Optimal split of orders across liquidity pools: a stochastic algorithm approach

Abstract

Evolutions of the trading landscape lead to the capability to exchange the same financial instrument on different venues. Because of liquidity issues, the trading firms split large orders across several trading destinations to optimize their execution. To solve this problem we devised two stochastic recursive learning procedures which adjust the proportions of the order to be sent to the different venues, one based on an optimization principle, the other on some reinforcement ideas. Both procedures are investigated from a theoretical point of view: we prove convergence of the optimization algorithm under some light ergodic (or “averaging”) assumption on the input data process. No Markov property is needed. When the inputs are i.i.d. we show that the convergence rate is ruled by a Central Limit Theorem. Finally, the mutual performances of both algorithms are compared on simulated and real data with respect to an “oracle” strategy devised by an ”insider” who a priori knows the executed quantities by every venues.

First Version : 6th October 2009

This Version : March 18, 2024

Keywords

Asset allocation, Stochastic Lagrangian algorithm, reinforcement principle, monotone dynamic system.

2001 AMS classification: 62L20, secondary: 91B32, 62P05

1 Introduction

The trading landscape have seen a large number of evolutions following two regulations: Reg NMS in the US and MiFID in Europe. One of their consequences is the capability to exchange the same financial instrument on different trading venues. New trading destinations appeared to complement the trading capability of primary markets as the NASDAQ and the NYSE in the US, or EURONEXT, the London Stock Exchange and Xetra in Europe. Such alternative venues are called “Electronic Communication Network” (ECN) in the US and Multilateral Trading Facilities (MTF) in Europe. Each trading venue differentiates from the others at any time because of the fees or rebate it demands to trade and the liquidity it offers.

As the concerns about consuming liquidity increased with the financial crisis, trading firms use Smart Order Routers (SOR) as a key element in the process of optimizing their execution of large orders. Such devices are dedicated to split orders across trading destinations as a complement to the temporal slicing coming from the well known balance between the need to trade rapidly (to minimize market risk) and trading slow (to avoid market impact).

If the temporal slicing has been studied since the end of the nineties [1] with recent advances to adapt it to sophisticated investment strategies [19], this kind of spatial slicing (across trading destinations) has been mainly studied by economists from the point of view of its global market efficiency [8] rather than from one investor’s point of view.

The complexity of spreading an order between trading destinations comes from the fact that you never knows the quantity available on the trading venue to execute your order of size during a time interval at your given price. If the fraction of your order that you sent to the liquidity pool is higher than : you will loose time and may loose opportunity to execute in an another pool; on another hand if is lower than : you will loose money if this pool fees are cheap, and an opportunity to execute more quantity here. The only way to optimize such a split on real time is to adjust on the fly the proportions according to the result of your previous executions.

This paper is an in depth analysis of the optimal split of orders. The illustrations and most of the vocabulary come from the “Dark pool” case, where the price is not chosen by the trader (it is the market “mid point” price) and the answer of the pool is immediate (i.e. ). Dark pools are MTFs that do not publish pre-trade informations, so an efficient use of the results of the previous executions (namely the realizations of the for any and all in the past) is crucial. The results exposed here solve the problem of simultaneously splitting orders and using the information coming back from the pools to adjust the proportions to send for the next order, according to a criteria linked to the overall quantity executed ( a linear combination of the ).

The resulting trading strategy (which optimality is proven here) can be considered as an extension of the one conjectured by Almgren in [2]. It may also be related to the class of multi-armed bandit recursive learning procedures, recently brought back to light in several papers (see [14, 22], [15, 16]; which in turn belongs to the wide family of “recursive stochastic algorithms” also known as “stochastic approximation” and extensively investigated in the applied probability literature (see [13], [3], [7], etc)).

In fact, we introduce two learning algorithms one based on an optimization under constraints principle and a second algorithm based on a reinforcement principle for which we establish the existence of an equilibrium. We extensively investigate the first one, considering successively the classical – although unrealistic – case where the inputs (requests, answers) are i.i.d. and a setting in which the input only share some averaging properties. In the i.i.d. setting we establish convergence of the procedure and a Central Limit Theorem relying on classical results from Stochastic Approximation Theory. By averaging setting (also referred as ergodic setting), we mean that the inputs of the procedure has an averaging property with respect to a distribution at a given rate, say , , for a wide enough class of Borel functions. Typically, in our problem, these inputs are the successive -tuples , . Typically, if we denote this input sequence inputs by , we will assume that, for every ,

Usually, is supposed to contain at least bounded continuous function and subsequently all bounded - continuous functions. This will be enough for our purpose in this paper (Stochastic approximation in this general framework is investigate in [17]). But the key point to be noted here is that no Markov assumption is needed on this input sequence . These assumptions are hopefully light enough to be satisfied by real data since it can be seen as a kind of “light” ergodicity at a given rate. In a Markovian framework it could be related to the notion of “stability” in the literature, see [7].

Thus, this setting includes stationary -mixing processes (satisfying an Ibragimov condition) like those investigated in [6] (in [5] weaker dependence assumptions are made in the chapter devoted to stochastic approximation but the perturbation is supposed to be additive and non causal which is not at all the case in our problem). As concerns the second procedure for which no Lyapunov function seems to be (easily) made available, we establish the existence of an equilibrium and show the related to the algorithm is a competitive system in the terminology of monotonous differential systems extensively studied by Hirsch et al. (see [12]). The behaviour of such competitive systems is known to be the most challenging, even when the equilibrium point is unique (which is not the case here).

Both procedures are compared in the final section, using simulated and real data. Further numerical tests and applications are ongoing works in CA Cheuvreux.

The paper is organized as follows: in Section 2, we make precise the modeling of splitting orders among several venues in the framework of Dark pools, first in static then in a dynamic way. This leads to an optimization problem under constraints. In Section 3, we study the execution function of one dark pool and introduce the recursive stochasic algorithm resulting from the optimization problem. In Section 4 we analyze in depth this algorithm ( convergence and weak rate) when the “innovations” (data related to the orders, the executed quantities and the market price) are assumed i.i.d. In Section 5 we extend the convergence result to a more realistic framework where these innovations are supposed to share some appropriate averaging properties ( satisfied by -mixing processes satisfying Ibragimov’s condition). Section 6 is devoted to the second learning procedure, based this time on reinforcement principle, introduced in [4]. We make a connexion with the theory of (competitive) monotonous dynamical systems. Finally, in Section 7, we present several simulations results on simulated and real data to evaluate the performances of both procedures with respect to an “oracle” strategy of an “insider” who could know a priori the executed quantities by every dark pool.

Notations: For every , set , . Let .

denotes the Kronecker symbol.

denotes the canonical inner product on and the derived Euclidean norm.

denotes the interior of a subset of .

denotes the Dirac mass at .

2 A simple model for the execution of orders by dark pools

2.1 Static modelling

As mentioned in the introduction, we will focus in this paper on the splitting order problem in the case of (competing) dark pools. The execution policy of a dark pool differs from a primary market: thus a dark pool proposes bid/ask prices with no guarantee of executed quantity at the occasion of an over the counter transaction. Usually its bid price is lower than the bid price offered on the regular market (and the ask price is higher). Let us temporarily focus on a buying order sent to several dark pools. One can model the impact of the existence of dark pools () on a given transaction as follows: let be the random volume to be executed and let be the discount factor proposed by the dark pool . We will make the assumption that this discount factor is deterministic or at least known prior to the execution. Let denote the percentage of sent to the dark pool for execution and let be the quantity of securities that can be delivered (or made available) by the dark pool at price where denotes the bid price on the primary market (this is clearly an approximation since on the primary market, the order will be decomposed into slices executed at higher and higher prices following the order book). The rest of the order has to be executed on the primary market, at price . Then the cost of the executed order is given by

where , . At this stage, one may wish to minimize the mean execution cost , given the price . This amounts to solving the following (conditional) maximization problem

| (2.1) |

However, none of the agents being insiders, they do not know the price when the agent decides to buy the security and when the dark pools answer to their request. This means that one may assume that and are independent so that the maximization problem finally reads

| (2.2) |

where we assume that all the random variables , …, are integrable (otherwise the problem is meaningless).

An alternative choice could be to include the price of the security into the optimization which leads to the mean maximization problem

| (2.3) |

(with the appropriate integrability assumption to make the problem consistent). It is then convenient to include the price into both random variables and by considering and instead of and which leads again to the maximization problem (2.2).

If one considers symmetrically a selling order to be executed, the dark pool is supposed to propose a higher ask price , , than the order book. The seller aims at maximizing the execution global (mean) price of the transaction. This yields to the same formal optimization problem, this time with , .

All these considerations lead us to focus on the abstract optimal allocation problem (2.2) which explains why the price variable will no longer appear explicitly in what follows.

2.2 The dynamical aspect

In practice, there is no a priori assumption – or information available – on the joint distribution of under . So the only reasonable way to provide a procedure to solve this allocation problem is to devise an on-line learning algorithm based on historical data, namely the results of former transactions with the dark pools on this security executed in the past. This underlines that our agent dealing with the dark pools is a financial institution like a bank, a broker or possibly a large investor which often – that means at least daily – faces some large scale execution problems on the same securities.

This means that we will have to make some assumptions on the dynamics of these transactions on the data input sequence supposed to be defined on the same probability space .

Our basic assumption on the sequence is of statistical – or ergodic – nature: we ask this sequence to be -averaging ( and in ), at least on bounded continuous functions, where is a distribution on . This leads to the following formal assumption:

where denotes the weak convergence of probability measures on . For convenience, we will denote the canonical random vector on so that we can write .

Assumption on the marginal distribution of the sequence is mainly technical. In fact standard arguments from weak convergence theory show that combining and implies

( would be enough). An important subcase is the the setting

This more restrictive assumption is undoubtedly less realistic from a modeling point of view but it remains acceptable as a first approximation. It is the most common framework to apply the standard Stochastic Approximation machinery ( convergence, asymptotically normal fluctuations, etc). So, its interest may be considered at least as pedagogical. The setting is slightly more demanding in terms of assumptions and needs more specific methods of proof. It will be investigated as a second step, using some recent results established in [18] which are well suited to the specificities of our problem (in particular we will not need to assume the existence of a solution to the Poisson equation related to the procedure like in the reference book [3]).

3 Optimal allocation: a stochastic Lagrangian algorithm

3.1 The mean execution function of a dark pool

In view of the modeling section, we need to briefly describe the precise behaviour of the mean execution function of a single dark pool.

Let be an -valued random vector defined on a probability space representing the global volume to be executed and the deliverable quantity (by the dark pool) respectively. Throughout this paper we will assume the following consistency assumption

| (3.1) |

The positivity of means that we only consider true orders. The fact that is not identically means that the dark pool does exist in practice. The “rebate” coefficient is specific to the dark pool.

To define in a consistent way the mean execution function of a dark pool we only need to assume that (although more stringent integrability assumptions are made throughout the paper).

Here the mean execution function of the dark pool is defined by

| (3.2) |

where . The function is finite, non-identically . It is clearly a concave non-decreasing bounded function. Furthermore, one easily checks that its right and left derivatives are given at every by

| (3.3) |

In particular,

and if

| (3.4) |

then

Assumption (3.4) means that the distribution of has no atom except possibly at . It can be interpreted as the fact that a dark pool has no “quantized” answer to an order.

More general models of execution functions in which the rebate and the deliverable quantity may depend upon the quantity to be executed are briefly discussed further on.

3.2 Design of the stochastic Lagrangian algorithm

Let be the quantity to be executed by dark pools. For every dark pool the available quantity is defined on the same probability space as . We assume that all couples satisfy the consistency assumption (3.1).

To each dark pool is attached a (bounded concave) mean execution function of type (3.2), introduced in Section 2.1, or (8.1), (8.3) studied in Section 8.

Then for every ,

| (3.5) |

In order to design the algorithm we will need to extend the mean execution function (whatever its form is) as a concave function on the whole real line by setting

| (3.6) |

Based on the extension of the functions defined by (3.6), we can formally extend on the whole affine hyperplane spanned by

As announced, we aim at solving the following maximization problem

but we will also have to deal for algorithmic purpose with the same maximization problem when runs over .

Before stating a rigorous result, let us a have a look at a Lagrangian approach that only takes into account the affine constraint that is . Straightforward formal computations suggest that

iff is constant when runs over

or equivalently if

| (3.7) |

In fact this statement is not correct in full generality because the Lagrangian method does not provide a necessary and sufficient condition for a point to be a maximum of a (concave) function; thus, it does not take into account the case where reaches its maximum on the boundary where the above condition on the derivatives may fail. So, an additional assumption is necessary to make it true as established in the proposition below.

Proposition 3.1

Assume that the functions defined by (3.2) satisfy the following assumption

Then is a compact convex set and

Furthermore .

If the functions satisfy the slightly more stringent assumption,

then

Remarks. If , one checks that Assumption () is also necessary to derive the conclusion of item .

As a by-product of the proof below we have the following more precise result on the optimal allocation : if and , then

Interpretation and comments: In the case of a “regular” mean execution function, Assumption () is a kind of homogeneity assumption on the rebates made by the involved dark pools. If we assume that for every (all dark pools buy or sell at least one security with the announced rebate), then reads

since . In particular,

| Assumption () is always satisfied when all the ’s are equal |

(all dark pools propose the same rebates).

Assumption () is in fact our main assumption in terms of modeling. It may look somewhat difficult to satisfy when the rebates are not equal. But the crucial fact in order to preserve the generality of what follows is that it contains no assumption about the dependence between the volume and the “answers” from the dark pools.

Proof. The function is continuous on a compact set hence is not empty. Let and . Clearly so that . Let such that , . Then defined on the right neighbourhood of reaches its maximum at so that its derivative at is non-positive. Specifying the vector yields

Now if with , , then the is defined on a neighbourhood of and reaches its maximum at so that its derivative is at ; specifying the vector yields

Now, there exists at least one index such that . Hence which implies in turn that for every , . Finally Assumption implies that these inequalities hold as equalities so that

Conversely, let satisfying the above equalities. Then, for every , the function is concave on with a right derivative equal to at . So it is maximum at .

Now we pass to the the maximization over . Since it is an affine space and is concave, it is clear, by considering as a function of , that

(which is non-empty since it contains at least ). Now let . Assume there exists such that . Then there always exists an index such that . Consequently

which contradicts the equality of these two derivatives. Consequently all ’s are non-negative so that .

If holds, the above proof shows that so that .

3.3 Design of the stochastic algorithm

Now we are in position to devise the stochastic algorithm for the optimal allocation among the dark pools, taking advantage of the characterization of . In fact we will simply use the obvious remark that numbers ,…, are equal if and only if they are all equal to their arithmetic mean .

We consider the mean execution function as defined by (3.2). We assume from now on that the continuity assumption (3.4) holds so that the representation (3.3) of its derivative can be taken as its right or its left derivative on (and its right derivative only at ).

Using this representation (3.3) for all the derivatives yields that, if Assumption is satisfied, then and

However, the set is not stable for the “naive” zero search algorithm naturally derived from the above characterization, we are led to devise the procedure on the hyperplane .

Consequently, this leads to devise the following zero search procedure

| (3.8) |

where, for every , every , every and every ,

and the “innovation” is a sequence of random vectors with non negative components such that, for every , and the remainder terms have a mean-reverting effect to pull back the algorithm into . They are designed from the extension (3.6) of the derivative functions outside the unit interval ; to be precise, for every ,

3.4 Interpretation and implementability of the procedure

Implementability. The vector in (3.8) represents the dispatching of the orders among the dark pools to be sent at time by the investor. It is computed at time . On the other hand represents the volume to be executed (or its monetary value if one keeps in mind that we “plugged” the price into the volume) and the the “answer” of dark pool , still at time .

The point is that the investor does have no access to the quantities . However, he/she knows what he/she receives from dark pool , . As a consequence, the investor has access to the event

which in turn makes possible the updating of the procedure although he/she has no access to the true value of .

So, except for edge effects outside the simplex , the procedure as set can be implemented on real data.

Interpretation. As long as is a true allocation vector, lies in the simplex , the interpretation of the procedure is the following: assume first that all the factors are equal (to ). Then the dark pools which fully executed the sent orders () are rewarded proportionally to the numbers of dark pools which did not fully executed the request they received. Symmetrically, the dark pools which could not execute the whole request are penalized proportionally to the number of dark pools which satisfied the request.

Thus, if only one dark pool, say dark pool , fully executes the request at time , its pourcentage will be increased for the request at time by it will asked to execute % of the total order . The other dark pools will be penalized symmetrically: the pourcentage of the total request each of them will receive at time will be reduced by .

If dark pools totally execute their request at time and the other fail, the pourcentages of that the “successful” dark pools will receive for execution at time will be increased by , each of the “failing dark pools” being reduced by .

If no dark pool was able to satisfy their received request at time , none will be penalized and if all dark pools fully execute the received orders, none will be rewarded.

In short, the dark pools are rewarded or penalized by comparing their mutual performances. When the “attractivity” coefficents are not equal, the reasoning is the same but weighted by these attractivities.

Practical implementation. One may force the above procedure to stay in the simplex by projecting, once updated, the procedure on each time it exits the simplex. This amounts to replace the possibly negative by , the by and to renormalize the vector by dividing it by the sum of its terms.

Furhermore, to avoid that the algorithm leaves too often the simplex, one may simply normalize the step by considering the predictable step

4 The setting: convergence and

Theorem 4.1

Assume that satisfy (3.1), that and that Assumption holds. Assume furthermore that the distribution of satisfies the continuity Assumption (3.4). Let be a step sequence satisfying the usual decreasing step assumption

Let be an i.d.d. sequence defined on a probability space . Then, there exists an -valued random variable such that

If the functions satisfy then .

Proof of the theorem. In this setting, the algorithm is (non homogenous) Markov discrete time process with respect to the natural filtration with the following canonical representation

where, for every ,

is the so-called mean function of the algorithm, and

since is independent of .

One derives from Proposition 3.1 that the mean function of the algorithm satisfies and that, for every and every ,

| (4.1) |

simply because each function is non-increasing which implies that each term of the sum is non-positive. The sum is not zero otherwise as soon as which would imply .

The random vector being square integrable, it is clear that satisfies the linear growth assumption

At this stage one may conclude using a simple variant of the standard Robbins-Monro Theorem (like that established in [20]): there exists a random variable taking values in such that .

4.1 Rate of convergence

Our aim in this section is to show that the assumptions of the regular Central Limit Theorem () for stochastic approximation procedures are fulfilled. For a precise statement, we refer (among others) to [3] (Theorem 13 p.332). For the sake of simplicity, we will assume that the mean function has a single zero denoted . The following lemma provides a simple criterion to ensure this uniqueness.

Lemma 4.1

Assume that all the functions , , are decreasing (strictly). Then

Proof. In particular is satisfied so that . If , , , it follows from (4.1) that for some index such that .

The second ingredient needed to establish a will be the Hessian of function . To ensure its existence we will make one further assumption on a generic random couple , keeping in mind that , but that may possibly be positive too. Namely, assume that the distribution function of given is absolutely continuous with a probability density defined on . Furthermore we make the following assmptions on :

| (4.2) |

Note that is clearly always satisfied when and is bounded. The conditional distribution function of given and is given by

Lemma 4.2

Assume satisfies the above assumption (4.2). Then the mean execution function is concave, twice differentiable on and for every ,

If satisfies the above assumption (4.2) for every , then the function defined on by is differentiable on and admits a continuous extension on given by

Let , and let . Its kernel is one dimensional, and is bijective. Every non-zero eigenvalue (with eigenspace ) satisfies

Proof. is a straightforward application of the Lebesgue differentiation Theorem for expectation.

is a consequence of .

The transpose of has a strict dominating diagonal structure , , and for every . Consequently, it follows from Gershgorin’s Lemma (see [9]) that is an eigenvalue of order of (with 1 as an eigenvector and that all other eigenvalues have (strictly) positive real parts). Consequently is one dimensional. The fact that is obvious so that this inclusion holds as an equality by the dimension formula. Hence all the eigenvectors not in are in . Set , . Then has a dominating diagonal structure so that all its eigenvalues have non-negative real parts. Now if is an eigenvalue of , it is obvious that is an eigenvalue of . Consequently .

Theorem 4.2

Assume that the assumptions of Theorem 4.1 holds and that is reduced to a single point so that - as . Furthermore, suppose that Assumption (4.2) holds for every , and that , . Set

where denotes the eigenvalue of with the lowest real part. Then

where the asymptotic covariance matrix is given by

where

and stands for the transpose operator of .

Remark. The above claim is consistent since preserves .

Proof. First note that, since , the above Lemma 4.2 shows that (still making the confusion between the linear operator and its matrix representation in the canonical basis)

Then, Lemma 4.2 implies that has eigenvalues with positive real parts, all lower bounded by .

At this stage, one can apply the for stochastic algorithms defined on (see [3], p.341).

5 The setting: convergence

For the sake of simplicity, although it is not really necessary, we will assume throughout this section that

possibly because all the execution functions are decreasing so that, following the former Lemma 4.1.

So we assume that the sequence satisfies with a limiting distribution such that, for every , its marginal satisfies the consistency assumption (3.1) and the continuity assumption (3.4). We will also need to make a specific assumption: there exists such that

| (5.1) |

This assumption means that all allocations across the pools lying in the neihbourhood of can be executed.

On the other hand, it follows from and some standard weak convergence arguments that

since the (non-negative) functions , , are - continuous and as by (3.4). Moreover this convergence holds uniformly on compact sets with respect to since is continuous, still owing to (3.4). Our specific assumption is to require a rate in the above and -convergence. Namely, we assume that there exists an exponent such that

| (5.2) |

This assumption from the more general assumption that, for every , the marginal satisfies (3.4) and

on a subspace containing all the functions .

Note that, when the sequence is i.i.d. with distribution then elementary martingale arguments show that the whole sequence is -averaging at rate for every on (and all , , since ). So, the theorem below almost embodies the convergence theorem established in the setting (except for the integrability assumption on ).

Now we are in position to state the main convergence result of this section. We rely on the extension of Robbins-Siegmund Lemma proposed in [18]. For the reader’s convenience it is recalled in the Appendix.

Theorem 5.1

Let be a sequence of input satisfying and such that, for every , the marginal distribution satisfies the consistency assumptions (3.1) and (3.4). Suppose furthermore that, the sequence satisfies the rate assumption (5.2). If the step sequence satisfies

where , then the algorithm defined by (3.3) converges towards .

technical comment. The above condition on the step sequence is satisfied as soon as with .

Proof. Step 1. First, we aim at applying the extended Robbins-Siegmund Lemma established in [18] (see Appendix, Theorem A.1 for its statement) for stochastic algorithms with -averaging inputs dynamics in presence of a Lyapunov function. We will consider the case and . We set and and we consider the input , . Let be our candidate as a Lyapunov function.

First note that it follows from (3.3) that the function satisfies the growth assumption (A.4) since

where and .

In view of the ergodic assumption (5.2) and the fact that lies in , it is clear from its definition that for every .

At this stage it remains to check the “weak local Lyapunov” assumption (A.5) for . This fact is obvious since, for every and every input ,

where

| (5.3) |

is clearly non-increasing with respect to .

At this stage, using that , we can apply our extended Robbins-Siegmund lemma also that

| (5.4) |

Step 2. At this stage it suffices to show that is a limiting point of since converges to

Let denote a positive real number such that, for every , . One derives from (5.3) and the monotonicity of in that for every and every ,

where . As a consequence

where and the open set is defined by

Now, one derives from (5.4) that

Now Assumption (5.1) implies that . Furthermore owing to the continuity assumption so that implies

An Abel transform and the facts that the sequence is non-increasing and classically implies that

so that

In turn, this implies that

This holds of course for a sequence of real numbers decreasing to .

Let be the set of limiting values of the sequence . It is is non-empty since the sequence is bounded. Then is compact and it follows from what precedes that (and is compact). Hence a decreasing intersection of non-empty compact sets being a (non-empty) compact set . On the other hand since the algorithm is -valued. But . Consequently is a limiting point of the algorithm which implies that it is its true limit.

Application to -mixing stationary data. If is a stationary -mixing sequence which mixing coefficients satisfy Ibragimov’s condition for some :

(which is satisfied in case of geometric -mixing) then the sequence is -averaging where is the stationary marginal distribution of the sequence (supposed to satisfy (3.1) and (3.4)) at rate for every . To be precise, and

In particular, all the functions , , lie in every , , so that the rate condition (5.2) is satisfied.

As concerns the stationary assumption on the input data sequence, it can be considered as realistic if one think of execution objectives given on a daily basis.

Example: An exponential discrete time Ornstein-Ulhenbeck model for .

where , , …, are positive real numbers and the sequence satisfies the linear auto-regressive dynamics

with , , , with rank () and is an i.i.d. sequence of -distributed random variables. We assume that the sequence is stationary that the distribution of is the (Gaussian) invariant distribution (with covariance matrix solution to the Lyapunov equation where t stands for transpose). Then (see [6], p. 99), the sequence is geometrically -mixing and subsequently so is (with respect to its natural filtration). Furthermore, it is clear that its distribution satisfies the dispersion assumption (5.1) the process is a non-degenerate Gaussian distribution over since has full rank .

6 An alternative procedure based on a reinforcement principle.

Recently, inspired by the discussion developed by Almgren and Harts in [2] about liquidity estimation, Berenstein and Lehalle devised a “smart routing” recursive procedure of requests to be executed by a pool of dark pools (see [4]). This procedure is not based on the opimization of a potential function but on a intuitive reinforcement mechanism. Let be the profit induced by the execution of the order sent to dark pool at time . The proportion of the global order to be sent to dark pool for execution at time is defined as proportional to this profit by

The updating of the random vector is as follows

The first equation models the idea of “reinforcement” since the proportion of orders sent for execution to dark pool is proportional to the historical performances of this dark pool since the beginning of the procedure.

The second equation describes in a standard way – like in the optimization algorithm – the way dark pools execute orders.

Elementary computations show that the algorithm can be written directly in a recursive way in terms of a new vector valued variable

since

This is a standard form a stochastic algorithm (with step ).

Furthermore, note that setting ,

since for at least one dark pool . Consequently, as soon as the sequence is stationary and ergodic

So if we make the natural assumption that

then, , the algorithm cannot converge to .

If we make the additional assumption that the sequence is then the algorithm is a discrete time (non homogenous) -Markov process with respect to the filtration , , so that it admits the canonical representation

where and

is an -martingale increment. Furthermore it is -bounded as soon as .

In fact the specific difficulties induced by this algorithm are more in relation with its mean function

| (6.1) |

than with the martingale “disturbance term” . Our first task will be to prove under natural assumptions the existence of a non degenerate equilibrium point. Then we will show why this induces the existence of many parasitic equilibrium points.

6.1 Existence of an equilibrium

In this section, we will need to introduce a new function associated to a generic order and a generic dark pool with characteristics .

| (6.2) |

If Assumption (3.1) holds then and is continuous at . It follows from the concavity of and that is non-increasing. It is continuous as soon as is if Assumption (3.4) holds true.

Proposition 6.1

Let . Assume that Assumption (3.1) holds for every couple , .

There exists a such that

| (6.3) |

Proof. We define for every

This function maps the compact convex set into itself. Furthermore it is continuous since, on the one hand, for every , is continuous owing to the fact that satisfies and, on the other hand,

Indeed, for every ,

since - and . Then it follows from the Brouwer Theorem that the function has a fixed point . Set for every ,

It follows immediately from this definition that

which in turn implies that so that , .

For every we consider the inverse of defined on the interval . This function is decreasing continuous and . Then, let be the continuous function defined by

We know that and we derive from Assumption (6.4) that . So, owing to the (strict) monotonicity of , there exists such that . Set

Then since by definition of . If , then which is impossible.

Corollary 6.1

Assume that all the functions are continuous and decreasing. If furthermore, the rebate coefficients are equal (to ) and if for every then there exists an equilibrium point lying in .

Proof. Under the above assumptions . Consequently

Comments. Unfortunately there is no hope to prove that all the equilibrium points lie in the interior of since one may always adopt an execution strategy which boycotts a given dark pool or, more generally, dark pools. So it seems hopeless to get uniqueness of the equilibrium point. To be more precise, under the assumptions of claim of the above Proposition 6.1, there exists at least one strategy involving a subset of dark pools (one dark pool is needed at least). Elementary combinatorial arguments show that there are at least equilibrium points.

So, from a theoretical point of view, we are facing a situation where there may be many parasitic equilibrium points, some of them being clearly parasitic. However it is quite difficult to decide a priori, even if we make the unrealistic assumption that we know all the involved distributions, which equilibrium points are parasitic.

This is a typical situation encountered when dealing with procedures devised from a reinforcement principle.

However, one may reasonably hope that some of them are so-called “traps”, that means equilibrium points which are repulsive at least in one noisy direction so that the algorithm escapes from it. Another feature described below suggests that a theoretical study of the convergence behaviour of this procedure would need a specific extra work.

The next natural question is to wonder whether an equilibrium of the algorithm – namely a zero of – is (at least) a target for the algorithm is attractive for the companion , .

Proposition 6.2

Remark. In fact the following inequalities are satisfied by any equilibrium :

This follows from the convexity of the function which is zero at with positive derivative. As a consequence, the right hand side in the above sufficient condition is always positive which makes this criterion more realistic.

Proof. Elementary computations show that the differential of at is given by

As a consequence all the diagonal terms of are positive. The above condition for all the eigenvalues of to have positive real parts follows from a standard application of Gershgorin’s Lemma to the transpose of .

6.2 A competitive system

But once again, even if we could show that all equilibrium points are noisy traps, the convergence would not follow for free since this algorithm is associated to a so-called competitive system. A competitive differential system is a system in which the field is differentiable and satisfies

As concerns Almgren and Harts’s algorithm, the mean function is given by (6.1), and under the standard differentiability assumption on the functions ’s,

These systems are known to have possibly a non converging behaviour even in presence of a single (attracting) equilibrium. This is to be compared to their cooperative counterparts (with negative non-diagonal partial derivatives) whose flow converge uniformly on compact sets toward the single equilibrium in that case. This property can be transferred to the stochastic procedure by the mean if the so-called method which shows that the algorithm almost behaves like some trajectories of the Ordinary differential Equation associated to its mean field (see [13, 3, 7] for an introduction). Cooperativeness and competitiveness are in fact some criterions which ensure some generalized monotonicity properties on the flow of the viewed as a function of its space variable. For some background on cooperative and competitive systems we refer to [11, 12] and the references therein.

7 Numerical tests

The aim of this section is to compare the behaviour of both algorithms on different data sets : simulated i.i.d. data, simulated -mixing data and (pseudo-)real data.

Two natural situations of interest can be considered a priori: abundance and shortage. By “abundance” we mean (in average, the requested volume is lower than the available one). The ”shortage” setting is the reverse situation where .

In fact, in the “abundance” setting, both our procedures (optimization and reinforcement) tend to remain “frozen” at their starting allocation value (usually uniform allocation) and they do not provide a significant improvement with respect to more naive approaches. By contrast the shortage setting is by far more commonly encountered on true markets and turns out to be much more challenging for our allocation procedures, so from now on we will focus on this situation.

Our first task is to define a reference strategy. To this end, we introduce an “oracle strategy” devised by an insider who knows all the values and before making his/her optimal execution requests to the dark pools. It can be described as follows: assume for simplicity that the rebates are ordered . Then, it is clear that the “oracle” startegy yields the following cost reduction (CR) of the execution at time ,

Now, we introduce indexes to measure the performances of our recursive allocation procedures.

-

•

Relative cost reduction (w.r.t. the regular market): they are defined as the ratios between the cost reduction of the execution using dark pools and the cost resulting from an execution on the regular market for the three algorithms, , for every ,

-

Oracle:

-

Recursive “on-line” algorithms:

(with algo = opti, reinf).

-

-

•

Performances (w.r.t. the oracle): the ratios between the relative cost reductions of our allocation algorithms and that of the oracle, for every

which seems a more realistic measure of the performance of our allocation procedures since the oracle strategy cannot be beaten.

Since these relative cost reductions are strongly fluctuating (with variables and in fact), we will plot the moving average of these ratios (on the running period of interest) and express them in pourcentage.

Moreover, when we simulate the data, we have chosen simulations because it corresponds approximatively to the number of pseudo-real data observed within a day.

The choice of the gain parameter is the following (in the different settings considered below)

where equals to some units.

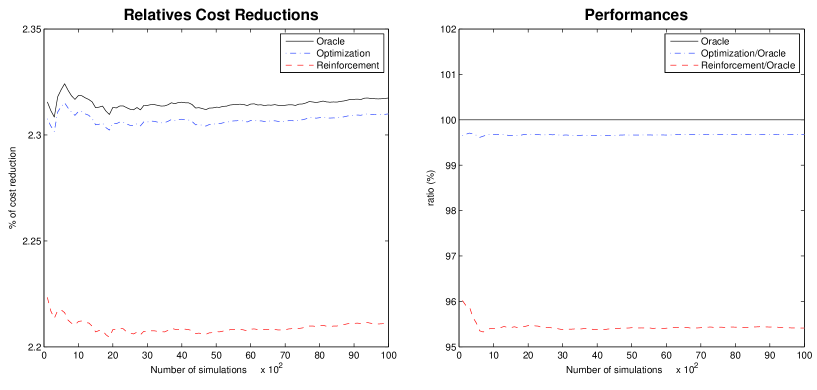

7.1 The setting

We consider here simulated data in the i.i.d. setting, where the quantity and , , are log-normal variables and . The variables and , , satisfy the assumptions of the CLT and we have the rate of convergence at least of the optimization algorithm.

The shortage setting is specified as follows:

with

The running means of the performances are computed from the very beginning for the first 100 data, and by a moving average on a window of 100 data.

The initial value for both algorithms is set at , .

As expected, the optimization procedure outperforms the reinforcement one and both procedures quickly converge (see Figure 1) with respect to the data set size. Note that the allocation coefficients (not reproduced here) generated by the two algorithms are significantly different. A more interesting feature is that the performances of the optimization procedure almost replicate those of the “oracle”. Further simulations suggest that the optimization algorithm also seems more robust when the variances of the random variables fluctuate.

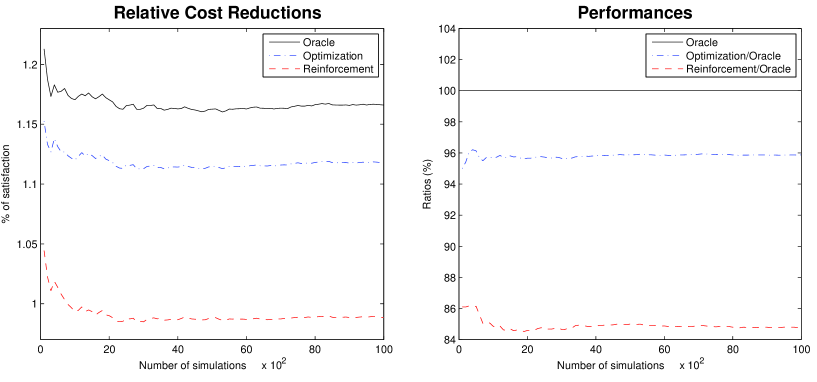

7.2 The setting

We consider here simulated data in the ergodic setting, where the quantity and , , are exponentials of an Ornstein-Uhlenbeck process,

where , and

We are still interested in the shortage situation. The initial value of the algorithms is , and we set

The running means of the performances are computed from the very beginning for the first 100 data, and by a moving average on a window of 100 data.

We observe in this ergodic setting a very similar behaviour to the i.i.d. one, with maybe a more significant advantage for the optimization approach (see Figure 2 right): the difference between the performances of both algorithms reaches 11% in favour of the optimization algorithm.

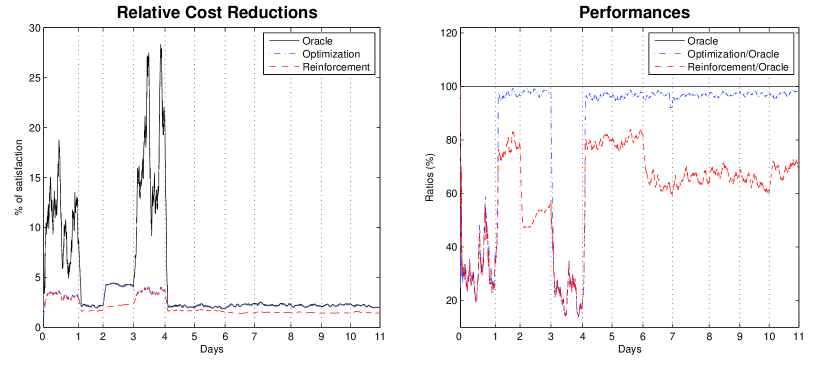

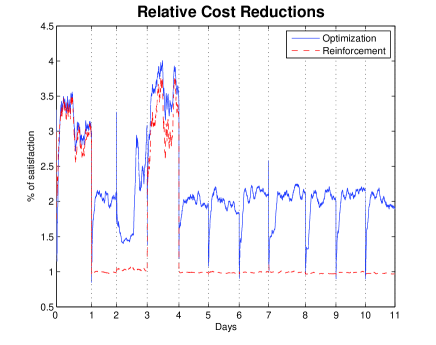

7.3 The pseudo-real data setting

Firstly we explain how the data have been created. We have considered for the traded volumes of a very liquid security – namely the asset BNP – during an day period. Then we selected the most correlated assets (in terms of traded volumes) with the original asset. These assets are denoted , and we considered their traded volumes during the same 11 day period. Finally, the available volumes of each dark pool have been modelled as follows using the mixing function

where are the mixing coefficients, some scaling parameters and and stand for the empirical mean of the data sets of and .

The shortage situation corresponds to since it implies .

The simulations presented here have been made with four dark pools (). Since the data used here covers days and it is clear that unlike the simulated data, these pseudo-real data are not stationary: in particular they are subject to daily changes of trend and volatility (at least). To highlight this resulting changes in the response of the algorithms, we have specified the days by drawing vertical doted lines. The dark pool pseudo-data parameters are set to

and the dark pool trading (rebate) parameters are set to

The mean and variance characteristics of the data sets of and , are the following:

| Mean | 955.42 | 95.54 | 191.08 | 286.63 | 191.08 |

|---|---|---|---|---|---|

| Variance |

Firstly, we benchmarked both algorithms on the whole data set ( days) as though it were stationary without any resetting (step, starting allocation, etc.). In particular, the running means of the performances are computed from the very beginning for the first 1500 data, and by a moving average on a window of 1500 data. As a second step, we proceed on a daily basis by resetting the parameters of both algorithms (the initial profit for the reinforcement algorithm ( , ) and the step parameter of the optimization procedure) at the beginning of every day. The performances of both algorithms are computed on each day.

Long-term optimization

We observe that, except for the first and the fourth days where they behave similarly, the optimization algorithm is more performing than the reinforcement one. Its performance is approximately 30 % higher on average (see Figure 3).

This test confirms that the statistical features of the data are strongly varying from one day to another (see Figure 3), so there is no hope that our procedures converge in standard sense on a long term period. Consequently, it is necessary to switch to a short term monitoring by resetting the parameters of the algorithms on a daily basis as detailed below.

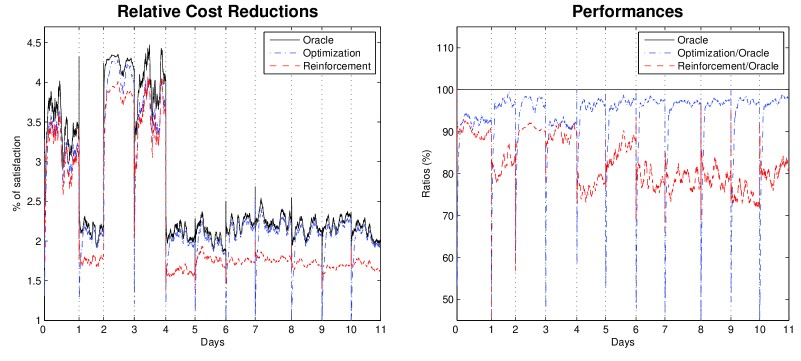

Daily resetting of the procedure

We consider now that we reset each day all the parameters of the algorithm, namely we reset the step at the beginning of each day and the satisfaction parameters and we keep the allocation coefficients of the precedent day. We obtains the following results

We observe (see Figure 4) that the optimization algoritm still significantly outperforms the reinforcement one, reaching more of the performance of the oracle. Furthermore, although not represented here, the allocation coefficients look more stable.

8 Provisional remarks

8.1 Toward more general mean execution functions

One natural idea is to take into account that the rebate may depend on the quantity sent to be executed by the dark pool. The mean execution function of the dark pool can be modeled by

| (8.1) |

where the rebate function is a non-negative, bounded, non-decreasing right differentiable function.

For the sake of simplicity, we assume that satisfies (3.4). The right derivative of reads

| (8.2) |

with in particular as above. The main gap is to specify the function so that remains concave which is the key assumption to apply the convergence theorem. Unfortunately the choice for turns out to strongly depend on the (unknown) distribution of the random variable . Let us briefly consider the case where and are independent and has an exponential distribution .

First note that the function defined by is given by

so that, owing to the independence of and ,

At this stage, will be concave as soon as the function is so. Among all possible choices, elementary computations show that a class of possible choices is to consider with . Of course this may appear as not very realistic since the rebate function is a structural feature of the different dark pools.

However several numerical experiments not reproduced here testify that both algorithms are robust to a realistic choice for the function a non-decreasing and stepwise constant.

Another natural extension is to model the fact that the dark pool may take into account the volume to decide which quantity will really executed rather than simply the a priori deliverable quantity . One reason for such a behaviour is that the dark pool may wish to preserve the possibility of future transactions with other clients.

One way to model this phenomenon is to introduce a delivery function , non-decreasing and concave w.r.t. its first variable and satisfying , so that the new mean execution function is as follows:

| (8.3) |

It is clear that the function is concave (as the minimum of two concave functions) and bounded. In this case, the first (right) derivative of reads

| (8.4) |

where denotes the right derivative with respect to . In particular .

As concerns the implementations resulting from these new execution functions, the adaptation is straightforward. Note for the optimization procedure under constraints that, firstly, the “edge” functions functions are not impacted by the type of the execution function. On the other hand the definition of the functions or the updating of the variables for the reinforcement procedure should be adapted in accordance with the representations (8.2) and (8.4) of the new mean execution function .

Example: We consider for modelling the quantity delivered by the dark pool a function where we can define a minimal quantity required to begin to consum , namely

where is a parameter of the dark pool assumed to be deterministic.

Pseudo-real data setting

8.2 Optimization reinforcement ?

For practical implementation what conclusions can be drawn from our investigations on both procedures. Both reach quickly a stabilization/convergence phase close to optimality. The reinforcement algorithm leaves the simplex structurally stable which means the proposed dispatching at each time step is realistic whereas the stochastic Lagrangian algorithm in its present form sometimes needs to be corrected from time to time. This can be corrected by adding a projection on the simplex at each step. We did not consider this variant from a theoretical point of view to keep our convergence proofs more elementary.

In a high volatility context, the stochastic Lagrangian algorithm clearly prevails with performances that turn out to be significantly better. This optimization procedure also relies on established convergence results in a rather general framework (stationary -mixing input data). However, given the computational cost of these procedures which is close to zero, a possible strategy is to implement them in parallel to get a synergistic effect. In particular, one may the reinforcement algorithm – which step parameter is structurally fixed equal to – can be used to help tuning the constant in the gain parameter of the stochastic Lagrangian. Doing so one may start with a small constant , preventing a variance explosion of the procedure. Then based one may increase slowly this constant until the Lagragian outperforms the reinforcement procedure.

References

- [1] Almgren, R. F. and Chriss N. (2000). Optimal execution of portfolio transactions. Journal of Risk, 3(2):5-39.

- [2] Almgren R. and Harts B. (2008). A dynamic algorithm for smart order routing. Technical report, StreamBase.

- [3] Benveniste M., Métivier M., Priouret P. (1987). Adaptive Algorithms and Stochastic Approximations, Springer Verlag, Berlin, 365p.

- [4] Berenstein R. (2008). Algorithmes stochastiques, microstructure et exécution d’ordres, Master 2 internship report (Quantitative Research, Dir. C.-A. Lehalle, CA Cheuvreux), Probabilités & Finance, UPMC-École Polytechnique.

- [5] Dedecker J., Doukhan P., Lang G., León J.R., Louhichi S., Prieur C. (2007). Weak dependence (with Examples and Apllications), Lecture notes in Statistcs, 190, Springer, Berlin, 317p.

- [6] Doukhan P. (1991). Mixing: Properties and Examples, Lect. Notes Statist. 85, Springer, New York, 142p.

- [7] Duflo M. (1997). Random Iterative Models. Series: Stochastic Modelling and Applied Probability, Vol. 34. XVI, 385 p., Springer, Berlin.

- [8] Foucault, T. and Menkveld, A. J. (2006). Competition for order flow and smart order routing systems, Journal of Finance, 63(1):119-158.

- [9] Gantmacher F. R. (1959). The theory of matrices, 1-2, Chelsea, New York, 374p.

- [10] Gál I.S. and Koksma J.F. (1950). Sur l’ordre de grandeur des fonctions sommables, Indigtiones Math., 12:192-207.

- [11] Hirsch M., Smith H. (2004). Monotone Dynamical systems, monography, 136p.

- [12] Hirsch M., Smith H. (2005). Monotone Dynamical systems, Handbook of differential equations: ordinary differential equations. Vol. II, Elsevier B. V., Amsterdam, 2005, 239-357.

- [13] Kushner H.J., Yin G.G. (1997). Stochastic approximation and recursive algorithms and applications, New York, Springer, 496p; and edition, 2003.

- [14] Lamberton D., Pagès G., Tarrès P. (2004). When can the two-armed bandit algorithm be trusted? The Annals of Applied Probability, 14(3):1424-1454.

- [15] Lamberton D., Pagès G. (2008). How fast is the bandit? Stoch. Anal. and Appl., 26:603-623.

- [16] Lamberton D., Pagès G. (2008) A penalized bandit algorithm, EJP, 13:341-373.

- [17] Laruelle S., PhD Thesis, in progress.

- [18] Laruelle S., Pagès G. (2009). Stochastic Approximation with Ergodic Innovation, in progress.

- [19] Lehalle C.-A. (2009). Rigorous strategic trading: Balanced portfolio and mean-reversion. The Journal of Trading, 4(3):40-46.

- [20] Lemaire V., Pagès G. (2008). Unconstrained recursive importance sampling, pre-pub LPMA 1231, to appear in Annals of Applied Probability.

- [21] Pagès G. (2001). Sur quelques algorithmes récursifs pour les probabilités numériques, ESAIM P&S, 5:141-170.

- [22] Tarrès P. (2001). Traps of stochastic algorithms and vertex-reinforced random walks, thèse d’Université, ENS Cachan, 180p.

Appendix

Appendix A Robbins-Zygmund with averaging innovation

We consider an algorithm of the following form

| (A.1) |

where is a Borel function from to , is a sequence of -valued random vectors adapted to a filtration , is an -measurable -valued random vector independent of , all defined on the same probability space , is a sequence of -martingale increments and is a non-increasing sequence of positive real numbers going to as goes to infinity.

We will say that is -averaging (under ) on a class of functions if, for every ,

| (A.2) |

Let , let . We denote by the class of functions whose convergence rate in (A.2) and in is , namely

| (A.3) |

Now we are in a position to state the convergence theorem.

Theorem A.1 (A Robbins-Zygmund like Lemma) Let be a Borel function, let be an -adapted -averaging sequence of -valued random vectors and let be a sequence of -martingale increments. Assume that there exists a continuously differentiable function satisfying

| (A.4) |

such that the function satisfies the following local weak mean-reverting assumption:

| (A.5) |

Suppose there exists , such that

| (A.6) |

Moreover, assume that satisfies the following linear growth assumption

| (A.7) |

and

| (A.8) |

where the function satisfies (convention ).

Let be a non-negative, non-increasing sequence of gain parameters satisfying

| (A.9) |

Assume that is -adapted and , -. Then, the recursive procedure defined by (A.1) satisfies