Feedback and efficiency in limit order markets

Abstract

A consistency criterion for price impact functions in limit order markets is proposed that prohibits chain arbitrage exploitation. Both the bid-ask spread and the feedback of sequential market orders of the same kind onto both sides of the order book are essential to ensure consistency at the smallest time scale. All the stocks investigated in Paris Stock Exchange have consistent price impact functions.

keywords:

Limit order markets, efficiency, arbitrage, feedback, data analysis, econophysicsPACS:

89.20.-a, 89.65.Gh, 89.75.-k1 Introduction

Mainstream finance and mathematical finance suppose that the price dynamics follows a random walk [1, 5]. This is an extreme point of view describing an average idealised behaviour that does not account for every detail of the microscopic price dynamics. And indeed extreme assumptions are most useful in a theoretical framework. This is why the opposite one is worth considering [4]: suppose that trader is active at time ; he buys/sells a given amount of shares , leading to (log-)price change , where is in transaction time, being the -th transaction. In addition, one also assumes that trader has perfect information about and and exploits it accordingly.

A related situation is found in Ref. [6] whose main result is that a arbitrage opportunity, when exploited, does not disappear but is spread around . It is a counter-intuitive outcome, that raises two questions: how to accommodate the never-disappearing arbitrage, and how microscopic arbitrage removal is possible at all at this time scale. This proceeding, a short version of Ref. [4], suggests that real markets remove arbitrage on a single transaction basis by a double feedback of the last transactions on the order book.

The price impact function is by definition the relative price change caused by a transaction of (integer) shares ( for buying, for selling); mathematically,

| (1) |

where is the log-price and is in transaction time. The above notation misleadingly suggests that does not depend on time. In reality, is not only subject to random fluctuations (which will be neglected here), but also, for instance, to feed-back from the type of market orders which has a long memory (see e.g. [3, 8, 2, 7] for discussions about the dynamical nature of market impact). Neglecting the dynamics of requires us to consider specific shapes for that enforce some properties of price impact for each transaction, whereas in reality they only hold on average. For example, one should restrict oneself to the class of functions that makes it impossible to obtain round-trip positive gains [6]. But the inappropriateness of constant price impact functions is all the more obvious as soon as one considers how price predictability is removed by speculation, which is inter-temporal by nature.

The most intuitive (but wrong) view of market inefficiency is to regard price predictability as a scalar deviation from the unpredictable case: if there were a relative price deviation caused by a transaction of shares at some time , according to this view, one should exchange shares so as to cancel perfectly this anomaly, where is such that . This view amounts to regarding predictability as something that can be remedied with a single trade. However, the people that would try and cancel would not gain anything by doing it unless they are market makers who try to stabilise the price.

It is most instructive to understand how constant price impact functions are paradoxical by considering a simple example. Trader , a perfectly (and possibly illegally) informed speculator, will take advantage of his knowledge by opening a position at time and closing it at time . It is important to be aware that if one places an order at time , the transaction takes place at price . Provided that trader buys/sells shares irrespective of the price that he obtains, the round-trip of trader yields a monetary gain of

where is the log-price before any trader considered here makes a transaction. Since generally increases with , there is an optimal number of shares that maximises . The discussion so far is a simplification, in real-money instead of log-money space, of the one found in Ref. [6]. One should note that far from diminishing price predictability, the intervention of trader increases the fluctuations. Therefore, in the framework of constant price impact functions, an isolated arbitrage opportunity never vanishes but becomes less and less exploitable because of the fluctuations, thus the reduction, of signal-to-noise ratio caused by the speculators.

It seems that trader cannot achieve a better gain than by holding shares at time . Since the actions of trader do not modify in any way the arbitrage opportunity between and , he can inform a fully trusted friend, trader , of the gain opportunity on the condition that the latter opens his position before and closes it after so as to avoid modifying the relative gain of trader .111If trader were not a good friend, trader could in principle ask trader to open his position after him and to close it after him, thus earning more. But relationships with real friends are supposed to egalitarian in this paper. For instance, trader informs trader when he has opened his position and trader tells trader when he has closed his position. From the point of view of trader , this is very reasonable because the resulting action of trader is to leave the arbitrage opportunity unchanged to since . Trader will consequently buy shares at time and sell them at time , earning the same return as trader . This can go on until trader has no fully trusted friend. Note that the advantage of trader is that he holds a position over a smaller time interval, thereby increasing his return rate; in addition, since trader increases the opening price of trader , the absolute monetary gain of trader actually increases provided that he has enough capital to invest. Before explaining why this situation is paradoxical, it makes sense to emphasise that the gains of traders are of course obtained at the expense of trader , and that the result the particular order of the traders’ actions is to create a bubble which peaks at time .

The paradox is the following: if trader is alone, the best return that can be extracted from his perfect knowledge is according to the above reasoning. When there are traders in the ring of trust, the total return extracted is times the optimal gain of a single trader. Now, assume that trader has two brokering accounts; he can use each of his accounts, respecting the order in which to open and close his positions, effectively earning the optimal return on each of his accounts. The paradox is that his actions would be completely equivalent to investing and then from the same account. In particular, in the case of , this seems a priori exactly similar to grouping the two transactions into , but this results of course in a return smaller than the optimal return for a doubled investment. Hence, in this framework, trader can earn as much as pleases provided that he splits his investment into sub-parts of shares whatever is, as long as it is constant.

This paradox seems too good to be present in real markets. As a consequence, one should rather consider its impossibility as an a contrario consistency criterion for price impact functions. Let us introduce the two relevant mechanisms that are at work in real markets.

Half of the solution lies in the dynamics of the order book, particularly the reaction of the order book to a sequence of market orders of the same kind. Generically, the impact of a second market order of the same kind and size is smaller by a factor than that of the first one, and similarly by a factor for a third one, etc [9, 7]. To this contraction of market impact on one side also corresponds an increase of market impact on the other side for the next market order of opposite type [9]; therefore, we shall assume that the impact function on the other side is divided by after the first market order, by after the second, etc. As shown in the next section, is a very good approximation when and are averaged over all the stocks, hence we shall only use ; for the same reason, we assume that .

2 Feedback

In order to investigate whether the feedback restricted on the side on which the first sequential market orders are placed is enough to make price impact consistent, one sets . In the case of price impact functions, the optimal number of shares and gain of trader are

| (2) |

and

| (3) |

These two equations already show that the reaction of the limit order book reduces the gain opportunity of player . Adding trader will reduce further the impact of trader , hence the gain of trader , and, as before, trader should pay for it. In this case, the reduction of gain of trader is

| (4) | |||||

while the gain that trader optimises is

| (5) |

Trader ’s impact functions are when he opens his position and when he closes it, which is an additional cause of loss for trader , which must be also compensated for by trader . Fortunately for the latter, his impact functions are when opening and when closing his position. Therefore, provided that is large enough so as not to make too small, trader can earn more than trader in some circumstances. Impact functions are inconsistent when , and for impact functions. It turns out that the regions in which while are disjoint if for impact functions.

As previously mentioned, the feedback acts on both order book sides. Assuming that in order to be able to use available market measurements, one finds a critical value of of about for price impact functions. For this value, only a small area of inconsistent impact functions, corresponding to , still exists in the plane, but cannot be reached since both and are outside of the inconsistent region. Therefore, even double feedback does not guarantee consistency

3 Empirical data

The values of and can be measured in real markets. The response function is the average price change after trades, conditional on the sign of the trade and on volume ; similarly, one defines the response function conditional on two trades of the same sign , and . A key finding of Refs [3, 2] is that factorises into . Thus we will be interested in , and .

Using measures kindly provided by J.-Ph. Bouchaud and J. Kockelkoren, one finds that the estimate of this ratio , that the average over all stocks and , while . ; for a given stock, there is some correlation between and ; the data presented here does not contain error bars for the measures of , and . The approximation is reasonable, and we shall from now on call and replace and by everywhere.

In other words there is some variations between the stocks, some of them being less sensitive to successive market orders of the same kind. The values of estimated start at . Therefore, even feedback on both book sides does not yield consistent impact functions. One concludes that the feedback of the order book is not enough to make price impact functions consistent.

4 Spread

The above discussion neglects the bid-ask spread . It is of great importance in practice, as the impact of one trade is on average of the same order of magnitude as the spread [9]. This means that must be large enough in order to make the knowledge of trader valuable. It is easy to convince oneself that it is enough to replace by in the relevant equations, and multiply all the gains by . For example, the optimal number of shares that trader invests if trader has infinite capital is

| (6) |

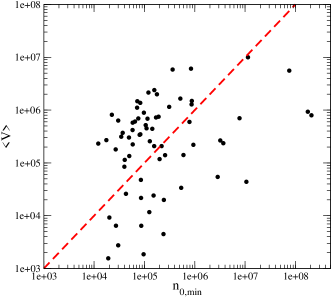

From this equation one sees that . Since in practice, the minimal amount of shares needed to create an arbitrage, denoted by is increased about 20,000 folds by the spread. The respective values of and are not independent, and can be measured in real markets for a given stock. In the language of [3], where is the average of the logarithm of transaction size and is the response function after one time step. Using and measured in Paris Stock Exchange one finds that , with median of (Fig. 1), which is not unrealistic for very liquid stocks. Indeed, the fraction of with respect to the average daily volume of each stock ranges from to more than , with a median of about . Therefore, for most of the stocks, trader needs to trade less than two fifths of the daily average volume in one transaction in order to be leave an exploitable arbitrage; for 12 stocks (), trading less than of the average daily volume suffices. It is unlikely that a single trade is larger than the average daily volume, hence, 29 stocks () do not allow on average a single large trade to be exploitable by a simple round-trip. Interestingly, stocks with average daily volumes smaller than about are all consistent from that point of view (Fig. 1). In addition, the stocks for which all have a .

Therefore, the role of the spread is to increase considerably the minimum size of the trade, which in some cases remain within reasonable bounds. The mathematical discussions of the previous sections on price impact functions are therefore still valid, provided that one replaces with , which is equivalent to rescaling by . Therefore, the spread must be taken into account, but does not yield systematically consistent impact functions for some stocks with a high enough daily volume.

5 Spread and feedback

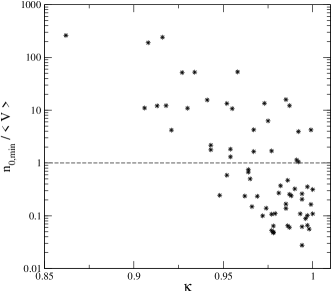

The question is whether the feedback and the spread make impact function systematically consistent. The stocks that are the most likely to become consistent are those whose is large while having a strong feedback. According to Fig. 2, these properties are compatible.

Using for each stock , , and from the data, we find that three additional stocks are made consistent by feedback on trader ’s market order side alone: the feedback limited to one side of the order book, even when the spread is taken into account, is insufficient. However, adding finally the feedback on both book sides makes consistent all the stocks, even in the case of infinite capital. Therefore, both the spread and the feedback are crucial ingredients of consistency at the smallest time scale.

6 Conclusion

The paradox proposed in this paper provides an a contrario simple and necessary condition of consistency for price impact functions. And indeed, financial markets ensure consistent market price impact functions at the most microscopic dynamical level by two essential ingredients: the spread and the dynamics of the order book.

I am indebted to Jean-Philippe Bouchaud, Julien Kockelkoren and Michele Vettorazzo from CFM for their hospitality, measurements, and comments. It is a pleasure to acknowledge discussions and comments from Doyne Farmer, Sam Howison, Matteo Marsili, Sorin Solomon and David Brée.

References

- [1] Louis Bachelier. Théorie de la Spéculation, volume 3 of Annales Scientifiques de l’Ecole Normale Superieure, pages 21–86. 1900.

- [2] J. P. Bouchaud, J. Kockelkoren, and M. Potters. Random walks, liquidity molasses and critical response in financial markets. Quant. Fin., 6:115–123, 2006.

- [3] Jean-Philippe Bouchaud, Yuval Gefen, Marc Potters, and Matthieu Wyart. Fluctuations and response in financial markets: the subtle nature of ‘random’ price changes. Quant. Fin., 4:176, 2004.

- [4] Damien Challet. So you are about to make money in financial markets. should you tell you friends how? submitted to Applied Mathematical Finance, 2007.

- [5] E. F. Fama. Efficient capital markets: a review of theory and empirical work. J. of Fin., 25:383–417, 1970.

- [6] J. D. Farmer. Market force, ecology and evolution. Technical Report 98-12-117, Santa Fe Institute, 1999.

- [7] J. Doyne Farmer, Austin Gerig, Fabrizio Lillo, and Szabolcs Mike. Market efficiency and the long-memory of supply and demand: Is price impact variable and permanent or fixed and temporary? 2007.

- [8] F. Lillo and J. D. Farmer. The long memory of efficient markets. Non-lin. Dyn. and Econometric, 8, 2004.

- [9] Matthieu Wyart, Jean-Philippe Bouchaud, Julien Kockelkoren, Marc Potters, and Michele Vettorazzo. Relation between bid-ask spread, impact and volatility in double auction markets. 2006.