , then there is no choice for the right endpoint of such an edge. In general, the maximal number of possible right endpoints depends on the multiplicity of as a marked vertex. Knowing the parity of , one also knows whether is a vertex on the top or on the bottom line of . Thus the sole top or bottom multiplicity of the vertex has to be taken into account to estimate the number of ways to close the edges. Thus, it is not hard to see that the number of ways to close the path is at most

The extra factor comes from the case (negligible) where the origin is of type . To consider simultaneously, the expectation of the path, one also has to take into account the number of times each oriented edge is read. Assume that an edge is read times, with . Call (resp. ) the number of times (resp. ) is a marked vertex of this edge. Then, if , one has that Now if an oriented edge is read times then it is closed times along the same edge. That is, we overcount the number of ways to close the path. Thus, if we let be the number of times the oriented edge is read in the path, we obtain that

where are some constants independent of and

Remark 2.3.

In the case where the entries have polynomial tails, with for some , one can first consider (up to a set of negligible probability) that all the entries of are smaller in absolute value than for some small enough. This is true if Then Proposition 2.3 has to be replaced with

This follows from the fact that to each edge seen times there corresponds at least marked occurences of one of its endpoints.

In the two following subsections, we investigate moments of Traces of powers of in scales This will give the foundations for the asymptotics of higher moments.

2.4 Narayana numbers and the Marchenko-Pastur distribution

In this subsection, we illustrate our counting strategy and present a refinement of (13), which allows to consider higher moments than in Proposition 2.2.

Proposition 2.4.

If one has that

Proof of Proposition 2.4

The proof is similar to that of the classical Wigner theorem using Dyck paths (see e.g. [1]). It is divided into two steps. First, we show that paths for which yield a negligible contribution to . Then we estimate the contribution of paths with vertices of type 1 at most, which give the leading term of the asymptotic expansion of , as long as

We denote by the contribution of paths for which . By Proposition 2.3, and using summation, one has that

where and . Thus, it is straightforward to see that there exists some constant independent of such that

| (20) |

From this, we can deduce that .

We now show that only paths with vertices of type 1 (except the origin which is unmarked) have to be taken into account. In this case, once the vertices occuring in the path have been chosen, there is no choice for filling in the blanks of the path Furthermore, each edge is passed only twice in the path , once at an odd instant and once at an even instant. Thus, denoting by the contribution of such paths, one has that

Using (20), this finishes the proof that . The contribution of paths with marked origin and vertices of type at most is of order and thus negligible. This finishes the proof of Proposition 2.4.

Remark 2.4.

Set For any sequence , one has that and that the main contribution to the expectation (6) should come from paths with odd marked instants. Indeed, using Stirling’s formula, one has

It is also easy to check that, for any , one has that

| (21) |

for some constant depending on only. In the case where , we fix some large. Then one can show that, for any , One also has that for any , This ensures that yielding Remark 2.4.

Remark 2.5.

In the case of polynomial tails, (19) is multiplied by a factor If and (which is the largest scale considered in this paper), this has no impact on computations as for any . All the results stated in the following can be proved in the case of polynomial tails up to minor technical modifications (which amounts essentially to considering apart vertices of type at least ).

2.5 A Central Limit Theorem

The main result of this subsection is the following Proposition. Set We show that all the moments of are bounded and universal, as long as . Assume that and set where (resp. ) in the case where is real (resp. complex).

Proposition 2.5.

Assume that and set Then, there exists such that for any , and Similarly, for any integer ,

Remark 2.6.

In [17], a Central Limit Theorem (CLT) is also established for traces of fixed (independent of ) moments of . In this case, the limiting Gaussian distribution does depend on the fourth moment of the law of the entries. The above CLT is also stated but not proved in Remark 6 of [27] (a factor is missing) in the case where .

Proof of Proposition 2.5

We only give the proof for the variance. The proof of the asymptotics for higher moments is a rewriting of pages 128-129 in [28] (also [9] Section 6) and is skipped. In the following, denote some positive constants independent of . One has that

Here, given an edge , stands for if occurs at an odd instant of or for if it occurs at an even instant.

Now it is clear that the non zero terms in the above sum come from pairs of paths ,

sharing at least one oriented edge and such that each edge appears an even number of times in the union of the two paths. We say that such paths are correlated.

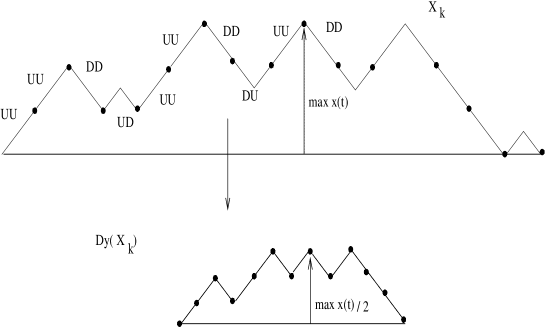

To estimate the number of correlated paths and their contribution to the variance, we use the construction procedure defined in Section 3 of [27]. This construction associates a path of length to a pair of correlated paths.

Let and be two correlated paths of length . When reading the edges of , let denote the first oriented edge common to the two paths. Let also and be the instants of the first occurrence of this edge in and . Then we are going to glue the two paths and , in such a way that we erase the two first occurrences of in each of these paths. The glued path, denoted , is obtained as follows.

We first read until we meet the left endpoint of at the instant . Then we switch to as follows. Assume first that and are of the same parity. We then read the path , starting from , in the reverse direction to the origin and restart from the end of until we come back to the instant . If and are not of the same parity, we read the edges of in the usual direction starting from and until we come back to the instant . We have then read all the edges of except the edge occuring between and We then read the end of , starting from

Having done so, we obtain a path which is of length .

One can also note that the trajectory of does not descent lower than the level during the time interval , by the definition of and .

Now, to reconstruct the paths and from , it is enough to determine the instant at which one has switched from one path to the other, the origin of the path and the direction in which is read. There are at most ways to determine the origin and the direction once the instant of switch is known.

To estimate the number of preimages of a given path of length and with odd up steps, one has to give an upper bound for the number of instants in , which can be the instants of switch.

To this aim, fix some and assume that the trajectory of does not go below the level during an interval of time of length greater than or equal to Assume that Set then

Denote by the sub-trajectory in the interval . It is a Dyck path. Denote also by the remaining part of the trajectory: it is also a Dyck path, along which the instant has been chosen. We denote by the number of the odd up steps of . As the trajectory of is obtained by inserting at the instant in , and using the fact that and have all the same edges but one, one can then deduce (see [27], p. 11-13, for the detail) that the contribution of correlated pairs is at most of order

| (22) | |||

| (23) | |||

| (24) | |||

| (25) | |||

| (26) | |||

| (27) |

Here is the contribution of paths of length with odd up steps to the expectation

and (resp. ) corresponds to the case where is even (resp. odd). The term in (24) comes from the determination of and where , if is the edge erased from . It can indeed be shown that paths for which such an edge occurs also in yield a contribution of order that of typical paths and are thus negligible.

We first show that the variance is bounded. In the following, we set and

Considering for instance , ( is similar), it is enough to prove that there exists a constant such that

One can easily see that it is enough to consider the case where It is also straightforward by Remark 2.4 and Proposition 2.4 to see that one can choose such that

This is enough to ensure that the contribution of correlated pairs such that the corresponding glued path has odd up instants for some or is negligible in the large--limit. We now set

| (28) |

Then, and being fixed, is maximal at Furthermore, one can check that there exist constants such that for any . From this we deduce that

| (29) | |||

| (30) |

It is now an easy consequence of Stirling’s formula that

| (31) |

where Using Proposition 2.4, one can also show that there exists such that

Combining the whole yields that there exists a constant such that

In the case where , is chosen amongst the returns to the level of the trajectory. It can be shown that the number of such instants is negligible with respect to in typical paths. This follows from arguments already used above and in [27] p. 13.

To compute the variance, we notice that in (24), the term can actually be replaced with . Indeed as is even, the first step after is a down step occuring at an odd instant. Also, there are only choices for the origin of , since one knows the parity of in once the orientation of is fixed.

Then, using (24), (27), Remark 2.4, the exponential decay of , and Proposition 2.4, one can deduce that (for the real case)

| (32) | |||

| (33) | |||

| (34) | |||

| (35) | |||

In (35), we have set , and the equality follows from the fact that is a Cauchy product. The value of can be deduced from Formulas 4.7 in [30] and 3.6 in [27]. The computation of follows from the fact that, in the complex case, the occurences in and cannot have the same parity (in typical paths).

3 The case where

The aim of this section is to prove the following universality results. Let be a sequence of sample covariance matrices satisfying to (resp. to . Let be some given integer and be constants chosen in some compact interval (independent of ). Consider sequences such that

Theorem 3.1.

Set There exists a constant such that

The proof of Theorem 3.1 is the object of this section. We actually focus on the case where . Indeed, the proof of Theorem 3.1 for is a rewriting of the arguments used in [29] (p. 41), Subsection 2.5 and of the arguments used in the case where . It is not developed further here. Then, we essentially show that typical paths (i.e. those having a non negligible contribution to the expectation) have no oriented edge read more than twice. This ensures that the expectation (6) only depends on the variance of the entries . Universality of the expectation then follows.

3.1 Number of self-intersections and odd marked instants in typical paths

We first give a technical Proposition which bounds the number of self intersections and give the approximate number of odd marked instants in typical paths. In the following, we denote by the contribution of paths with odd marked instants. We also denote the number of self-intersections on each line as

Proposition 3.1.

There exists a positive constant such that the contribution of paths for which

is negligible in the large--limit, whatever is.

And for any such that , one has that

Proof of Proposition 3.1

We first give the proof of the first point of Proposition 3.1. Denote by the contribution of paths with odd marked instants and of type Using (19), Remark 2.4 (and exactly the same arguments as in [29] p. 34), one can see that, for large enough,

We now turn to the second statement. Let then and be chosen as in Proposition 3.1. We assume that is large enough so that We now show that Given any integer , and using (19), one can show that there exists a constant independent of and such that . Thus

for large enough. Similarly, the contribution of paths for which is negligible in the large--limit.

3.2 Asymptotics of

In this subsection, we refine the estimate (19) and in particular deal with vertices of type . Indeed, when summing (19) over and , one can note that terms associated to vertices of type make the summation go to infinity. To this aim, we shall control the number of vertices for which there is an ambiguity to continue the path at an unmarked instant. We shall also control the number of such vertices associated to edges passed four times or more. Finally, we shall also show that amongst vertices of type , none belongs to edges passed more than twice, while there are no more complex self-intersections in typical paths.

From now on, given , we consider a path of type with (resp. ) self-intersections on the bottom (resp. top line). Our counting strategy is refined as follows.

Knowing the moments of self-intersection, we first choose the vertices occuring at the remaining marked moments.

One fills in the blanks of the path until the first moment of self-intersection is encountered. Then,

one chooses the vertex which is repeated among the preceding ones (and repeat it if needed at the moment of second self-intersection and so on). We then proceed in the same way for subsequent vertices.

Assume that the instants of self-intersections have been chosen on each line:

for vertices of type 2 on the bottom line,

for vertices of type 2 on the top line,

for the first repetition of a

vertex of type 3 on the bottom line, for the second repetition of a vertex of type 3 on the

bottom line.

We do not go deeper in the list of instants since it is exactly the same as in [29] p. 724,

except that we make a distinction between instants marked on the top or bottom line (even if it is the same vertex).

The number of pairwise distinct vertices in the order of appearance on each line (top or bottom) occuring in the path is at most

| (36) |

Note that

First, we focus on vertices of type 2. In the general case, there are choices for the vertex occuring at the instant , since one chooses vertices occuring twice as marked instants. Assume first that the path is such that there

are no choices for closing any edge from such vertices at unmarked instants and that none belongs

to edges passed four times or more. Then choosing the instants and vertices of type 2 gives a contribution

at most of order

Such an estimate combined with formula (36) and Remark 2.4 then ensures that the contribution of such paths to is bounded.

Yet amongst vertices of type on the bottom or on the top line, at an unmarked instant where one closes an edge with such a vertex as left endpoint, there might be a choice for closing the edge. Note that there are at most three choices. An example of such a vertex is the distinguished vertex on Figure 2, as the distinguished edge could have been . Indeed, the two up edges with as marked vertex on the top line are read before the first time a down edge is closed starting from . This leads to the notion of non-closed vertex.

Definition 3.1.

A vertex of type 2 is said to be non-MP-closed if it is an odd (resp. even) marked instant and if there are more than one choice for closing an edge at an unmarked instant starting from this vertex on the top (resp. bottom) line.

Remark 3.1.

The definition of non-MP-closed vertices differs from that of non-closed vertices in [29], essentially due to the distinction which is made between the top and bottom lines.

Let be a given instant. Assume that the marked vertices before have been chosen and that, at the instant , there is a non-MP-closed vertex. Then, by the definition of the trajectory and of non-MP-closed vertices, there are at most possible choices for this vertex. This can be checked as in [28], p 122. In Lemma 3.1 below, we show that in typical paths.

Apart from non-MP-closed vertices, a vertex of type can also belong to an edge that is read four times in the path. To consider such vertices, we need to introduce other characteristics of the path. Let be the maximal number of vertices that can be visited at marked instants from a given vertex of the path Let also be the maximal type of a vertex in Then, if at the instant , one reads for the second time an oriented up edge , there are at most choices for the vertex occuring at the instant . Indeed, one shall look among the oriented edges already encountered in the path and of which one endpoint is the vertex occuring at the instant (see the Appendix in [28] and [9] Section 5.1.2 e.g.). It is an easy fact that paths for which lead to a negligible contribution, if is large enough (independently of ). We prove at the end of this subsection, using Lemma 3.2 stated below, that there exists small enough such that, for typical paths,

For vertices of type , once the moments of self-intersection are fixed, one chooses at the first moment of self-intersection the vertex to be repeated amongst those already occurred in the path.

Assuming the above estimates on and hold, we consider paths of type with and self-intersections respectively on the bottom or on the top line, non-MP-closed vertices of type () on the bottom and top lines and () vertices of type on the bottom or top line, visited at the second marked instant along an oriented edge already seen in the path. By Proposition 2.3, (36) and the above, their contribution to is then at most of order (see also [29], p725)

| (37) | |||

| (38) | |||

| (39) | |||

| (40) | |||

| (41) |

Here are positive constants independent of and , and denotes the expectation with respect to the uniform distribution on . Here we have used the fact that

for any function .

Before considering paths in complete generality, we first restrict to paths with less than self-intersections and no self-intersection of type strictly greater than :

Let denote the total contribution of paths with odd marked instants such that , with no oriented edges read more than twice and satisfying the above conditions.

Proposition 3.2.

There exists a constant independent of such that

Proof of Proposition 3.2

Assuming that there are no self-intersections of type greater than , we can then show that paths for which give a contribution of order and thus there are no edges read more than twice (associated to vertices of type 2). We then proceed in the same way to show that there are no more than vertices of type in typical paths and that there are no oriented edges read more than twice associated to vertices of type . It is then easy to deduce from the above result that paths with self-intersections of type or greater, or a marked origin, lead to a contribution of order . The detail is skipped.

Finally we investigate the total contribution of paths for which where is fixed (small). Denote by such a contribution. We only indicate the tools needed to prove that

since the detail of the proof is a rewriting of the arguments of the proof of Lemma 7.8 in [9]. To consider such paths, we introduce the following characteristic of the path, namely Assume then that and are given. We can then divide the interval into sub-intervals, so that inside an interval, there are only closed vertices of type 2 or no self-intersection. Then there is no choice for closing the edges inside these sub-intervals. Assume that a vertex is the starting point of up edges. Then, there is a time interval during which the trajectory of comes times to the level (of ) and never goes below. Denote by the event that there exists such an interval in a trajectory and let denote the uniform distribution on In Lemma 3.2, we show that the probability of such an event decreases as

for some positive constants independent of . Using Lemma 3.1, one can also show that there exists a constant such that in any non-negligible path. Using these estimates, formula , and Lemma 3.2 proved below, one can then copy the arguments used

in [9] Lemma 7.8, to deduce that

This finishes the proof that typical paths have a non-marked origin, vertices of type at most (and less than of type ), less than self-intersections and no edges read more than twice.

The proof of Theorem 3.1 is

completed once Lemmas 3.1 and 3.2 are proved.

3.3 Technical Lemmas

In this subsection, we prove the results used in the previous subsection on characteristics of typical paths. The first quantity of interest here is the maximum level reached by the trajectory of a path, namely . We shall show that it roughly behaves as in typical paths. The second one is the maximal number of vertices visited from a given vertex, which should not grow faster than for any power (but we get a weaker bound).

We shall now prove the announced estimate for , where denotes the level of the trajectory associated to a path . Let be some constant independent of and and denote by the expectation with respect to the uniform distribution on the set of trajectories of length with up edges at odd instants.

Lemma 3.1.

Given there exists independent of (and ) such that

Proof of Lemma 3.1

It was proved in [28] that the above result holds if one replaces with the expectation with respect to the uniform distribution on Dyck paths (no constraint on ) of length We will call on this result to prove Lemma 3.1. To this aim, we cut the Dyck path into steps, so that there are 4 types of basic 2-steps : , , and ( stands here for down, for up). It is an easy fact that the number of steps equals that of steps. Let then be the number of steps (and steps), be those of and be those of steps. Then,

| (43) |

As a step or brings the path to the same level, it is easy to see that the steps and are arranged in such a way that they form a Dyck path (if we identify a step with an up step and a step with a down step) of length . We denote this sub-Dyck path associated to the trajectory (see Fig. 3).

|

We now explain how to build a trajectory given of length and (resp. ) (resp. ) steps. To construct from , one has to insert “horizontal” steps, namely and steps, in a particular way. Note that two distinct insertions lead to two different trajectories. The sole constraint is to insert steps when the path is at a level greater than or equal to one. This is the reason why we enumerate Dyck paths with steps according to the number of times they come back to the level . Call the number of Dyck paths with steps and returns to . We then have to insert horizontal steps into boxes. Then we can insert the steps arbitrarily. This yields that

| (44) |

From this construction, it is easy to see that the maximum level reached by the trajectory is twice the maximum reached by the sub-path Let then denote the set of Dyck paths of length with returns to We do not consider the degenerate case where , which corresponds to the trajectory obtained with steps only. Then one has that

| (45) | |||

| (46) | |||

| (47) | |||

| (48) |

Let denote the uniform distribution on . Let also (small) be given. It can easily be inferred from [28], p. 11 (see also [29] and [9], Lemma 7.10) that there exist positive constants , independent of and such that, if , one has that

| (49) |

Thus, inserting (49) in (48), we deduce that there exist some positive constants independent of and such that, provided and for any This yields Lemma 3.1.

The second estimate we need is a suitable bound on . Recall that denotes the event that the trajectory of a path comes back from above times to some level .

Lemma 3.2.

There exist positive constants independent of such that

| (50) |

Proof of Lemma 3.2

Let be an interval such that for some and and for which there exists such that . We first consider the case where and are even instants (then is also even). Modifications to be made in the case where they are odd will be indicated at the end of the proof. The instants are then called instants of returns from above to of the trajectory . Set now to be the Dyck path of length defined by . Then the returns from above to correspond to returns to of . Now, the returns to of can either be made using steps or correspond to a return of the sub-trajectory to this level. Thus, either the number of steps is large or the number of returns of to level is large. We shall show that in both cases, (50) holds. Thanks to Proposition 3.1, it is enough to consider trajectories for which The proof of Lemma 3.2 is divided into three steps.

Step 1

We first show that there exist positive constants independent of and such that, provided

| (51) |

Assume that there exists a time interval with consecutive steps only. Given even instants and (with ), the proportion of trajectories that have steps in is at most

| (52) |

for some constant This readily yields (51).

Step 2

We consider the case where the number of returns to level made by the associated path is large. It was proved in [28] that, if denotes the uniform distribution on the set of Dyck paths with length , then there exist constants independent of such that

| (53) | |||

| (54) |

Denote by the number of sub-Dyck paths of starting and ending at level From the above result and (44), one can deduce that there exists constants , independent of and , such that

| (55) |

Step 3

We can now turn to the proof of Lemma 3.2. A trajectory coming back times to the level during can be described as follows. Denote by the number of sub-Dyck paths going from level to and starting with a step and ending with a step. Denote by the respective length of these sub-Dyck paths. Then these sub-Dyck paths are interspaced by steps that split in at most sequences. Let () be the respective lengths of these disjoint sequences of steps from to . Using the estimates of Step 1 and Step 2, there exist constants such that for any constants (fixed later),

| (56) | |||

| (57) |

Thus it is enough to consider trajectories such that To count these

trajectories, we study their structure in more detail. Set and let then

be the number of odd marked instants of the sub-trajectory inside the interval . The

remaining trajectory , is then a Dyck path of length with odd up steps. Given and and in order to count the number of such trajectories we first re-order the paths and steps inside the interval as follows. We first read the Dyck paths and then read all the steps.

Fix some (small). Assume first that

| (58) |

The latter condition ensures, as for some , that . Thus, we can apply Step 1 to the sub-trajectory obtained from by erasing the sub-paths . Then, given , and , the number of trajectories of length with odd up steps and that have steps between is of order

Here are some positive constants independent of and Note that the constant depends only on and . Then, the number of Dyck paths of length , with odd up steps and coming back times to the level 0 using steps is at most of order

As above

are positive constants independent of and

Finally the number of ways to order the paths

and the steps inside the interval is equal to the number of

ways to write as a sum of integers. There are such ways.

Thus the number of trajectories coming times to some level never falling

below is at most, if

| (59) | |||

| (60) |

since, and being fixed, . This yields the following estimate:

We can then choose large enough so that there exists a constant independent of and such that

This yields Lemma 3.2 if (58) is satisfied.

Assume now that (58) is not satisfied. Then necessarily

Thus the number of trajectories coming times to some level with returns made using steps is at most

where is the number of Dyck paths of length , with returns to made only with steps and admitting odd up steps. From Step 2, one has that there exists a constant (independent of ) such that

As , there also exists (depending on and only) such that

The end of the proof is as above. This finishes the proof of Lemma 3.2 in the case where and are even.

To consider the case where and are odd, one can then use exactly the same arguments as above, up to the following modifications. An odd marked instant of simply defines an even marked instant of . Then it is an easy task to show that Step 1 holds if one replaces with in (52). Step 2 and Step 3 can then be obtained using arguments as above.

This finally completes the proof of Theorem 3.1.

4 The case where and

In this section, we consider the sequence of random sample covariance matrices instead of . We also consider moments of traces of to some powers The above scaling readily comes from Theorem 1.4 proved by [6]. In particular, one has that

| (61) |

We here prove the following universality result. Let be some given integer and be positive constants chosen in a fixed compact interval of . Consider sequences such that

Theorem 4.1.

Let There exists such that

The proof of Theorem 4.1 is the object of the whole section. We only consider the case where and is some sequence such that

| (62) |

As in the preceding section, we establish that the typical paths have no edges read more than twice. This ensures that the leading term in the asymptotic expansion of is the same as that for Wishart ensembles. The idea of the proof is very similar to that of the preceding section, but requires some minor modifications. This is essentially due to the discrepancy between marked vertices on the bottom and top lines, due to the fact that

In this section, , denote some positive constants independent of and whose value may vary from line to line (and from the preceding sections).

4.1 Typical paths

We now state the counterpart of the second point in Proposition 3.1 in the two following Propositions. Let be the sub-sum corresponding to the contribution to (61) of paths for which , for some to be fixed.

Proposition 4.1.

There exists such that

Proof of Proposition 4.1

By (19), one has that

| (64) | |||||

Now there exists a constant such that, for any ,

| (65) |

Similarly, using the fact that , we deduce that

| (66) | |||

| (67) | |||

| (68) |

as and provided . Inserting (68) and (65) in (64) yields that

| (69) |

We then deduce the following upper bound. For large enough, one has

where in the last line we have chosen This finishes the proof of Proposition 4.1.

Given , we also consider the contribution of paths for which .

Proposition 4.2.

There exists such that

Proof of Proposition 4.2

Set now . Thanks to Proposition 4.1 and Proposition 4.2, typical paths are such that . This implies in particular that and Using the fact that , it is easy to deduce from (19), that it is enough to consider paths for which for some constant independent of , and . For such paths, denote by the contribution of paths with odd marked instants. We now prove the following Proposition yielding Theorem 4.1.

Proposition 4.3.

There exists such that Furthermore, the contribution of paths admitting either an edge read more than twice, or more than vertices of type , or a vertex of type 4 or greater, or a marked origin is negligible in the large--limit.

Remark 4.1.

Considering paths admitting only vertices of type 2 at most and no non-MP-closed vertices, one can also deduce from the subsequent proof of Proposition 4.3, that there exists such that

Proof of Proposition 4.3

First, one can state the counterpart of Formula (41). Due to the different scales while , we need in this section to distinguish vertices being the left endpoint of an up edge according to the parity of the corresponding instant. Define (resp. to be the maximum number of vertices visited (at marked instants) from a vertex of the path occuring at odd instants (resp. even instants). Then,

| (77) | |||||

One still has that for some in typical paths (independently of ). This ensures that the analysis performed for the case where can be copied, provided the counterparts of technical lemmas of Subsection 3.3 hold. Let be given. Assume for a while that typical paths are such that there exists such that, ,

| (78) | |||

| (79) |

The above statement will be proved in the subsequent subsection (Lemma 4.1 and Lemma 4.2) and using exactly the same arguments as in Lemma 7.8 in [9].

We then copy the arguments of Proposition 3.2 and the sequel.

Then it is easy to deduce that typical paths have a non-marked origin, vertices of type at most

(and a number of vertices of type smaller than ) and no edge passed more than twice.

The other paths lead to a negligible contribution. We can also deduce that non-MP-closed vertices of type 2 as well as vertices of type occur only on the bottom line in typical paths.

In particular, let denote the contribution of paths for which

, and no edges read more than twice.

Then and

This ensures that the limiting expectation depends only on the variance and has the same behavior as for Wishart ensembles. The proof of Theorem 4.1 is complete, provided we prove the announced Lemmas.

4.2 Technical Lemmas

We now state the counterpart of Lemma 3.1.

Lemma 4.1.

Given , there exists such that

Remark 4.2.

Lemma 4.1 also yields that

Proof of Lemma 4.1

One next turns to establish the counterpart of Lemma 3.2. We denote (resp. ) the event that the maximal number of times the trajectory comes from above (without falling below) to some level at even instants (resp. odd instants) is (resp. ).

Lemma 4.2.

There exist positive constants independent of and such that

| (80) | |||

| (81) |

Proof of Lemma 4.2

As in the preceding section, we have to estimate the

probability that the trajectory comes to some level times without falling below in some time interval Note that the two steps leading and starting at (resp. ) are up (resp. down) steps. This is because is a maximal interval. Thus the number of possible choices for and is at most of order , as

We first prove (80) and thus assume that is odd. Then the returns to occur at odd instants.

The counterpart of formula (52) states

| (82) |

The two steps preceding (and following) are either both up steps or both down steps (regardless of the fact that are even or odd).

The estimate (53) still holds (up to the change ) so that formula (80) is proved,

copying the proof of Lemma 3.2.

We now turn to the proof of (81) which is more involved than in Lemma 3.2.

Formula (52) translates to

Step 1 and Step 2 are then obtained as in Lemma 3.2 (with ). From that, we can deduce that we can consider in Step 3 only the paths for which for some constants . We need to refine the estimate for Step . Let then be the interval where returns to some level occur. We call the trajectory defined by We then define to be its number of odd up steps, to be its number of returns to using steps, (resp. , ) to be its number of steps (resp. of steps and of steps occuring at some positive level). Assume that are given and observe that . Let then denote the conditional probability on the event that has odd up steps, steps and has steps and returns to . Then, one has that

One first shows that it is enough to consider the subpaths such that for some small enough. This follows from the fact that and arguments already used in Subsection 2.5 (see also (21)). This yields that

for some provided , where has been fixed in Proposition 4.1. The analysis of the case where is similar. We can assume that is small enough to ensure that This yields (81) and ensures that it is enough to consider the case where Fixing and we set As one has that One can check that there exist a constant independent of and such that, for a given constant ,

Thus it is clear that the proportion of paths coming back times from above to some level and for which is at most of order Paths for which are considered as in Step 2. This is enough to ensure (81).

Remark 4.3.

The investigation of higher moments follows the same steps as in Subsection 2.5. In particular, considering , only pairs of correlated paths such that has a number of odd up steps of order are non-negligible. In (24), one can also replace the term with . Considering as above the exponential decay of (28), one can also show that where Thus (31) can be replaced with

where One can readily deduce from the above that the contribution of (27) is negligible. The case where yields a negligible contribution, as readily seen from (79) and Lemma 4.2. The latter is then enough to ensure that is bounded and only depends on the variance of the entries. The investigation of higher moments is similar.

References

- [1] Bai, Z.D. (1999). Methodologies in spectral analysis of large-dimensional random matrices, a review. Statist. Sinica 9 no. 3, 611–677.

- [2] Bai, Z.D., Krishnaiah, P.R. and Yin, Y.Q. (1988). On the limit of the largest eigenvalue of the large-dimensional sample covariance matrix. Probab. Theory Related Fields 78, 509–521.

- [3] Baik, J. and Slverstein, J. (2006). Eigenvalues of large sample covariance matrices of spiked population models. Journ. of Mult. Anal. 97, 1382–1408.

- [4] Bronk, B.V. (1965). Exponential ensembles for random matrices. J. Math. Phys. 6, 228–237.

- [5] Chen, W., Yan, S. and Yang, L. Identities from Weighted Motzkin paths. Available at www.billchen.org/publications/identit/identit.pdf.

- [6] El Karoui, N. (2003). On the largest eigenvalue of Wishart matrices with identity covariance when , and tend to infinity. ArXiv math.ST/0309355.

- [7] El Karoui, N. (2005). Recent results about the largest eigenvalue of random covariance matrices and statistical application. Acta Phys. Polon. B 36 no. 9, 2681–2697.

- [8] El Karoui, N. (2006). A rate of convergence result for the largest eigenvalue of complex white Wishart matrices. Ann. Prob. 34 no. 6, 2077-2117.

- [9] Féral, D. and Péché, S. (2006). The largest eigenvalue of some rank one deformation of large Wigner matrices. ArXiv math.PR/0605624, to be published in Comm. Math. Phys.

- [10] Geman, S. (1980). A limit theorem for the norm of random matrices. Ann. Prob. 8, 252–261.

- [11] Hotelling, H. (1933). Analysis of a complex of statistical variables into principal components. Jour. Educ. Psych. 24, 417–441.

- [12] Hoyle, D. and Rattray, M. (2003). Limiting form of the sample covariance eigenspectrum in PCA and kernel PCA. Advances in Neural Information Processing Systems NIPS 16.

- [13] James, A. (1960). Distributions of matrix variates and latent roots derived from normal samples. Ann. Math. Statist. 31, 151–158.

- [14] Johansson, K. (2000). Shape fluctuations and random matrices. Comm. Math. Phys. 209, 437–476.

- [15] Johnstone, I. M. (2001). On the distribution of the largest Principal Component. Ann. Statist. 29, 295–327.

- [16] Johnstone, I. M. (2007). High dimensional statistical inference and random matrices. arXiv:math/0611589, to appear in Proc. International Congress of Mathematicians, 2006.

- [17] Jonsson, D. (1982). Some limit theorems for the eigenvalues of sample covariance matrices. Journ. of Mult. Anal. 12, 1–38.

- [18] Laloux, L., Cizeau, P., Potters, M. and Bouchaud, J. (2000). Random matrix theory and financial correlations. Intern. J. Theor. Appl. Finance 3 no.3, 391–397.

- [19] Malevergne, Y. and Sornette, D. (2004). Collective origin of the coexistence of apparent RMT noise and factors in large sample correlation matrices. Physica A 331 no3-4, 660–668.

- [20] Marcenko, V.A. and Pastur, L.A. (1967). Distribution of eigenvalues for some sets of random matrices. Math. USSR-Sbornik 1, 457–486.

- [21] Patterson, N., Price, A.L. and Reich, D. (2006). Population structure and eigenanalysis. PLoS Genet 2(12): e190 DOI: 10.1371/journal.pgen.0020190.

- [22] Péché, S. and Soshnikov, A. (2007) Wigner random matrices with non-symmetrically distributed entries. arXiv:math/0702035. To appear in the special issue of J. Stat. Phys.: Applications of random matrices, determinants and pfaffians to problems in statistical mechanics.

- [23] Oravecz, F. and Petz, D. (1997). On the eigenvalue distribution of some symmetric random matrices. Acta Sci. Math. 63, 383–395.

- [24] Plerous, V., Gopikrishnan, P., Rosenow, B., Amaral, L., Guhr, T. and Stanley, H. (2002). Random matrix approach to cross correlations in financial data. Phys. Rev. E 65 no.6, 66–126.

- [25] Sear, R. and Cuesta, J. (2003). Instabilities in complex mixtures with a large number of components. Phys. Rev. Lett. 91 no.24, 245–701.

- [26] Silverstein, J. (1989). On the weak limit of the largest eigenvalue of a large-dimensional sample covariance matrix. J. Multivariate Anal. 30 no. 2, 307–311.

- [27] Sinai, Y. and Soshnikov, A. (1998). Central limit theorem for traces of large random symmetric matrices with independent matrix elements. Bol. Soc. Brasil. Mat. (N.S.) 29 no. 1, 1–24.

- [28] Sinai, Y. and Soshnikov, A. (1998). A refinement of Wigner’s semicircle law in a neighborhood of the spectrum edge for random symmetric matrices. Funct. Anal. Appl. 32, 114-131.

- [29] Soshnikov, A. (1999). Universality at the edge of the spectrum in Wigner random matrices. Comm. Math. Phys. 207, 697-733.

- [30] Soshnikov, A. (2002). A note on universality of the distribution of the largest eigenvalues in certain sample covariance matrices. J. Statist. Phys. 108, 1033–1056.

- [31] Stanley, R. (1999). Enumerative combinatorics. Vol. 2. Cambridge Studies in Advanced Mathematics, 62. Cambridge University Press, Cambridge.

- [32] Sulanke, R. (2000). Counting lattice paths by Narayana polynomials. Electron. J. Combin. 7, 9p (electronic).

- [33] Sulanke, R. (1998). Catalan path statistics having the Narayana distribution. Proceedings of the 7th Conference on Formal Power Series and Algebraic Combinatorics (Noisy-le-Grand, 1995). Discrete Math. 180 no. 1-3, 369–389.

- [34] Telatar, E. (1999). Capacity of milti-antenna Gaussian channels. European transactions on Telecommunications. 10 no.6, 585–595.

- [35] Tracy, C. and Widom, H. (1994). Level-spacing distribution and Airy kernel. Commun. Math. Phys. 159, 151-174.

- [36] Tracy, C. and Widom, H. (1996). On orthogonal and symplectic matrix ensembles. Commun. Math. Phys. 177, 727-754.

- [37] Wachter, K. (1978). The strong limits of random matrix spectra for sample covariance matrices of independent elements. Ann. Probab. 6, 1-18.