Explicit Solutions of Optimal Consumption, Investment and Insurance Problems with Regime Switching

Abstract

We consider an investor who wants to select her/his optimal consumption, investment and insurance policies.

Motivated by new insurance products, we allow not only the financial market but also the insurable loss to

depend on the regime of the economy.

The objective of the investor is to maximize her/his expected total discounted utility of

consumption over an infinite time horizon.

For the case of hyperbolic absolute risk aversion (HARA) utility functions, we obtain

the first explicit solutions for

simultaneous

optimal consumption, investment, and insurance problems when there is regime switching.

We determine that the optimal insurance contract is either no-insurance

or deductible insurance, and calculate when it is optimal to buy insurance.

The optimal policy depends strongly on the regime of the economy.

Through an economic analysis, we calculate the advantage of buying insurance.

JEL classification: C61, E32, E44, G11, G22.

keywords:

Economic analysis; Hamilton-Jacobi-Bellman equation; Insurance; Regime switching; Utility maximization.1 Introduction

In the classical consumption and investment problem, a risk-averse investor wants to maximize her/his expected discounted utility of consumption by selecting optimal consumption and investment strategies. Merton (1969) was the first to obtain explicit solutions to this problem in continuous time. Many generalizations to Merton’s work can be found in Karatzas (1996), Karatzas and Shreve (1998), Sethi (1997), et cétera. In the traditional models for consumption and investment problems, there is only one source of risk that comes from the uncertainty of the stock prices. But in real life, apart from the risk exposure in the financial market, investors often face other random risks, such as property-liability risk and credit default risk. Thus, it is more realistic and practical to extend the traditional models by incorporating an insurable risk. When an investor is subject to an additional insurable risk, buying insurance is a trade-off decision. On one hand, insurance can provide the investor with compensation and then offset capital losses if the specified risk events occur. On the other hand, the cost of insurance diminishes the investor’s ability to consume and therefore reduces the investor’s expected utility of consumption.

The initial optimal insurance problem studies an individual who is subject to an insurable risk and seeks the optimal amount of insurance under the utility maximization criterion. Using the expected value principle for premium, Arrow (1963) found the optimal insurance is deductible insurance in discrete time. Promislov and Young (2005) reviewed optimal insurance problems (without investment and consumption). They proposed a general market model and obtained explicit solutions to optimal insurance problems under different premium principles, such as variance principle, equivalent utility principle, Wang’s principle, et cétera.

Moore and Young (2006) combined Merton’s optimal consumption and investment problem and Arrow’s optimal insurance problem in continuous time. They found explicit or numerical solutions for different utility functions (although they did not verify rigourously that the obtained strategies were indeed optimal). Perera (2010) revisited Moore and Young’s work by considering their problem in a more general Levy market, and applied the martingale approach to obtain explicit optimal strategies for exponential utility functions. Pirvu and Zhang (2012) considered the insurable risk to be mortality risk and studied optimal investment, consumption and life insurance problems in a financial market in which the stock price followed a mean-reverting process.

In traditional financial modeling, the market parameters, like the risk-free interest rate, stock returns and volatility, are assumed to be independent of general macroeconomic conditions. However, historical data and empirical research show that the market behavior is affected by long-term economic factors, which may change dramatically as time evolves. Regime switching models use a continuous-time Markov chain with a finite-state space to represent the uncertainty of those long-term economic factors.

Hamilton (1989) introduced a regime switching model for the first time to capture the movements of the stock prices and showed that the regime switching model represents the stock returns better than the model with deterministic coefficients. Thereafter, regime switching has been applied to model many financial and economic problems. In regard to optimal portfolio selection problems, Zhou and Yin (2004) considered a financial market with regime switching and studied the problem under the Markowitz’s mean-variance criterion. Sotomayor and Cadenillas (2009) considered the problem under the expected utility of consumption maximization criterion, and obtained explicit solutions for HARA utility functions.

In the insurance market, insurance policies can depend on the regime of the economy. In the case of traditional insurance, the underwriting cycle has been well documented in the literature. Indeed, empirical research provides evidence for the dependence of insurance policies’ underwriting performance on external economic conditions (see for instance Grace and Hotchkiss (1995), Haley (1993) on property-liability insurance, and Chung and Weiss (2004) on reinsurance). In the case of non-traditional insurance, by investigating the comovements of credit default swap (CDS) and the bond/stock markets, Norden and Weber (2007) found that CDS spreads are negatively correlated with the price movements of the underlying stocks and such cointegration is affected by the corporate bond volume.

In this paper, we use an observable continuous-time finite-state Markov chain to model the regime of the economy, and allow both the financial market and the insurance market to depend on the regime. Our objective is to obtain simultaneously optimal consumption, investment and insurance policies for a risk-averse investor who wants to maximize her/his expected total discounted utility of consumption over an infinite time horizon. We extend Sotomayor and Cadenillas (2009) by including a random loss in the model and an insurance policy in the control. The most important difference between the model of Moore and Young (2006) and our paper is that they do not allow regime switching, while we allow regime switching in both the financial market and the insurance market.

This paper is organized as follows. In Section 2, we discribe the problem. The verification theorems are presented in Section 3. In Section 4, we obtain explicit solutions for four HARA utility functions. In Section 5, we conduct an economic analysis to investigate the impact of various factors on the optimal policy and calculate the advantage of buying insurance. Section 6 concludes our study.

2 The Model

Consider a complete probability space in which a standard Brownian motion and an observable continuous-time, stationary, finite-state Markov chain are defined. Denote by the state space of this Markov chain, where is the number of regimes in the economy. The matrix denotes the strongly irreducible generator of , where , , when and .

We consider a financial market consisting of two assets, a bond with price (riskless asset) and a stock with price (risky asset), respectively. Their prices processes are driven by the following dynamics:

with initial conditions and . The coefficients , and , , are all positive constants.

An investor chooses , the proportion of wealth invested in the stock, and a consumption rate process . We assume the investor is subject to an insurable loss , where denotes the investor’s wealth at time . We shall use the short notation to replace if there is no confusion. We use a Poisson process with intensity , where for every , to model the occurrence of this insurable loss. In the insurance market, there are insurance policies available to insure against the loss . We further assume the investor can control the payout amount , where and , or in short, . For example, if , then at time the investor suffers a loss of amount but receives a compensation of amount from the insurance policy, so the investor’s net loss is . Following the premium setting used in Moore and Young (2006) (the famous expected value principle), we assume investors pay premium continuously at the rate given by

where the positive constant , is known as the loading factor in the insurance industry. Such extra positive loading comes from insurance companies’ administrative cost, tax, profit, et cétera.

Following Sotomayor and Cadenillas (2009), we assume the Brownian motion , the Poisson process and the Markov chain are mutually independent. We also assume that the loss process is independent of . We take the augmented filtration generated by , , and as our filtration and define .

For an investor with triplet strategies , the associated wealth process is given by

| (1) |

with initial conditions and .

We define the criterion function as

| (2) |

where is the discount rate and means conditional expectation given and . We assume that for every , the utility function is , strictly increasing and concave, and satisfies the linear growth condition

Besides, we use the notation , .

We define the bankruptcy time as

Since an investor can consume only when her/his wealth is strictly positive, we define

A control is called admissible if is predictable with respect to the filtration and satisfies,

and

We use to denote the set of all admissible controls with initial conditions and . Then we formulate our optimization problem as follows.

Problem 2.1

Select an admissible control that maximizes the criterion function . In addition, find the value function

The control is called an optimal control or an optimal policy.

Moore and Young (2006) also incorporated an insurable risk into the consumption and investment framework. However, they did not consider a regime switching model, or equivalently they assumed that there is only one regime in the economy. Nevertheless, the insurable risk and the coefficients of the financial market most likely depend on the regime of the economy. Hence, in the above regime switching model, we assume that the insurance market (insurable loss and insurance performance) and the financial market are regime dependent. Furthermore, we assume these two markets depend on the same regime. We mention three examples below. First, the assumption that the financial market and the insurance market depend on the same regime is supported by the bailout case of AIG (see Sjostrom (2009) for details) and the financial derivatives in the insurance industry. Before the crash of the U.S. housing market in 2007, many investors, banks and financial institutions bought obligations constructed from mortgage payments or made loans to the housing agencies. To insure against the credit risk that the obligations or loans may default, they purchased credit default swap (CDS) contracts from insurance companies like AIG. In a CDS contract, the buyer makes periodic payments to the seller, and in return, receives the par value of the underlying obligation or loan in the event of a default. Apparently, the credit default risk insured by CDS contracts is negatively correlated with the reference entity’s stock performance (see Norden and Weber (2007) for empirical evidence). Second, generated by the financial engineering on derivatives, insurance companies have created numerous equity-linked products, such as equity-linked life insurance (see Hardy (2003) for more details on such insurance policy). If the insured of an equity-linked life insurance policy survivals to the expiration, then the beneficiary receives investment benefit that depends upon the market value of the reference equity. Hence, equity-linked life insurance and its reference equity are affected by the same long-term economic factors. Third, even in traditional insurance products like property-liability insurance, there is empirical evidence (see for instance Grace and Hotchkiss (1995)) that the loading factor depends on the regime of the economy. Indeed, in those traditional insurance products, and might be independent of but depends on .

3 Verification Theorems

Let be a function with . We define the operator by

where and .

Theorem 3.1

Suppose is finite, . Let be an increasing and concave function such that for every . If satisfies the Hamilton-Jacobi-Bellman equation

| (3) |

for every , and the control defined by

is admissible, then is optimal control to Problem 2.1. In addition, the value function is given by

where .

Furthermore, if the utility function does not depend on the regime, namely , for every , then the value function .

Proof 1

, consider . By applying Ito’s formula for Markov-modulated processes (see, for instance, Sotomayor and Cadenillas (2009)), we get

| (4) |

where is a martingale with .

Let and define a stopping time . Then by replacing by in (1), taking conditional expectation and applying the HJB equation (3.1), we obtain

Let , and . Then . Since is continuous, we obtain

Hence,

| (5) |

Define . Applying Ito’s formula to yields

where is a square-integrable martingale with .

Taking conditional expectation and applying the monotone convergence theorem to the above equality, we get

and then

If the utility function does not depend on the regime, then , and so .

is an increasing function for every , so if is not finite, then . The following theorem deals with the case when , .

Theorem 3.2

Suppose for every . Let be an increasing and concave function such that for every . If satisfies the Hamilton-Jacobi-Bellman equation

| (6) |

for every , and the control defined by

is admissible, then is an optimal control to Problem 2.1 and the value function is .

Proof 2

Define . For any admissible control , by following a similar argument as in Theorem 3.1, we obtain

is well defined and finite, because is an admissible control and satisfies the linear growth condition. Then the above inequality becomes

By assumption, is increasing in and for every , so

By letting , and , and applying the monotone convergence theorem, we obtain

and the equality holds when .

4 Explicit Solutions of Value Function and Optimal Strategies

In this section, we obtain explicit solutions to optimal consumption, investment and insurance problem when there is regime switching in the economy. We assume the utility function is of HARA type and the insurable loss is proportional to the investor’s wealth, . Here for every , measures the intensity of the insurable loss in regime , and for every , denotes the loss proportion at time . We assume that is measurable and for all .

To obtain optimal policy, we first construct a candidate policy at time , which is a function of , namely, , and (In fact, we find and are independent of ). The candidate policy is indeed optimal once we can prove it is an admissible policy.

We conjecture that is strictly increasing and concave for every . Then a candidate for is given by

| (9) |

Since is strictly decreasing, the inverse of exists. Then a candidate for is given by

| (10) |

For the optimal insurance, we have the following Lemma and Theorem.

Lemma 4.1

, denote , where constant . We denote the optimal insurance policy by . Then we have

-

(a) if and only if

-

(b) if and only if

Proof 3

, we use the notation . We then break the proof into four steps.

Step 1: We want to show that , .

Assume to the contrary that such that . Consider , where and when and otherwise, . Here we choose small and to ensure that . Let

Since is the maximizer of , we have

Using Taylor expansion and letting , we get

Letting () and applying the mean value theorem of integrals, we obtain

which is a contradiction since and , .

Step 2: We want to show that .

To this purpose, we consider . For small enough and , we have . Then a similar argument as above gives the desired result

Step 3: We want to show that .

In this step, we consider and . From the results in Step 1 and Step 2, we obtain and at the same time, and thus the equality is achieved.

Step 4: We want to show that .

We assume to the contrary that . Then the results above give , which is a contradiction to the given condition. A similar method also applies to the proof of .

Theorem 4.3

The optimal insurance is either no insurance or deductible insurance (almost surely).

-

(a) The optimal insurance is no insurance , when

(11) -

(b) The optimal insurance is deductible insurance , , when there exists satisfying

(12)

Proof 4

We complete the proof in three steps.

Step 1: We want to prove Case (a).

Assume there exists such that . Then according to (b) in Lemma 4.1, we have . Define the set (we have ). If (on the set ), then , which is a contradiction to the given condition. Therefore on the set .

Besides, if two policies and only differ on a negligible set, we have , because the integration of a bounded function on a negligible set is zero.

Step 2: We want to prove Case (b).

We notice that is a strictly decreasing function, so if such exists, it must be unique. We then break our discussion into two disjoint scenarios.

(i)

(ii)

In this scenario, we have since . Then the result in Lemma 4.1 shall give

Due to the monotonicity of , we must have

If condition (11) fails, then

where . Since is continuous and strictly decreasing in , there must exist a unique such that

If (12) has no solution in , then

Therefore, we conclude that the optimal insurance is either no insurance or deductible insurance.

Remark 4.1

The optimal insurance also satisfies the usual properties: and is an increasing function of the loss.

To find explicit solutions to the optimal consumption, investment and insurance problem, we consider four utility functions of HARA class. The first three utility functions do not depend on the market regimes:

-

1.

,

-

2.

,

-

3.

.

The fourth utility function depends on the regime of the economy and we assume there are two regimes in the economy ().

-

4.

All these four utility functions are , strictly increasing and concave, and satisfy the linear growth condition. To be specific, we can take for the first three utility functions and for the last one.

4.1

In this case, a solution to the HJB equation (4) is given by

| (13) |

where the constants , , will be determined below.

Solving gives . Then by Theorem 4.3,

Let , , , , and be the identity matrix. Then the constant vector satisfies the linear system

| (14) |

Proposition 4.1

Proof 5

The function defined above is a smooth function which is strictly increasing and concave such that , for every . By the construction of the vector , satisfies the HJB equation (4).

To show that the candidate policy is admissible, we consider an upper bound process of

with initial value .

Solving the above SDE gives

By the definition of , we have , . Notice that if for , then

So is a linear combination of independent Brownian motions. By the exponential martingale property of a Brownian motion, we have

For the candidate of optimal investment proportion ,

where .

Since , for the candidate of optimal consumption ,

where .

For the candidate of optimal insurance , -measurable random variable , , so .

Furthermore, we have

where .

Example 4.1

In this example, we assume there are two regimes in the economy, where regime 1 represents a bull market and regime 2 represents a bear market. According to French et al. (1987), the stock returns are higher in a bull market, so . Hamilton and Lin (1996) found stock volatility is higher in a bear market, thus . The data of overnight financing rate and treasury bill rate (see, for instance, the statistical data from Bank of Canada) suggests the risk-free interest rate is higher in good economy, hence . Haley (1993) found the underwriting margin is negatively correlated with the interest rate, which implies the loading factor is smaller in a bull market, . Norden and Weber (2007) observed that CDS spreads (default risk) are negatively correlated with the stock prices. Equivalently, the default risk is higher in a bear market, that is, .

The generator matrix entries become

with , so the linear system (14) becomes

which gives a unique solution

where and .

From the above expression of , we notice that only is not directly given by the market. To calculate , we assume the loss proportion does not depend on time and we discuss the cases that is constant or uniformly distributed on . We further assume . If the opposite is true, then we switch the expressions when calculating and .

-

1.

is constant.

If , thenOtherwise, we obtain

-

2.

is uniformly distributed on .

If , thenOtherwise, through straightforward calculus, we obtain

Hence,

4.2

In this scenario, a solution to the HJB equation (4) is given by

| (15) |

where the constants , , will be determined below.

From , and , we obtain

Solving gives , where . Then

By plugging the candidate policy into the HJB equation (4), we find the constants should satisfy the following non-linear system

| (16) |

where .

In order to guarantee the above non-linear system has a unique positive solution, we need the following technical condition

| (17) |

Lemma 4.2

Proof 6

See Lemma 4.1 in Sotomayor and Cadenillas (2009).

Proposition 4.2

Proof 7

To verify that the candidate policy is admissible, we consider an upper bound process of with the dynamics

Given , we can solve the above SDE to obtain

We use this upper bound process to verify that the conditions for an admissible control are satisfied. We have for every that

where and .

Besides, we can verify that since , for every -measurable random variable .

Therefore, defined above is admissible and then is optimal policy of Problem 2.1. By definition, smooth function is strictly increasing and concave, and satisfies , . From the construction of , the HJB equation (4) holds for all . Therefore, according to Theorem 3.2, is the value function of Problem 2.1.

Example 4.2

To solve the non-linear system (16), we need to find first. In this example, we show how to find when is constant or is uniformly distributed on . Without loss of generality, we assume . If the opposite holds, we switch the formulas for and . The results will be used for economic analysis in the next section.

-

1.

is constant.

If , thenOtherwise, we obtain

-

2.

is uniformly distributed on .

If , thenOtherwise, we obtain

and when ,

and when ,

Therefore, if , and , then

and if , and , then

4.3

In this case, a solution to the HJB equation (4) has the form

| (18) |

where the constants , , will be determined below.

Then we can find the candidate for and as

From , we can solve to obtain with . By Theorem 4.3, we have

We need to impose an extra requirement for

| (20) |

Lemma 4.3

Proof 8

See Lemma 4.2 in Sotomayor and Cadenillas (2009).

Proposition 4.3

Proof 9

We use the same upper bound process defined in Section 4.2. By following a similar argument as in the previous proposition, we can easily verify , and , .

By definition, is strictly increasing and concave, and satisfies for all . By the construction of constants , the HJB equation (4) holds for all .

4.4

In this case, a solution to the HJB equation (4) is given by

| (21) |

where the constants , will be determined below.

From , and , we obtain the candidate for and

Solving gives where . Thus a candidate for optimal insurance is

Since , so we have with . Thus we can rewrite the above system as

| (22) |

where .

Lemma 4.4

The non-linear system (22) has a real solution , , if .

Proof 10

The non-linear system (22) is equivalent to

Solving this system for gives

The discriminant of the above quadratic equation is

Since , we have , and then , which implies has a real solution. Besides, , so . Similar analysis also applies to .

Proposition 4.4

Proof 11

We consider an upper bound process of to verify that the candidate policy is admissible. The dynamics of is given by

with initial condition .

The solution to the above SDE is

Since , , we have

where , and .

Furthermore, we calculate

where (Notice due to the assumption that , ).

Besides, ,

and , for every -measurable random variable .

5 Economic Analysis

In this section, we analyze the impact of market parameters and the investor’s risk aversion on optimal policy, and how insurance affects the expected total discounted utility of consumption (the value function). To conduct the economic analysis, we assume there are two regimes in the economy, like in Example 4.1, Example 4.2, and Example 4.3: regime 1 represents a bull market while regime 2 represents a bear market. We only consider the first three utility functions in the economic analysis.

5.1 Impact of market parameters and risk aversion on optimal policy

According to the results obtained in Section 4, we write the optimal proportion invested in the stock in an uniform expression

| (23) |

where when .

During any given regime, the optimal investment proportion in the stock is constant, and only depends on market parameters (expected excess return over variance) and the investor’s risk aversion parameter .

The dependency of on market parameters is evident. Through empirical research, French et al. (1987) find that the expected excess return over variance is higher in good economy. Therefore, in a bull market, investors should invest a greater proportion of their wealth on the stock.

Expression (23) shows that is inversely proportional to the relative risk aversion , so low risk-averse investors (with greater ) will invest a higher proportion of their wealth on the stock.

For all three cases, the optimal consumption rate process is proportional to the wealth process and such ratio is given by

Since is positive in all three cases, investors will consume proportionally more when they become wealthier. To examine the dependency of the optimal consumption to wealth ratio on , we separate our discussion into the following three cases.

For moderate risk-averse investors (), is constant regardless of the market regimes, so moderate risk-averse investors consume the same proportion of their wealth in both bull and bear markets.

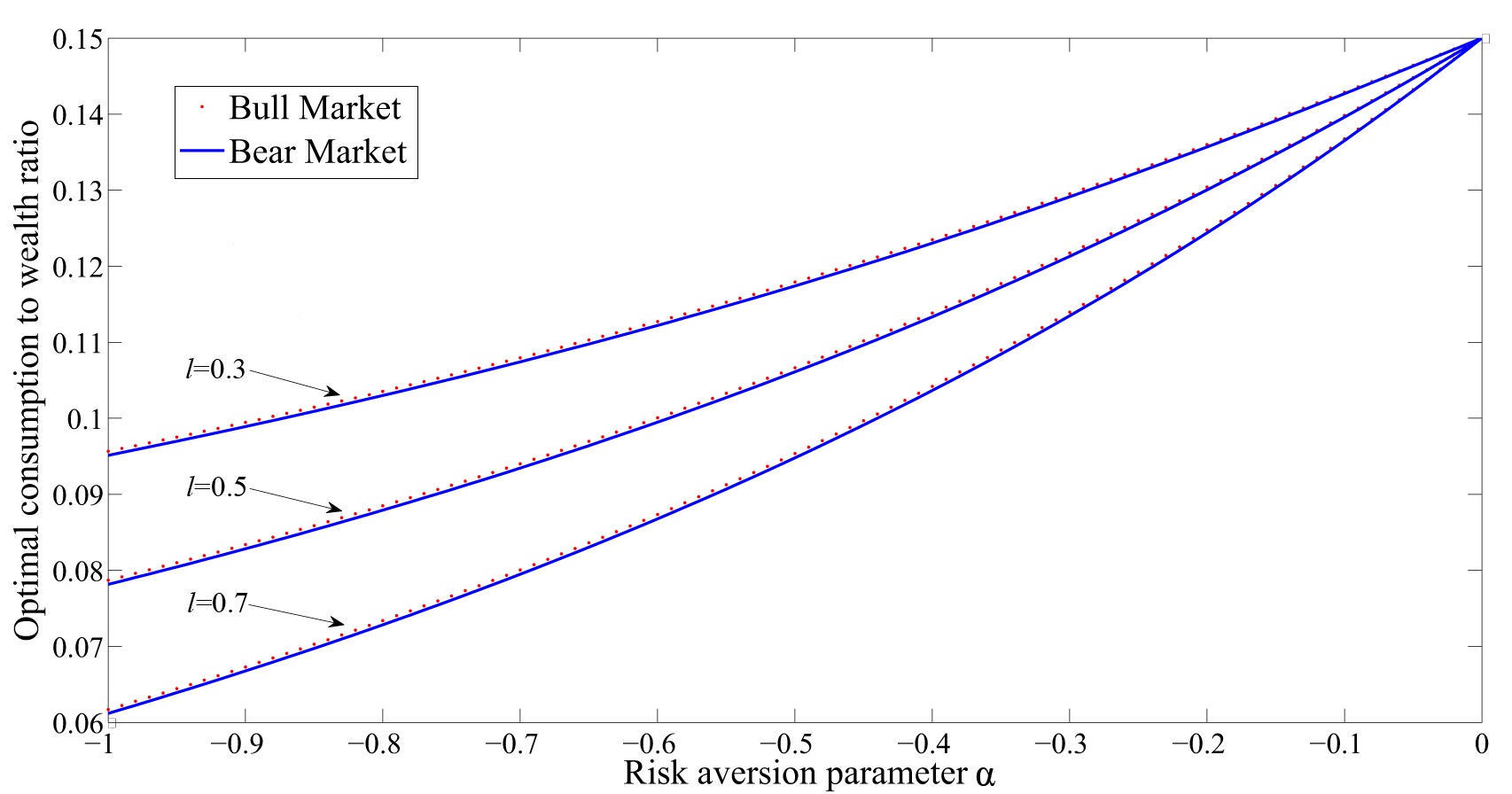

For high risk-averse investors (), their optimal consumption to wealth ratio is given by , where can be obtained from the system (16). To find a numerical solution to the system (16), we set market parameters as , and (for the convenience of citation thereafter, we denote the choice of market parameters here as Parameter Set I). Notice that these parameters satisfy the technical condition (17). We draw graphs in Figure 1 for the optimal consumption to wealth ratio when and , , and . We see that the optimal consumption to wealth ratio is an increasing function of . Thus, the higher the risk tolerance, the higher the proportion of consumption over wealth. For the above parameter values, we find , which can be seen from Figure 1.

Hence investors should allocate a higher proportion of their wealth to consumption in a bull market. For any chosen investor (fixed ), she/he will behave more conservatively by reducing the proportion spent in consumption when facing larger losses (greater ). This behavior was not noticed in Sotomayor and Cadenillas (2009), because they did not incorporate an insurable loss in their model. Besides, from a mathematical point of view, the ratios all converge to when approaches , which is exactly the same optimal consumption to wealth ratio when ().

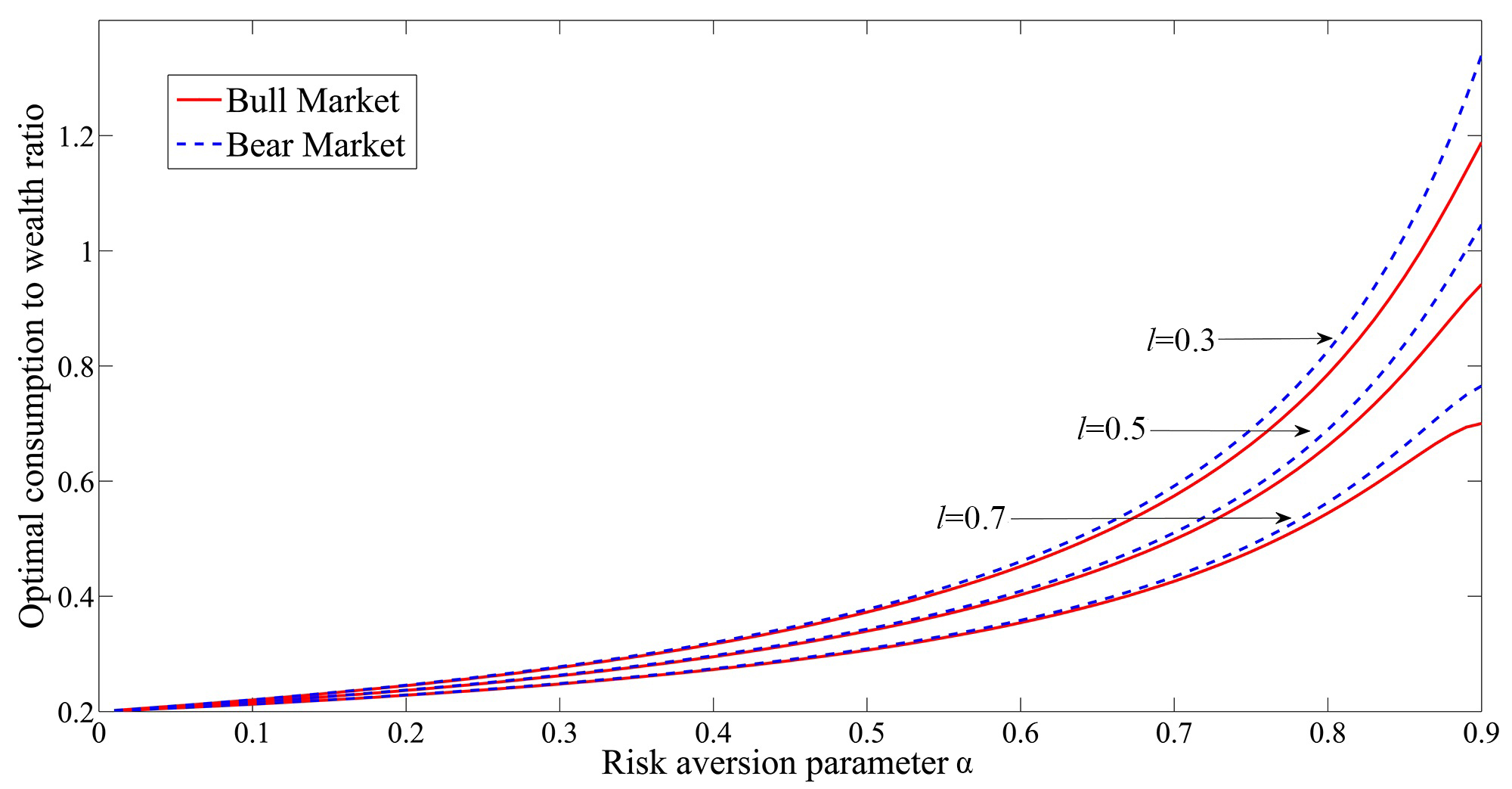

For low risk-averse investors (), the optimal consumption to wealth ratio is given by where can be calculated from the system (19). We set market parameters to be , and (denoted as Parameter Set II). For these parameters values, the corresponding technical condition (20) is satisfied.

Figure 2 shows that the optimal consumption to wealth ratio when , , and . Similar to the previous case, we also observe that the optimal consumption to wealth ratio is an increasing function of . However, contrary to the previous case, we have when . This means low risk-averse investors () spend a smaller proportion of their wealth on consumption in a bull market. We notice that for very low risk-averse investors ( close to 1), the optimal consumption to wealth ratio is even greater than 1, meaning they finance consumption by borrowing.

By comparing all three cases, we conclude that investors with high risk tolerance ( is large) consume at large proportion of their wealth in every market regime. However, investors’ consumption decision depends on the market regimes, and investors with different risk aversion attitudes behave differently in bull and bear markets.

The optimal insurance for all three utility functions is deductible insurance, and is given by

We observe that, for each fixed regime, the optimal insurance is proportional to the investor’s wealth . We note that it is optimal to buy insurance if and only if , or equivalently if and only if

| (24) |

Thus, it is optimal to buy insurance if and only if, relative to the other variables, is large, is large, is small, and is small (we recall that ). That is, it is optimal to buy insurance if the insurable loss is large, the cost of insurance is low, and the investor is very risk averse. It is surprising that the variable does not appear explicitly in this expression. Our explanation is that is implicitly incorporated in , so is important as well to determine the optimal insurance.

If it is optimal to buy insurance, or equivalently, the condition (24) is satisfied, then Thus, as expected, the optimal insurance is proportional to and . Furthermore,

Hence, the optimal insurance is a decreasing and convex function of . The decreasing property means that, as the premium loading increases, it is optimal to reduce the purchase of insurance. The convexity indicates the amount of reduction in insurance decreases as the premium loading rises.

In addition, if it is optimal to buy insurance (when condition (24) is satisfied), then

Hence, the optimal insurance is a decreasing function of , which implies the higher the risk tolerance, the smaller amount spent on insurance. We observe and have the same sign. Recall that is the premium loading, which usually does not exceed . So when , we have . This indicates that for high and moderate risk-averse investors (), the reduction in insurance is more significant when is greater. If , we find that when and when , where . So for low risk-averse investors (), the magnitude of reduction in insurance depends on the risk aversion attitude.

5.2 Impact of insurance on value function

In this subsection, we want to calculate the advantage of buying insurance for investors when facing a random insurable risk. To achieve this objective, we first assume some investors cannot access the insurance market. We then calculate the value function with the constraint of no insurance, denoted by , and compare with (the value function of the unconstrained Problem 2.1).

Under the constraint of no insurance, the dynamics of the wealth process is given by

Here the insurable loss .

We then formulate the constrained problem as follows.

Problem 5.1

Select an admissible policy that maximizes the criterion function , defined by (2). In addition, find the value function

For every , and need to satisfy all the conditions that and satisfy, where . Since for any , we have . Therefore, for all and .

We provide a verification theorem to Problem 5.1 when the utility function does not depend on the regime (see Theorems 3.1 and 3.2 for proofs), that is, for every .

Theorem 5.4

Suppose or . Let be an increasing and concave function such that for every . If satisfies the Hamilton-Jacobi-Bellman equation

| (25) |

where the operator is defined as

and the control defined by

is admissible, then is optimal control to Problem 5.1.

5.2.1

Under the logarithmic utility, we find the value function to Problem 5.1 is given by

where the constants satisfy the following linear system

| (26) |

with defined by .

To compare the value functions and , we assume there are two regimes () in the economy. Under this assumption, we find given by

where and .

We then calculate

| (27) |

where and .

To facilitate our scenario analysis, we assume and is either constant or uniformly distributed on .

-

1.

Case 1: is constant.

In this case, , .

(i) Optimal insurance is no insurance for both regimes.

From Example 4.1, we notice when the optimal insurance is no insurance, we have , . Then, we obtain for both regimes. Hence for all and .

(ii) Optimal insurance is strictly positive in at least one regime.

When the optimal insurance is strictly positive in at least one regime, we must have at least one in the form of . Without loss of generality, we assume in regime 1, or equivalently, . Then we obtain

where the second inequality comes from . Consider . We have and

This implies for all , and then . Together with the result above, we can claim that . Hence, regardless of the optimal insurance in regime 2, we have for both regimes according to (27). Even when , buying insurance in regime 1 increases the value function in regime 2, which is a surprising result.

To further study the advantage of buying insurance, we define the increase ratio of the value function by

where and are the value functions to Problem 2.1 and Problem 5.1, respectively.

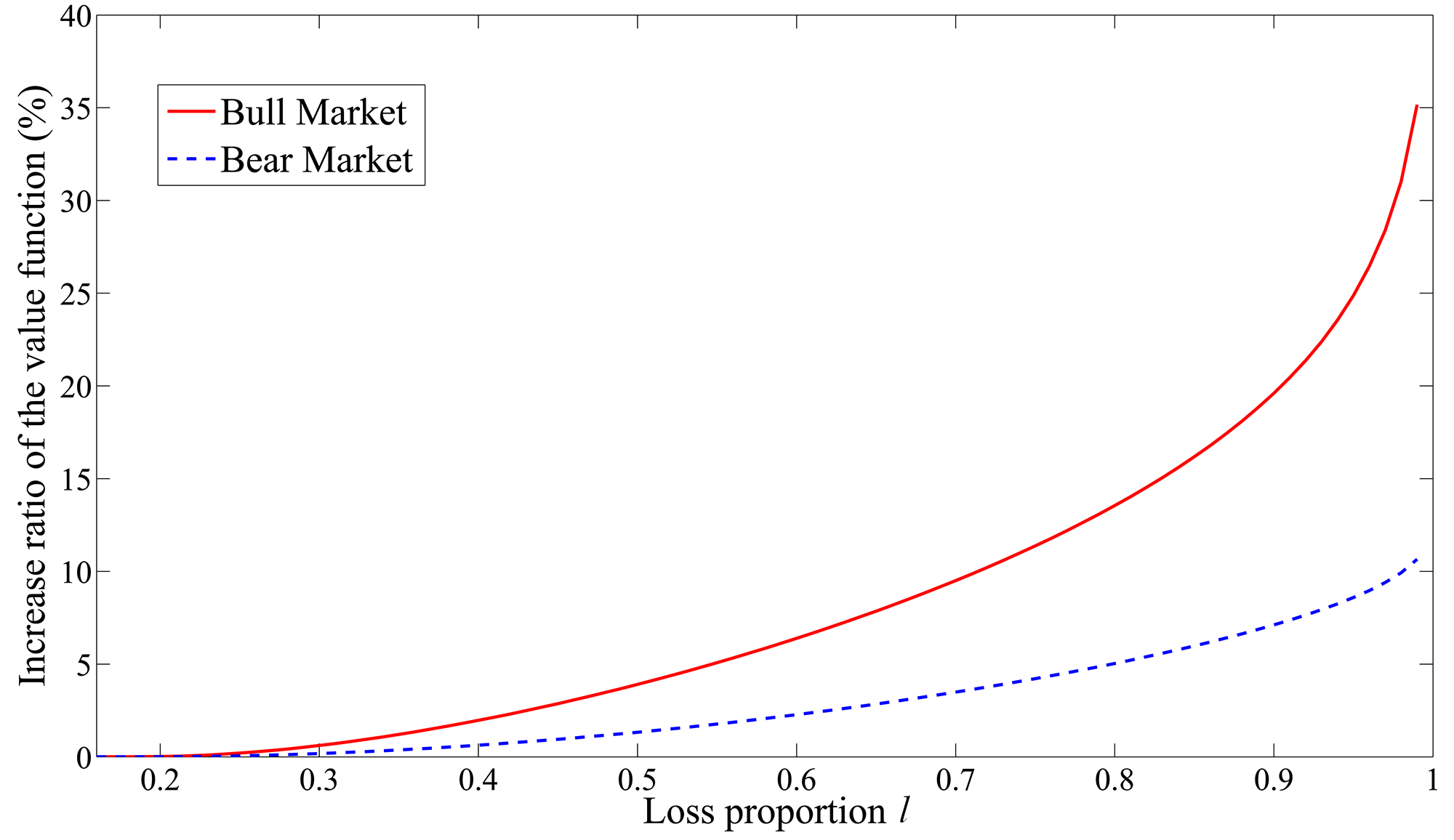

Without loss of generality, we assume (such assumption makes the constant be ). Hence, we have and , . Then we obtain for

To analyze the impact of the insurable loss on the ratio , we keep as a variable and choose Parameter Set I but . Notice that for the chosen parameters, our assumption is satisfied

Since we assume in regime , . We draw the graph of the increase ratio of the value function in Figure 3.

Figure 3: Increase ratio of the value function when loss proportion is constant As expected, the advantage of buying insurance increases when the insurable loss becomes larger in both regimes. But surprisingly, we find that buying insurance benefits investors more in a bull market, especially when the insurable loss is large.

-

2.

Case 2. is uniformly distributed on .

In this case, , .(i) Optimal insurance is no insurance for both regimes.

In this scenario, it is obvious that and then , for all and .

(ii) Optimal insurance is strictly positive in at least one regime.

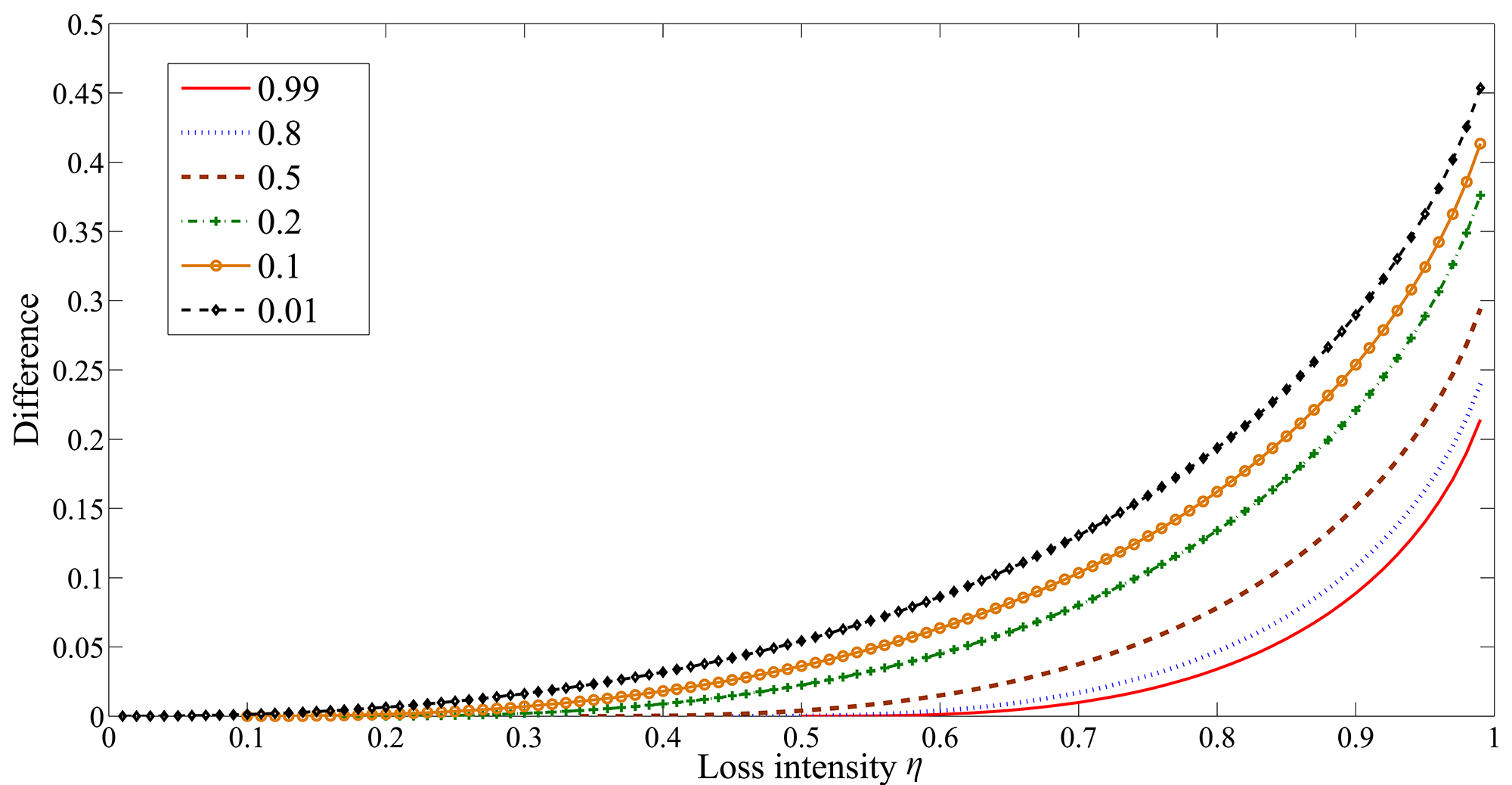

Again we assume in regime 1. Then we have

Here depends on the premium loading and loss intensity in regime 1. To investigate such dependency, we conduct a numerical calculation. Notice that must satisfy the condition . We draw the difference in Figure 4 when .

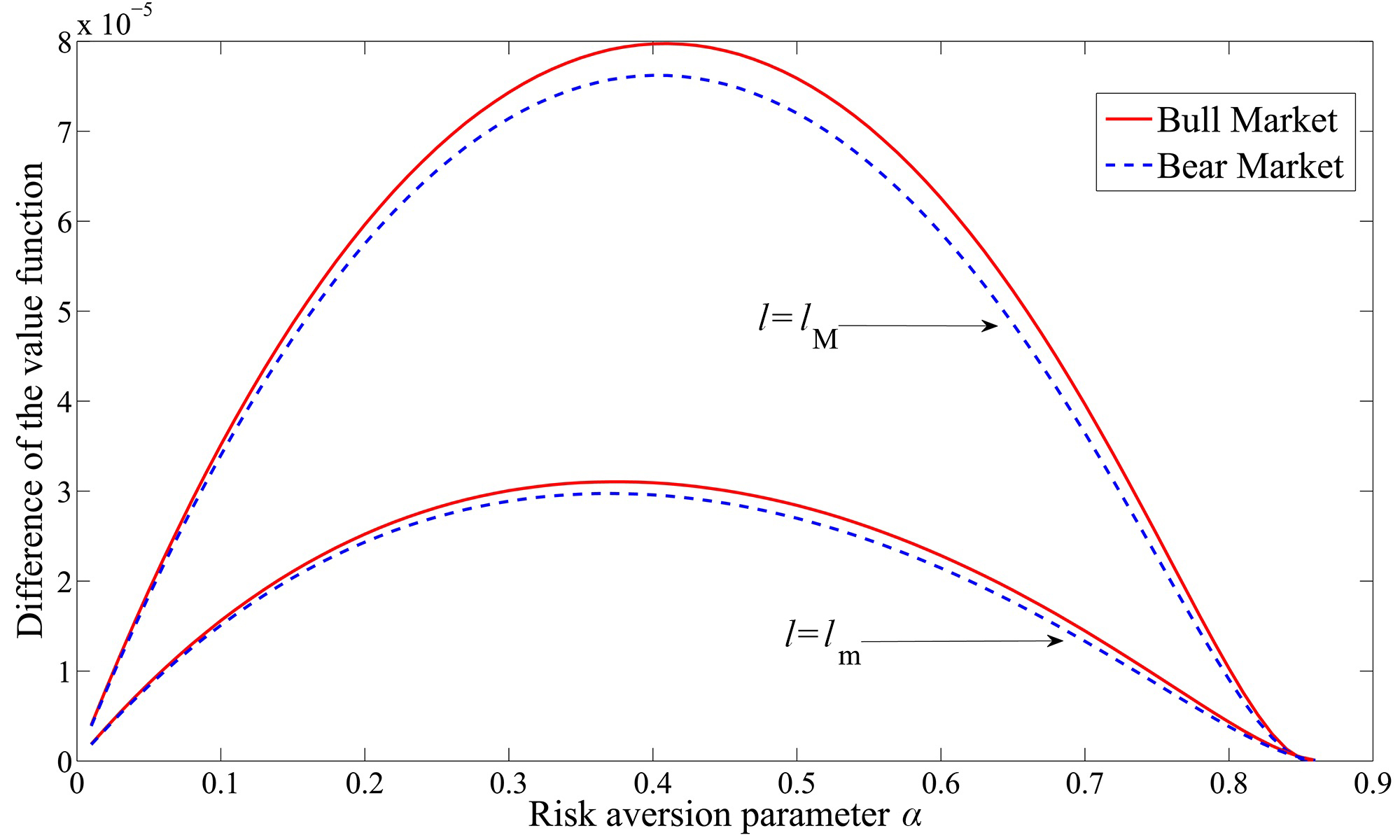

Figure 4: We observe that is strictly positive and therefore for both regimes, which is consistent with our findings in the previous case. Furthermore, as increases (which means the cost of insurance policy increases), the difference of becomes smaller, so the benefit of purchasing insurance policy decreases accordingly. Investors gain more advantage from insurance when the insurable loss becomes larger (that is, the loss intensity increases).

5.2.2

Comparing with the value function we found in Section 4.2, we have .

We assume there are two regimes in the economy and the loss proportion is constant. We skip the trivial case of , in which in both regimes. We then carry out a numerical calculation to study the non-trivial case, that is in at least one regime.

To solve the systems (16) and (28) numerically, we choose Parameter Set I but . For the chosen parameters, it is more reasonable to consider the case when (Since both and are small). In Table 1 we calculate for various values of (when calculating , we take ).

| -0.01 | |||

|---|---|---|---|

| 0.0041 | 0.0039 | ||

| 0.0015 | 0.0015 | ||

| -0.5 | 0.0797 | 0.0781 | |

| 0.3010 | 0.2961 | ||

| -1 | 0.8116 | 0.8036 | |

| 2.6969 | 2.6841 | ||

| 0.2454 | 0.2441 | ||

| -2 | 0.9421 | 0.9381 | |

| 2.2418 | 2.2344 |

The result clearly confirms that in both regimes. We also observe that the advantage of buying insurance is greater for investors with higher risk aversion. The size of the insurable loss affects the advantage of buying insurance as well. When the insurable loss increases (loss proportion increases), buying insurance will give investors more advantage. We obtain , meaning buying insurance is more advantageous in a bull market.

5.2.3

We find the corresponding value function to Problem 5.1 given by

where the constants satisfy the system (28) with .

From the discussion in Section 4.3, we obtain . We then follow all the assumptions made in Section 5.2.2 including and conduct a numerical analysis by choosing Parameter Set II. In this numerical example, we have when , , when , and when . We consider the first scenario: since it includes most low risk-averse investors. We are interested in the case of in at least one regime. For the chosen parameters, we find is so small that the case of is rare. So we further assume constant loss proportion . Notice that when , we have but .

From solving the non-linear systems (19) and (28), we draw for and in Figure 5. It is obvious that in both regimes. As have seen in the previous cases, the benefit of buying insurance in a bull market strictly outperforms that in a bear market. We also observe a surprising result that the difference of the value functions (advantage of buying insurance) is not an increasing function of , which is different from the result in Section 5.2.2. But the difference is a concave function of .

6 Conclusions

We have considered simultaneous optimal consumption, investment and insurance problems in a regime switching model which enables the regime of the economy to affect not only the financial but also the insurance market. A risk-averse investor facing an insurable risk wants to obtain the optimal consumption, investment and insurance policy that maximizes her/his expected total discounted utility of consumption over an infinite time horizon.

We have presented the first versions of verification theorems for simultaneous optimal consumption, investment and insurance problems when there is regime switching. We have also obtained explicitly the optimal policy and the value function when the utility function belongs to the HARA class.

The optimal proportion of wealth invested in the stock is constant in every regime, and is greater in a bull market regardless of the investor’s risk aversion attitude. We observe that investors with high risk tolerance invest a large proportion of wealth in the stock.

The optimal consumption to wealth ratio is a strictly increasing function of the investor’s risk aversion parameter (). Moderate risk-averse investors () consume at a constant proportion in both regimes. High risk-averse investors () consume a higher proportion of their wealth in a bull market. In contrast, low risk-averse investors () consume proportionally more in a bear market.

The optimal insurance is proportional to the investor’s wealth and such proportion depends on the premium loading and the investor’s risk aversion parameter . As the loading increases, the demand for insurance decreases. This decrease of the demand for insurance is more significant when is small. We observe that investors who are very risk tolerant (that is, investors with large ) spend a small amount of wealth in insurance. For high and moderate risk-averse investors (), the amount of reduction in insurance is greater when is far away from 0. However, low risk-averse investors () reduce the amount of insurance in different magnitudes that depend on the value of .

We have also obtained the conditions under which it is optimal to buy insurance, and analyzed their dependence on the different parameters.

We have calculated the advantage of buying insurance. Based on a comparative analysis, we find the value function to Problem 2.1 is strictly greater than the value function to Problem 5.1 when the optimal insurance is not equal to in all regimes. We also observe that the advantage of buying insurance is greater in a bull market. Investors who face a large random loss, gain more benefits from purchasing insurance.

Acknowledgements

The work of B. Zou and A. Cadenillas was supported by the Natural Science and Engineering Research Council of Canada. The results of this paper were presented at the 2nd Industrial-Academic Workshop on Optimization in Finance and Risk Management, Fields Institute for Research in Mathematical Sciences.

References

- Arrow (1963) Arrow, K.J., 1963. Uncertainty and the welfare economics of medical care. American Economic Review 53, 941-973.

- Chung and Weiss (2004) Chung, J., and Weiss, M., 2004. US reinsurance prices, financial quality, and global capacity. Journal of Risk and Insurance, 71(3), 437-467.

- French et al. (1987) French, K.R., Schwert, G.W., and Stambaugh, R.F., 1987. Expected stock returns and volatility. Journal of Financial Economics 19, 3-29.

- Grace and Hotchkiss (1995) Grace, M.F., and Hotchkiss, J.K., 1995. External impacts on the property-liability insurance cycle. Journal of Risk and Insurance 62(4), 738-754.

- Haley (1993) Haley, J.D., 1993. A cointegration analysis of the relationship between underwriting margins and interest rates: 1930-1989. Journal of Risk and Insurance 60(3), 480-493.

- Hardy (2003) Hardy, M., 2003. Investment Guarantees: Modeling and Risk Management for Equity-Linked Life Insurance. John Wiley & Sons, Inc..

- Hamilton (1989) Hamilton, J.D., 1989. A new approach to the economic analysis of nonstationary time series and the bussiness cycle. Econometrica 57, 357-384.

- Hamilton and Lin (1996) Hamilton, J.D., and Lin, G., 1996. Stock market volatility and the business cycle. Journal of Applied Economitrics 11, 573-593.

- Karatzas (1996) Karatzas, I., 1996. Lectures on the Mathematics of Finance. CRM Monograph Series 8. American Mathematical Society

- Karatzas and Shreve (1998) Karatzas, I., and Shreve, S., 1998. Methods of Mathematical Finance. Springer.

- Merton (1969) Merton, R., 1969. Lifetime portfolio selection under uncertainty: the continuous time case. Review of Economics and Statistics 51, 247-257.

- Moore and Young (2006) Moore, K.S., and Young, V.R., 2006. Optimal insurance in a continuous-time model. Insurance: Mathematics and Economics 39, 47-68.

- Norden and Weber (2007) Norden, L., and Weber, M., 2007. The co-movement of credit default swap, bond and stock markets: an empirical analysis. European Financial Management 15(3), 529-562.

- Perera (2010) Perera, R.S., 2010. Optimal consumption, investment and insurance with insurable risk for an investor in a Levy market. Insurance: Mathematics and Economics 46, 479-484.

- Pirvu and Zhang (2012) Pirvu, T.A., and Zhang, H.Y., 2012. Optimal investment, consumption and life insurance under mean-reverting returns: the complete market solution. Insurance: Mathematics and Economics 51, 303-309.

- Promislov and Young (2005) Promislow, S.D., and Young, V.R., 2005. Unifying framework for optimal insurance. Insurance: Mathematics and Economics 36, 347-364.

- Sethi (1997) Sethi, S.P., 1997. Optimal consumption and investment with bankruptcy. Springer.

- Sjostrom (2009) Sjostrom, W., 2009. The AIG bailout. Washington and Lee Law Review 66, 943-991.

- Sotomayor and Cadenillas (2009) Sotomayor, L.R., and Cadenillas, A., 2009. Explicit solutions of consumption investment problems in financial markets with regime switching. Mathematical Finance 19(2), 251-279.

- Zhou and Yin (2004) Zhou, X.Y., and Yin, G., 2004. Markowitz’s Mean-Variance Portfolio Selection with Regime Switching: A Continuous-Time Model. SIAM Journal on Control and Optimization 42, 1466-1482.