When the Cramér-Rao Inequality provides no information

Steven J. Miller

Department of Mathematics, Brown University, 151 Thayer

Street, Providence, RI 02912

sjmiller@math.brown.edu

Abstract.

We investigate a one-parameter family of

probability densities (related to the Pareto distribution, which

describes many natural phenomena) where the Cramér-Rao

inequality provides no information.

Key words and phrases:

Cramér-Rao Inequality, Pareto distribution, power law

2000 Mathematics Subject Classification:

62B10 (primary), 62F12, 60E05 (secondary).

The author would like to thank Alan Landman for many enlightening

conversations and the referees for helpful comments. The author was

partly supported by NSF grant DMS0600848.

1. Cramér-Rao Inequality

One of the most important problems in statistics is estimating a

population parameter from a finite sample. As there are often many

different estimators, it is desirable to be able to compare them and

say in what sense one estimator is better than another. One common

approach is to take the unbiased estimator with smaller variance.

For example, if are independent random variables

uniformly distributed on , and

, then and are both unbiased estimators of but the

former has smaller variance than the latter and therefore provides a

tighter estimate.

Two natural questions are (1) which estimator has the minimum

variance, and (2) what bounds are available on the variance of an

unbiased estimator? The first question is very hard to solve in

general. Progress towards its solution is given by the

Cramér-Rao inequality, which provides a lower bound for the

variance of an unbiased estimator (and thus if we find an estimator

that achieves this, we can conclude that we have a minimum variance

unbiased estimator).

Cramér-Rao Inequality: Let

be a probability density function with continuous

parameter . Let be independent random

variables with density , and let

be an unbiased estimator of

. Assume that satisfies two conditions:

(1)

we have

(1.1)

(2)

for each , the variance of

is finite.

Then

(1.2)

where denotes the expected

value with respect to the probability density function

.

For a proof, see for example [CaBe]. The expected value in

(1.2) is called the information number or the

Fisher information of the sample.

As variances are non-negative, the Cramér-Rao inequality

(equation (1.2)) provides no useful bounds on the

variance of an unbiased estimator if the information is infinite, as

in this case we obtain the trivial bound that the variance is

greater than or equal to zero. We find a simple one-parameter family

of probability density functions (related to the Pareto

distribution) that satisfy the conditions of the Cramér-Rao

inequality, but the expectation (i.e., the

information) is infinite. Explicitly, our main result is

Theorem:Let

(1.3)

where is chosen so that is a

probability density function. The information is infinite when

. Equivalently, the Cramér-Rao inequality yields the

trivial (and useless) bound that

for any unbiased estimator of when

.

In §2 we analyze the density in our theorem in

great detail, deriving needed results about and its

derivatives as well as discussing how is related to

important distributions used to model many natural phenomena. We

show the information is infinite when in

§3, which proves our theorem. We also discuss

there properties of estimators for . While it is not clear

whether or not this distribution has an unbiased estimator, there is

(at least for close to 1) an asymptotically unbiased

estimator rapidly converging to as the sample size tends to

infinity. By examining the proof of the Cramér-Rao inequality we

see that we may weaken the assumption of an unbiased estimator.

While typically there is a cost in such a generalization, as our

information is infinite there is no cost in our case. We may

therefore conclude that arguments such as those used to prove the

Cramér-Rao inequality cannot provide any information for

estimators of from this distribution.

2. An Almost Pareto Density

Consider

(2.1)

where is

chosen so that is a probability density function. Thus

(2.2)

We chose to have in the denominator to ensure that

the above integral converges, as does times the integrand;

however, the expected value (in the expectation in

(1.2)) will not converge.

For example, diverges (its integral looks like

) but converges (its integral looks like

); see pages 62–63 of [Rud] for more on close

sequences where one converges but the other does not. This

distribution is close to the Pareto distribution (or a power law).

Pareto distributions are very useful in describing many natural

phenomena; see for example [DM, Ne, NM]. The inclusion of the

factor of allows us to have the exponent of in the

density function equal and have the density function

defined for arbitrarily large ; it is also needed in order to

apply the Dominated Convergence Theorem to justify some of the

arguments below. If we remove the logarithmic factors then we obtain

a probability distribution only if the density vanishes for large

. As is a very slowly varying function, our

distribution may be of use in modeling data from an

unbounded distribution where one wants to allow a power law with

exponent , but cannot as the resulting probability integral would

diverge. Such a situation occurs frequently in the Benford Law

literature; see [Hi, Rai] for more details.

We study the variance bounds for unbiased estimators

of , and in particular we show that when

then the Cramér-Rao inequality yields a useless

bound.

Note that it is not uncommon for the variance of an unbiased

estimator to depend on the value of the parameter being estimated.

For example, consider again the uniform distribution on

. Let denote the sample mean of

independent observations, and be

the largest observation. The expected value of and

are both (implying each is an unbiased

estimator for ); however, and

both depend on , the parameter being estimated (see, for

example, page 324 of [MM] for these calculations).

Lemma 2.1.

As a function of , is a strictly

increasing function and . It has a one-sided derivative at

, and .

Proof.

We have

(2.3)

When we have

(2.4)

which is clearly positive and finite. In fact, because

the integral is

(2.5)

though all we

need below is that is finite and non-zero, we have chosen to

start integrating at to make easy to compute.

It is clear that is strictly increasing with , as

the integral in (2.4) is strictly decreasing with

increasing (because the integrand is decreasing with

increasing ).

We are left with determining the one-sided derivative of

at , as the derivative at any other point is handled

similarly (but with easier convergence arguments). It is technically

easier to study the derivative of , as

(2.6)

and

(2.7)

The reason we consider the derivative of is that

this avoids having to take the derivative of the reciprocals of

integrals. As is finite and non-zero, it is easy to pass to

. Thus we have

(2.8)

We want to interchange

the integration with respect to and the limit with respect to

above. This interchange is permissible by the Dominated

Convergence Theorem (see Appendix A for details of

the justification). Note

(2.9)

one way to see this

is to use the limit of a product is the product of the limits, and

then use L’Hospital’s rule, writing as .

Therefore

(2.10)

as this is finite and non-zero, this completes the

proof and shows .

∎

Remark 2.2.

We see now why we chose instead of . If we only had two factors of in the

denominator, then the one-sided derivative of at

would be infinite.

Remark 2.3.

Though the actual value of

does not matter, we can

compute it quite easily. By (2.10) we have

(2.11)

Thus by

(2.6), and the fact that (Lemma

2.1), we have

(2.12)

3. Computing the Information

We now compute the expected value, ; showing it is

infinite when completes the proof of our main result.

Note

(3.1)

By Lemma 2.1 we know that is finite for each . Thus

(3.2)

If then the expectation is finite and

non-zero. We are left with the interesting case when .

As is finite and

non-zero, for sufficiently large (say for some

, though by Remark 2.3 we see that we may

take any ) we have

(3.3)

As , we have

(3.4)

Thus the expectation is infinite. Let

be any unbiased estimator of . If

then the Cramér-Rao inequality gives

(3.5)

which provides no information

as variances are always non-negative. This completes the proof of

our theorem.

We now discuss estimators for for our distribution

. If are independent random

variables with common distribution , then as

the sample median converges to the population median

(if then the sample median converges

to being normally distributed with median

and variance ; see for example

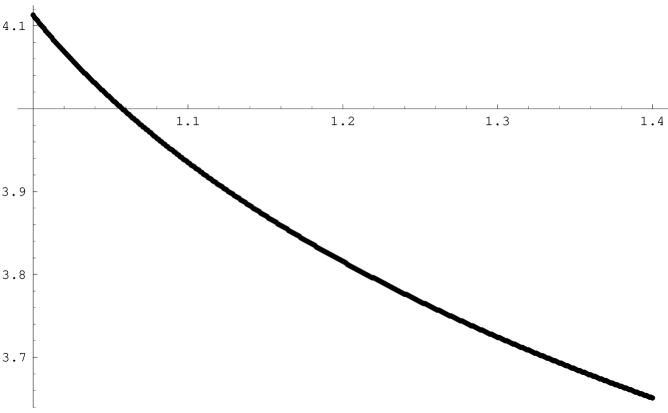

Theorem 8.17 of [MM]). For close to 1 we see in Figure

1 that the median of

is strictly decreasing with increasing ,

Figure 1. Plot of the median

of as a function of

().

which implies that there is an inverse function such that

. We obtain an estimator to

by applying to the sample median. This estimator is a consistent

estimator (as the sample size tends to infinity it will tend to

) and should be asymptotically unbiased.

The proof of the Cramér-Rao inequality starts with

(3.6)

where is an

unbiased estimator of depending only on the sample values

. In our case (when each ) we may not have an unbiased estimator. If we denote

this expectation by , for our investigations

all that we require is that is finite

(which is easy to show). Going through the proof of the

Cramér-Rao inequality shows that the effect of this is to

replace the factor of in (1.2) with ; thus the generalization of the

Cramér-Rao inequality for our estimator is

(3.7)

As our variance is infinite for

we see that, no matter what ‘nice’ estimator we use, we

will not obtain any useful information from such arguments.

Appendix A Applying the Dominated Convergence

Theorem

We justify applying the Dominated Convergence Theorem in the proof

of Lemma 2.1. See, for example, [SS] for the

conditions and a proof of the Dominated Convergence Theorem.

Lemma A.1.

For each fixed and any , we have

(A.1)

and is positive and integrable, and dominates each

.

Proof.

We first prove (A.1). As and ,

note . Consider the case of . Since

, we have

(A.2)

We

are left with the case of , or . We have

(A.3)

This, combined with and yields

(A.4)

It is clear that is positive and

integrable, and by L’Hospital’s rule (see (2.9)) we

have that

(A.5)

Thus the

Dominated Convergence Theorem implies that